Pegasystems (NASDAQ:PEGA) Beats Expectations in Strong Q3, Gross Margin Improves

Radek Strnad /

October 25, 2023

Enterprise workflow software provider Pegasystems (NASDAQ:PEGA) reported results ahead of analysts' expectations in Q3 FY2023, with revenue up 23.6% year on year to $334.6 million. Turning to EPS, Pegasystems made a GAAP loss of $0.09 per share, improving from its loss of $1.14 per share in the same quarter last year.

Is now the time to buy Pegasystems? Find out in our full research report.

Pegasystems (PEGA) Q3 FY2023 Highlights:

- Revenue: $334.6 million vs analyst estimates of $296.8 million (12.8% beat)

- EPS (non-GAAP): $0.44 vs analyst estimates of $0.01 ($0.43 beat)

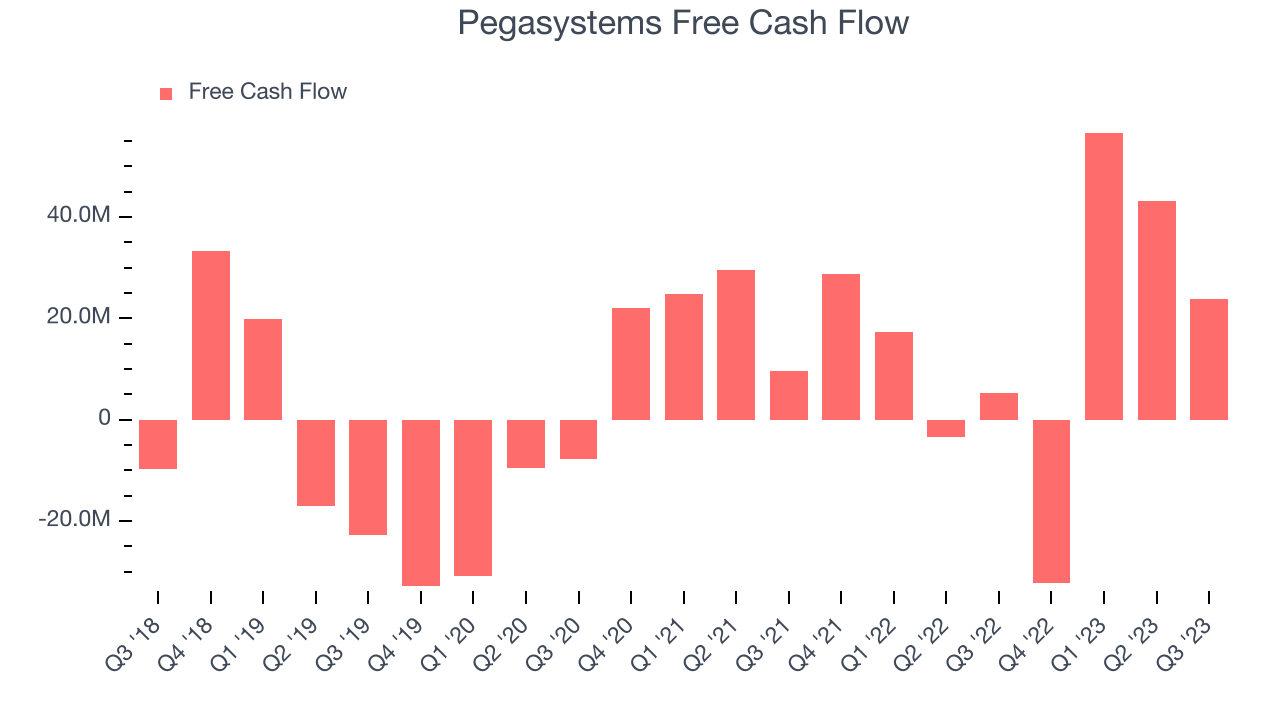

- Free Cash Flow of $23.8 million, down 44.8% from the previous quarter

- Gross Margin (GAAP): 72%, up from 65.6% in the same quarter last year

"In Q3, we launched Pega Infinity '23, with highly advanced and practical GenAI capabilities," said Alan Trefler, Founder and CEO.

Founded by Alan Trefler in 1983, Pegasystems (NASDAQ:PEGA) offers a software-as-a-service platform to automate and optimize workflows in customer service and engagement.

Automation Software

The whole purpose of software is to automate tasks to increase productivity. Today, innovative new software techniques, often involving AI and machine learning, are finally allowing automation that has graduated from simple one- or two-step workflows to more complex processes integral to enterprises. The result is surging demand for modern automation software.

Sales Growth

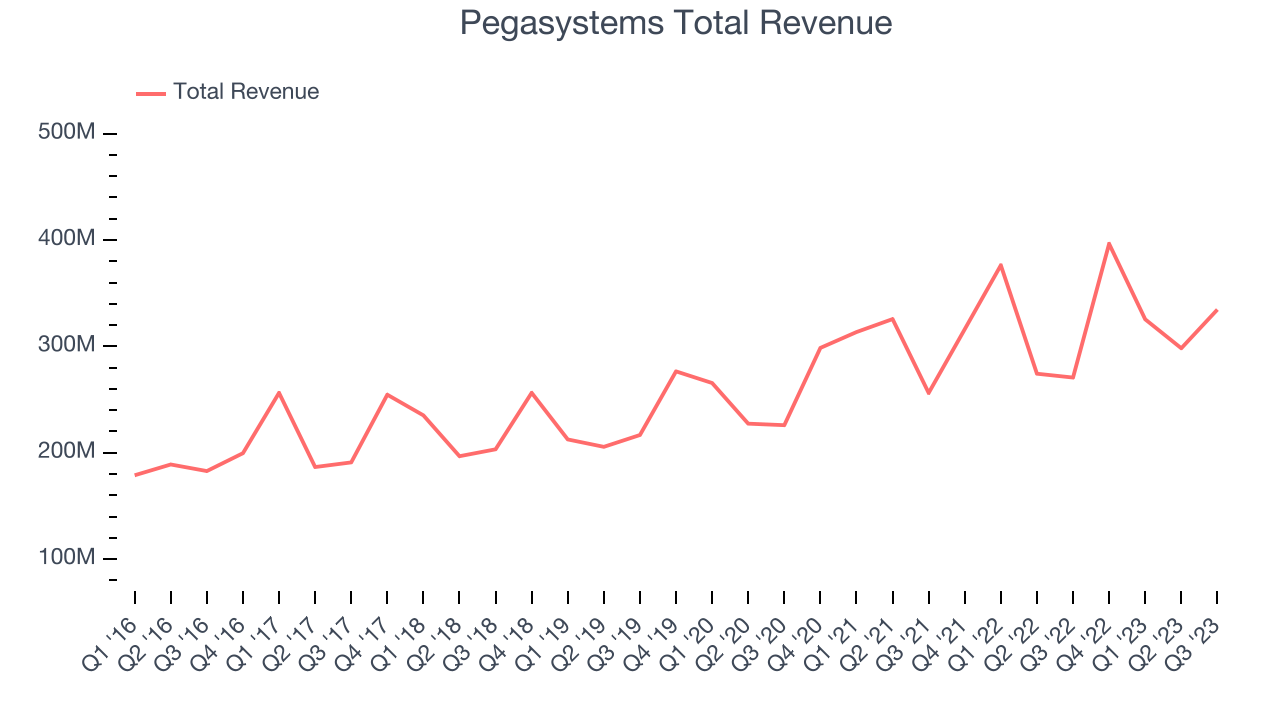

As you can see below, Pegasystems's revenue growth has been unimpressive over the last two years, growing from $256.3 million in Q3 FY2021 to $334.6 million this quarter.

This quarter, Pegasystems's quarterly revenue was up a very solid 23.6% year on year, above the company's historical trend. On top of that, its revenue increased $36.4 million quarter on quarter, a strong improvement from the $27.2 million decrease in Q2 2023. This is a sign of re-acceleration of growth and very nice to see indeed.

Looking ahead, analysts covering the company were expecting sales to grow 7.59% over the next 12 months before the earnings results announcement.

The pandemic fundamentally changed several consumer habits. There is a founder-led company that is massively benefiting from this shift. The business has grown astonishingly fast, with 40%+ free cash flow margins. Its fundamentals are undoubtedly best-in-class. Still, the total addressable market is so big that the company has room to grow many times in size. See it here.

Cash Is King

If you've followed StockStory for a while, you know that we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills. Pegasystems's free cash flow came in at $23.8 million in Q3, up 350% year on year.

Pegasystems has generated $91.5 million in free cash flow over the last 12 months, a decent 7.73% of revenue. This FCF margin stems from its asset-lite business model and gives it a decent amount of cash to reinvest in its business.

Key Takeaways from Pegasystems's Q3 Results

Sporting a market capitalization of $3.25 billion, Pegasystems is among smaller companies, but its more than $336.3 million in cash on hand and positive free cash flow over the last 12 months puts it in an attractive position to invest in growth.

We liked seeing that the company beat Wall Street's estimates for revenue and EPS. The devil is in the details, however, and what drove the revenue beat was actually license revenue, which is less exciting than a subscription revenue beat. Additionally to temper excitement, ACV (annual contract value) slightly missed. Zooming out, we think this was still a good quarter that should have shareholders pleased. The stock is up 1.24% after reporting and currently trades at $38.5 per share.

Pegasystems may have had a good quarter, but does that mean you should invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.

The author has no position in any of the stocks mentioned in this report.