PubMatic (NASDAQ:PUBM) Reports Sales Below Analyst Estimates In Q2 Earnings, Stock Drops 24%

Radek Strnad /

August 8, 2024

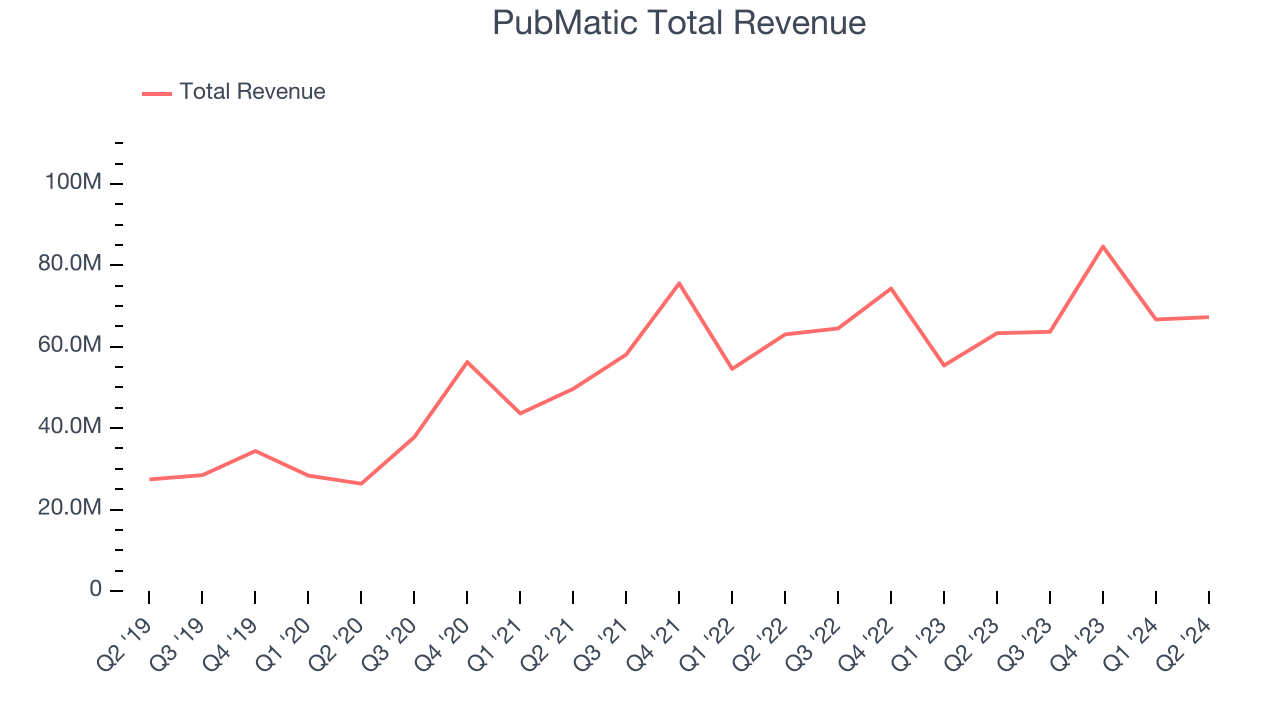

Programmatic advertising platform Pubmatic (NASDAQ: PUBM) fell short of analysts' expectations in Q2 CY2024, with revenue up 6.2% year on year to $67.27 million. Next quarter's revenue guidance of $66 million also underwhelmed, coming in 4.4% below analysts' estimates. It made a non-GAAP profit of $0.17 per share, improving from its loss of $0.11 per share in the same quarter last year.

Is now the time to buy PubMatic? Find out in our full research report.

PubMatic (PUBM) Q2 CY2024 Highlights:

- Revenue: $67.27 million vs analyst estimates of $70.11 million (4.1% miss)

- EPS (non-GAAP): $0.17 vs analyst estimates of $0.13 (33.3% beat)

- Revenue Guidance for Q3 CY2024 is $66 million at the midpoint, below analyst estimates of $69.03 million

- The company dropped its revenue guidance for the full year from $300 million to $290 million at the midpoint, a 3.3% decrease

- Gross Margin (GAAP): 62.6%, up from 60.4% in the same quarter last year

- Free Cash Flow of $6.91 million, down 57.5% from the previous quarter

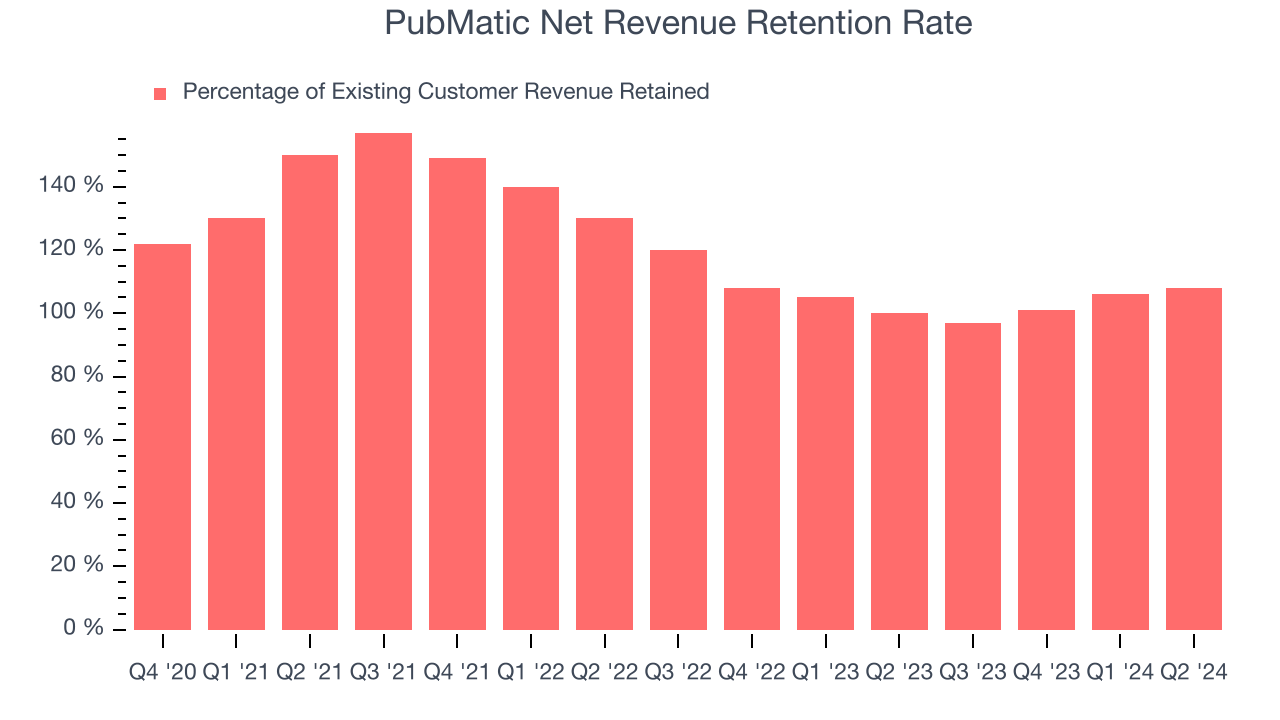

- Net Revenue Retention Rate: 108%, up from 106% in the previous quarter

- Market Capitalization: $946.7 million

“We delivered growth in key secular areas of the business with revenue from omnichannel video, which includes CTV, up 19% year-over-year and mobile app up over 20%. Ad buying activity on PubMatic continued to grow as well, with monetized impressions up 12% over last year and supply path optimization activity representing over 50% for the first time.” said Rajeev Goel, co-founder and CEO at PubMatic.

Founded in 2006 as an online ad platform helping ad sellers, Pubmatic (NASDAQ: PUBM) is a fully integrated cloud-based programmatic advertising platform.

Advertising Software

The digital advertising market is large, growing, and becoming more diverse, both in terms of audiences and media. As a result, there is a growing need for software that enables advertisers to use data to automate and optimize ad placements.

Sales Growth

As you can see below, PubMatic's 14.6% annualized revenue growth over the last three years has been sluggish, and its sales came in at $67.27 million this quarter.

PubMatic's quarterly revenue was only up 6.2% year on year, which might disappoint some shareholders. However, its revenue increased $566,000 quarter on quarter, a strong improvement from the $17.9 million decrease in Q1 CY2024. This is a sign of acceleration of growth and very nice to see indeed.

Next quarter's guidance suggests that PubMatic is expecting revenue to grow 3.6% year on year to $66 million, improving on the 1.3% year-on-year decline it recorded in the same quarter last year. Looking ahead, analysts covering the company were expecting sales to grow 10.9% over the next 12 months before the earnings results announcement.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Product Success

One of the best parts about the software-as-a-service business model (and a reason why SaaS companies trade at such high valuation multiples) is that customers typically spend more on a company's products and services over time.

PubMatic's net revenue retention rate, a key performance metric measuring how much money existing customers from a year ago are spending today, was 108% in Q2. This means that even if PubMatic didn't win any new customers over the last 12 months, it would've grown its revenue by 8%.

Significantly up from the last quarter, PubMatic has a decent net retention rate, showing us that its customers not only tend to stick around but also get increasing value from its software over time.

Key Takeaways from PubMatic's Q2 Results

It was great to see PubMatic improve its net revenue retention this quarter. We were also glad its gross margin improved. On the other hand, it lowered its full-year revenue and EBITDA guidance significantly. Overall, this was a weaker quarter for PubMatic. The stock traded down 24% to $14.90 immediately after reporting.

PubMatic may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.