Sleep Number (NASDAQ:SNBR) Misses Q3 Revenue Estimates

Jabin Bastian /

November 7, 2023

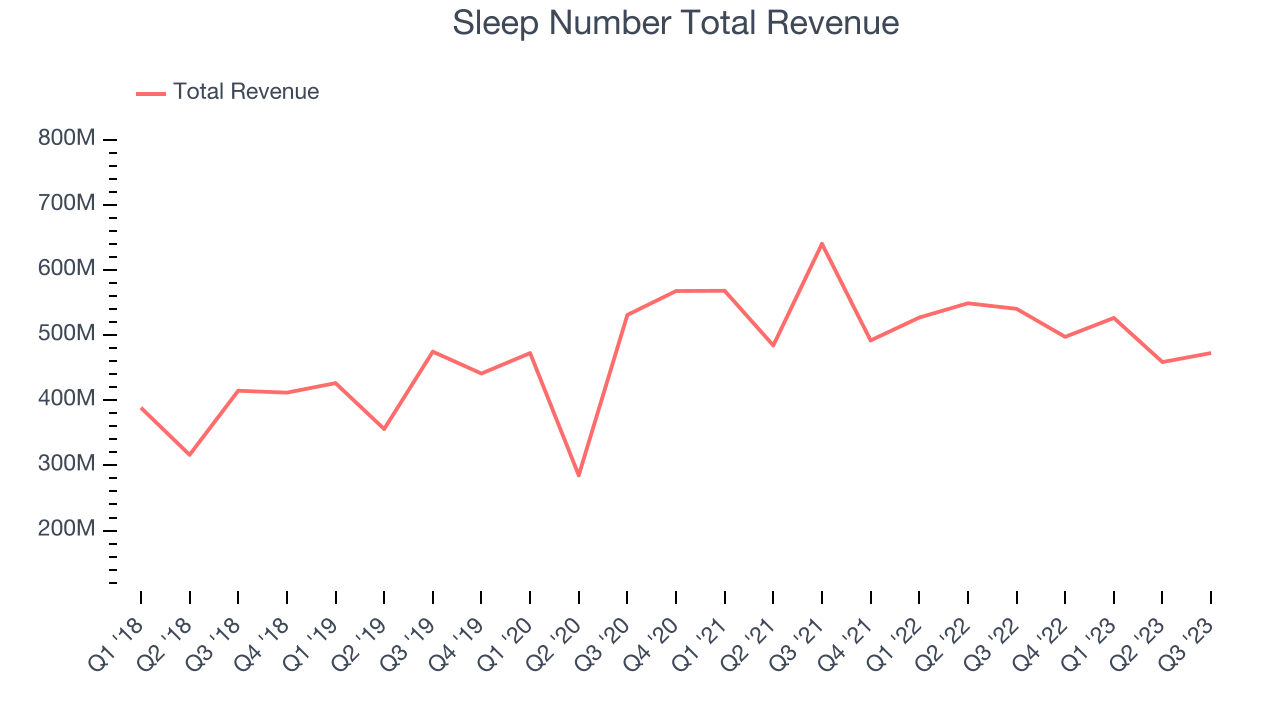

Bedding manufacturer and retailer Sleep Number (NASDAQ:SNBR) missed analysts' expectations in Q3 FY2023, with revenue down 12.6% year on year to $472.6 million. Turning to EPS, Sleep Number made a GAAP loss of $0.10 per share, down from its profit of $0.22 per share in the same quarter last year.

Is now the time to buy Sleep Number? Find out in our full research report.

Sleep Number (SNBR) Q3 FY2023 Highlights:

- Revenue: $472.6 million vs analyst estimates of $511.8 million (7.7% miss)

- EPS: -$0.10 vs analyst estimates of $0.17 (-$0.27 miss)

- Free Cash Flow was -$5 million, down from $35.2 million in the same quarter last year

- Gross Margin (GAAP): 57.4%, up from 56.1% in the same quarter last year

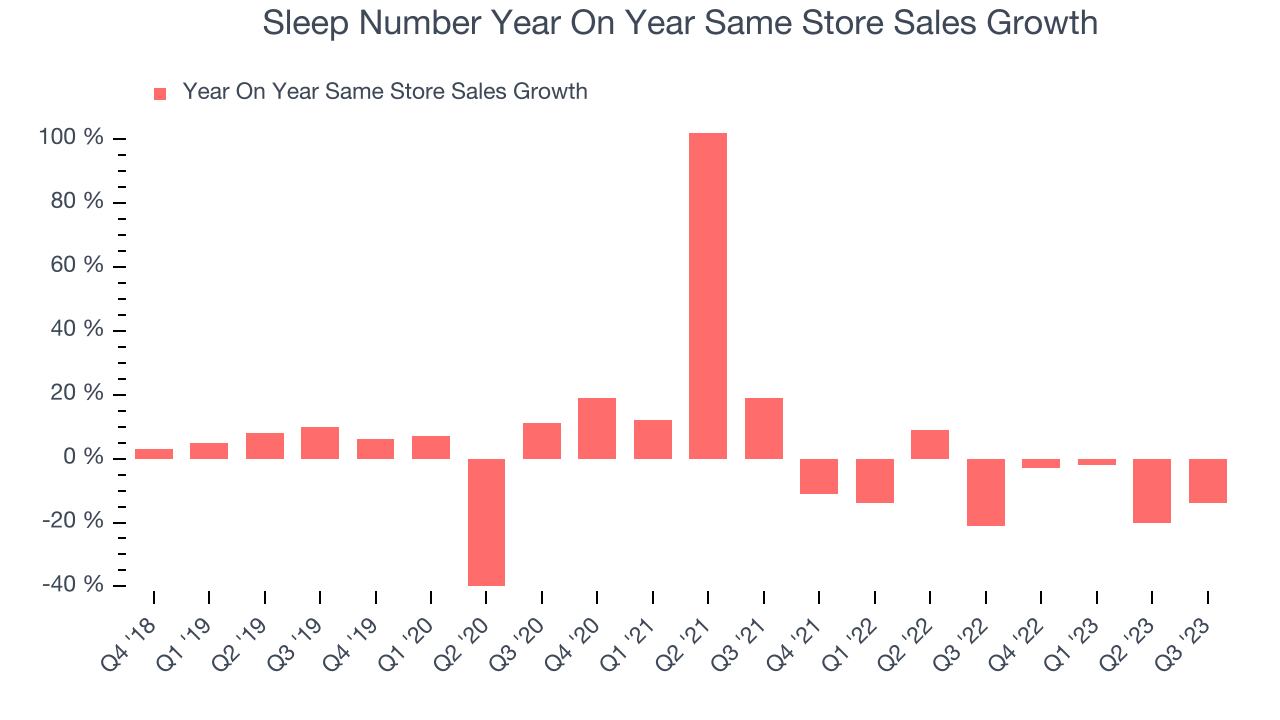

- Same-Store Sales were down 14% year on year

- Store Locations: 678 at quarter end, increasing by 16 over the last 12 months

“The third quarter was challenging for Sleep Number and the bedding industry as the consumer demand trajectory changed abruptly midway through the quarter,” said Shelly Ibach, Chair, President and CEO of Sleep Number.

Known for mattresses that can be adjusted with regards to firmness, Sleep Number (NASDAQ:SNBR) manufactures and sells its own brand of bedding products such as mattresses, bed frames, and pillows.

Home Furniture Retailer

Furniture retailers understand that ‘home is where the heart is’ but that no home is complete without that comfy sofa to kick back on or a dreamy bed to rest in. These stores focus on providing not only what is practically needed in a house but also aesthetics, style, and charm in the form of tables, lamps, and mirrors. Decades ago, it was thought that furniture would resist e-commerce because of the logistical challenges of shipping large furniture, but now you can buy a mattress online and get it in a box a few days later; so just like other retailers, furniture stores need to adapt to new realities and consumer behaviors.

Sales Growth

Sleep Number is a small retailer, which sometimes brings disadvantages compared to larger competitors that benefit from economies of scale.

As you can see below, the company's annualized revenue growth rate of 4% over the last four years (we compare to 2019 to normalize for COVID-19 impacts) was mediocre , but to its credit, it opened new stores and expanded its reach.

This quarter, Sleep Number reported a rather uninspiring 12.6% year-on-year revenue decline, missing analysts' expectations. Looking ahead, the analysts covering the company expect sales to grow 5.6% over the next 12 months.

Our recent pick has been a big winner, and the stock is up more than 2,000% since the IPO a decade ago. If you didn’t buy then, you have another chance today. The business is much less risky now than it was in the years after going public. The company is a clear market leader in a huge, growing $200 billion market. Its $7 billion of revenue only scratches the surface. Its products are mission critical. Virtually no customers ever left the company. See it here.

Number of Stores

The number of stores a retailer operates is a major determinant of how much it can sell, and its growth is a critical driver of how quickly company-level sales can grow.

When a retailer like Sleep Number is opening new stores, it usually means it's investing for growth because demand is greater than supply. Since last year, Sleep Number's store count increased by 16 locations, or 2.4%, to 678 total retail locations in the most recently reported quarter.

Over the last two years, the company has generally opened new stores and averaged 4.6% annual growth in its physical footprint, which is decent and on par with the broader sector. With an expanding store base and demand, revenue growth can come from multiple vectors: sales from new stores, sales from e-commerce, or increased foot traffic and higher sales per customer at existing stores.

Same-Store Sales

Same-store sales growth is a key performance indicator used to measure organic growth and demand for retailers.

Sleep Number's demand has been shrinking over the last eight quarters, and on average, its same-store sales have declined by 9.5% year on year. This performance is quite concerning and the company should reconsider its strategy before investing its precious capital into new store buildouts.

In the latest quarter, Sleep Number's same-store sales fell 14% year on year. This decrease was a further deceleration from the 21% year-on-year decline it posted 12 months ago. We hope the business can get back on track.

Key Takeaways from Sleep Number's Q3 Results

With a market capitalization of $361.2 million, Sleep Number is among smaller companies, but its more than $906,000 in cash on hand and near break-even free cash flow margins put it in a stable financial position.

We struggled to find many strong positives in these results. Its revenue and EPS missed Wall Street's estimates, and it lowered its full-year guidance significantly for the same two metrics. Management cited a downturn in demand for mattresses during the quarter, consistent with commentary we've heard from the broader consumer durables sector. To adapt to the changing economic environment, Sleep Number initiated cost reductions that are expected to reduce 2024 operating expenses by approximately $50 million. Overall, this was a bad quarter for Sleep Number. The stock is down 14.3% after reporting and currently trades at $13.74 per share.

Sleep Number may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.

The author has no position in any of the stocks mentioned in this report.