Varonis (NASDAQ:VRNS) Misses Q3 Sales Targets

Petr Huřťák /

October 30, 2023

Data protection and security software company Varonis (NASDAQ:VRNS) fell short of analysts' expectations in Q3 FY2023, with revenue flat year on year at $122.3 million. Next quarter's outlook also missed expectations with revenue guided to $152 million at the midpoint, or 0.29% below analysts' estimates. Turning to EPS, Varonis made a GAAP loss of $0.21 per share, improving from its loss of $0.26 per share in the same quarter last year.

Is now the time to buy Varonis? Find out in our full research report.

Varonis (VRNS) Q3 FY2023 Highlights:

- Revenue: $122.3 million vs analyst estimates of $125.5 million (2.53% miss)

- EPS (non-GAAP): $0.08 vs analyst estimates of $0.03 ($0.05 beat)

- Revenue Guidance for Q4 2023 is $152 million at the midpoint, roughly in line with what analysts were expecting

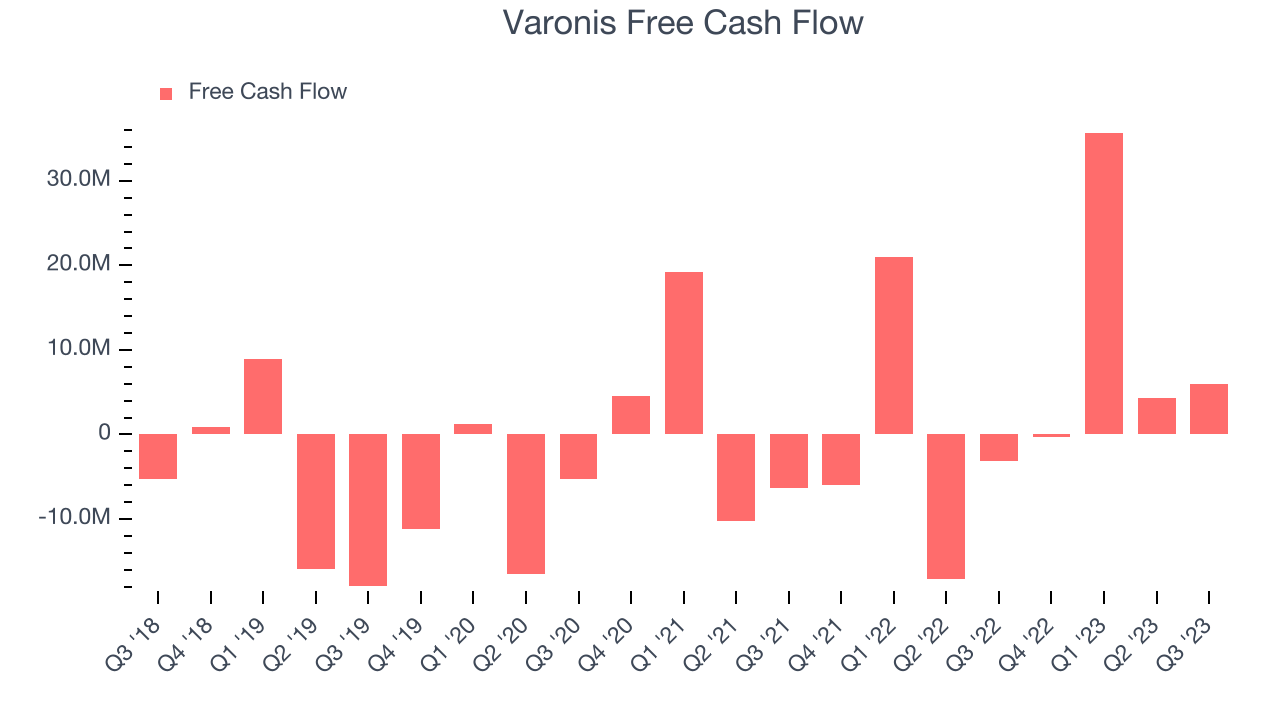

- Free Cash Flow of $5.98 million, up 38.7% from the previous quarter

- Gross Margin (GAAP): 85.8%, in line with the same quarter last year

Yaki Faitelson, Varonis CEO, said, "Our third quarter results reflect the continued healthy adoption of Varonis SaaS, and approximately 15% of total company ARR now comes from SaaS. The progress of our transition, coupled with our faster pace of innovation gets us closer to achieving our $1 billion ARR target and delivering meaningful stakeholder value."

Founded by a duo of former Israeli Defense Forces cyber warfare engineers, Varonis (NASDAQ:VRNS) offers software-as-service that helps customers protect data from cyber threats and gain visibility into how enterprise data is being used.

Endpoint Security

Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks. As the volume of internet enabled devices grows, every device that employees use to connect to business networks represents a potential risk. Endpoint security software enables businesses to protect devices (endpoints) that employees use for work purposes either on a network or in the cloud from cyber threats.

Sales Growth

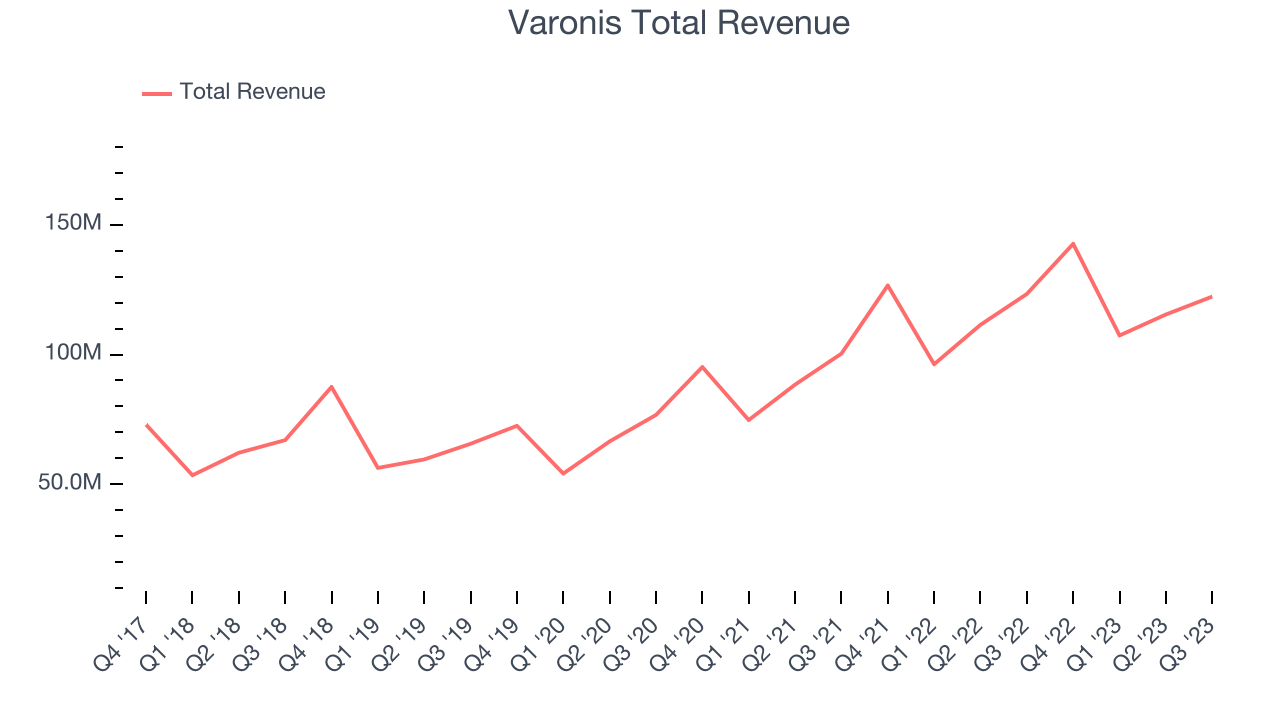

As you can see below, Varonis's revenue growth has been mediocre over the last two years, growing from $100.4 million in Q3 FY2021 to $122.3 million this quarter.

This quarter, Varonis's revenue was down 0.81% year on year, which might disappointment some shareholders.

Next quarter's guidance suggests that Varonis is expecting revenue to grow 6.58% year on year to $152 million, slowing down from the 12.7% year-on-year increase it recorded in the same quarter last year. Looking ahead, analysts covering the company were expecting sales to grow 9.7% over the next 12 months before the earnings results announcement.

The pandemic fundamentally changed several consumer habits. There is a founder-led company that is massively benefiting from this shift. The business has grown astonishingly fast, with 40%+ free cash flow margins. Its fundamentals are undoubtedly best-in-class. Still, the total addressable market is so big that the company has room to grow many times in size. See it here.

Cash Is King

If you've followed StockStory for a while, you know that we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills. Varonis's free cash flow came in at $5.98 million in Q3, turning positive over the last year.

Varonis has generated $45.7 million in free cash flow over the last 12 months, a solid 10.4% of revenue. This strong FCF margin stems from its asset-lite business model, giving it optionality and plenty of cash to reinvest in its business.

Key Takeaways from Varonis's Q3 Results

Sporting a market capitalization of $3.46 billion, Varonis is among smaller companies, but its more than $448.9 million in cash on hand and positive free cash flow over the last 12 months puts it in an attractive position to invest in growth.

Revenue missed, next quarter's revenue guidance was in line, but full year guidance was below expectations. However, billings in the quarter beat expectations. Adjusted operating profit guidance for next quarter and the full year were mixed like with revenue guidance, where the former was ahead but the latter was below. Overall, the results were mixed and could have been better. The company is down 4.1% on the results and currently trades at $30.18 per share.

Varonis may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.

The author has no position in any of the stocks mentioned in this report.