Varonis' (NASDAQ:VRNS) Q4 Sales Top Estimates, Growth To Accelerate Next Year

Max Juang /

February 5, 2024

Data protection and security software company Varonis (NASDAQ:VRNS) reported Q4 FY2023 results beating Wall Street analysts' expectations, with revenue up 8.1% year on year to $154.1 million. On the other hand, next quarter's revenue guidance of $113 million was less impressive, coming in 3.3% below analysts' estimates. It made a non-GAAP profit of $0.27 per share, improving from its profit of $0.21 per share in the same quarter last year.

Is now the time to buy Varonis? Find out in our full research report.

Varonis (VRNS) Q4 FY2023 Highlights:

- Revenue: $154.1 million vs analyst estimates of $151.7 million (1.6% beat)

- EPS (non-GAAP): $0.27 vs analyst estimates of $0.23 (18.5% beat)

- Revenue Guidance for Q1 2024 is $113 million at the midpoint, below analyst estimates of $116.8 million

- Management's revenue guidance for the upcoming financial year 2024 is $541 million at the midpoint, missing analyst estimates by 0.8% and implying 8.4% growth (vs 5.6% in FY2023)

- Free Cash Flow of $8.30 million, up 38.5% from the previous quarter

- Gross Margin (GAAP): 87.4%, in line with the same quarter last year

- Market Capitalization: $4.95 billion

Yaki Faitelson, Varonis CEO, said, "Our fourth quarter results reflect the sustained momentum of our SaaS platform and I’m happy to announce that SaaS ARR represented approximately 23% of total company ARR at year-end. This progress gives us the confidence to accelerate our SaaS transition timeline, which we now expect to complete by the end of 2026, a year earlier than our initial outlook."

Founded by a duo of former Israeli Defense Forces cyber warfare engineers, Varonis (NASDAQ:VRNS) offers software-as-service that helps customers protect data from cyber threats and gain visibility into how enterprise data is being used.

Endpoint Security

Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks. As the volume of internet enabled devices grows, every device that employees use to connect to business networks represents a potential risk. Endpoint security software enables businesses to protect devices (endpoints) that employees use for work purposes either on a network or in the cloud from cyber threats.

Sales Growth

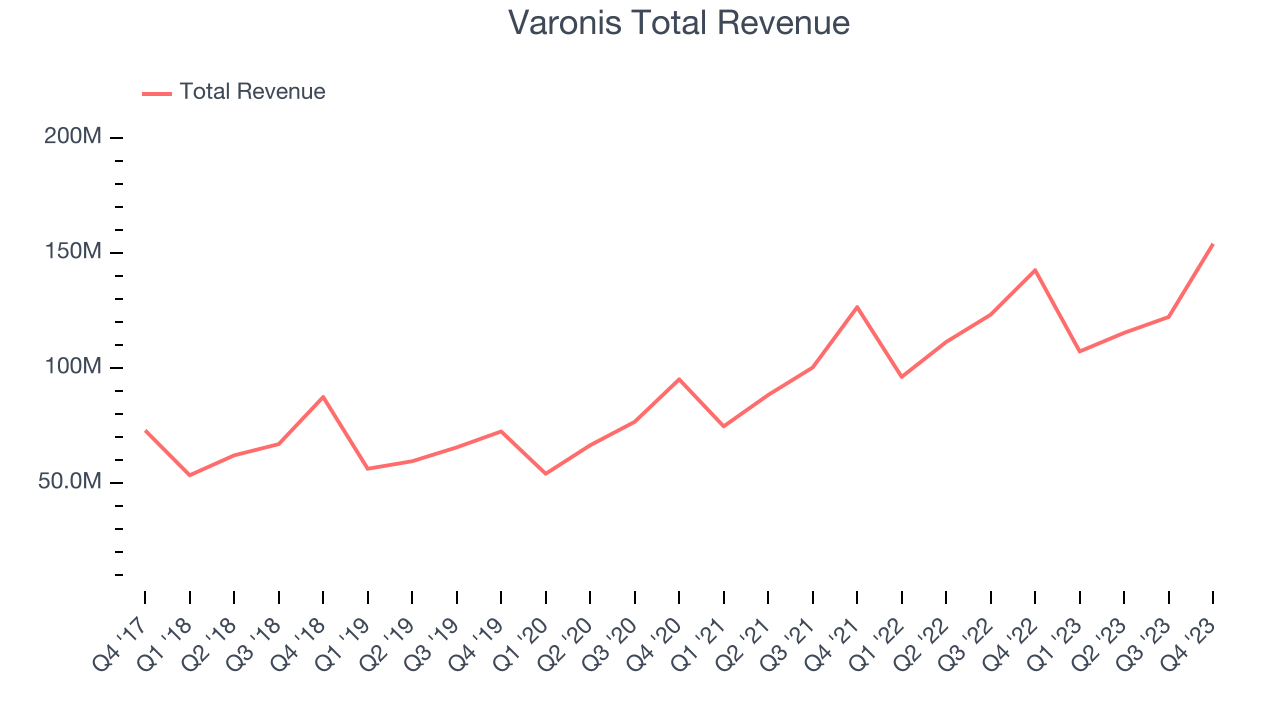

As you can see below, Varonis's revenue growth has been mediocre over the last two years, growing from $126.6 million in Q4 FY2021 to $154.1 million this quarter.

Varonis's quarterly revenue was only up 8.1% year on year. However, we can see that the company's revenue grew by $31.79 million quarter on quarter, accelerating from $6.89 million in Q3 2023.

Next quarter's guidance suggests that Varonis is expecting revenue to grow 5.3% year on year to $113 million, slowing down from the 11.5% year-on-year increase it recorded in the same quarter last year. For the upcoming financial year, management expects revenue to be $541 million at the midpoint, growing 8.4% year on year compared to the 5.4% increase in FY2023.

Our recent pick has been a big winner, and the stock is up more than 2,000% since the IPO a decade ago. If you didn’t buy then, you have another chance today. The business is much less risky now than it was in the years after going public. The company is a clear market leader in a huge, growing $200 billion market. Its $7 billion of revenue only scratches the surface. Its products are mission critical. Virtually no customers ever left the company. You can find it on our platform for free.

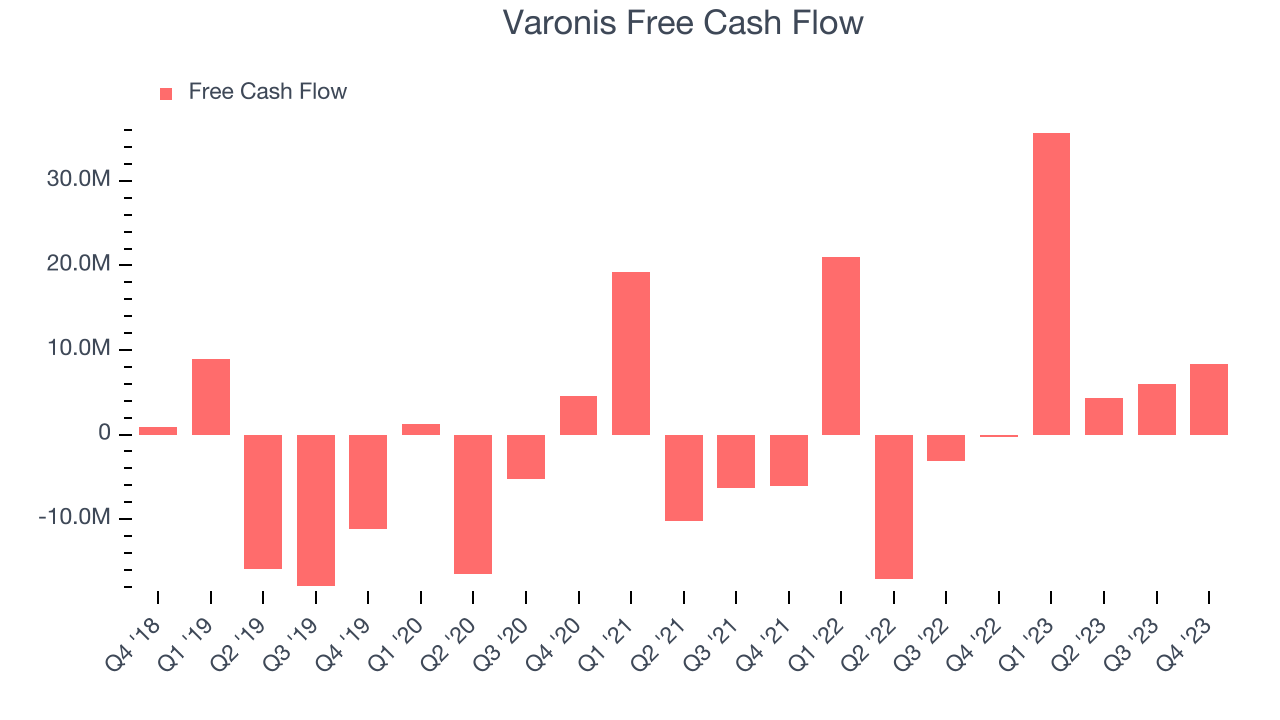

Cash Is King

If you've followed StockStory for a while, you know that we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills. Varonis's free cash flow came in at $8.30 million in Q4, turning positive over the last year.

Varonis has generated $54.32 million in free cash flow over the last 12 months, a solid 11.8% of revenue. This strong FCF margin stems from its asset-lite business model, giving it optionality and plenty of cash to reinvest in its business.

Key Takeaways from Varonis's Q4 Results

It was great to see Varonis expecting revenue growth to accelerate next year. We were also glad exceeded EPS and revenue expectations this quarter. On the other hand, despite the improvement its full-year revenue guidance missed Wall Street's estimates. Overall, this was a mixed quarter for Varonis. The stock is up 2.7% after reporting and currently trades at $46.75 per share.

Varonis may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.