Belden (NYSE:BDC) Surprises With Strong Q2

Max Juang /

August 1, 2024

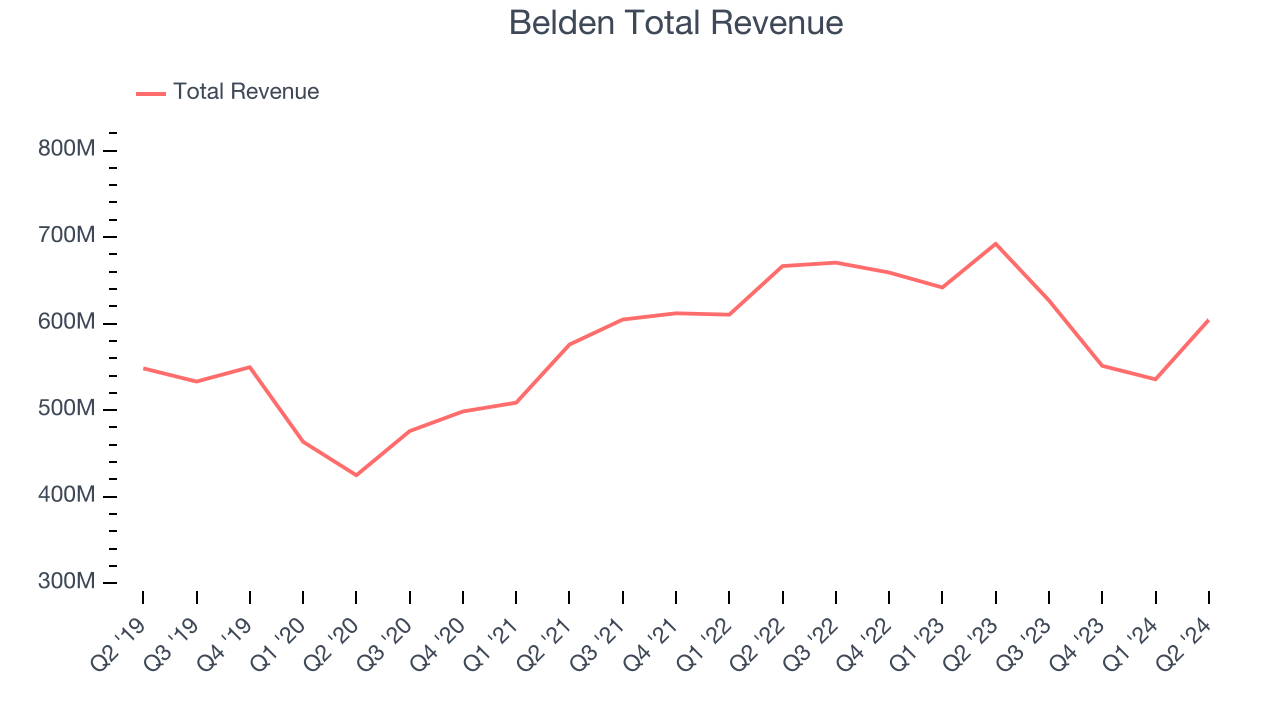

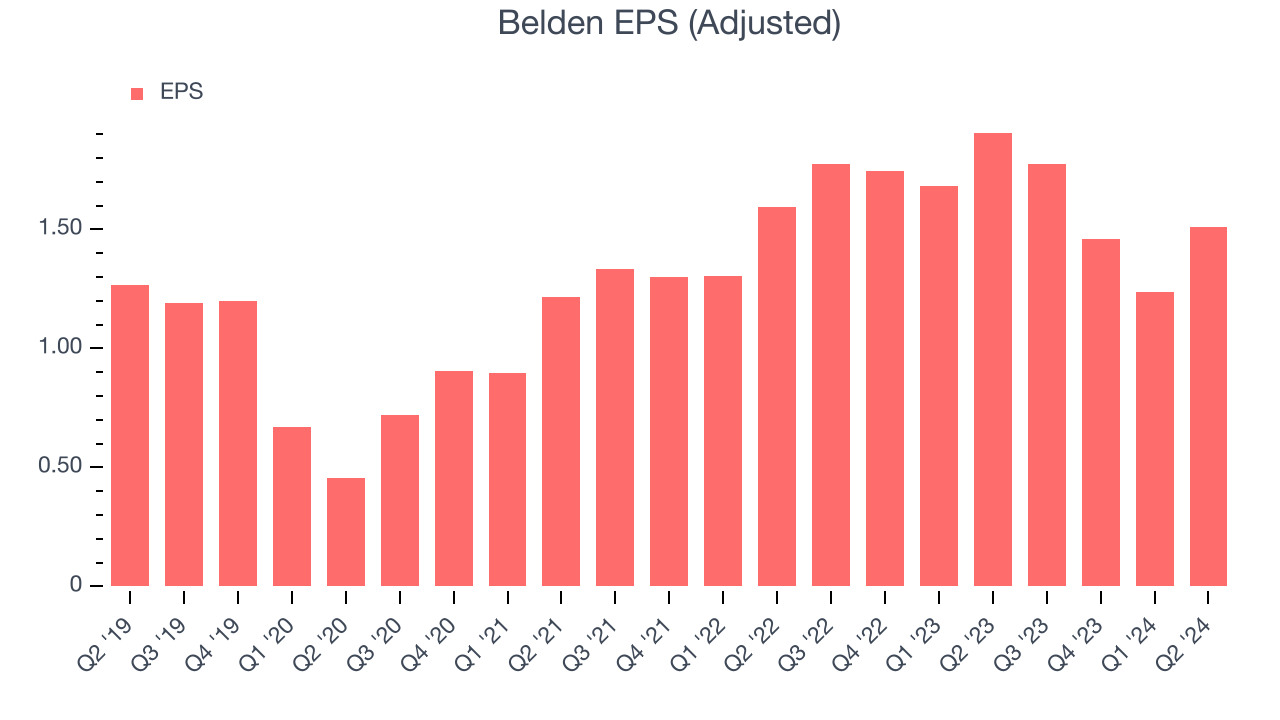

Electronic component manufacturer Belden (NYSE:BDC) reported Q2 CY2024 results exceeding Wall Street analysts' expectations, with revenue down 12.7% year on year to $604.3 million. Guidance for next quarter's revenue was also better than expected at $642.5 million at the midpoint, 1.9% above analysts' estimates. It made a non-GAAP profit of $1.51 per share, down from its profit of $1.91 per share in the same quarter last year.

Is now the time to buy Belden? Find out in our full research report.

Belden (BDC) Q2 CY2024 Highlights:

- Revenue: $604.3 million vs analyst estimates of $574.2 million (5.3% beat)

- EPS (non-GAAP): $1.51 vs analyst estimates of $1.37 (10.4% beat)

- Revenue Guidance for Q3 CY2024 is $642.5 million at the midpoint, above analyst estimates of $630.6 million

- EPS (non-GAAP) Guidance for Q3 CY2024 is $1.60 at the midpoint, below analyst estimates of $1.65

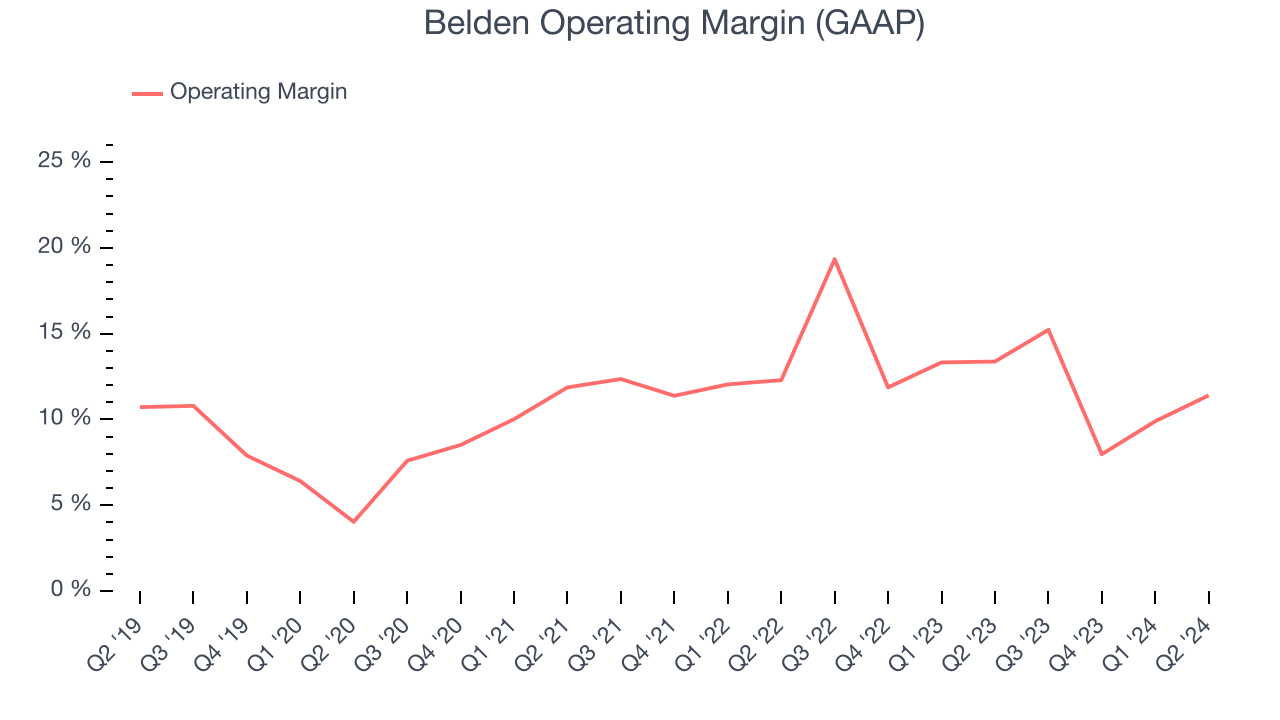

- Gross Margin (GAAP): 37.5%, in line with the same quarter last year

- Free Cash Flow of $60.93 million is up from -$21.5 million in the previous quarter

- Market Capitalization: $3.77 billion

“Demand for the quarter was steady, with our team delivering second quarter revenues and EPS exceeding expectations,” said Ashish Chand, President and CEO of Belden.

With its enamel-coated copper wire used in WWI for the Allied forces, Belden (NYSE:BDC) designs, manufactures, and sells electronic components to various industries.

Electronic Components

Like many equipment and component manufacturers, electronic components companies are buoyed by secular trends such as connectivity and industrial automation. More specific pockets of strong demand include data centers and telecommunications, which can benefit companies whose optical and transceiver offerings fit those markets. But like the broader industrials sector, these companies are also at the whim of economic cycles. Consumer spending, for example, can greatly impact these companies’ volumes.

Sales Growth

A company’s long-term performance can indicate its business quality. Any business can put up a good quarter or two, but many enduring ones tend to grow for years. Over the last five years, Belden's sales were flat. This shows demand was soft and is a tough starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Belden's recent history shows its demand has stayed suppressed as its revenue has declined by 3.6% annually over the last two years. Belden isn't alone in its struggles as the Electronic Components industry experienced a cyclical downturn, with many similar businesses seeing lower sales at this time.

We can dig further into the company's revenue dynamics by analyzing its most important segments, Enterprise and Industrial, which are 55.2% and 44.8% of revenue. Over the last two years, Belden's Enterprise revenue (network infrastructure and broadband solutions) averaged 1.5% year-on-year declines while its Industrial revenue (infrastructure digitization and automation) averaged 4.7% declines.

This quarter, Belden's revenue fell 12.7% year on year to $604.3 million but beat Wall Street's estimates by 5.3%. The company is guiding for revenue to rise 2.5% year on year to $642.5 million next quarter, improving from the 6.5% year-on-year decrease it recorded in the same quarter last year. Looking ahead, Wall Street expects sales to grow 11.8% over the next 12 months, an acceleration from this quarter.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

Operating Margin

Belden has managed its expenses well over the last five years. It demonstrated solid profitability for an industrials business, producing an average operating margin of 11.2%. This result isn't surprising as its high gross margin gives it a favorable starting point.

Looking at the trend in its profitability, Belden's annual operating margin rose by 3.8 percentage points over the last five years, showing its efficiency has improved.

In Q2, Belden generated an operating profit margin of 11.4%, down 2 percentage points year on year. Since Belden's operating margin decreased more than its gross margin, we can assume the company was recently less efficient because expenses such as sales, marketing, R&D, and administrative overhead increased.

EPS

Analyzing long-term revenue trends tells us about a company's historical growth, but the long-term change in its earnings per share (EPS) points to the profitability of that growth–for example, a company could inflate its sales through excessive spending on advertising and promotions.

Belden's EPS grew at a weak 3.4% compounded annual growth rate over the last five years. On the bright side, this performance was better than its flat revenue and tells us management responded to softer demand by adapting its cost structure.

Diving into the nuances of Belden's earnings can give us a better understanding of its performance. As we mentioned earlier, Belden's operating margin declined this quarter but expanded by 3.8 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; taxes and interest expenses can also affect EPS but don't tell us as much about a company's fundamentals.

Like with revenue, we also analyze EPS over a shorter period to see if we are missing a change in the business. For Belden, its two-year annual EPS growth of 3.9% is similar to its five-year trend, implying stable earnings.

In Q2, Belden reported EPS at $1.51, down from $1.91 in the same quarter last year. Despite falling year on year, this print easily cleared analysts' estimates. Over the next 12 months, Wall Street expects Belden to grow its earnings. Analysts are projecting its EPS of $5.98 in the last year to climb by 16% to $6.94.

Key Takeaways from Belden's Q2 Results

We were impressed by how significantly Belden blew past analysts' revenue and EPS expectations this quarter. We were also glad next quarter's revenue guidance topped Wall Street's estimates, but the drawback is its quarterly EPS forecast fell short. Zooming out, we think this was a solid quarter. The market was likely expecting more, however, and the stock traded down 1.4% to $91.28 immediately after reporting.

So should you invest in Belden right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.