Box (NYSE:BOX) Q1 Sales Beat Estimates, Next Quarter Growth Looks Optimistic

Adam Hejl /

May 27, 2021

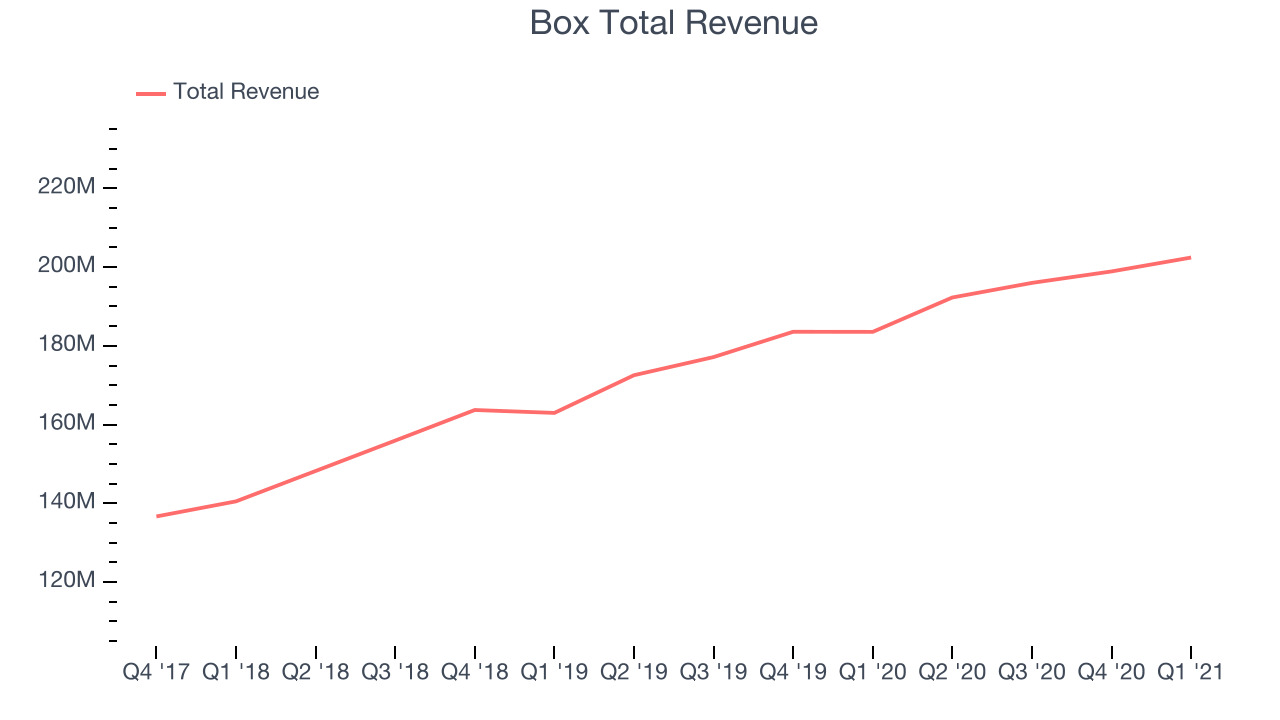

Cloud content storage and management platform Box (NYSE:BOX) reported solid growth in the Q1 FY2022 earnings announcement, with revenue up 10.2% year on year to $202.4 million. Box made a GAAP loss of $14.5 million, improving on its loss of $25.5 million, in the same quarter last year.

Is now the time to buy Box? Get early access to our full analysis of the earnings results here

Box (NYSE:BOX) Q1 FY2022 Highlights:

- Revenue: $202.4 million vs analyst estimates of $200.4 million (1% beat)

- EPS (non-GAAP): $0.18 vs analyst estimates of $0.17 (4.34% beat)

- Revenue guidance for Q2 2022 is $211.5 million at the midpoint, above analyst estimates of $209.5 million

- The company reconfirmed revenue guidance for the full year, at $849 million at the midpoint

- Free cash flow of $75.8 million, up 85.2% from previous quarter

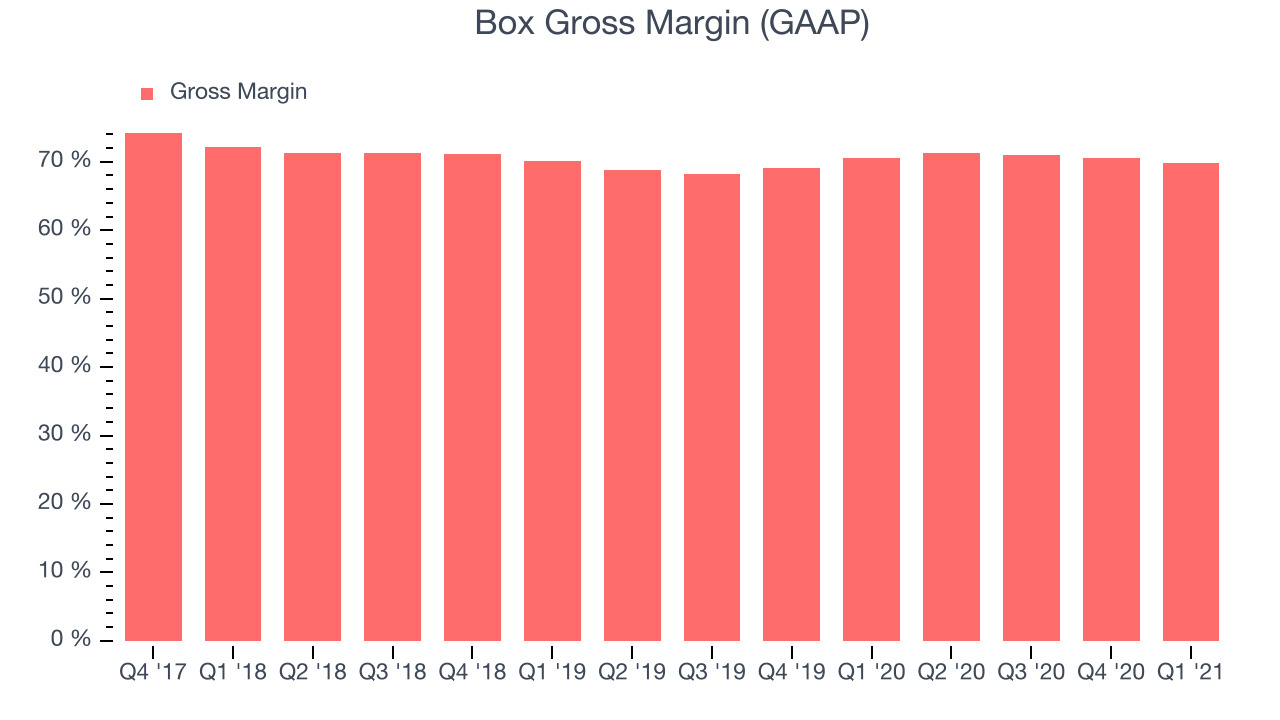

- Gross Margin (GAAP): 69.8%, in line with previous quarter

- Updated valuation: Box is flat at $22.88 and now trades at 4.7x price-to-sales (LTM), compared to 4.7x just before the results.

"Our vision for the Content Cloud is resonating with our customers. They recognize the strategic importance of securing, automating, integrating, and collaborating on content, and are investing in the full power of Box," said Aaron Levie, co-founder and CEO of Box.

Cloud Storage For Big Enterprise

Box (NYSE:BOX) started with offering cloud storage as a simple way for employees to share content more securely, but has since expanded into new functions such as e-signatures, monitoring anomalous behaviour and workflow management.

As you might have guessed, Box has plenty of competitors, such as Docusign (NASDAQ:DOCU) and Dropbox (NASDAQ:DBX), but it is also serving a growing market, as large enterprise increasingly moves all its data to the cloud, both for immediate cost savings, and to facilitate working from home for employees.

As you can see below, Box's revenue growth has been solid over the last twelve months, growing from $183.5 million to $202.4 million.

This quarter, Box's quarterly revenue was once again up 10.2% year on year. We can see that the company increased revenue by $3.52 million quarter on quarter. That's a solid improvement on the $2.91 million increase in Q4 2021, so shareholders should appreciate the acceleration of growth.

There are others doing even better. Founded by ex-Google engineers, a small company making software for banks has been growing revenue 90% year on year and is already up more than 400% since the IPO in December. You can find it on our platform for free.

Profitability With Scale

When you consider that Box has to actually store large amounts of data, you wouldn't expect it to have top class software margins. However, we should see its gross margins increase as the company grows revenue, and derives more of its revenue from software modules, not just cloud storage.

Box's gross profit margin, an important metric measuring how much money there is left after paying for servers, licences, technical support and other necessary running expenses was at 69.8% in Q1. That means that for every $1 in revenue the company had $0.69 left to spend on developing new products, marketing & sales and the general administrative overhead. This would be considered a low gross margin for a SaaS company and we would like to see it start improving again.

Key Takeaways from Box's Q1 Results

With market capitalisation of $3.76 billion Box is among smaller companies, but its more than $561.4 million in cash and positive free cash flow over the last twelve months put it in a very strong position to invest in growth.

It was good to see Box provide next quarter revenue outlook exceeding analysts’ expectations. And we were also happy to see it topped analysts’ revenue expectations, even if just narrowly. On the other hand, the revenue growth is quite weak compared to other SaaS businesses. Zooming out, we think this was still a decent quarter. But Box isn't our first pick as growth stock, and nothing we've seen today has changed that.

PS. If you found this analysis useful, you will love our earnings alerts! We publish so fast, you often have the opportunity to buy or sell before the market has fully absorbed the information. Never miss out on the right time to invest again. Signup here for free early access.

The author has no position in any of the stocks mentioned.