Box (BOX)

We’re cautious of Box. Its sluggish sales growth shows demand is soft, a worrisome sign for investors in high-quality stocks.― StockStory Analyst Team

1. News

2. Summary

Why We Think Box Will Underperform

Known as the "Content Cloud" for managing the 90% of business data that exists as unstructured files and documents, Box (NYSE:BOX) provides a cloud-based platform that enables organizations to securely manage, share, and collaborate on their content from anywhere on any device.

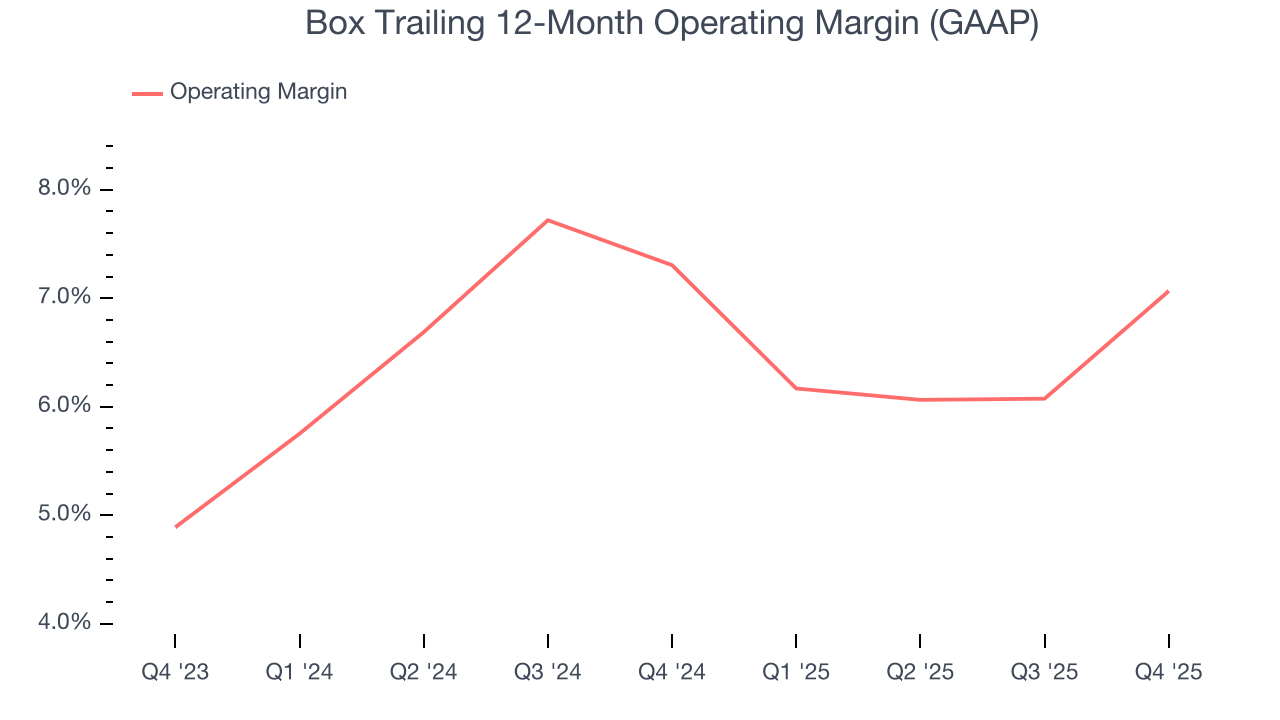

- Operating margin was unchanged over the last year, suggesting it failed to gain leverage on its fixed costs

- Muted 8.8% annual revenue growth over the last five years shows its demand lagged behind its software peers

- A silver lining is that its well-designed software integrates seamlessly with other workflows, enabling swift payback periods on marketing expenses and customer growth at scale

Box doesn’t pass our quality test. We’re on the lookout for more interesting opportunities.

Why There Are Better Opportunities Than Box

Box is trading at $24.89 per share, or 2.8x forward price-to-sales. This is a cheap valuation multiple, but for good reason. You get what you pay for.

It’s better to pay up for high-quality businesses with higher long-term earnings potential rather than to buy lower-quality stocks because they appear cheap. These challenged businesses often don’t re-rate, a phenomenon known as a “value trap”.

3. Box (BOX) Research Report: Q4 CY2025 Update

Cloud content management platform Box (NYSE:BOX) announced better-than-expected revenue in Q4 CY2025, with sales up 9.4% year on year to $305.9 million. Guidance for next quarter’s revenue was optimistic at $304 million at the midpoint, 2.1% above analysts’ estimates. Its non-GAAP profit of $0.49 per share was 45.9% above analysts’ consensus estimates.

Box (BOX) Q4 CY2025 Highlights:

- Revenue: $305.9 million vs analyst estimates of $304.3 million (9.4% year-on-year growth, 0.5% beat)

- Adjusted EPS: $0.49 vs analyst estimates of $0.34 (45.9% beat)

- Adjusted Operating Income: $93.72 million vs analyst estimates of $90.72 million (30.6% margin, 3.3% beat)

- Revenue Guidance for Q1 CY2026 is $304 million at the midpoint, above analyst estimates of $297.8 million

- Adjusted EPS guidance for the upcoming financial year 2027 is $1.55 at the midpoint, beating analyst estimates by 6.8%

- Operating Margin: 10.2%, up from 6.4% in the same quarter last year

- Free Cash Flow Margin: 31.9%, up from 20.4% in the previous quarter

- Billings: $419.8 million at quarter end, up 5.3% year on year

- Market Capitalization: $3.38 billion

Company Overview

Known as the "Content Cloud" for managing the 90% of business data that exists as unstructured files and documents, Box (NYSE:BOX) provides a cloud-based platform that enables organizations to securely manage, share, and collaborate on their content from anywhere on any device.

Box serves as the secure foundation for an organization's documents, images, videos, and other unstructured content throughout its lifecycle—from creation to retention. The platform offers advanced security features like encryption, information rights management, threat detection through Box Shield, and governance capabilities for compliance requirements across various industries. These tools allow administrators to set granular permissions and controls while maintaining easy access for authorized users.

Organizations use Box for a wide range of scenarios: facilitating secure external collaboration, creating specialized content portals, streamlining document workflows, and implementing electronic signature processes. The platform integrates with over 1,500 business applications including Microsoft 365, Google Workspace, Salesforce, and Slack, allowing content to flow securely between systems while maintaining consistent security policies.

Beyond basic file storage, Box offers productivity features like Box Notes for real-time document collaboration, Box Canvas for visual whiteboarding, and Box Relay for automating content-centric workflows without coding. Recently, Box has expanded into AI capabilities that allow users to summarize documents, generate content, and extract insights while maintaining enterprise security controls.

Box generates revenue through subscription plans sold to organizations ranging from small teams to Fortune 500 enterprises. The company focuses particularly on industries with complex content needs and compliance requirements, such as financial services, healthcare, life sciences, and government sectors.

4. Document Management

The catch phrase "digital transformation" originally referred to the digitization of documents within enterprises. The growth of digital documents has spurred an explosion of collaboration within and between businesses, which in turn is driving the demand for e-signature and content management platforms.

Box competes primarily with Microsoft SharePoint and OneDrive, Google Drive, OpenText Documentum, and to a lesser extent Dropbox in the content management and enterprise file sync-and-share markets.

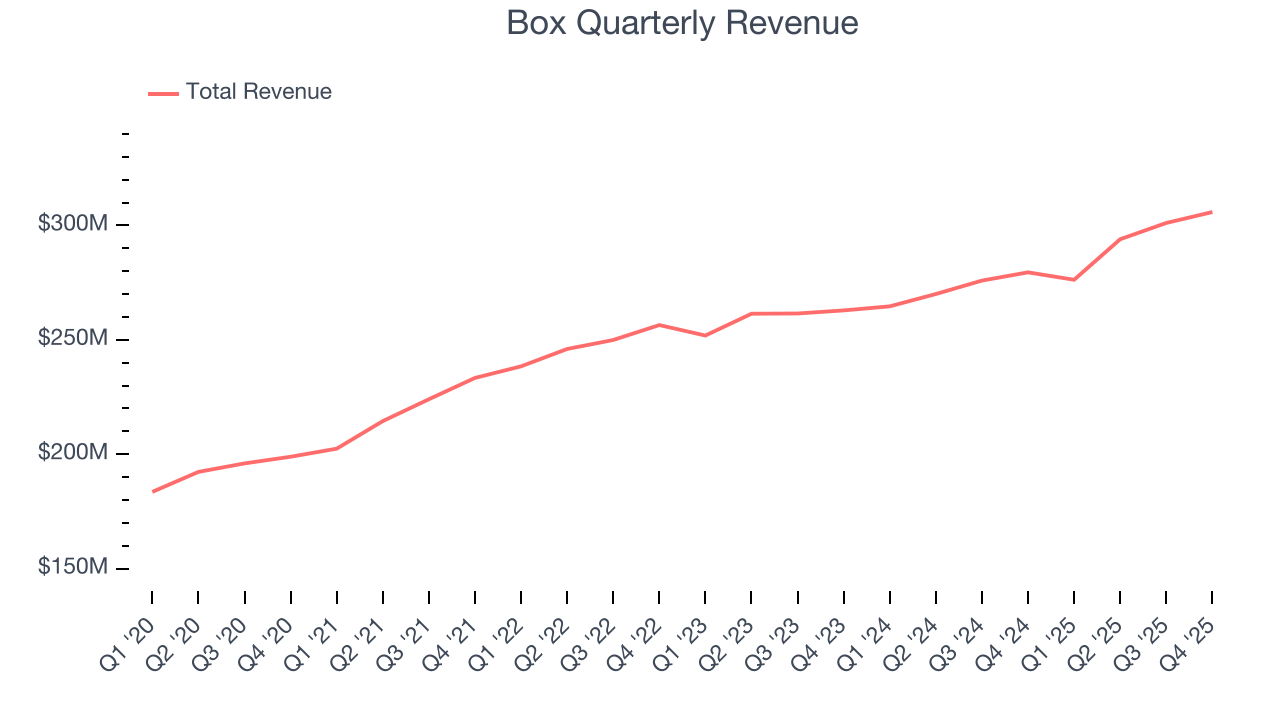

5. Revenue Growth

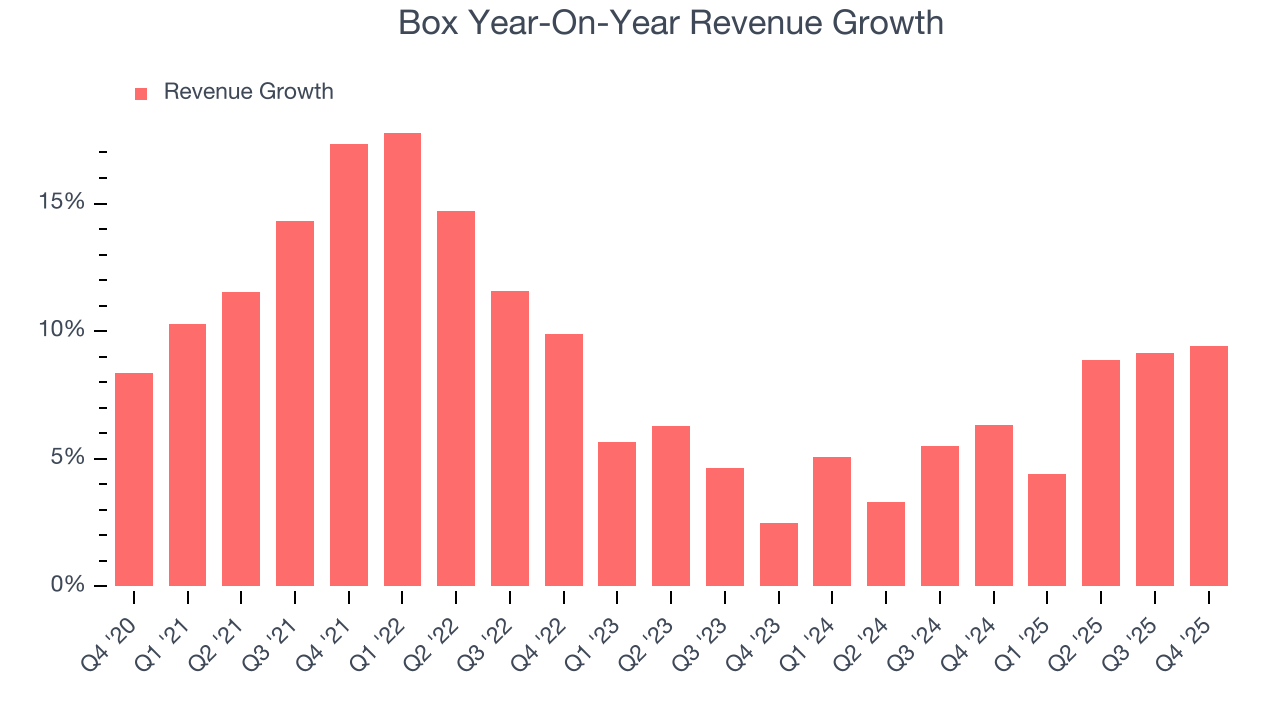

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Unfortunately, Box’s 8.8% annualized revenue growth over the last five years was sluggish. This was below our standard for the software sector and is a rough starting point for our analysis.

Long-term growth is the most important, but within software, a half-decade historical view may miss new innovations or demand cycles. Box’s recent performance shows its demand has slowed as its annualized revenue growth of 6.5% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

This quarter, Box reported year-on-year revenue growth of 9.4%, and its $305.9 million of revenue exceeded Wall Street’s estimates by 0.5%. Company management is currently guiding for a 10% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 7.3% over the next 12 months, similar to its two-year rate. This projection doesn't excite us and suggests its newer products and services will not lead to better top-line performance yet.

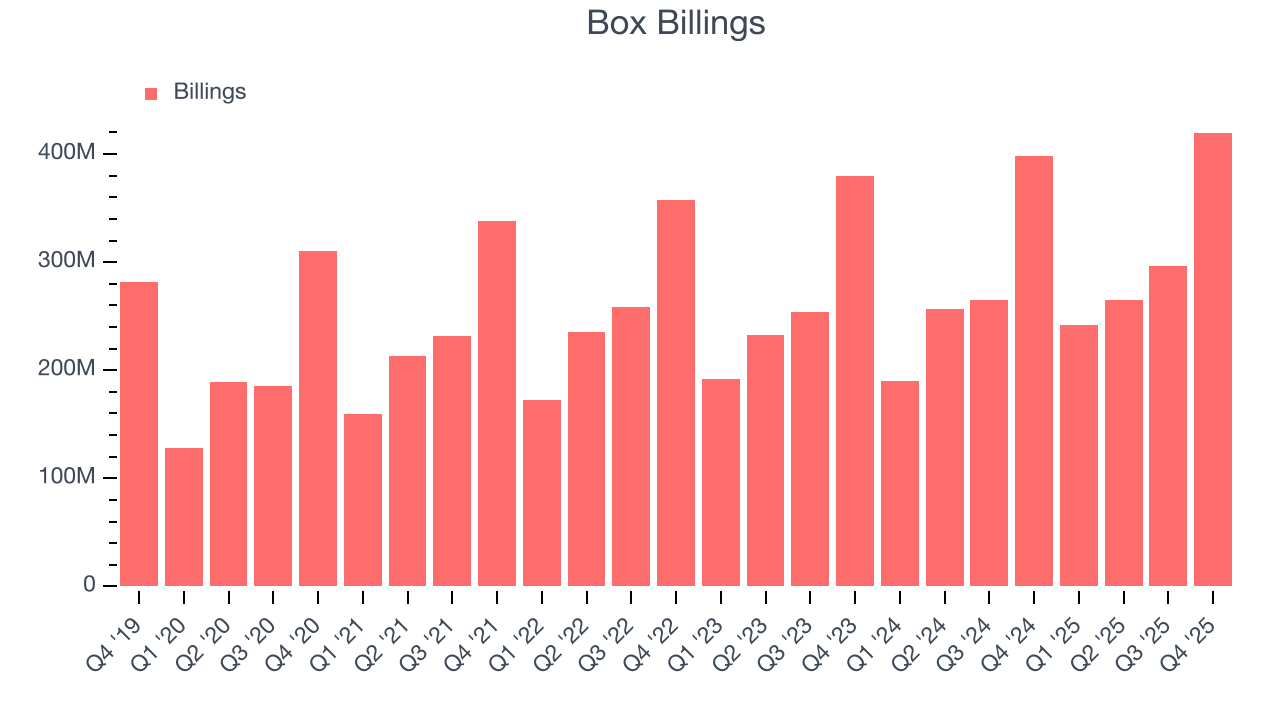

6. Billings

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Box’s billings came in at $419.8 million in Q4, and over the last four quarters, its growth was underwhelming as it averaged 11.9% year-on-year increases. However, this alternate topline metric grew faster than total sales, meaning the company collects cash upfront and then recognizes the revenue over the length of its contracts - a boost for its liquidity and future revenue prospects.

7. Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

Box is extremely efficient at acquiring new customers, and its CAC payback period checked in at 10.4 months this quarter. The company’s rapid recovery of its customer acquisition costs means it can attempt to spur growth by increasing its sales and marketing investments.

8. Gross Margin & Pricing Power

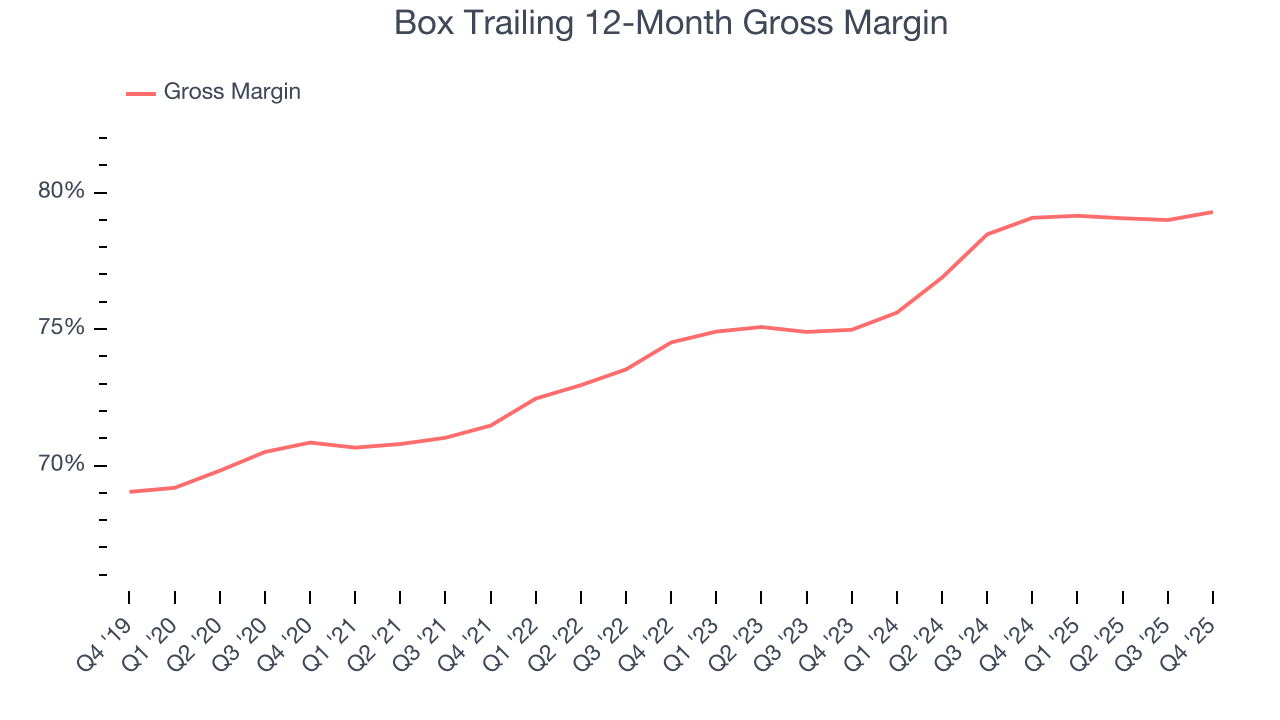

For software companies like Box, gross profit tells us how much money remains after paying for the base cost of products and services (typically servers, licenses, and certain personnel). These costs are usually low as a percentage of revenue, explaining why software is more lucrative than other sectors.

Box’s robust unit economics are better than the broader software industry, an output of its asset-lite business model and pricing power. They also enable the company to fund large investments in new products and sales during periods of rapid growth to achieve higher profits in the future. As you can see below, it averaged an excellent 79.3% gross margin over the last year. Said differently, roughly $79.29 was left to spend on selling, marketing, and R&D for every $100 in revenue.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. Box has seen gross margins improve by 4.3 percentage points over the last 2 year, which is very good in the software space.

Box’s gross profit margin came in at 80.1% this quarter, up 1.1 percentage points year on year. On a wider time horizon, the company’s full-year margin has remained steady over the past four quarters, suggesting its input costs have been stable and it isn’t under pressure to lower prices.

9. Operating Margin

Many software businesses adjust their profits for stock-based compensation (SBC), but we prioritize GAAP operating margin because SBC is a real expense used to attract and retain engineering and sales talent. This is one of the best measures of profitability because it shows how much money a company takes home after developing, marketing, and selling its products.

Box has managed its cost base well over the last year. It demonstrated solid profitability for a software business, producing an average operating margin of 7.1%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Looking at the trend in its profitability, Box’s operating margin might fluctuated slightly but has generally stayed the same over the last two years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, Box generated an operating margin profit margin of 10.2%, up 3.8 percentage points year on year. The increase was encouraging, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

10. Cash Is King

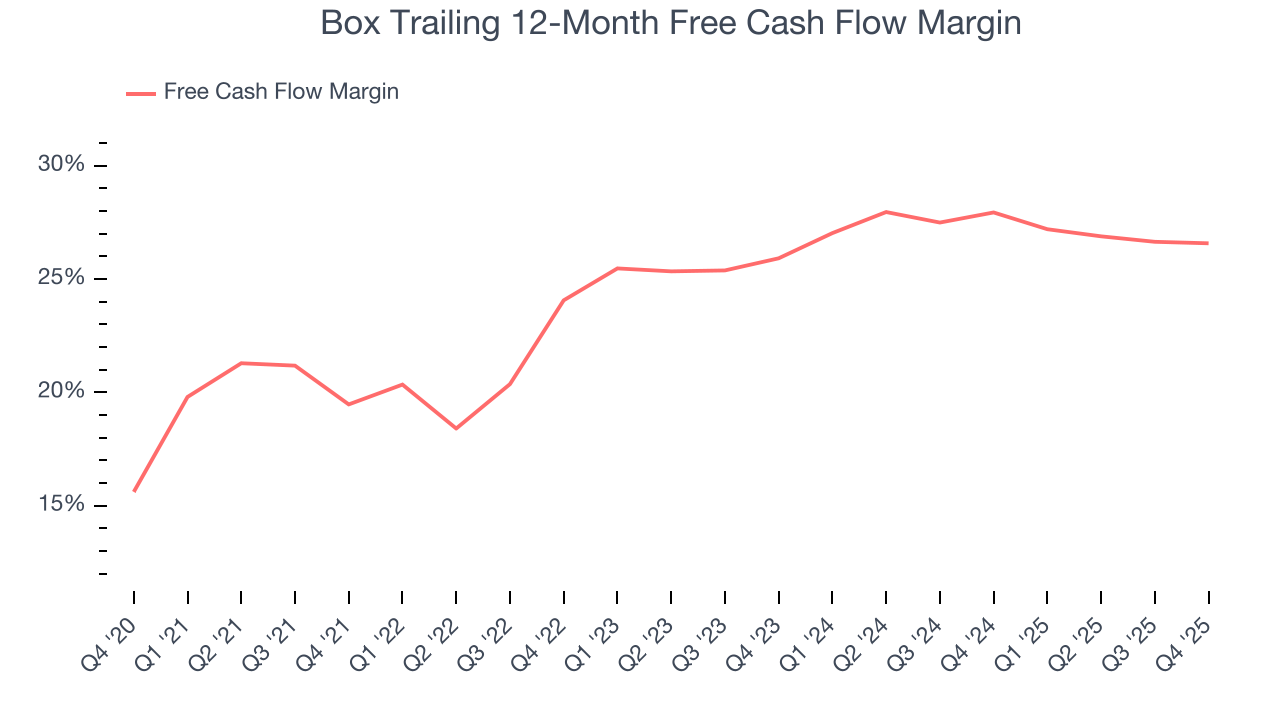

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Box has shown robust cash profitability, driven by its attractive business model and cost-effective customer acquisition strategy that enable it to invest in new products and services rather than sales and marketing. The company’s free cash flow margin averaged 26.6% over the last year, quite impressive for a software business. Box has shown robust cash profitability relative to peers over the last year, giving the company fewer opportunities to return capital to shareholders.

Box’s free cash flow clocked in at $97.51 million in Q4, equivalent to a 31.9% margin. This cash profitability was in line with the comparable period last year and above its one-year average.

Over the next year, analysts predict Box’s cash conversion will slightly improve. Their consensus estimates imply its free cash flow margin of 26.6% for the last 12 months will increase to 28%, giving it more flexibility for investments, share buybacks, and dividends.

11. Balance Sheet Assessment

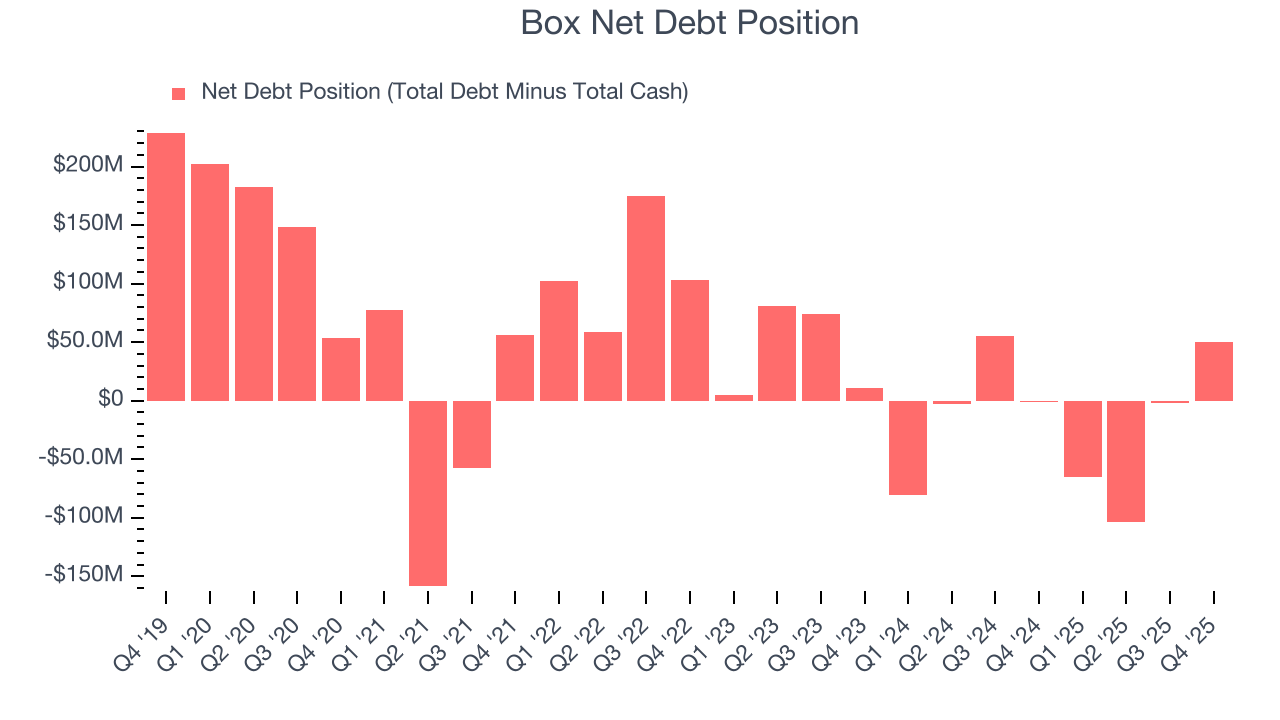

Box reported $478.1 million of cash and $528 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $366.5 million of EBITDA over the last 12 months, we view Box’s 0.1× net-debt-to-EBITDA ratio as safe. We also see its $14.04 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Box’s Q4 Results

We were impressed by Box’s optimistic EPS guidance for next quarter, which blew past analysts’ expectations. We were also glad its full-year EPS guidance trumped Wall Street’s estimates. Overall, we think this was still a solid quarter with some key areas of upside. The stock traded up 3.6% to $24.80 immediately following the results.

13. Is Now The Time To Buy Box?

Updated: March 15, 2026 at 10:17 PM EDT

When considering an investment in Box, investors should account for its valuation and business qualities as well as what’s happened in the latest quarter.

Box isn’t a terrible business, but it doesn’t pass our quality test. To kick things off, its revenue growth was weak over the last five years, and analysts don’t see anything changing over the next 12 months. And while Box’s efficient sales strategy allows it to target and onboard new users at scale, its operating margin hasn't moved over the last year.

Box’s price-to-sales ratio based on the next 12 months is 2.8x. This valuation multiple is fair, but we don’t have much faith in the company. We're fairly confident there are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $32.25 on the company (compared to the current share price of $24.89).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.