Appian (APPN)

We’re skeptical of Appian. Its growth has decelerated and its failure to generate meaningful free cash flow makes us question its prospects.― StockStory Analyst Team

1. News

2. Summary

Why We Think Appian Will Underperform

Powering billions of transactions daily since its founding in 1999, Appian (NASDAQ:APPN) provides a low-code platform that helps businesses automate complex processes and operationalize artificial intelligence without extensive programming knowledge.

- Long payback periods on sales and marketing expenses limit customer growth and signal the company operates in a highly competitive environment

- Estimated sales growth of 11.5% for the next 12 months implies demand will slow from its two-year trend

- A consolation is that its winning new contracts that can potentially increase in value as its billings growth has averaged 18.8% over the last year

Appian is in the penalty box. We believe there are better businesses elsewhere.

Why There Are Better Opportunities Than Appian

Appian is trading at $25.59 per share, or 2.3x forward price-to-sales. This sure is a cheap multiple, but you get what you pay for.

We’d rather pay up for companies with elite fundamentals than get a bargain on weak ones. Cheap stocks can be value traps, and as their performance deteriorates, they will stay cheap or get even cheaper.

3. Appian (APPN) Research Report: Q4 CY2025 Update

Low-code automation software company Appian (NASDAQ:APPN) announced better-than-expected revenue in Q4 CY2025, with sales up 21.7% year on year to $202.9 million. Guidance for next quarter’s revenue was better than expected at $191 million at the midpoint, 1.5% above analysts’ estimates. Its non-GAAP profit of $0.15 per share was 91.5% above analysts’ consensus estimates.

Appian (APPN) Q4 CY2025 Highlights:

- Revenue: $202.9 million vs analyst estimates of $189.3 million (21.7% year-on-year growth, 7.2% beat)

- Adjusted EPS: $0.15 vs analyst estimates of $0.08 (91.5% beat)

- Adjusted Operating Income: $67.1 million vs analyst estimates of $9.06 million (33.1% margin, significant beat)

- Revenue Guidance for Q1 CY2026 is $191 million at the midpoint, above analyst estimates of $188.3 million

- Adjusted EPS guidance for the upcoming financial year 2026 is $0.89 at the midpoint, beating analyst estimates by 15.6%

- EBITDA guidance for the upcoming financial year 2026 is $94 million at the midpoint, above analyst estimates of $86.56 million

- Operating Margin: -0.3%, down from 3% in the same quarter last year

- Free Cash Flow Margin: 0.1%, down from 9.7% in the previous quarter

- Net Revenue Retention Rate: 114%, up from 111% in the previous quarter

- Market Capitalization: $1.78 billion

Company Overview

Powering billions of transactions daily since its founding in 1999, Appian (NASDAQ:APPN) provides a low-code platform that helps businesses automate complex processes and operationalize artificial intelligence without extensive programming knowledge.

Appian's platform combines four key capabilities that form the backbone of its offering: process automation, data fabric, total experience, and continuous improvement through process mining. The platform allows organizations to orchestrate workflows involving both AI systems and human workers, encode business rules to reduce risk, and integrate robotic process automation (RPA) to boost efficiency.

At its core, Appian's data fabric technology enables customers to unify disparate data sources across their enterprise into a single virtual model that can be used to train AI models and support informed decision-making. This capability processed billions of queries in 2023 alone, demonstrating its robust adoption.

A financial services company might use Appian to streamline loan processing by connecting customer data across systems, automating approval workflows, and providing visibility into bottlenecks. Government agencies might implement Appian solutions to coordinate citizen services across departments, reducing paperwork and improving response times.

Appian generates revenue primarily through subscription sales, with the U.S. federal government representing over 21% of its total revenue. The company maintains strategic partnerships with major consulting firms like Accenture, Deloitte, and PwC, which often introduce Appian to potential customers during digital transformation projects. Appian serves approximately 1,000 customers across industries including financial services, government, life sciences, insurance, and healthcare.

4. Automation Software

The whole purpose of software is to automate tasks to increase productivity. Today, innovative new software techniques, often involving AI and machine learning, are finally allowing automation that has graduated from simple one- or two-step workflows to more complex processes integral to enterprises. The result is surging demand for modern automation software.

Appian competes with other low-code and business process management platform providers including ServiceNow (NYSE:NOW), Pegasystems (NASDAQ:PEGA), and Microsoft's Power Platform (NASDAQ:MSFT), as well as private companies like OutSystems and Mendix (owned by Siemens).

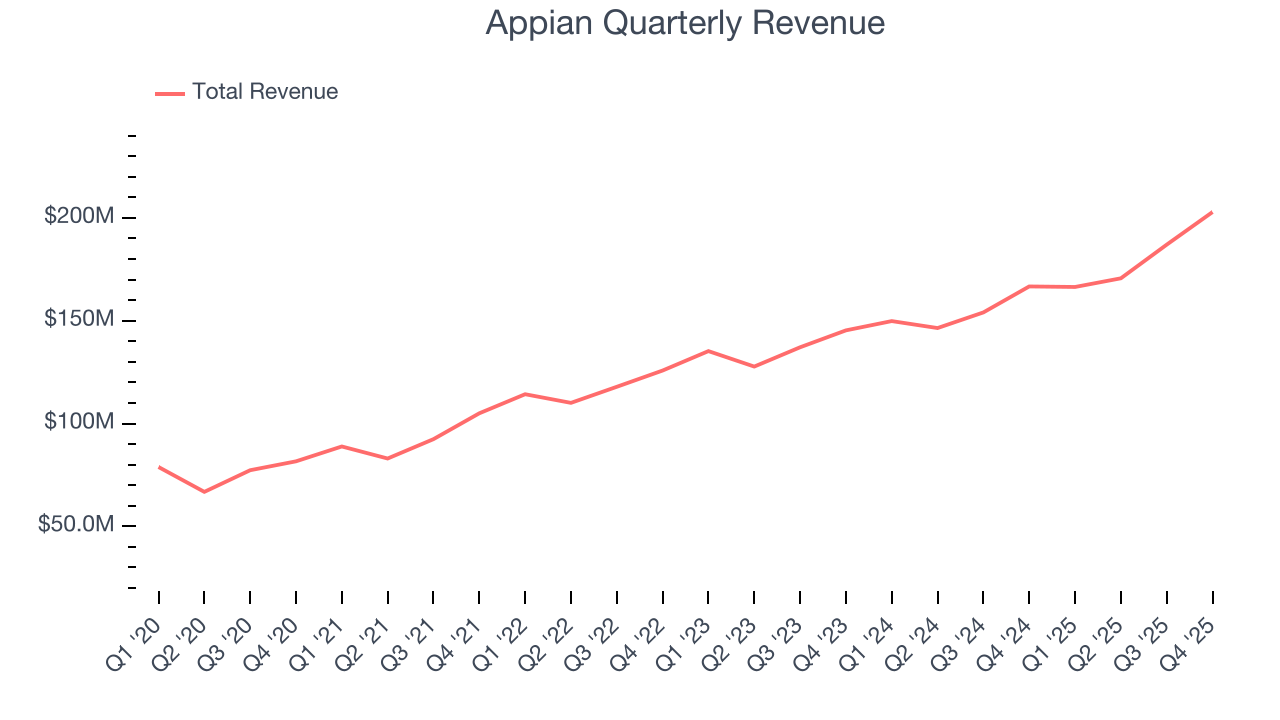

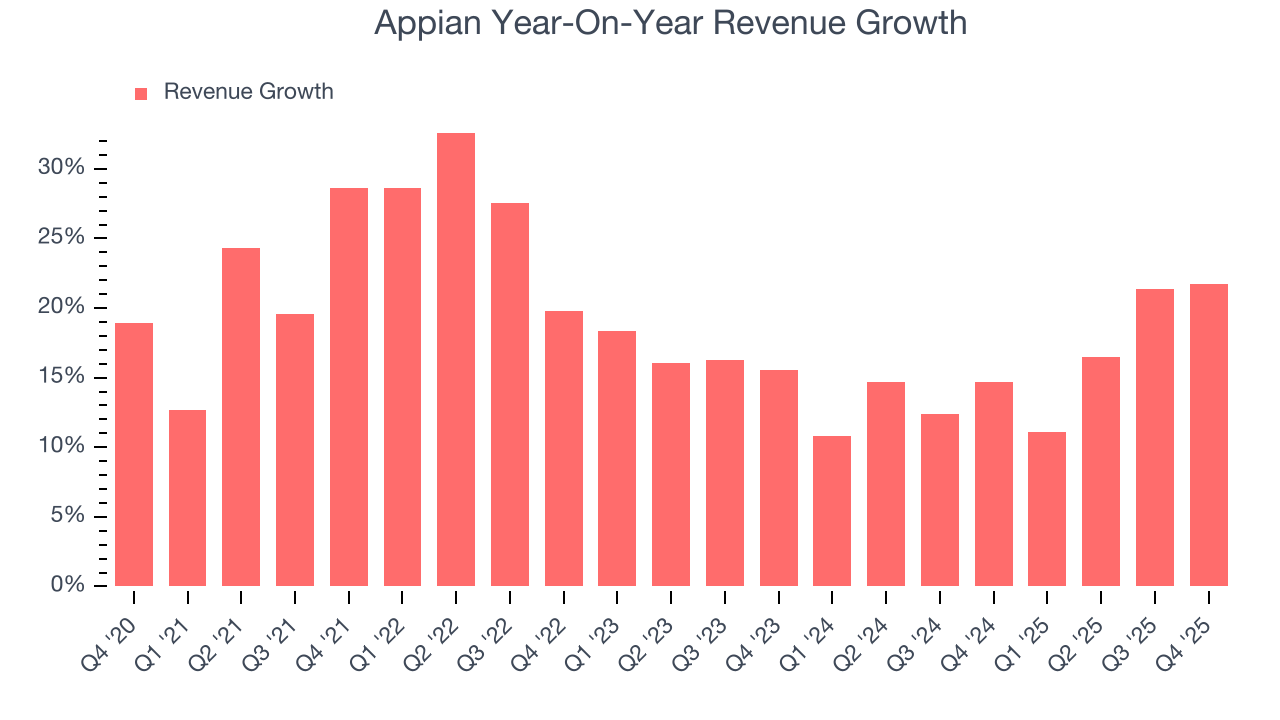

5. Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Luckily, Appian’s sales grew at a decent 19% compounded annual growth rate over the last five years. Its growth was slightly above the average software company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within software, a half-decade historical view may miss recent innovations or disruptive industry trends. Appian’s annualized revenue growth of 15.5% over the last two years is below its five-year trend, but we still think the results were respectable.

This quarter, Appian reported robust year-on-year revenue growth of 21.7%, and its $202.9 million of revenue topped Wall Street estimates by 7.2%. Company management is currently guiding for a 14.8% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 9.5% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and indicates its products and services will face some demand challenges.

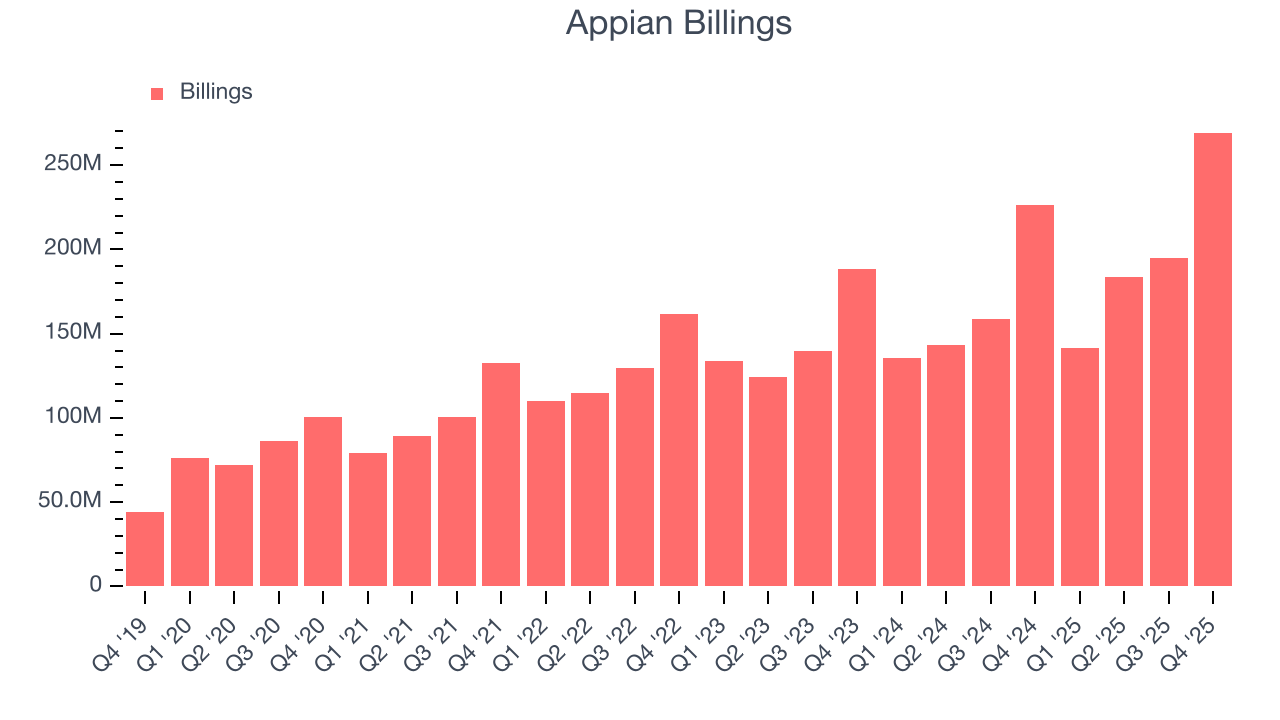

6. Billings

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Appian’s billings punched in at $269.3 million in Q4, and over the last four quarters, its growth was solid as it averaged 18.8% year-on-year increases. This performance aligned with its total sales growth, indicating robust customer demand. The cash collected from customers also enhances liquidity and provides a solid foundation for future investments and growth.

7. Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

Appian’s recent customer acquisition efforts haven’t yielded returns as its CAC payback period was negative this quarter, meaning its incremental sales and marketing investments outpaced its revenue. The company’s inefficiency indicates it operates in a competitive market and must continue investing to grow.

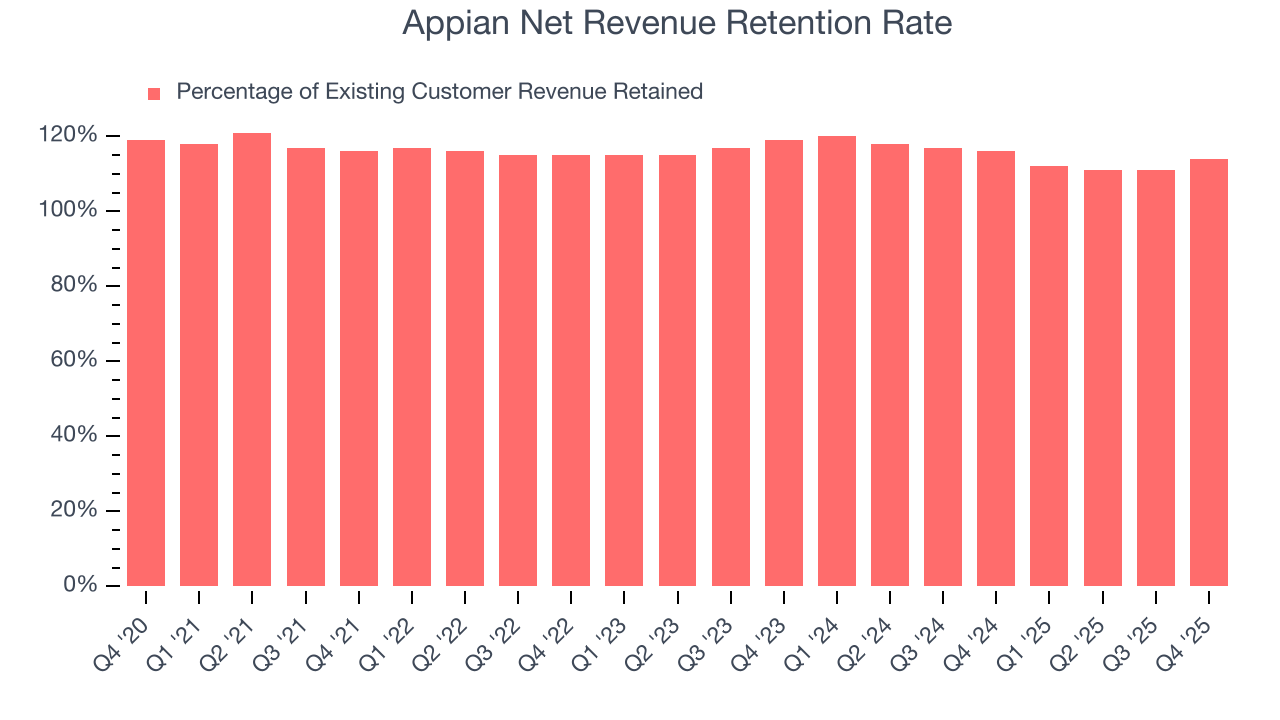

8. Customer Retention

One of the best parts about the software-as-a-service business model (and a reason why they trade at high valuation multiples) is that customers typically spend more on a company’s products and services over time.

Appian’s net revenue retention rate, a key performance metric measuring how much money existing customers from a year ago are spending today, was 112% in Q4. This means Appian would’ve grown its revenue by 12% even if it didn’t win any new customers over the last 12 months.

Appian has a good net retention rate, proving that customers are satisfied with its software and getting more value from it over time, which is always great to see.

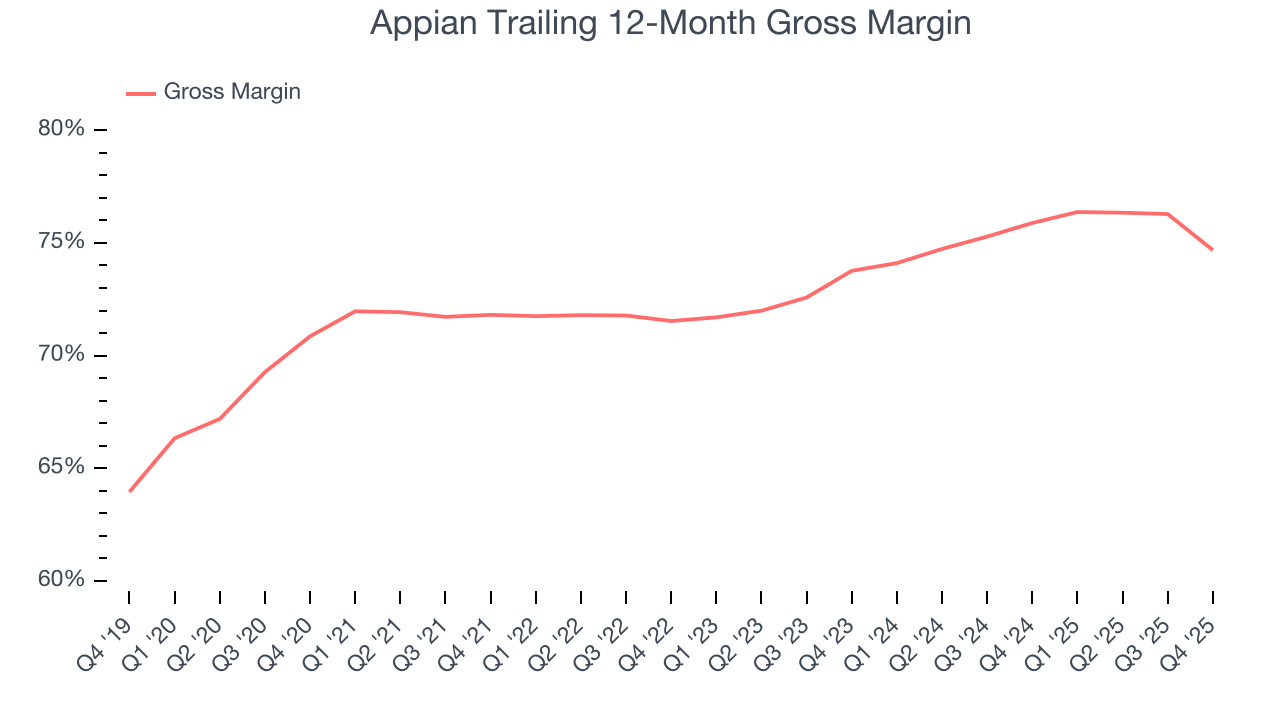

9. Gross Margin & Pricing Power

For software companies like Appian, gross profit tells us how much money remains after paying for the base cost of products and services (typically servers, licenses, and certain personnel). These costs are usually low as a percentage of revenue, explaining why software is more lucrative than other sectors.

Appian’s gross margin is better than the broader software industry and signals it has solid unit economics and competitive products. As you can see below, it averaged a decent 74.7% gross margin over the last year. Said differently, Appian paid its providers $25.32 for every $100 in revenue.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. Appian has seen gross margins improve by 0.9 percentage points over the last 2 year, which is slightly better than average for software.

In Q4, Appian produced a 72.4% gross profit margin, down 6.1 percentage points year on year. Appian’s full-year margin has also been trending down over the past 12 months, decreasing by 1.2 percentage points. If this move continues, it could suggest a more competitive environment with some pressure to lower prices and higher input costs.

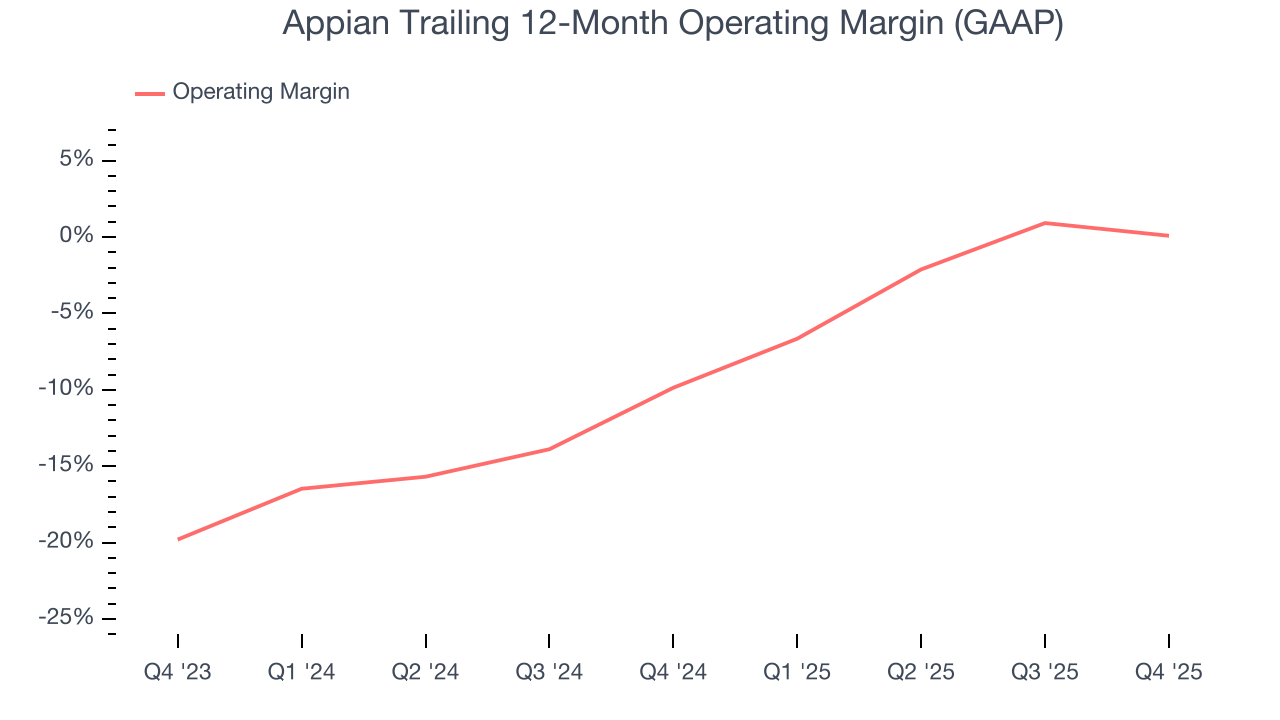

10. Operating Margin

While many software businesses point investors to their adjusted profits, which exclude stock-based compensation (SBC), we prefer GAAP operating margin because SBC is a legitimate expense used to attract and retain talent. This is one of the best measures of profitability because it shows how much money a company takes home after developing, marketing, and selling its products.

Appian was roughly breakeven when averaging the last year of quarterly operating profits, decent for a software business.

Analyzing the trend in its profitability, Appian’s operating margin rose by 9.9 percentage points over the last two years, as its sales growth gave it operating leverage.

In Q4, Appian’s breakeven margin was -0.3%, down 3.4 percentage points year on year. Since Appian’s gross margin decreased more than its operating margin, we can assume its recent inefficiencies were driven more by weaker leverage on its cost of sales rather than increased marketing, R&D, and administrative overhead expenses.

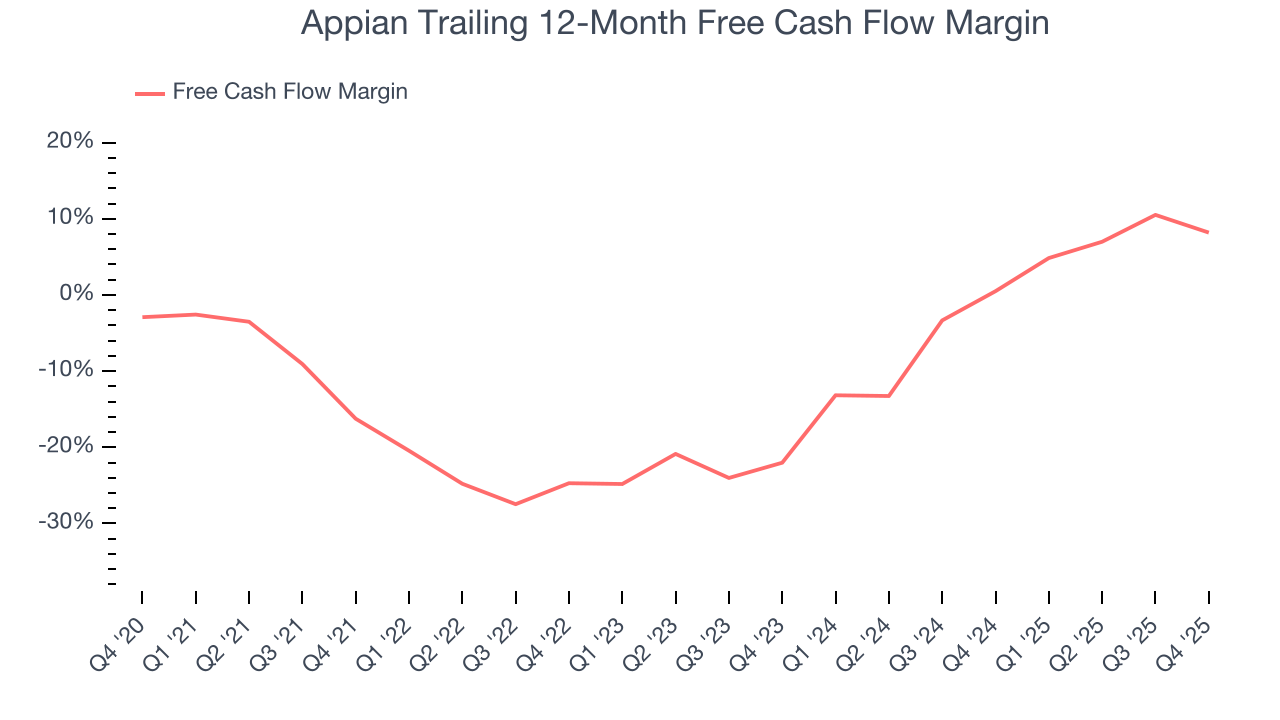

11. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Appian has shown weak cash profitability over the last year, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 8.2%, subpar for a software business.

Appian broke even from a free cash flow perspective in Q4. The company’s cash profitability regressed as it was 7.9 percentage points lower than in the same quarter last year, prompting us to pay closer attention. Short-term fluctuations typically aren’t a big deal because investment needs can be seasonal, but we’ll be watching to see if the trend extrapolates into future quarters.

Over the next year, analysts’ consensus estimates show they’re expecting Appian’s free cash flow margin of 8.2% for the last 12 months to remain the same.

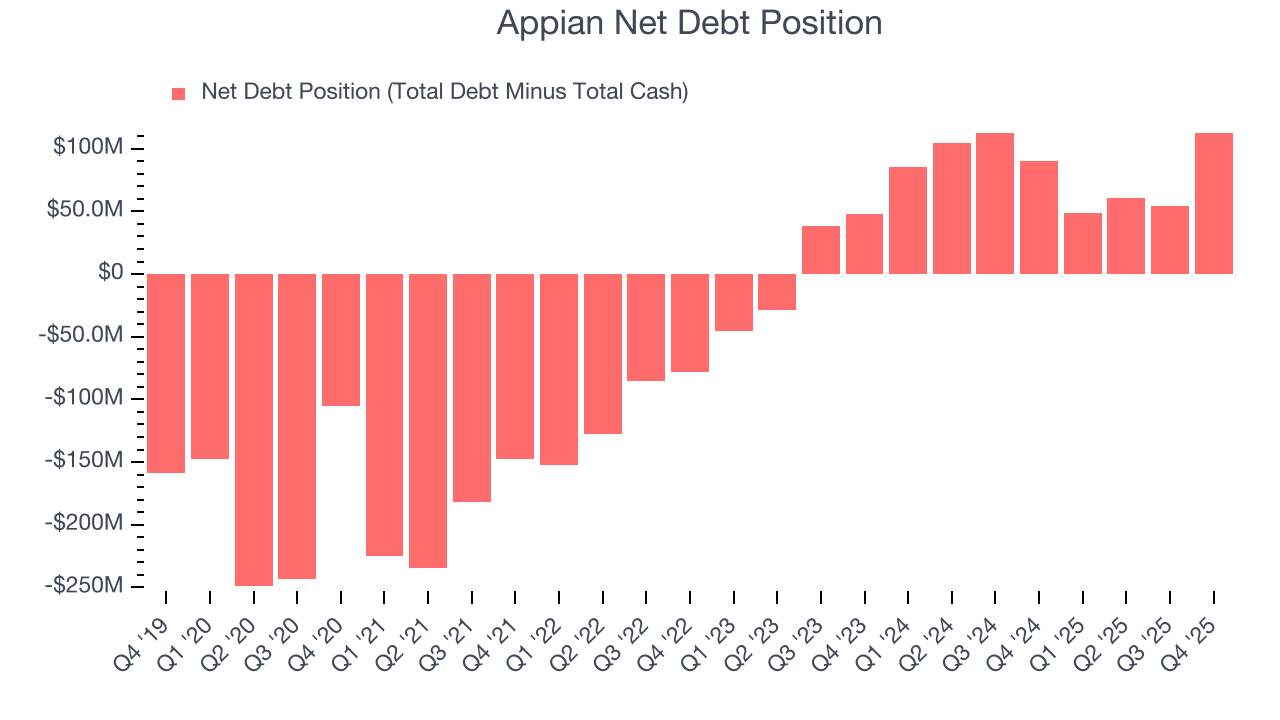

12. Balance Sheet Assessment

Appian reported $187.2 million of cash and $299.7 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $76.8 million of EBITDA over the last 12 months, we view Appian’s 1.5× net-debt-to-EBITDA ratio as safe. We also see its $11.05 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

13. Key Takeaways from Appian’s Q4 Results

We were impressed by Appian’s optimistic EBITDA guidance for next quarter, which blew past analysts’ expectations. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. On the other hand, its revenue guidance for next year suggests a significant slowdown in demand. Zooming out, we think this quarter featured some important positives. The stock traded up 14.3% to $27.50 immediately following the results.

14. Is Now The Time To Buy Appian?

Updated: March 15, 2026 at 10:16 PM EDT

Before deciding whether to buy Appian or pass, we urge investors to consider business quality, valuation, and the latest quarterly results.

Appian isn’t a terrible business, but it doesn’t pass our quality test. Although its revenue growth was solid over the last five years, it’s expected to deteriorate over the next 12 months and its customer acquisition is less efficient than many comparable companies. On top of that, the company’s low free cash flow margins give it little breathing room.

Appian’s price-to-sales ratio based on the next 12 months is 2.3x. While this valuation is fair, the upside isn’t great compared to the potential downside. We're fairly confident there are better investments elsewhere.

Wall Street analysts have a consensus one-year price target of $31 on the company (compared to the current share price of $25.59).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.