Macy's (NYSE:M) Q2: Beats On Revenue But Stock Drops

Anthony Lee /

August 22, 2023

Department store chain Macy’s (NYSE:M) beat analysts' expectations in Q2 FY2023, with revenue down 9.03% year on year to $5.28 billion. On the other hand, its full-year revenue guidance of $23 billion at the midpoint came in 0.97% below analysts' estimates. Macy's made a GAAP loss of $22 million, down from its profit of $275 million in the same quarter last year.

Is now the time to buy Macy's? Find out in our full research available to StockStory Edge members.

Macy's (M) Q2 FY2023 Highlights:

- Revenue: $5.28 billion vs analyst estimates of $5.11 billion (3.33% beat)

- EPS (non-GAAP): $0.26 vs analyst estimates of $0.14 ($0.12 beat)

- The company reconfirmed revenue guidance for the full year of $23 billion at the midpoint

- Free Cash Flow was -$183 million compared to -$152 million in the same quarter last year

- Gross Margin (GAAP): 39.8%, down from 41% in the same quarter last year

- Same-Store Sales were down 8.2% year on year

“In the second quarter, we delivered better-than-expected top and bottom-line results. Our teams surgically implemented clearance markdowns and promotions to effectively clear spring seasonal receipts and ensure fresh assortments for the fall and Holiday seasons” said Jeff Gennette, chairman and chief executive officer of Macy’s.

With a storied history that began with its 1858 founding, Macy’s (NYSE:M) is a department store chain that sells clothing, cosmetics, accessories, and home goods.

Department stores emerged in the 19th century to provide customers with a wide variety of merchandise under one roof, offering a convenient and luxurious shopping experience. They played an important role in the history of American retail and urbanization, and prior to department stores, retailers tended to sell narrow specialty and niche items. But what was once new is now old, and department stores are somewhat considered a relic of the past. They are being attacked from multiple angles–stagnant foot traffic at malls where they’ve served as anchors; more nimble off-price and fast-fashion retailers; and e-commerce-first competitors not burdened by large physical footprints.

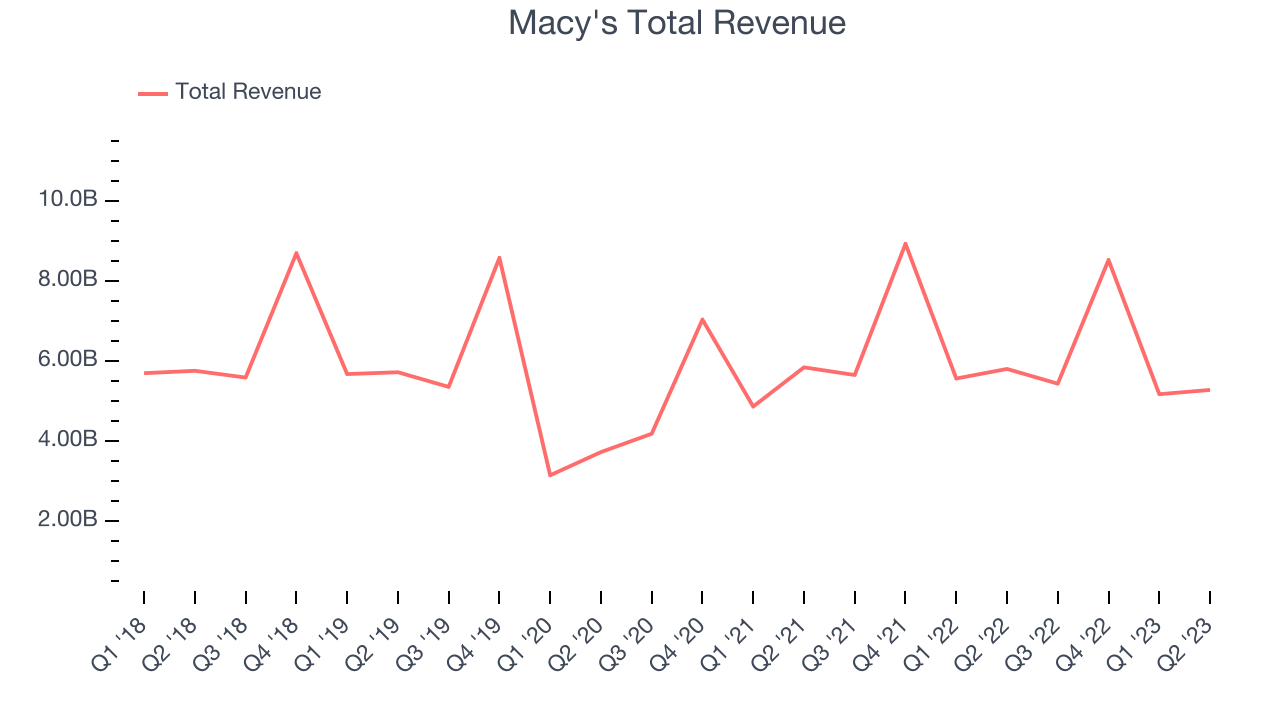

Sales Growth

Macy's is one of the larger companies in the consumer retail industry and benefits from economies of scale, enabling it to gain more leverage on fixed costs and offer consumers lower prices.

As you can see below, the company's revenue has declined over the last four years, dropping 1.26% annually .

This quarter, Macy's revenue fell 9.03% year on year to $5.28 billion but beat Wall Street's estimates by 3.33%. Looking ahead, Wall Street expects revenue to decline 5.05% over the next 12 months.

While most things went back to how they were before the pandemic, a few consumer habits fundamentally changed. One founder-led company is benefiting massively from this shift and is set to beat the market for years to come. The business has grown astonishingly fast, with 40%+ free cash flow margins, and its fundamentals are undoubtedly best-in-class. Still, its total addressable market is so big that the company has room to grow many times in size. You can find it on our platform for free.

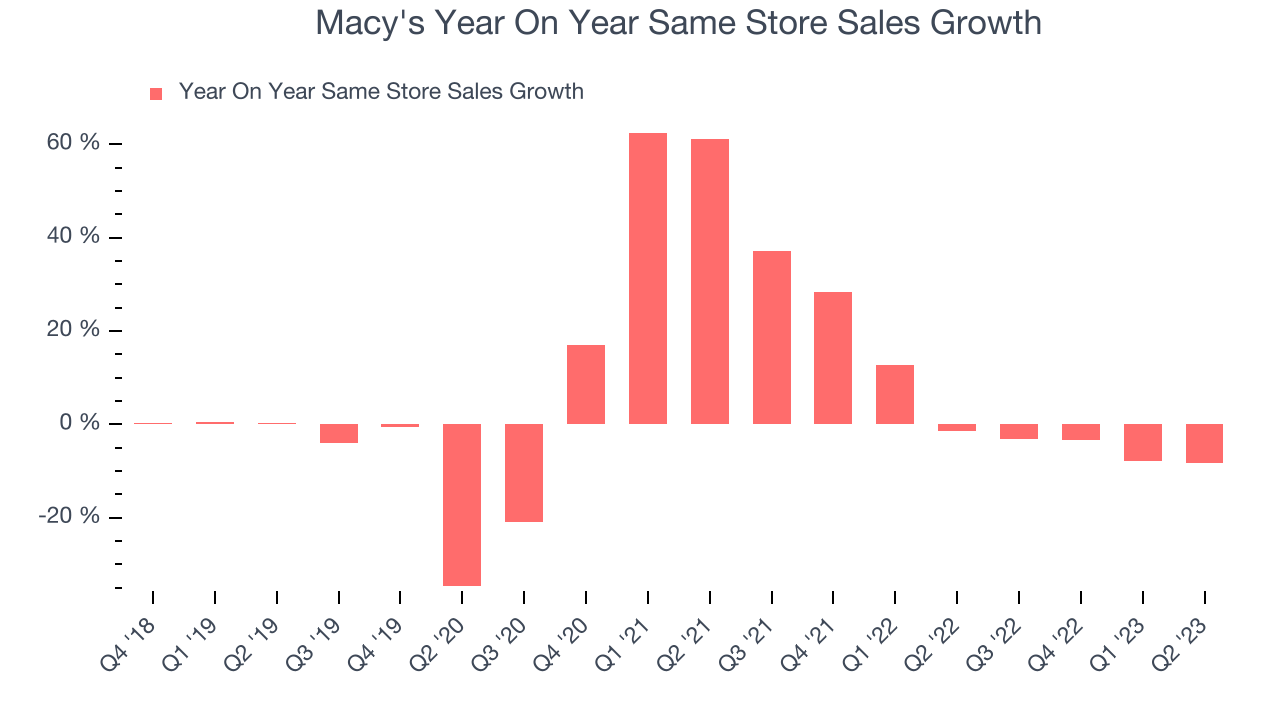

Same-Store Sales

Same-store sales growth is an important metric that tracks demand for a retailer's established brick-and-mortar stores and e-commerce platform.

Macy's demand within its existing stores has generally risen over the last two years but lagged behind the broader consumer retail sector. On average, the company's same-store sales have grown by 6.79% year on year.

In the latest quarter, Macy's same-store sales fell 8.2% year on year. This decrease was a further deceleration from the 1.5% year-on-year decline it had posted 12 months ago. We hope the business can get back on track.

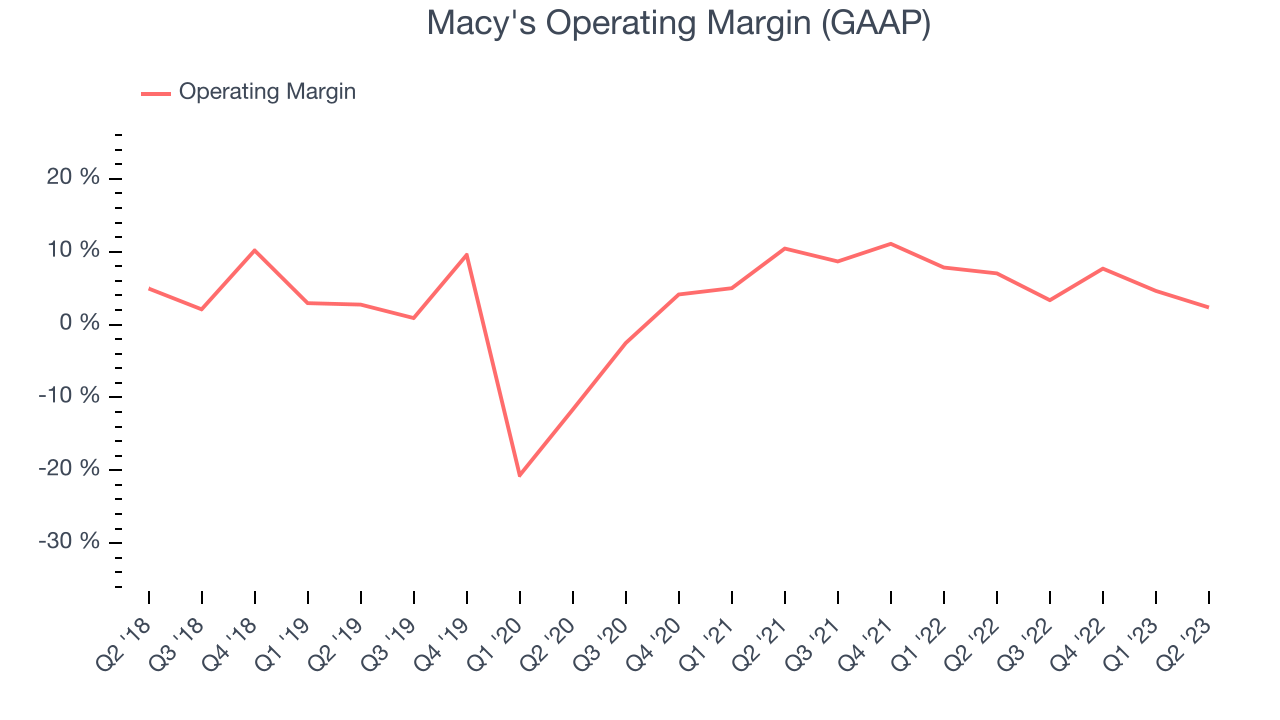

Operating Margin

Operating margin is an important measure of profitability for retailers as it accounts for all expenses that keep the lights on, including wages, rent, advertising, and other administrative costs.

This quarter, Macy's generated an operating profit margin of 2.35%, down 4.7 percentage points year on year. We can infer that Macy's was less efficient with its expenses or had lower leverage on its fixed costs because its operating margin decreased more than its gross margin.

From an operational perspective, Macy's was profitable but held back because of its expense base over the last two years. The company has produced an average operating margin of 6.58%, mediocre for a consumer retail business.

From an operational perspective, Macy's was profitable but held back because of its expense base over the last two years. The company has produced an average operating margin of 6.58%, mediocre for a consumer retail business.Key Takeaways from Macy's Q2 Results

Sporting a market capitalization of $4.01 billion, Macy's is among smaller companies, but its more than $438 million in cash on hand and positive free cash flow over the last 12 months puts it in an attractive position to invest in growth.

We were impressed by how significantly Macy's blew past analysts' EPS and EBITDA expectations this quarter. That really stood out as a positive in these results. On the other hand, its full-year revenue guidance missed analysts' expectations. Like in the previous quarter, Macy's management team called out the uncertain macro environment, causing investors to worry. The company is down 7.84% on the results and currently trades at $13.57 per share.

So should you invest in Macy's right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.

The author has no position in any of the stocks mentioned in this report.