Guardant Health (GH)

Guardant Health is intriguing, but its negative EBITDA and debt balance put it in a tough position.― StockStory Analyst Team

1. News

2. Summary

Why Guardant Health Is Not Exciting

Pioneering the field of "liquid biopsy" with technology that can identify cancer-specific genetic mutations from a simple blood draw, Guardant Health (NASDAQ:GH) develops blood tests that detect and monitor cancer by analyzing tumor DNA in the bloodstream, helping doctors make treatment decisions without invasive biopsies.

- Historical adjusted operating margin losses point to an inefficient cost structure

- Negative free cash flow raises questions about the return timeline for its investments

- Negative earnings profile makes it challenging to secure favorable financing terms from lenders

Guardant Health shows some promise. However, we’d hold off on buying the stock until its EBITDA can comfortably service its debt.

Why There Are Better Opportunities Than Guardant Health

Guardant Health is trading at $85.73 per share, or 8.5x forward price-to-sales. The market typically values companies like Guardant Health based on their anticipated profits for the next 12 months, but it expects the business to lose money. We also think the upside isn’t great compared to the potential downside here - there are more exciting stocks to buy.

Paying a premium for high-quality companies with strong long-term earnings potential is preferable to owning challenged businesses with questionable prospects.

3. Guardant Health (GH) Research Report: Q4 CY2025 Update

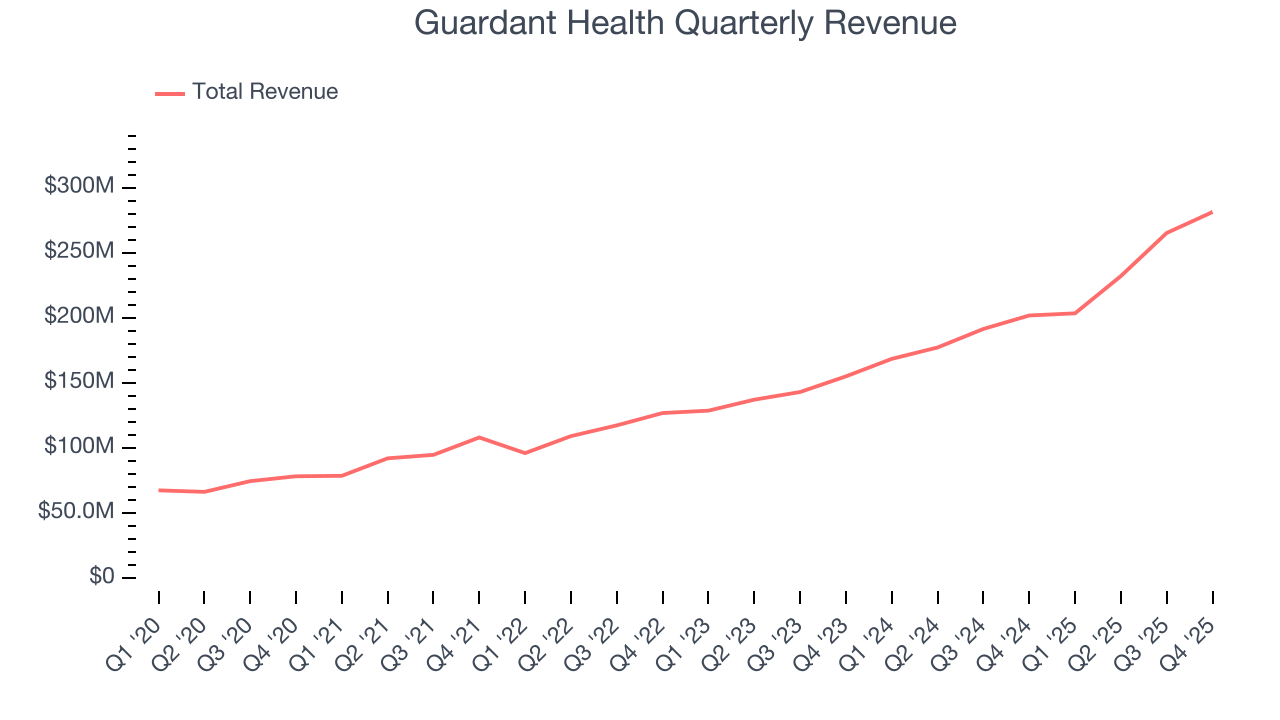

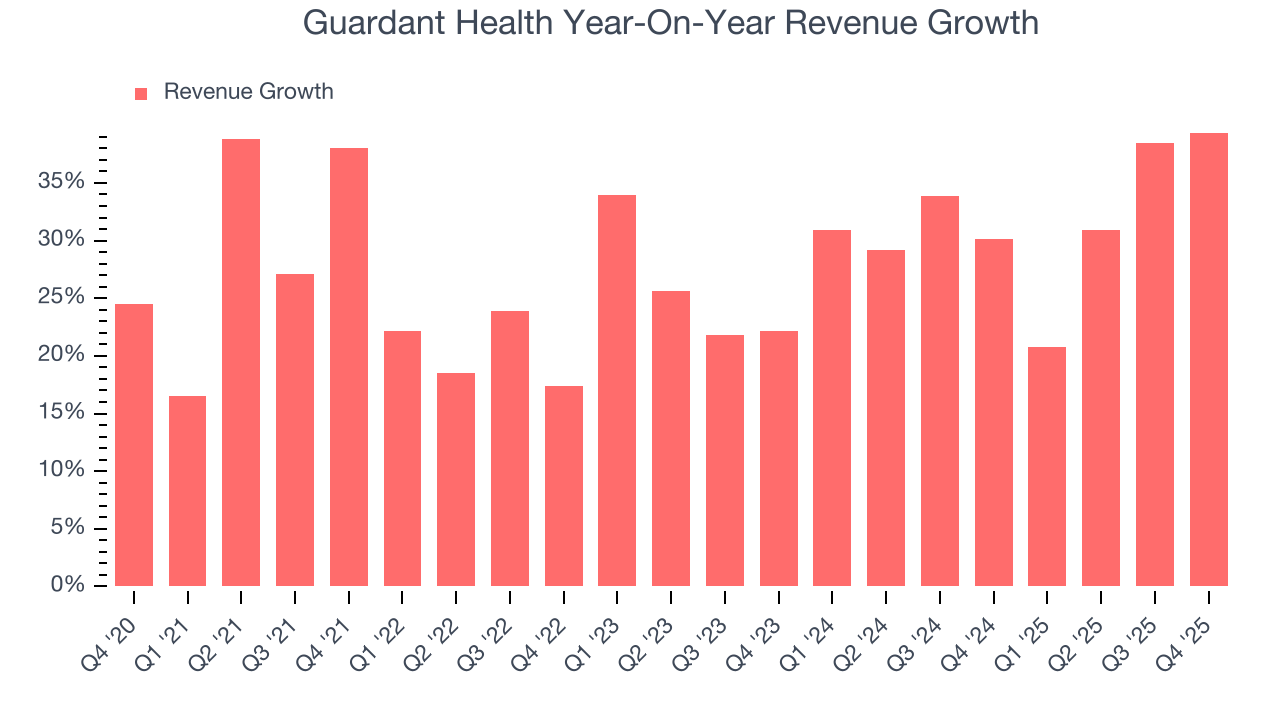

Diagnostics company Guardant Health (NASDAQ:GH) announced better-than-expected revenue in Q4 CY2025, with sales up 39.4% year on year to $281.3 million. The company’s full-year revenue guidance of $1.27 billion at the midpoint came in 1.8% above analysts’ estimates. Its non-GAAP loss of $0.50 per share was 6.5% below analysts’ consensus estimates.

Guardant Health (GH) Q4 CY2025 Highlights:

- Revenue: $281.3 million vs analyst estimates of $271.7 million (39.4% year-on-year growth, 3.5% beat)

- Adjusted EPS: -$0.50 vs analyst expectations of -$0.47 (6.5% miss)

- Adjusted EBITDA: -$64.91 million (-23.1% margin, 17.2% year-on-year growth)

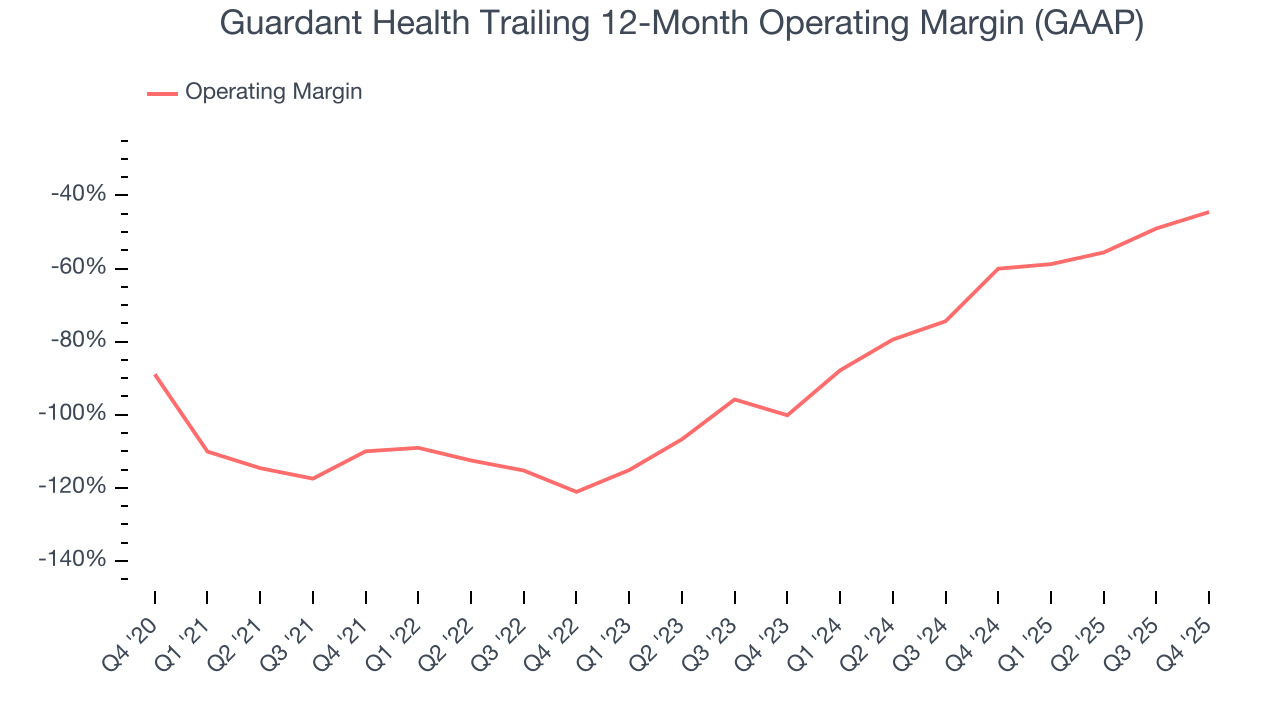

- Operating Margin: -43%, up from -62.4% in the same quarter last year

- Free Cash Flow was -$54.22 million compared to -$83.39 million in the same quarter last year

- Market Capitalization: $13.84 billion

Company Overview

Pioneering the field of "liquid biopsy" with technology that can identify cancer-specific genetic mutations from a simple blood draw, Guardant Health (NASDAQ:GH) develops blood tests that detect and monitor cancer by analyzing tumor DNA in the bloodstream, helping doctors make treatment decisions without invasive biopsies.

Guardant Health's technology platform analyzes circulating tumor DNA (ctDNA) that cancer cells release into the bloodstream. This approach offers significant advantages over traditional tissue biopsies, which can be invasive, risky, and sometimes impossible to obtain. The company's flagship Guardant360 tests help oncologists match patients with advanced cancers to appropriate targeted therapies and immunotherapies based on the specific genetic mutations driving their tumors.

For patients with early-stage cancer, Guardant's Reveal test monitors for minimal residual disease after surgery or treatment, detecting microscopic cancer cells that might indicate recurrence months before they would be visible on imaging scans. This early warning system allows doctors to intervene sooner when cancer returns, potentially improving survival outcomes.

The company has also entered the cancer screening market with its Shield blood test for colorectal cancer detection. Unlike traditional colonoscopies, which many eligible patients avoid due to their invasive nature, Shield requires only a blood sample. The test uses both genomic and epigenomic signals to identify cancer markers, and has demonstrated 83% sensitivity in detecting colorectal cancer in clinical studies.

Beyond serving individual patients, Guardant provides tools for pharmaceutical companies developing cancer therapies. Its GuardantOMNI and GuardantINFINITY tests offer comprehensive genomic profiling to support clinical trials and drug development. The GuardantINFORM platform aggregates real-world data from thousands of cancer patients, helping researchers understand treatment outcomes and resistance patterns.

Guardant's business model generates revenue through both clinical testing services and biopharmaceutical partnerships. When oncologists order tests for their patients, Guardant bills insurance companies or patients directly. The company also contracts with drug developers who use its tests in clinical trials or access its anonymized patient data for research purposes.

The company has expanded internationally, establishing partnerships with cancer centers in Europe and Asia. In Japan, Guardant has received regulatory approval for its Guardant360 CDx test as a companion diagnostic for several cancer therapies, and the Japanese government has approved national reimbursement for the test.

4. Testing & Diagnostics Services

The testing and diagnostics services industry plays a crucial role in disease detection, monitoring, and prevention, serving hospitals, clinics, and individual consumers. This sector benefits from stable demand, driven by an aging population, increased prevalence of chronic diseases, and growing awareness of preventive healthcare. Recurring revenue streams come from routine screenings, lab tests, and diagnostic imaging, with reimbursement from Medicare, Medicaid, private insurance, and out-of-pocket payments. However, the industry faces challenges such as pricing pressures, regulatory compliance, and the need for continuous investment in new testing technologies. Looking ahead, industry tailwinds include the expansion of personalized medicine, increased adoption of at-home and rapid diagnostic tests, and advancements in AI-driven diagnostics that enhance accuracy and efficiency. However, headwinds such as reimbursement uncertainties, competition from decentralized testing solutions, and regulatory scrutiny over test validity and cost-effectiveness may impact profitability. Adapting to evolving healthcare models and integrating automation will be key for sustaining growth and maintaining operational efficiency.

Guardant Health competes with other liquid biopsy providers including Foundation Medicine (owned by Roche), Thermo Fisher Scientific (NYSE:TMO), and Exact Sciences (NASDAQ:EXAS). In the minimal residual disease testing space, competitors include Natera (NASDAQ:NTRA) and NeoGenomics (NASDAQ:NEO), while in cancer screening, GRAIL (owned by Illumina) and Freenome are significant rivals.

5. Revenue Scale

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With just $982 million in revenue over the past 12 months, Guardant Health is a small company in an industry where scale matters. This makes it difficult to build trust with customers because healthcare is heavily regulated, complex, and resource-intensive.

6. Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Thankfully, Guardant Health’s 27.9% annualized revenue growth over the last five years was exceptional. Its growth beat the average healthcare company and shows its offerings resonate with customers.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Guardant Health’s annualized revenue growth of 32% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

This quarter, Guardant Health reported wonderful year-on-year revenue growth of 39.4%, and its $281.3 million of revenue exceeded Wall Street’s estimates by 3.5%.

Looking ahead, sell-side analysts expect revenue to grow 26.6% over the next 12 months, a deceleration versus the last two years. Still, this projection is noteworthy and suggests the market is baking in success for its products and services.

7. Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Guardant Health’s high expenses have contributed to an average operating margin of negative 77.2% over the last five years. Unprofitable healthcare companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

On the plus side, Guardant Health’s operating margin rose by 65.5 percentage points over the last five years, as its sales growth gave it operating leverage. Zooming in on its more recent performance, we can see the company’s trajectory is intact as its margin has also increased by 55.6 percentage points on a two-year basis. These data points are very encouraging and show momentum is on its side.

This quarter, Guardant Health generated a negative 43% operating margin.

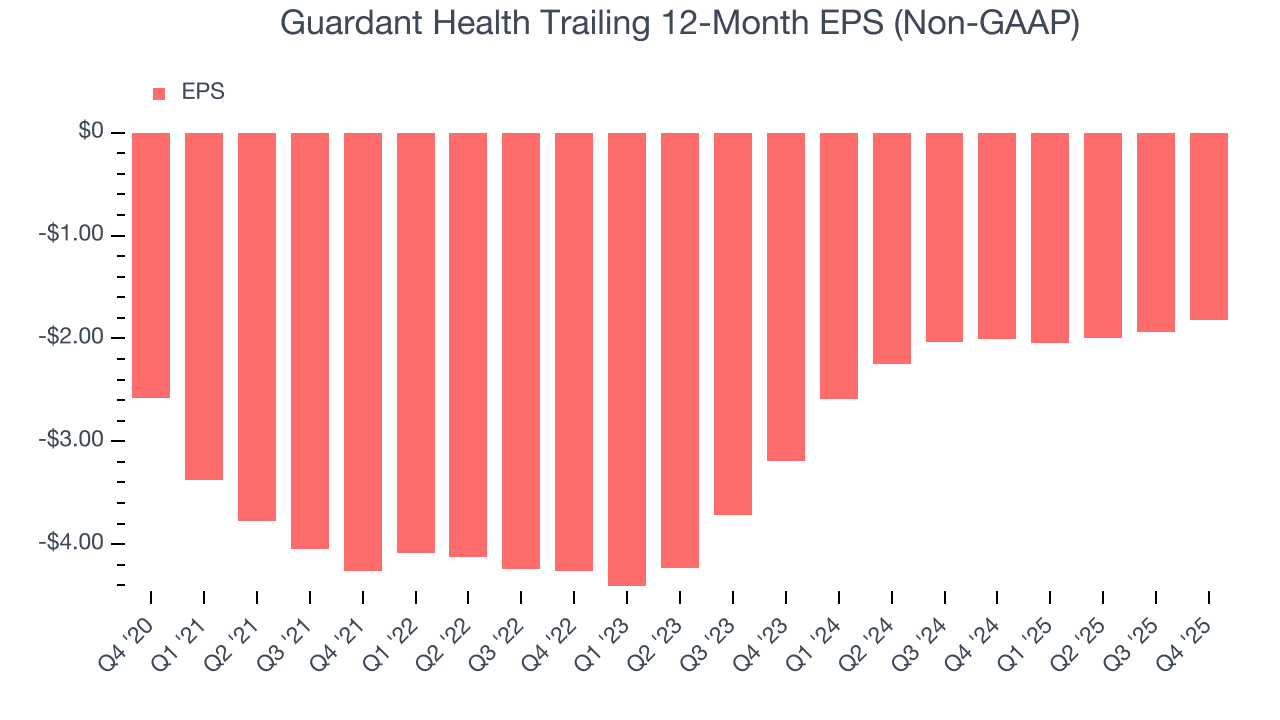

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Although Guardant Health’s full-year earnings are still negative, it reduced its losses and improved its EPS by 6.7% annually over the last five years. The next few quarters will be critical for assessing its long-term profitability. We hope to see an inflection point soon.

In Q4, Guardant Health reported adjusted EPS of negative $0.50, up from negative $0.62 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates. Over the next 12 months, Wall Street expects Guardant Health to improve its earnings losses. Analysts forecast its full-year EPS of negative $1.82 will advance to negative $1.44.

9. Cash Is King

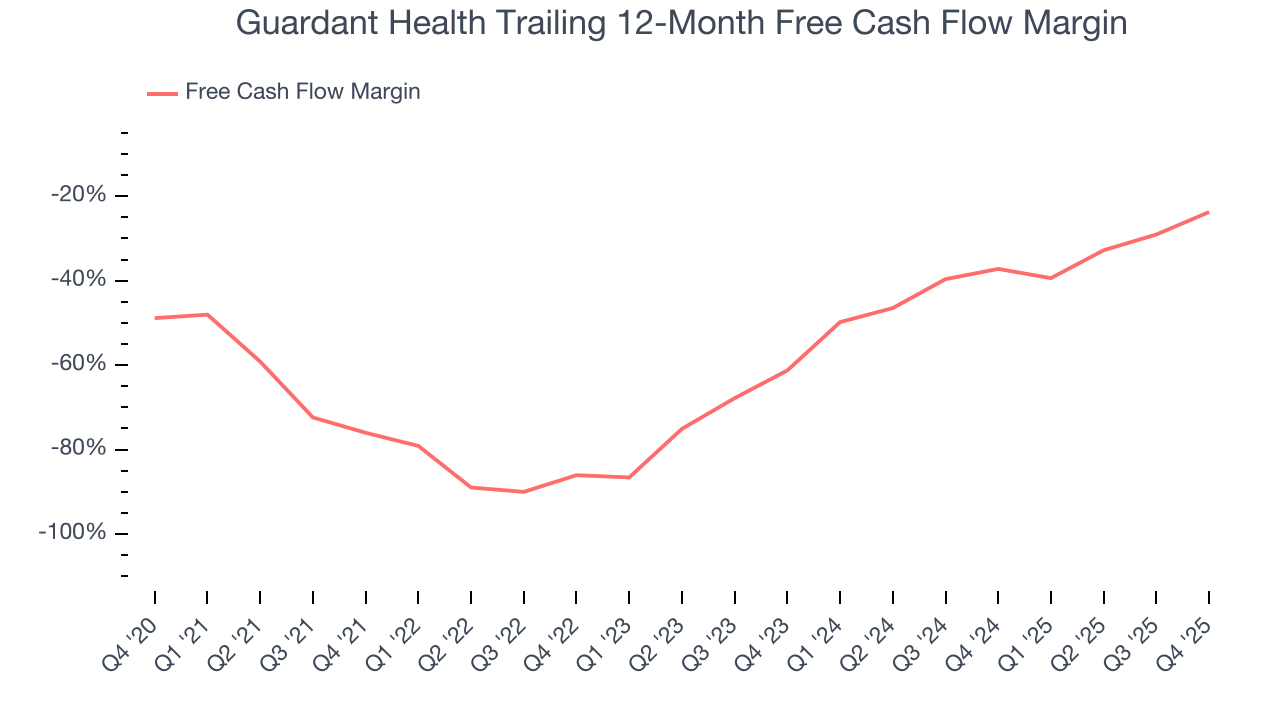

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Guardant Health’s demanding reinvestments have drained its resources over the last five years, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 49%, meaning it lit $49.05 of cash on fire for every $100 in revenue.

Taking a step back, an encouraging sign is that Guardant Health’s margin expanded by 52.3 percentage points during that time. In light of its glaring cash burn, however, this improvement is a bucket of hot water in a cold ocean.

Guardant Health burned through $54.22 million of cash in Q4, equivalent to a negative 19.3% margin. The company’s cash burn slowed from $83.39 million of lost cash in the same quarter last year.

10. Balance Sheet Risk

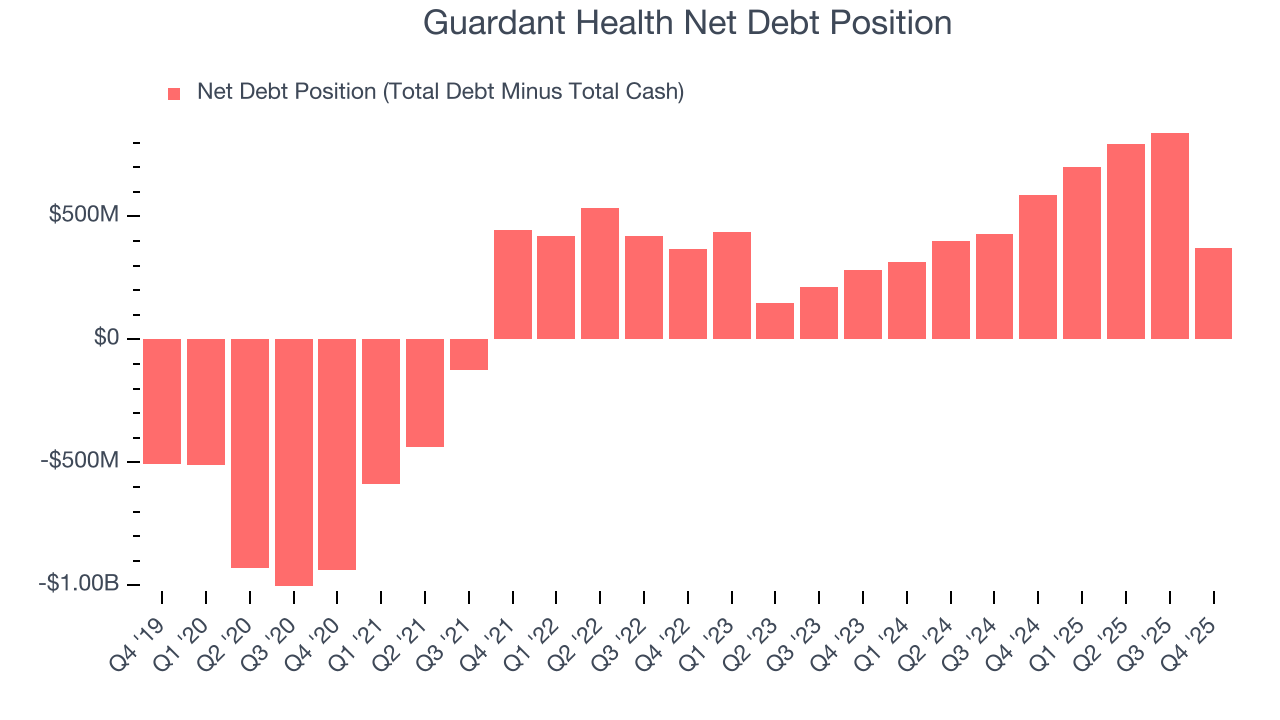

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

Guardant Health posted negative $220.9 million of EBITDA over the last 12 months, and its $1.68 billion of debt exceeds the $1.31 billion of cash on its balance sheet. This is a deal breaker for us because indebted loss-making companies spell trouble.

We implore our readers to tread carefully because credit agencies could downgrade Guardant Health if its unprofitable ways continue, making incremental borrowing more expensive and restricting growth prospects. The company could also be backed into a corner if the market turns unexpectedly. We hope Guardant Health can improve its profitability and remain cautious until then.

11. Key Takeaways from Guardant Health’s Q4 Results

We enjoyed seeing Guardant Health beat analysts’ revenue expectations this quarter. We were also glad its full-year revenue guidance exceeded Wall Street’s estimates. On the other hand, its EPS missed. Overall, this print had some key positives. The stock traded up 2.6% to $109.16 immediately after reporting.

12. Is Now The Time To Buy Guardant Health?

Updated: March 14, 2026 at 11:49 PM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Guardant Health.

Aside from its balance sheet, Guardant Health is a pretty good company. To begin with, its revenue growth was exceptional over the last five years, and its growth over the next 12 months is expected to accelerate. And while its operating margins reveal poor profitability compared to other healthcare companies, its rising cash profitability gives it more optionality. Additionally, Guardant Health’s expanding adjusted operating margin shows the business has become more efficient.

Guardant Health’s forward price-to-sales ratio is 8.5x. Certain aspects of its fundamentals are attractive, but we aren’t investing at the moment because its balance sheet makes us uneasy. If you’re interested in buying the stock, wait until it generates sufficient cash flows or raises some money.

Wall Street analysts have a consensus one-year price target of $132.57 on the company (compared to the current share price of $85.73).