News Corp (NWSA)

News Corp is up against the odds. Not only are its sales cratering but also its low returns on capital suggest it struggles to generate profits.― StockStory Analyst Team

1. News

2. Summary

Why We Think News Corp Will Underperform

Established in 2013 after a restructuring, News Corp (NASDAQ:NWSA) is a multinational conglomerate known for its news publishing, broadcasting, digital media, and book publishing.

- Sales stagnated over the last five years and signal the need for new growth strategies

- Responsiveness to unforeseen market trends is restricted due to its substandard operating margin profitability

- Lacking free cash flow limits its freedom to invest in growth initiatives, execute share buybacks, or pay dividends

News Corp’s quality is not up to our standards. There are more profitable opportunities elsewhere.

Why There Are Better Opportunities Than News Corp

News Corp is trading at $24.21 per share, or 19.8x forward P/E. This multiple is higher than that of consumer discretionary peers; it’s also rich for the top-line growth of the company. Not a great combination.

We’d rather invest in similarly-priced but higher-quality companies with more reliable earnings growth.

3. News Corp (NWSA) Research Report: Q4 CY2025 Update

Global media and publishing company News Corp (NASDAQ:NWSA) reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 5.5% year on year to $2.36 billion. Its GAAP profit of $0.34 per share was in line with analysts’ consensus estimates.

News Corp (NWSA) Q4 CY2025 Highlights:

- Revenue: $2.36 billion vs analyst estimates of $2.29 billion (5.5% year-on-year growth, 3% beat)

- EPS (GAAP): $0.34 vs analyst estimates of $0.34 (in line)

- Adjusted EBITDA: $517 million vs analyst estimates of $498.9 million (21.9% margin, 3.6% beat)

- Operating Margin: 10.2%, down from 16.3% in the same quarter last year

- Free Cash Flow Margin: 5.6%, down from 6.8% in the same quarter last year

- Market Capitalization: $14.33 billion

Company Overview

Established in 2013 after a restructuring, News Corp (NASDAQ:NWSA) is a multinational conglomerate known for its news publishing, broadcasting, digital media, and book publishing.

News Corp was created to focus on delivering news and media services in the digital age. At its core, it seeks to address the need for reliable news, diverse entertainment, and educational content.

The company's portfolio spans well-known news outlets such as The Wall Street Journal, TV stations, digital media platforms, and publishing houses. This wide range of perspectives and formats caters to diverse consumer preferences for both traditional and digital media.

News Corp generates revenue through advertising, licensing fees, and subscription fees. Some of its content can also be purchased on a one-off basis.

4. Media

The advent of the internet changed how shows, films, music, and overall information flow. As a result, many media companies now face secular headwinds as attention shifts online. Some have made concerted efforts to adapt by introducing digital subscriptions, podcasts, and streaming platforms. Time will tell if their strategies succeed and which companies will emerge as the long-term winners.

Competitors in the news publishing and media sector include The New York Times (NYSE:NYT), Gannett (NYSE:GCI), and The E.W. Scripps (NASDAQ:SSP).

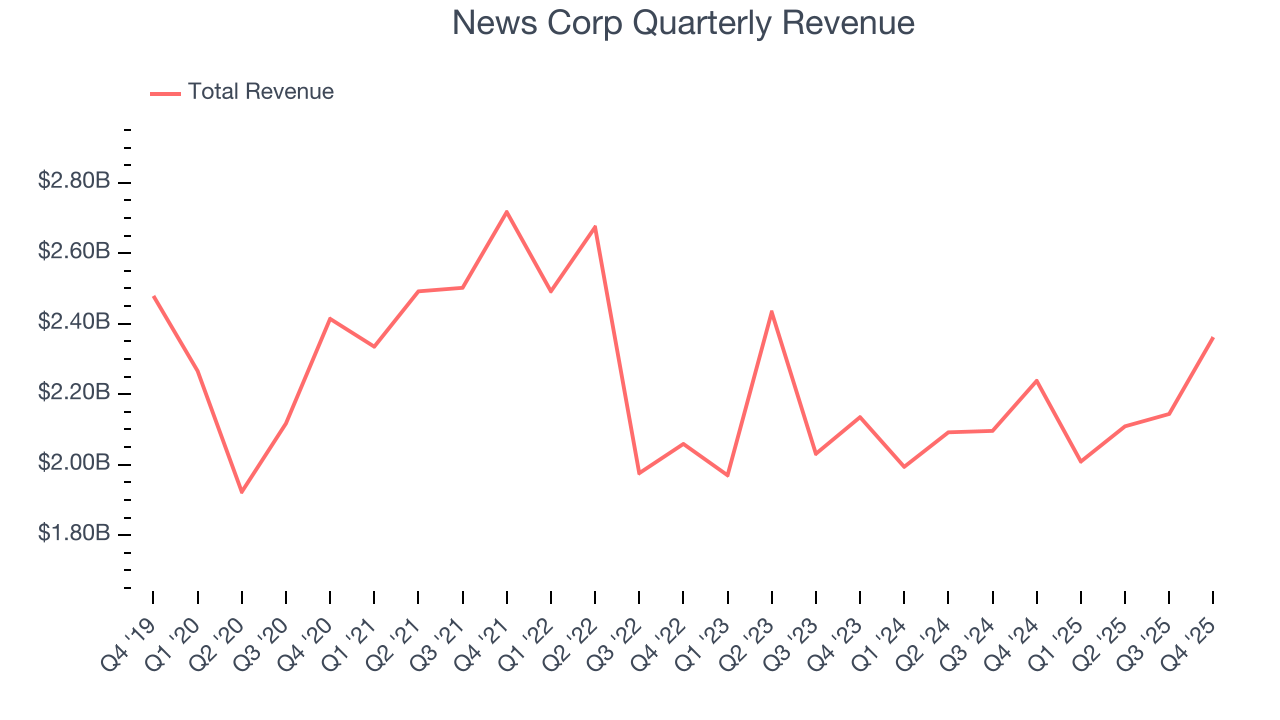

5. Revenue Growth

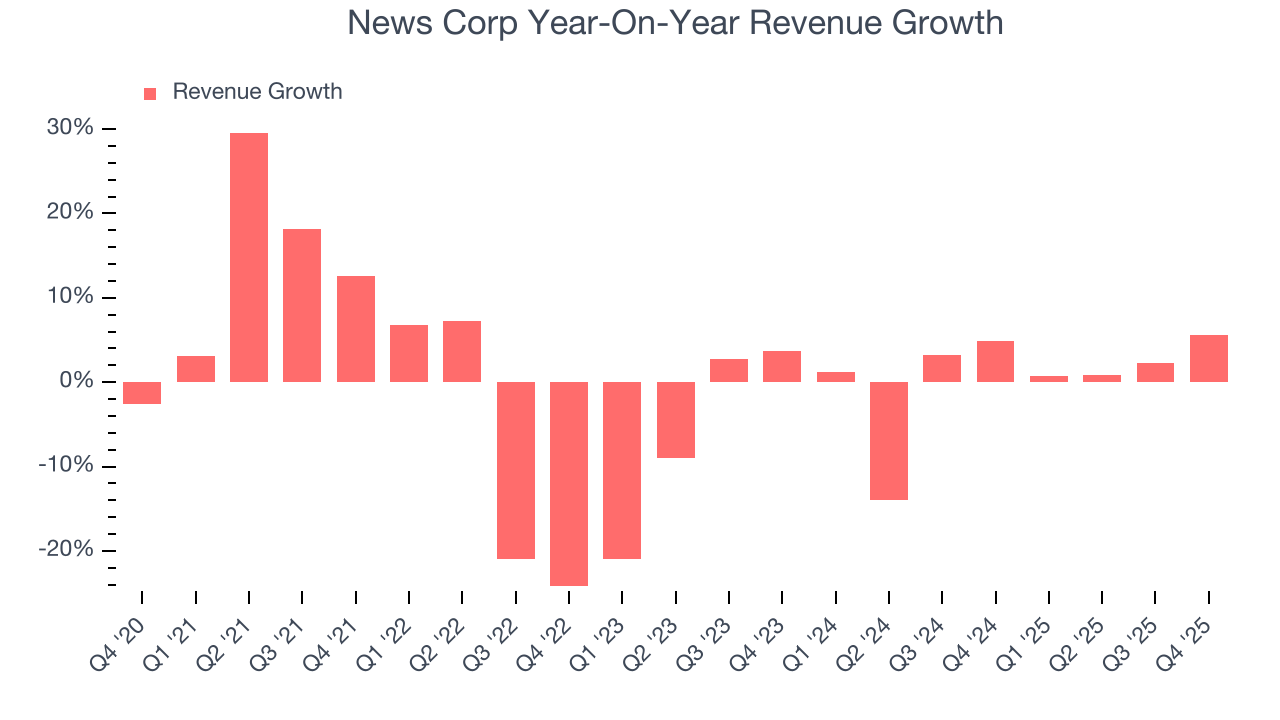

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Unfortunately, News Corp struggled to consistently increase demand as its $8.62 billion of sales for the trailing 12 months was close to its revenue five years ago. This wasn’t a great result and suggests it’s a low quality business.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Just like its five-year trend, News Corp’s revenue over the last two years was flat, suggesting it is in a slump.

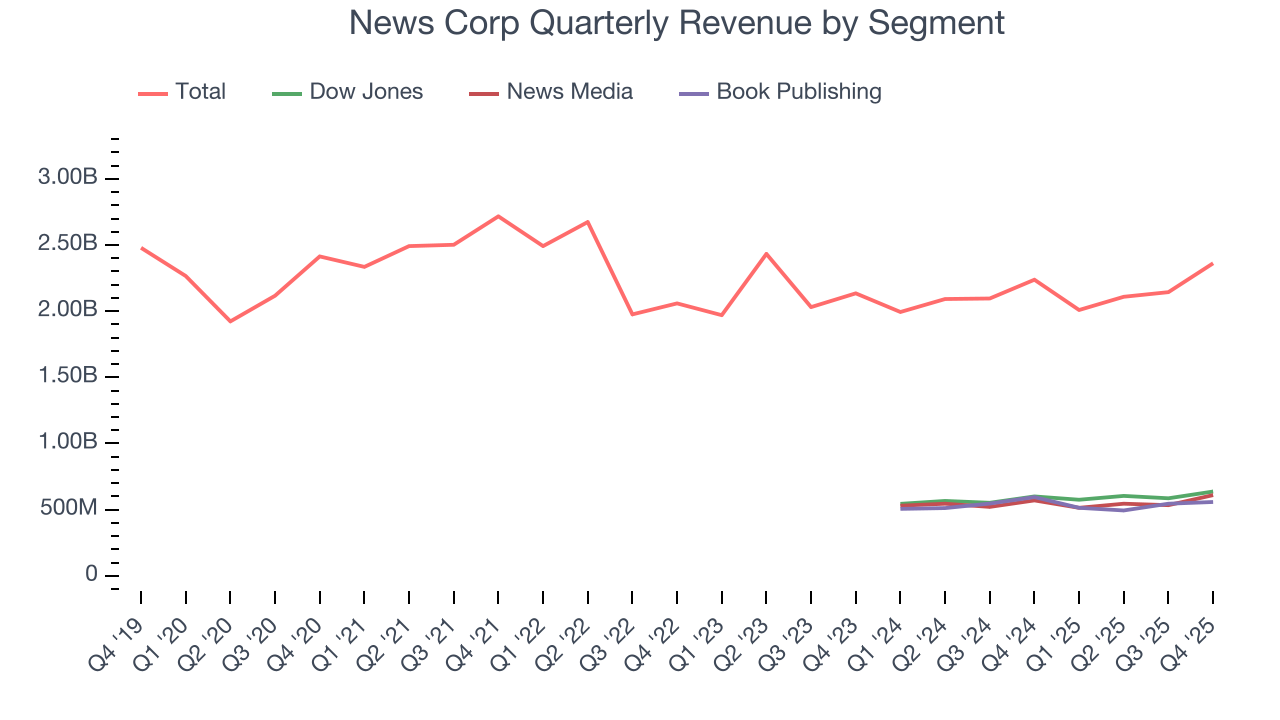

News Corp also breaks out the revenue for its three most important segments: Dow Jones, News Media, and Book Publishing, which are 27%, 25.8%, and 23.6% of revenue. Over the last two years, News Corp’s Dow Jones (media subsidiary) and News Media (general media) revenues averaged year-on-year growth of 6.2% and 1.6% while its Book Publishing revenue (general publishing) averaged 2.1% declines.

This quarter, News Corp reported year-on-year revenue growth of 5.5%, and its $2.36 billion of revenue exceeded Wall Street’s estimates by 3%.

Looking ahead, sell-side analysts expect revenue to grow 3% over the next 12 months. Although this projection indicates its newer products and services will spur better top-line performance, it is still below average for the sector.

6. Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

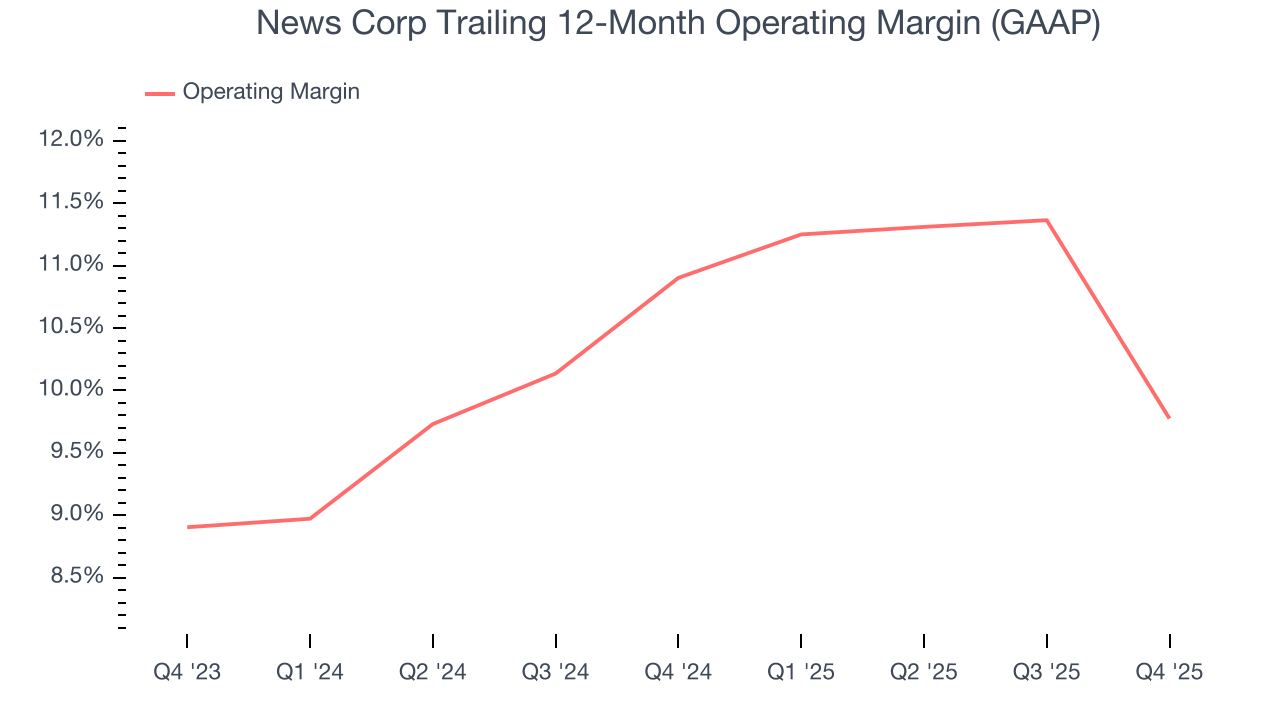

News Corp’s operating margin has been trending down over the last 12 months and averaged 10.3% over the last two years. The company’s profitability was mediocre for a consumer discretionary business and shows it couldn’t pass its higher operating expenses onto its customers.

In Q4, News Corp generated an operating margin profit margin of 10.2%, down 6.1 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

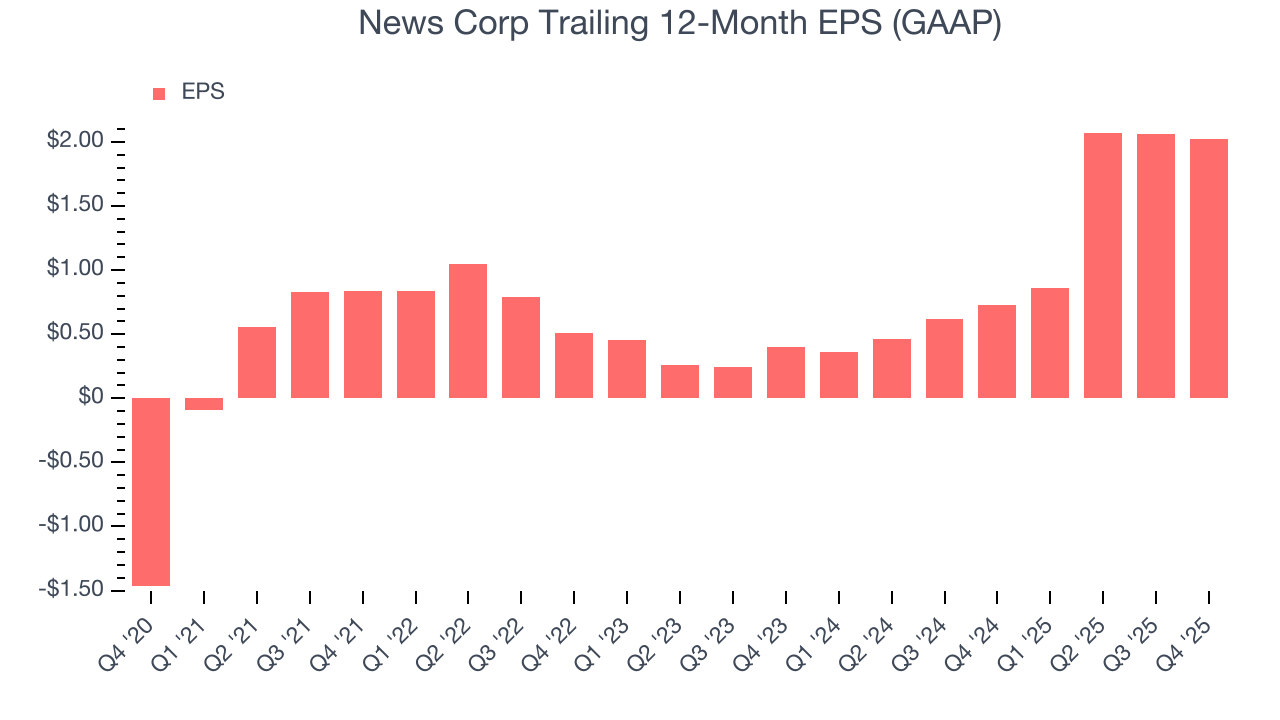

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

News Corp’s full-year EPS flipped from negative to positive over the last five years. This is encouraging and shows it’s at a critical moment in its life.

In Q4, News Corp reported EPS of $0.34, down from $0.38 in the same quarter last year. This print slightly missed analysts’ estimates. We also like to analyze expected EPS growth based on Wall Street analysts’ consensus projections, but there is insufficient data.

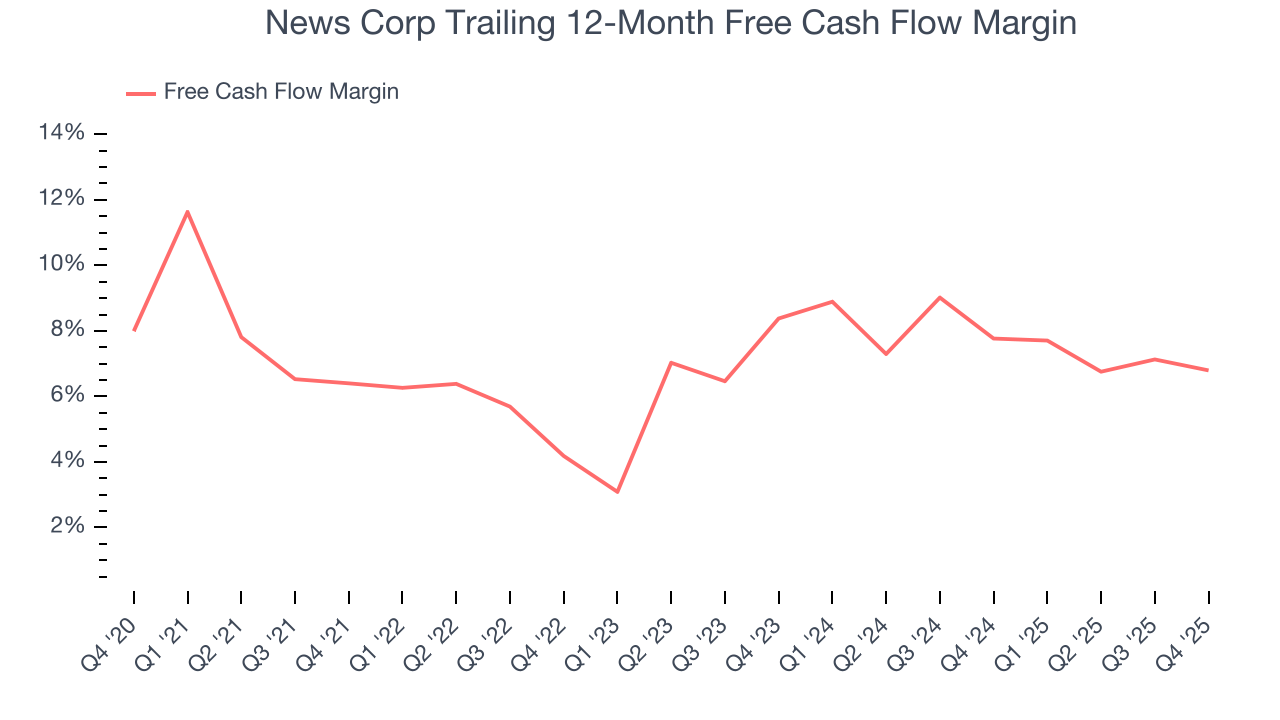

8. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

News Corp has shown poor cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 7.3%, lousy for a consumer discretionary business.

News Corp’s free cash flow clocked in at $132 million in Q4, equivalent to a 5.6% margin. The company’s cash profitability regressed as it was 1.2 percentage points lower than in the same quarter last year, prompting us to pay closer attention. Short-term fluctuations typically aren’t a big deal because investment needs can be seasonal, but we’ll be watching to see if the trend extrapolates into future quarters.

Over the next year, analysts predict News Corp’s cash conversion will slightly improve. Their consensus estimates imply its free cash flow margin of 6.8% for the last 12 months will increase to 9.1%, it options for capital deployment (investments, share buybacks, etc.).

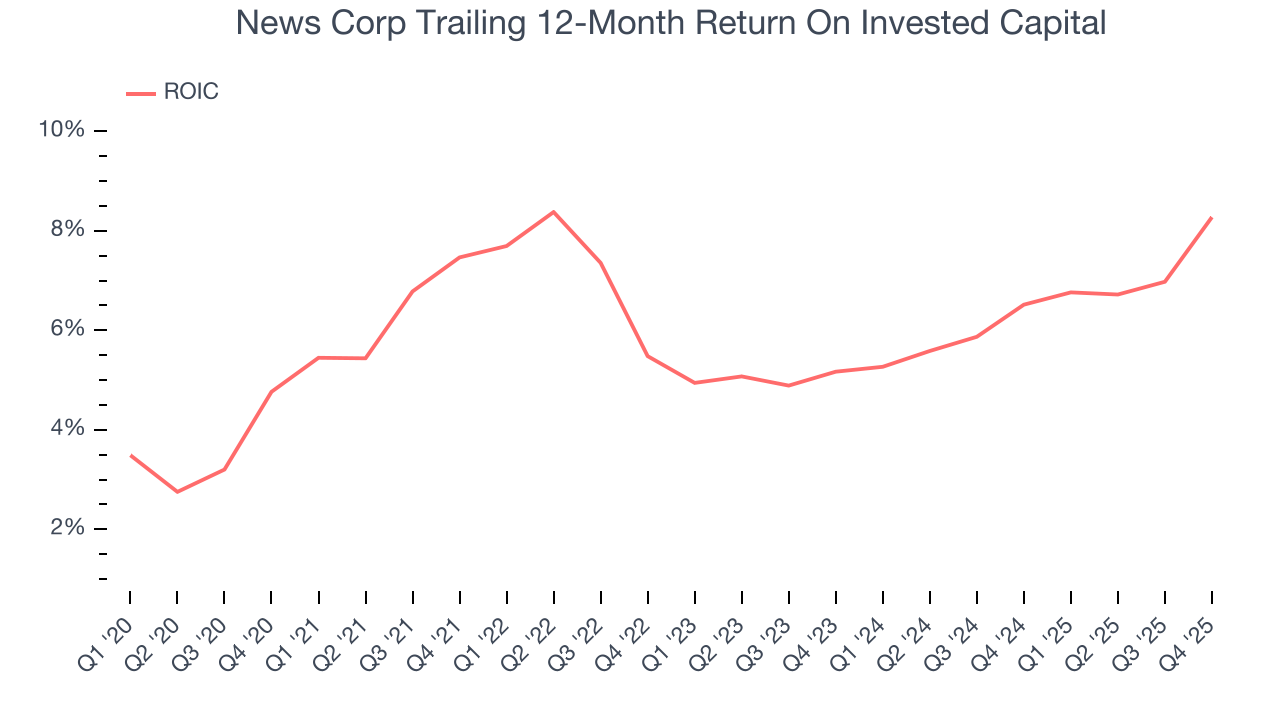

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

News Corp historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 6.6%, somewhat low compared to the best consumer discretionary companies that consistently pump out 25%+.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, News Corp’s ROIC has stayed the same over the last few years. If the company wants to become an investable business, it must improve its returns by generating more profitable growth.

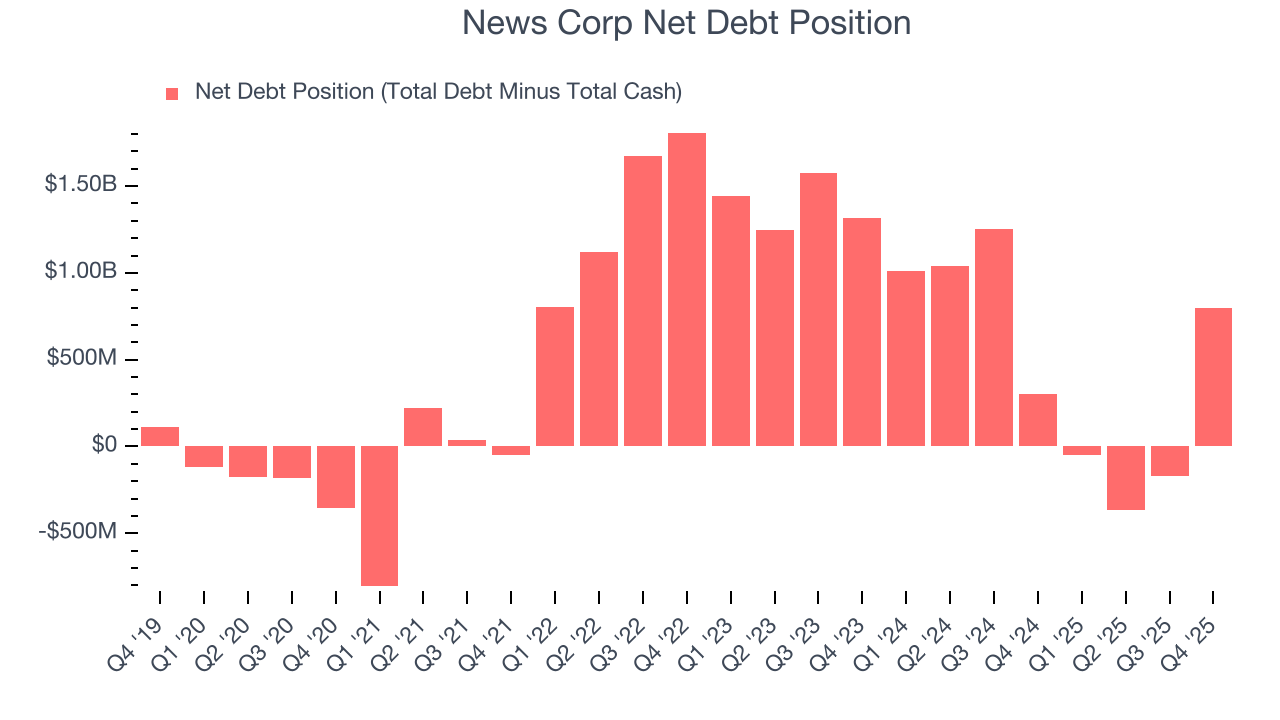

10. Balance Sheet Assessment

News Corp reported $2.05 billion of cash and $2.85 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $1.47 billion of EBITDA over the last 12 months, we view News Corp’s 0.5× net-debt-to-EBITDA ratio as safe. We also see its $21 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from News Corp’s Q4 Results

It was encouraging to see News Corp beat analysts’ revenue expectations this quarter. We were also happy its EBITDA outperformed Wall Street’s estimates. On the other hand, its EPS was in line. Overall, this print had some key positives. The stock traded up 1.3% to $24.94 immediately after reporting.

12. Is Now The Time To Buy News Corp?

Updated: March 16, 2026 at 11:12 PM EDT

We think that the latest earnings result is only one piece of the bigger puzzle. If you’re deciding whether to own News Corp, you should also grasp the company’s longer-term business quality and valuation.

We cheer for all companies serving everyday consumers, but in the case of News Corp, we’ll be cheering from the sidelines. On top of that, News Corp’s relatively low ROIC suggests management has struggled to find compelling investment opportunities, and its low free cash flow margins give it little breathing room.

News Corp’s P/E ratio based on the next 12 months is 19.8x. While this valuation is fair, the upside isn’t great compared to the potential downside. There are superior stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $34.05 on the company (compared to the current share price of $24.21).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.