Accel Entertainment (ACEL)

We wouldn’t buy Accel Entertainment. Its sales have underperformed and its low returns on capital show it has few growth opportunities.― StockStory Analyst Team

1. News

2. Summary

Why We Think Accel Entertainment Will Underperform

Established in Illinois, Accel Entertainment (NYSE:ACEL) is a provider of electronic gaming machines and interactive amusement terminals to bars and entertainment venues.

- 6.6% annual revenue growth over the last two years was slower than its consumer discretionary peers

- Operating margin falls short of the industry average, and the smaller profit dollars make it harder to react to unexpected market developments

- Poor free cash flow generation means it has few chances to reinvest for growth, repurchase shares, or distribute capital

Accel Entertainment is in the penalty box. Our attention is focused on better businesses.

Why There Are Better Opportunities Than Accel Entertainment

At $10.91 per share, Accel Entertainment trades at 12.5x forward P/E. This multiple is lower than most consumer discretionary companies, but for good reason.

Cheap stocks can look like great bargains at first glance, but you often get what you pay for. These mediocre businesses often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. Accel Entertainment (ACEL) Research Report: Q4 CY2025 Update

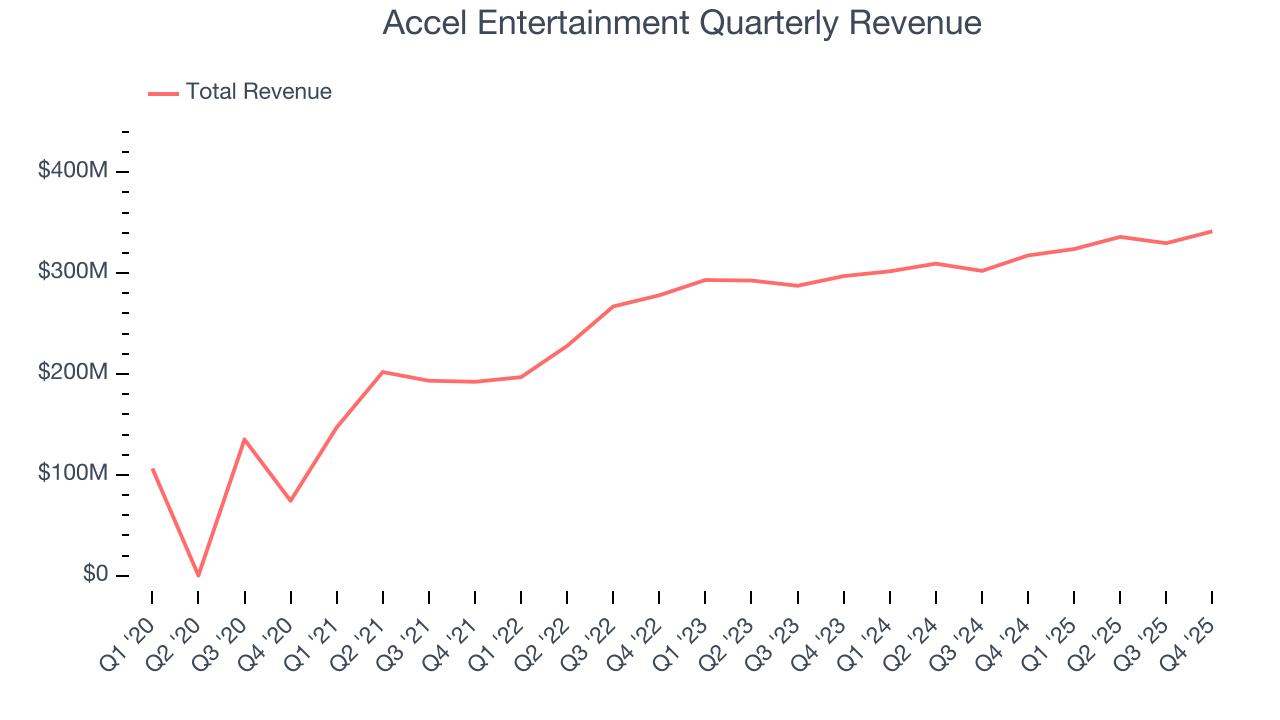

Slot machine and terminal operator Accel Entertainment (NYSE:ACEL) reported Q4 CY2025 results exceeding the market’s revenue expectations, with sales up 7.5% year on year to $341.4 million. Its GAAP profit of $0.19 per share was 29% above analysts’ consensus estimates.

Accel Entertainment (ACEL) Q4 CY2025 Highlights:

- Revenue: $341.4 million vs analyst estimates of $335.7 million (7.5% year-on-year growth, 1.7% beat)

- EPS (GAAP): $0.19 vs analyst estimates of $0.15 (29% beat)

- Adjusted EBITDA: $56.28 million vs analyst estimates of $51.15 million (16.5% margin, 10% beat)

- Operating Margin: 8.7%, up from 6.5% in the same quarter last year

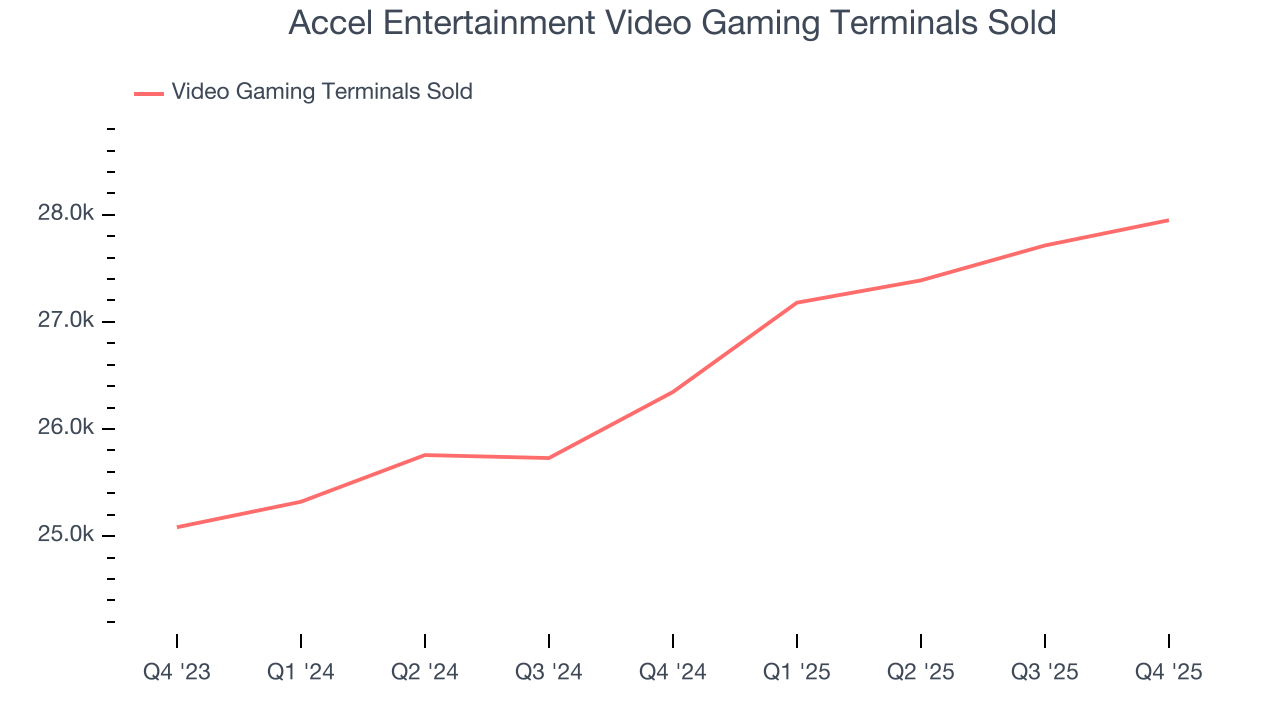

- Video Gaming Terminals Sold: 27,950, up 1,604 year on year

- Market Capitalization: $921.9 million

Company Overview

Established in Illinois, Accel Entertainment (NYSE:ACEL) is a provider of electronic gaming machines and interactive amusement terminals to bars and entertainment venues.

Accel Entertainment was founded to capitalize on new legislation in Illinois that permitted video gaming terminals (VGTs) in licensed non-casino locations such as bars, restaurants, and truck stops. This strategic move allowed the company to establish a foothold in a niche market, providing gaming solutions in environments different from traditional casinos.

The company specializes in providing an array of electronic gaming machines tailored for use in various entertainment settings. By offering engaging gaming experiences, it addresses the needs of venue owners seeking to enhance their customers' entertainment options. This service diversifies the entertainment experience for patrons and provides an additional revenue stream for venue operators.

Accel Entertainment’s revenue model is built on partnerships with venue operators. The company installs gaming machines at partner locations and participates in revenue share agreements, where it gets paid depending on how much money its machines win per day. This model is mutually beneficial as operators do not have to purchase these expensive machines outright, which can cost north of $10,000.

4. Consumer Discretionary - Gaming Solutions

The Consumer Discretionary sector, by definition, is made up of companies selling non-essential goods and services. When economic conditions deteriorate or tastes shift, consumers can easily cut back or eliminate these purchases. For long-term investors with five-year holding periods, this creates a structural challenge: the sector is inherently hit-driven, with low switching costs and fickle customers. As a result, only a handful of companies can reliably grow demand and compound earnings over long periods, which is why our bar is high and High Quality ratings are rare.

Gaming solutions companies provide the technology infrastructure behind gambling—slot machines, table game systems, lottery terminals, sports-betting platforms, and back-end software for casinos and online operators. Tailwinds include the ongoing legalization of sports betting across U.S. states and international markets, growing adoption of digital and mobile wagering, and casino operators' demand for data-driven player engagement tools. However, headwinds include stringent and evolving regulatory requirements across jurisdictions, high upfront R&D costs to develop next-generation platforms, and customer concentration risk given the limited number of large casino operators. Increasing competition from in-house technology development by major operators also pressures demand.

Competitors in the video gaming terminal (VGT) market include Everi Holdings (NYSE:EVRI), PlayAGS (NYSE:AGS), and Inspired Entertainment (NASDAQ:INSE)

5. Revenue Growth

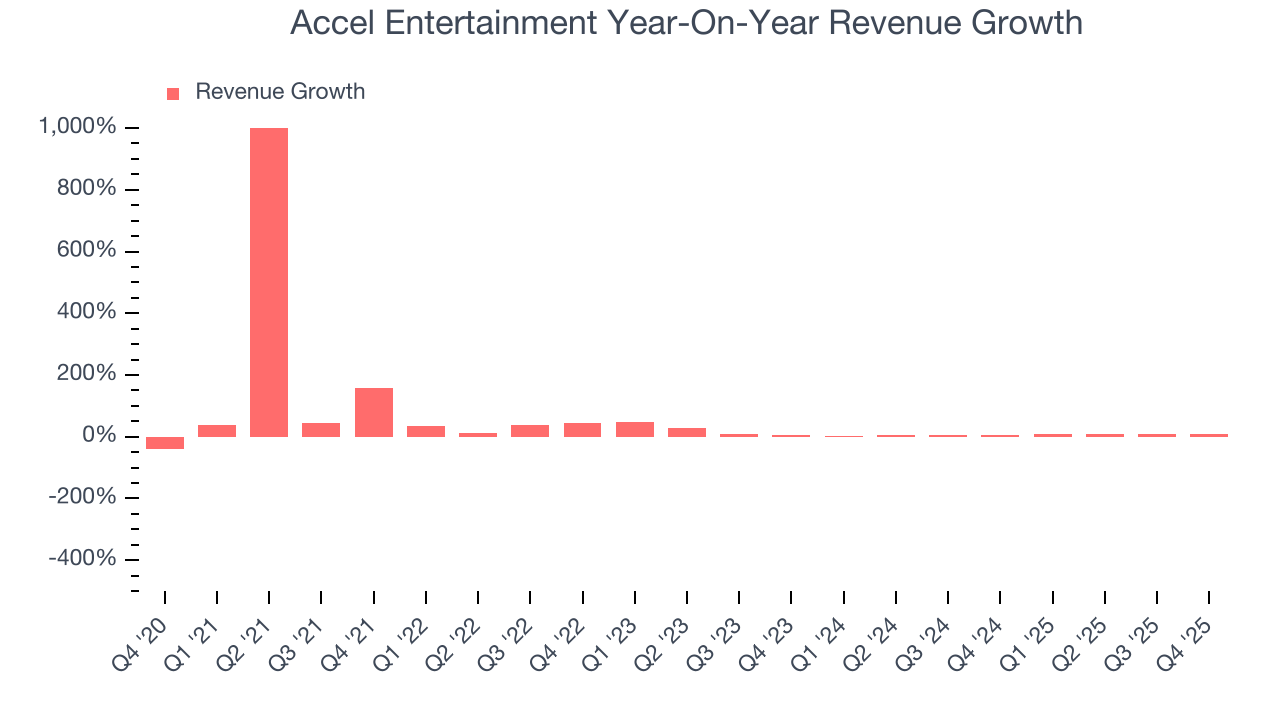

A company’s long-term performance is an indicator of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, Accel Entertainment grew its sales at a 33.3% annual rate. Though this growth is acceptable on an absolute basis, we need to see more than just topline growth for the consumer discretionary sector, which can display significant earnings volatility. This means our bar for the sector is particularly high, reflecting the non-essential and hit-driven nature of the products and services offered. Additionally, five-year CAGR starts around Covid, when revenue was depressed then rebounded.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. Accel Entertainment’s recent performance shows its demand has slowed as its annualized revenue growth of 6.6% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

Accel Entertainment also discloses its number of video gaming terminals sold, which reached 27,950 in the latest quarter. Over the last two years, Accel Entertainment’s video gaming terminals sold averaged 6.5% year-on-year growth. Because this number aligns with its revenue growth during the same period, we can see the company’s monetization was fairly consistent.

This quarter, Accel Entertainment reported year-on-year revenue growth of 7.5%, and its $341.4 million of revenue exceeded Wall Street’s estimates by 1.7%.

Looking ahead, sell-side analysts expect revenue to grow 4% over the next 12 months, a slight deceleration versus the last two years. This projection is underwhelming and suggests its products and services will see some demand headwinds.

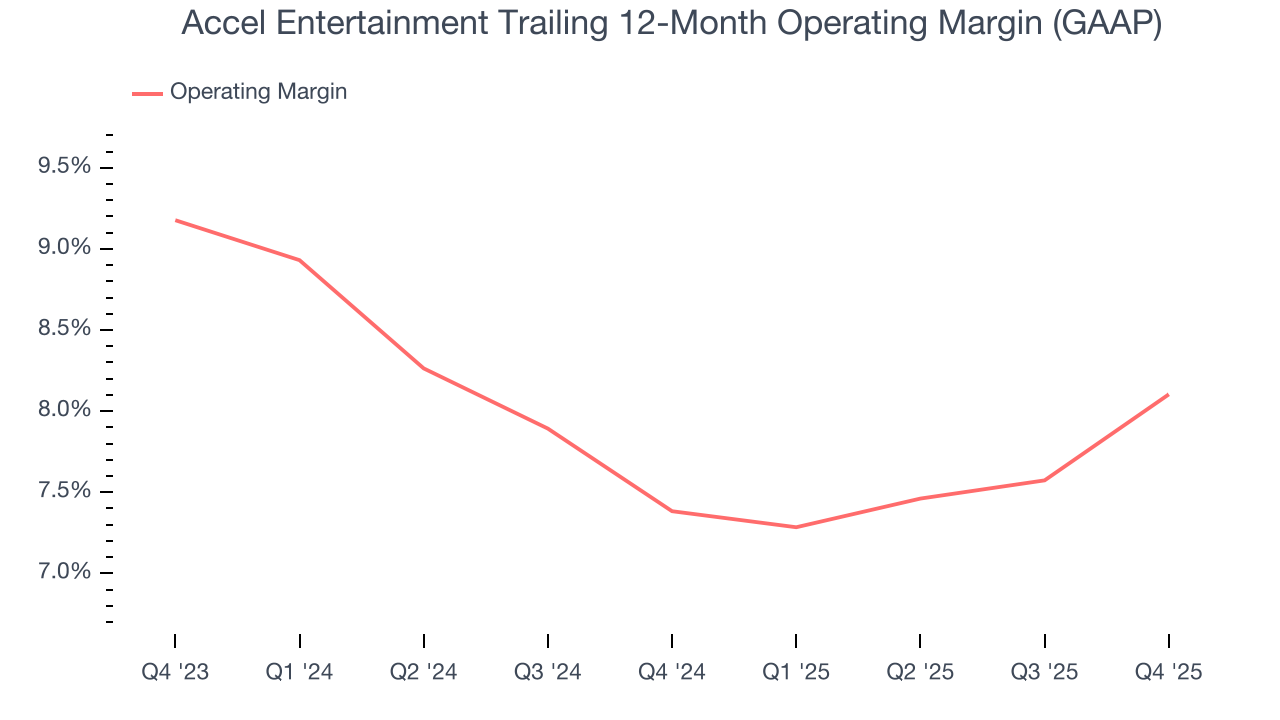

6. Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Accel Entertainment’s operating margin has generally stayed the same over the last 12 months, and we generally like to see margin increases due to economies of scale and cost efficiency over time.

In Q4, Accel Entertainment generated an operating margin profit margin of 8.7%, up 2.1 percentage points year on year. This increase was a welcome development and shows it was more efficient.

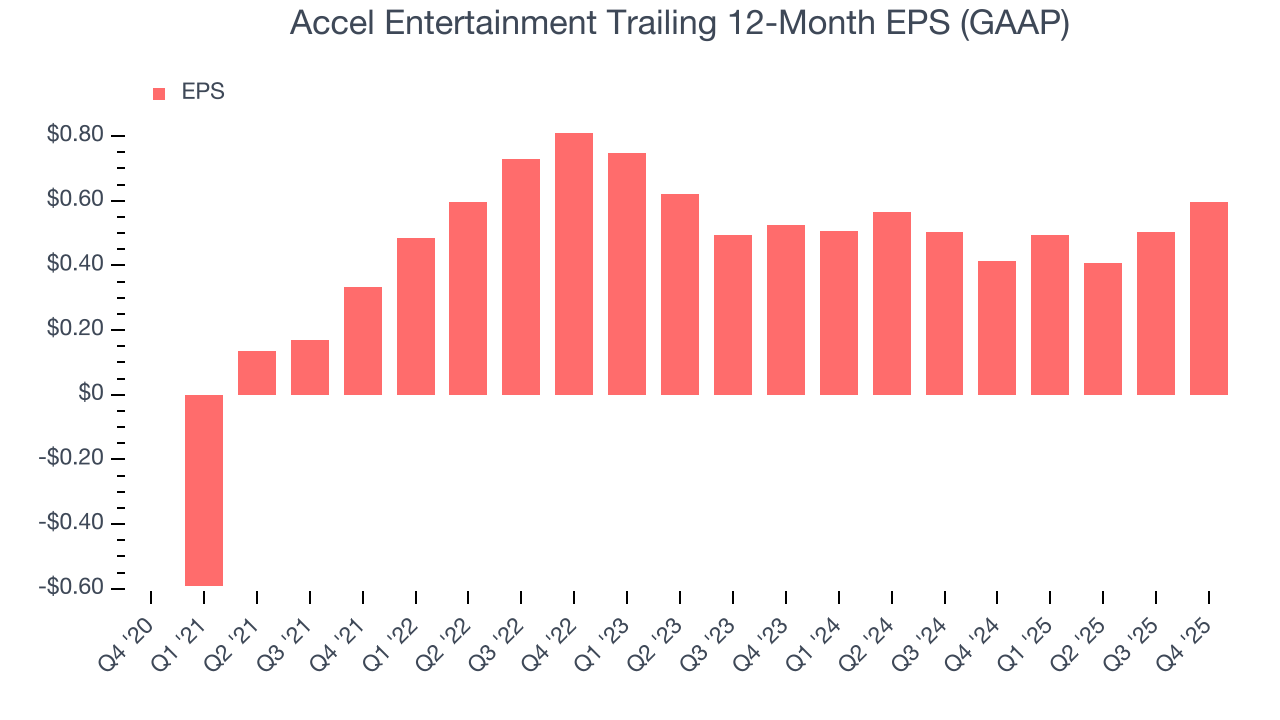

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Accel Entertainment’s full-year EPS flipped from negative to positive over the last five years. This is encouraging and shows it’s at a critical moment in its life.

In Q4, Accel Entertainment reported EPS of $0.19, up from $0.10 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Accel Entertainment’s full-year EPS of $0.60 to grow 10%.

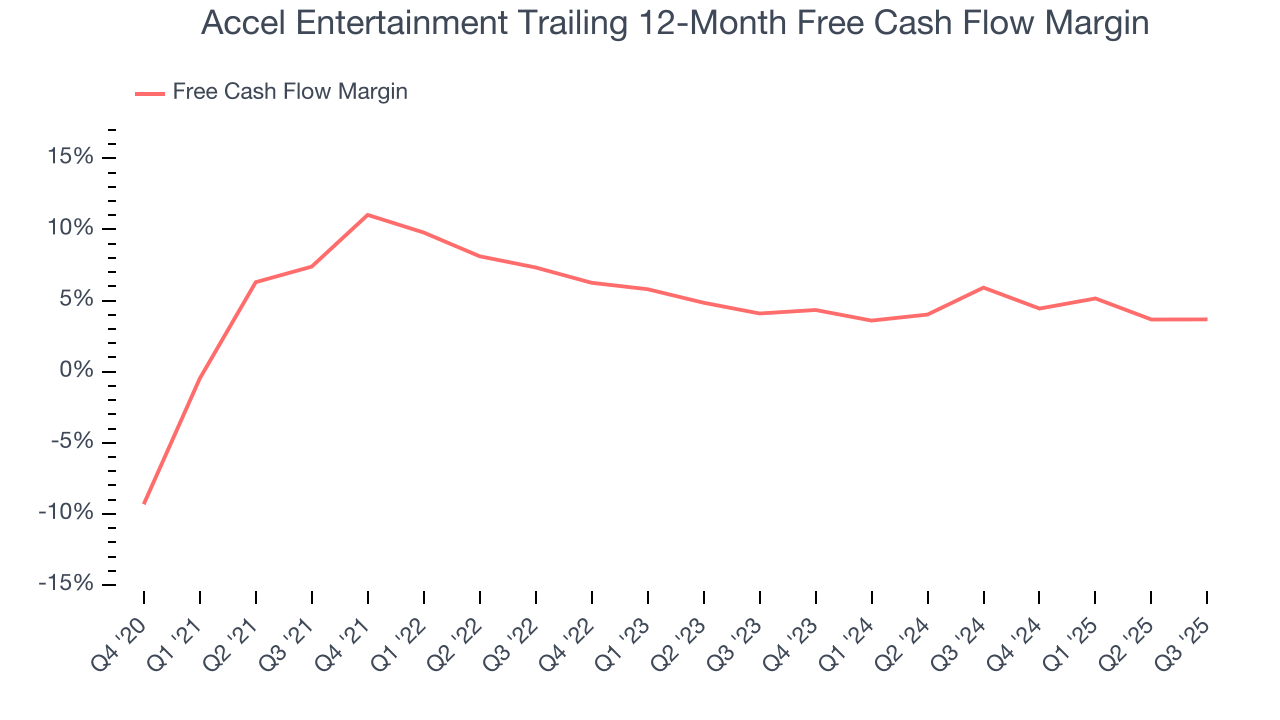

8. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Accel Entertainment has shown poor cash profitability relative to peers over the last two years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 4.5%, below what we’d expect for a consumer discretionary business.

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Accel Entertainment historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 18.1%, somewhat low compared to the best consumer discretionary companies that consistently pump out 25%+.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, Accel Entertainment’s ROIC averaged 2.9 percentage point decreases each year over the last few years. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

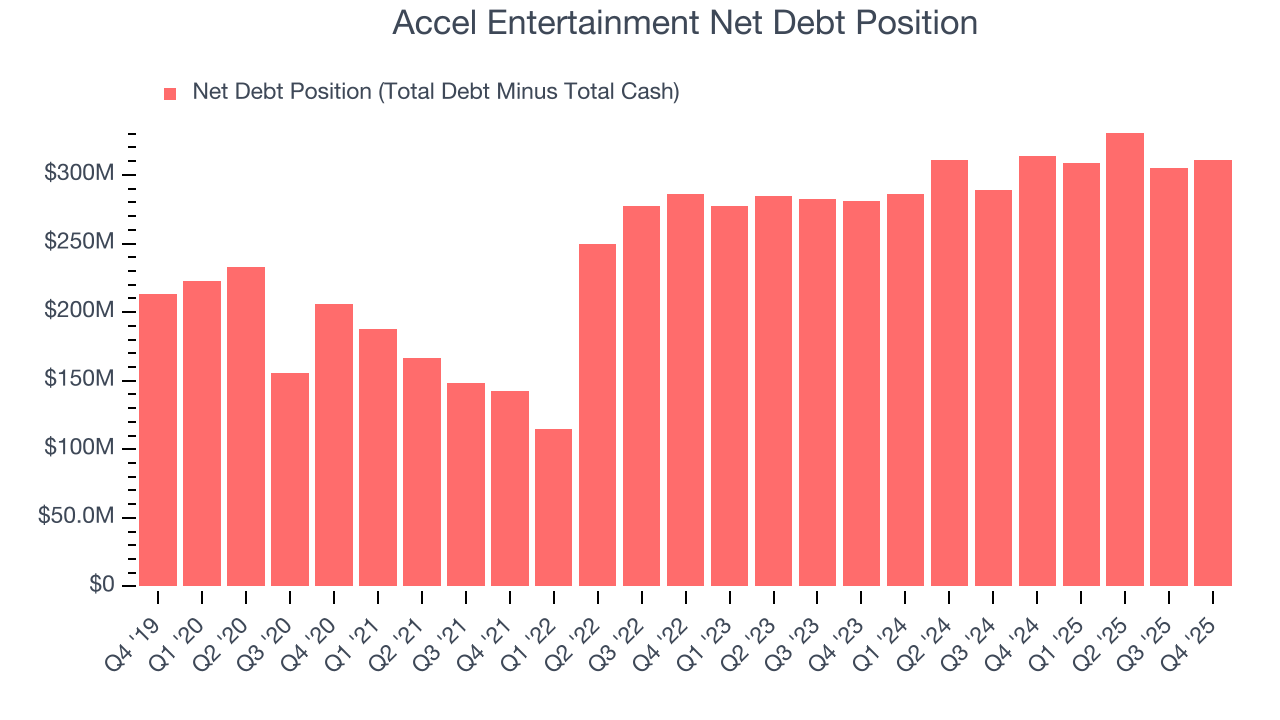

10. Balance Sheet Assessment

Accel Entertainment reported $296.6 million of cash and $607.4 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $210.1 million of EBITDA over the last 12 months, we view Accel Entertainment’s 1.5× net-debt-to-EBITDA ratio as safe. We also see its $25.53 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from Accel Entertainment’s Q4 Results

It was good to see Accel Entertainment beat analysts’ EPS expectations this quarter. We were also happy its EBITDA outperformed Wall Street’s estimates. Zooming out, we think this was a solid print. The stock traded up 6.2% to $11.76 immediately after reporting.

12. Is Now The Time To Buy Accel Entertainment?

Updated: March 22, 2026 at 10:53 PM EDT

Before making an investment decision, investors should account for Accel Entertainment’s business fundamentals and valuation in addition to what happened in the latest quarter.

We see the value of companies helping consumers, but in the case of Accel Entertainment, we’re out. While its astounding EPS growth over the last five years shows its profits are trickling down to shareholders, the downside is its number of video gaming terminals sold has disappointed. On top of that, its Forecasted free cash flow margin suggests the company will have more capital to invest or return to shareholders next year.

Accel Entertainment’s P/E ratio based on the next 12 months is 12.5x. While this valuation is reasonable, we don’t see a big opportunity at the moment. There are more exciting stocks to buy at the moment.

Wall Street analysts have a consensus one-year price target of $15.50 on the company (compared to the current share price of $10.91).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.