Avery Dennison (AVY)

We aren’t fans of Avery Dennison. Its weak sales growth and declining returns on capital show its demand and profits are shrinking.― StockStory Analyst Team

1. News

2. Summary

Why We Think Avery Dennison Will Underperform

Founded as Kum Kleen Products, Avery Dennison (NYSE:AVY) is a manufacturer of adhesive materials, display graphics, and packaging products, serving various industries.

- Organic sales performance over the past two years indicates the company may need to make strategic adjustments or rely on M&A to catalyze faster growth

- Anticipated sales growth of 4.4% for the next year implies demand will be shaky

- On the plus side, its market-beating returns on capital illustrate that management has a knack for investing in profitable ventures

Avery Dennison lacks the business quality we seek. There are superior stocks for sale in the market.

Why There Are Better Opportunities Than Avery Dennison

Avery Dennison is trading at $170.73 per share, or 16.9x forward P/E. Avery Dennison’s valuation may seem like a bargain, especially when stacked up against other industrials companies. We remind you that you often get what you pay for, though.

We’d rather pay up for companies with elite fundamentals than get a bargain on weak ones. Cheap stocks can be value traps, and as their performance deteriorates, they will stay cheap or get even cheaper.

3. Avery Dennison (AVY) Research Report: Q4 CY2025 Update

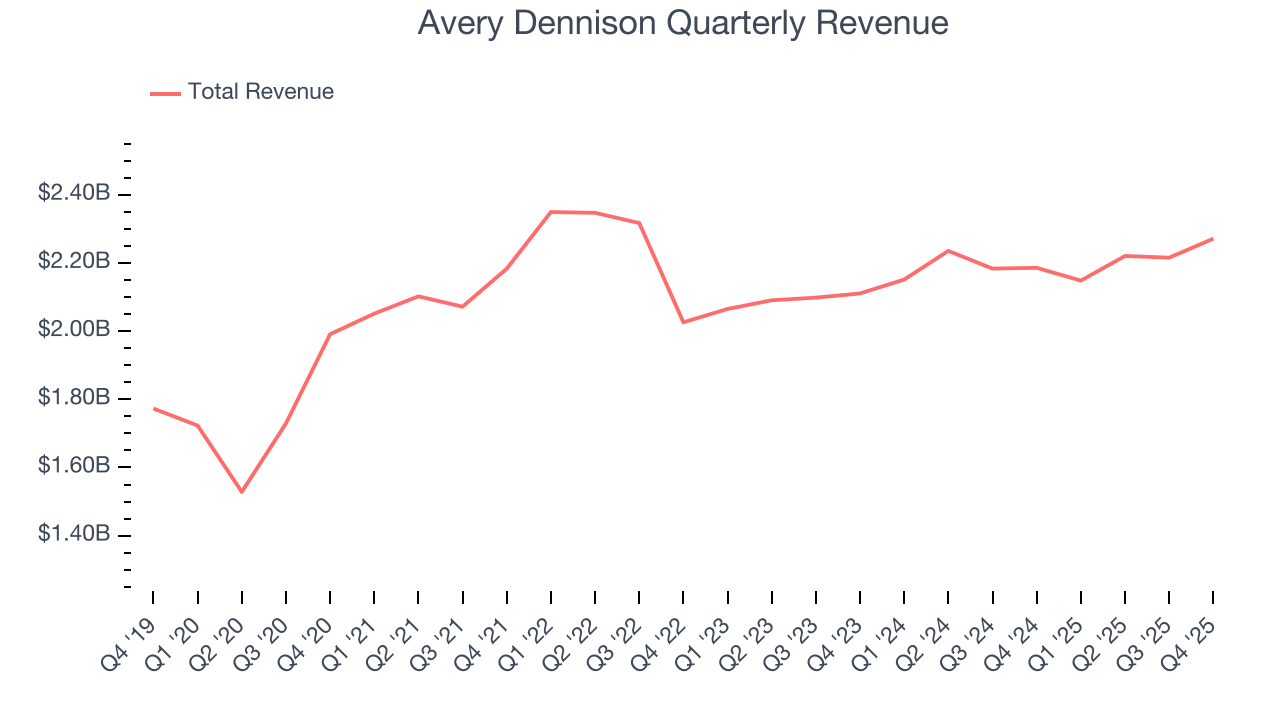

Adhesive manufacturing company Avery Dennison (NYSE:AVY) missed Wall Street’s revenue expectations in Q4 CY2025 as sales rose 3.9% year on year to $2.27 billion. Its non-GAAP profit of $2.45 per share was 2.9% above analysts’ consensus estimates.

Avery Dennison (AVY) Q4 CY2025 Highlights:

- Revenue: $2.27 billion vs analyst estimates of $2.28 billion (3.9% year-on-year growth, 0.5% miss)

- Adjusted EPS: $2.45 vs analyst estimates of $2.38 (2.9% beat)

- Adjusted EBITDA: $367 million vs analyst estimates of $368.2 million (16.2% margin, in line)

- Adjusted EPS guidance for Q1 CY2026 is $2.43 at the midpoint, above analyst estimates of $2.40

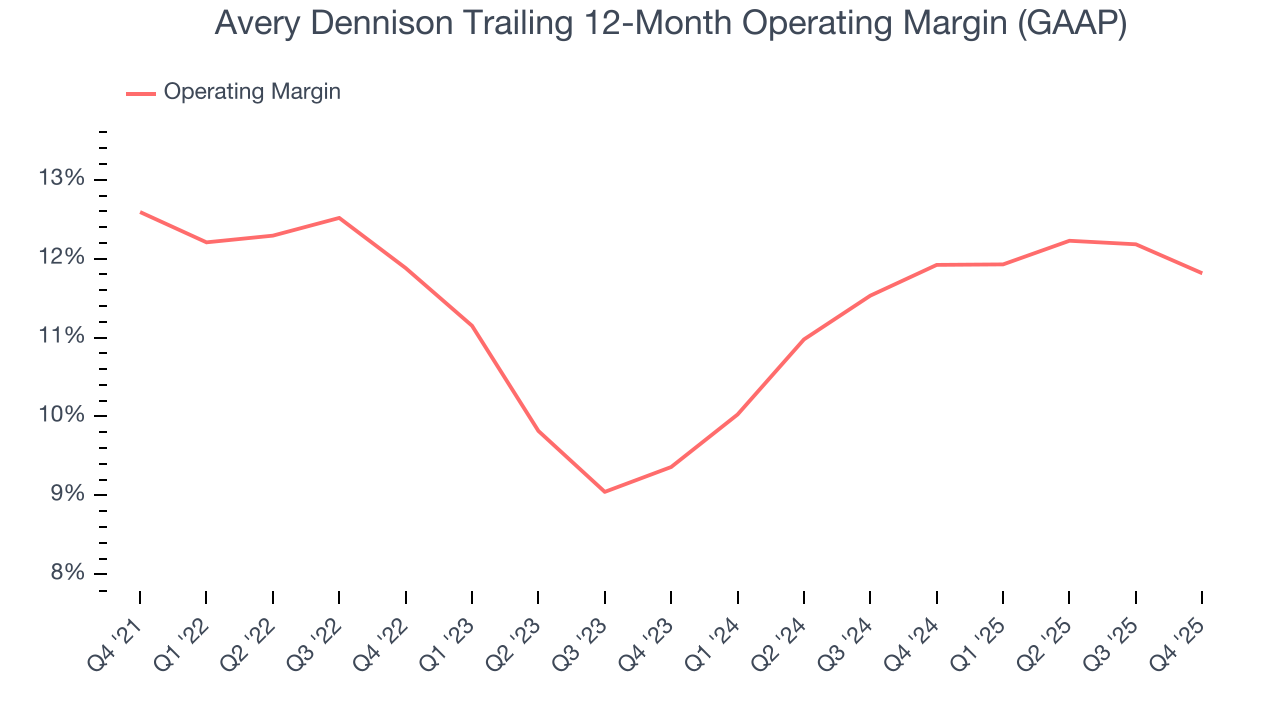

- Operating Margin: 10.6%, down from 12% in the same quarter last year

- Free Cash Flow Margin: 13.3%, similar to the same quarter last year

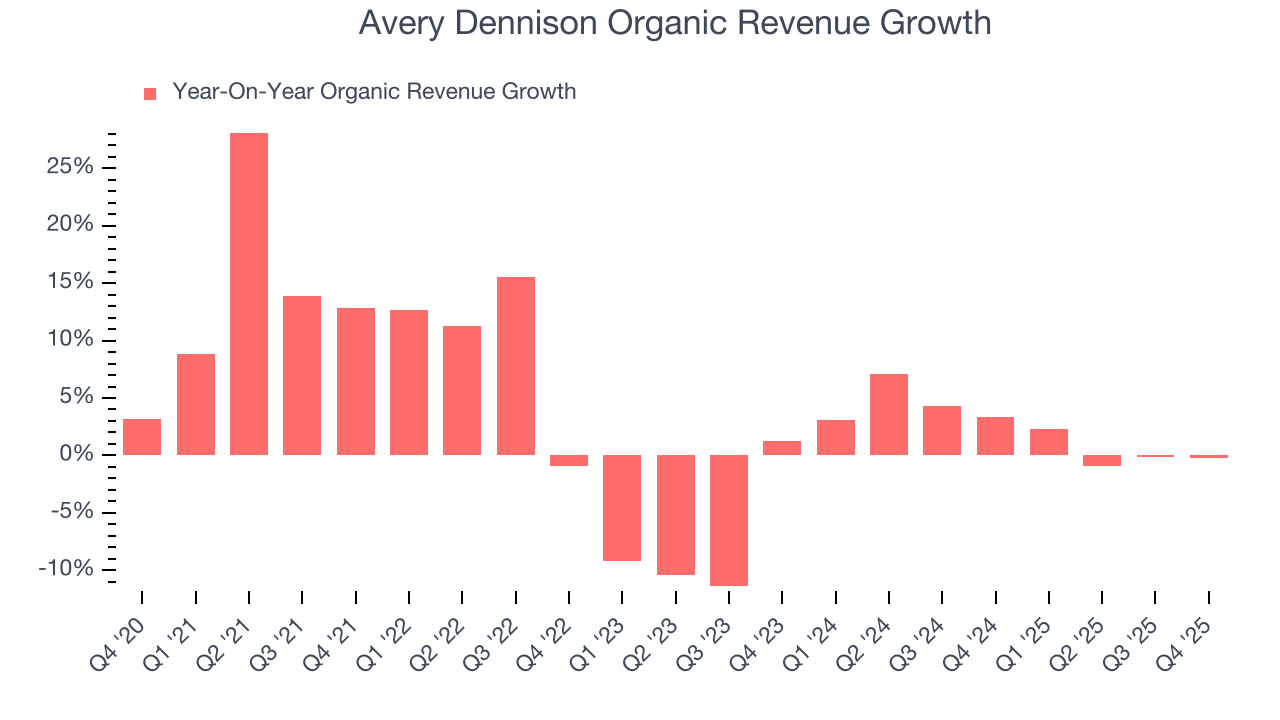

- Organic Revenue was flat year on year (miss)

- Market Capitalization: $14.44 billion

Company Overview

Founded as Kum Kleen Products, Avery Dennison (NYSE:AVY) is a manufacturer of adhesive materials, display graphics, and packaging products, serving various industries.

Avery Dennison was established in 1935 by R. Stanton Avery, the inventor of the self-adhesive label. The company initially emerged to simplify merchandising and labeling processes for businesses and now delivers a broad spectrum of material science-based labeling and packaging solutions.

Specifically, Avery Dennison offers pressure-sensitive materials, apparel branding tags and labels, RFID inlays, and specialty medical products. For example, its pressure-sensitive labels are used on consumer products for branding and informational labels, while RFID solutions are implemented in retail for inventory management and loss prevention.

Revenue at Avery Dennison is generated from multiple sources, primarily the sale of labeling and packaging materials. The company sells its products globally through direct sales forces and distribution partners. Revenue is largely recurring due to the continuous demand for consumable products like labels and tags, providing stable income streams.

4. Industrial Packaging

Industrial packaging companies have built competitive advantages from economies of scale that lead to advantaged purchasing and capital investments that are difficult and expensive to replicate. Recently, eco-friendly packaging and conservation are driving customers preferences and innovation. For example, plastic is not as desirable a material as it once was. Despite being integral to consumer goods ranging from beer to toothpaste to laundry detergent, these companies are still at the whim of the macro, especially consumer health and consumer willingness to spend.

Competitors in the packaging industry include Crown Holdings (NYSE:CCK), Ardagh Group (NYSE:ARD), and Silgan Holdings (NASDAQ:SLGN).

5. Revenue Growth

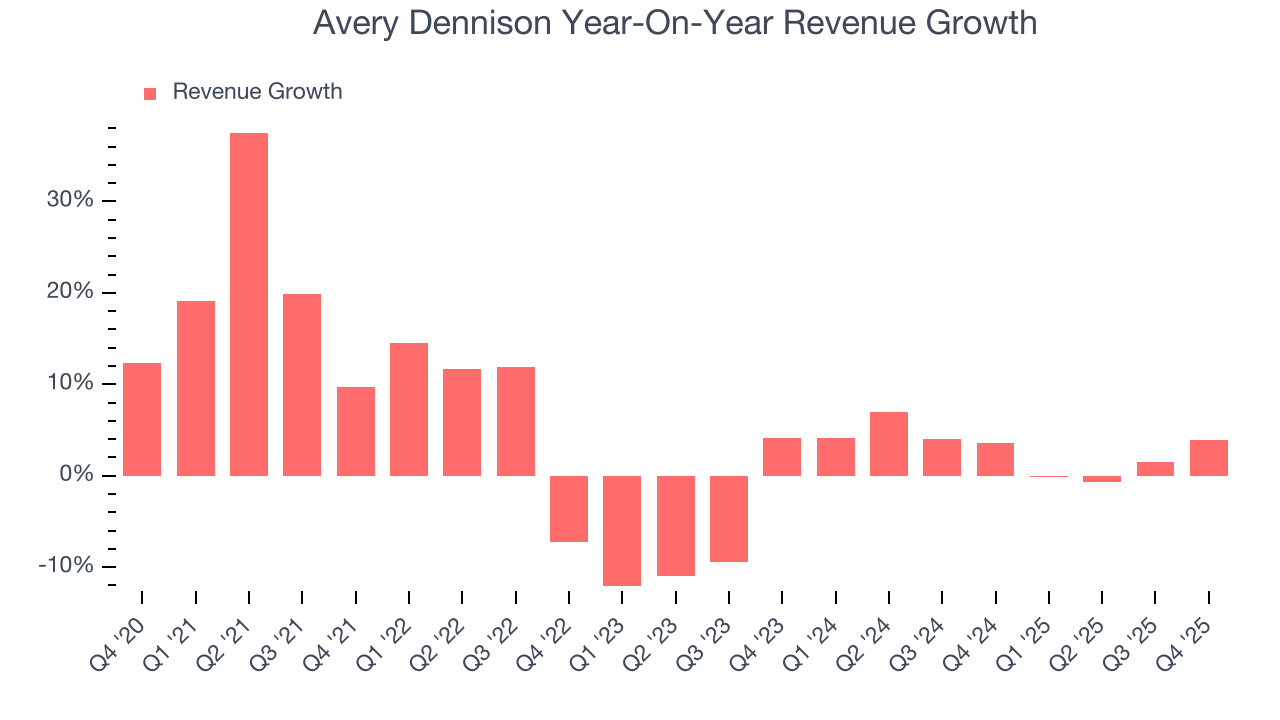

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, Avery Dennison grew its sales at a tepid 4.9% compounded annual growth rate. This fell short of our benchmark for the industrials sector and is a tough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Avery Dennison’s recent performance shows its demand has slowed as its annualized revenue growth of 2.9% over the last two years was below its five-year trend.

We can better understand the company’s sales dynamics by analyzing its organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, Avery Dennison’s organic revenue averaged 2.4% year-on-year growth. Because this number aligns with its two-year revenue growth, we can see the company’s core operations (not acquisitions and divestitures) drove most of its results.

This quarter, Avery Dennison’s revenue grew by 3.9% year on year to $2.27 billion, falling short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 4.7% over the next 12 months. While this projection suggests its newer products and services will spur better top-line performance, it is still below average for the sector.

6. Gross Margin & Pricing Power

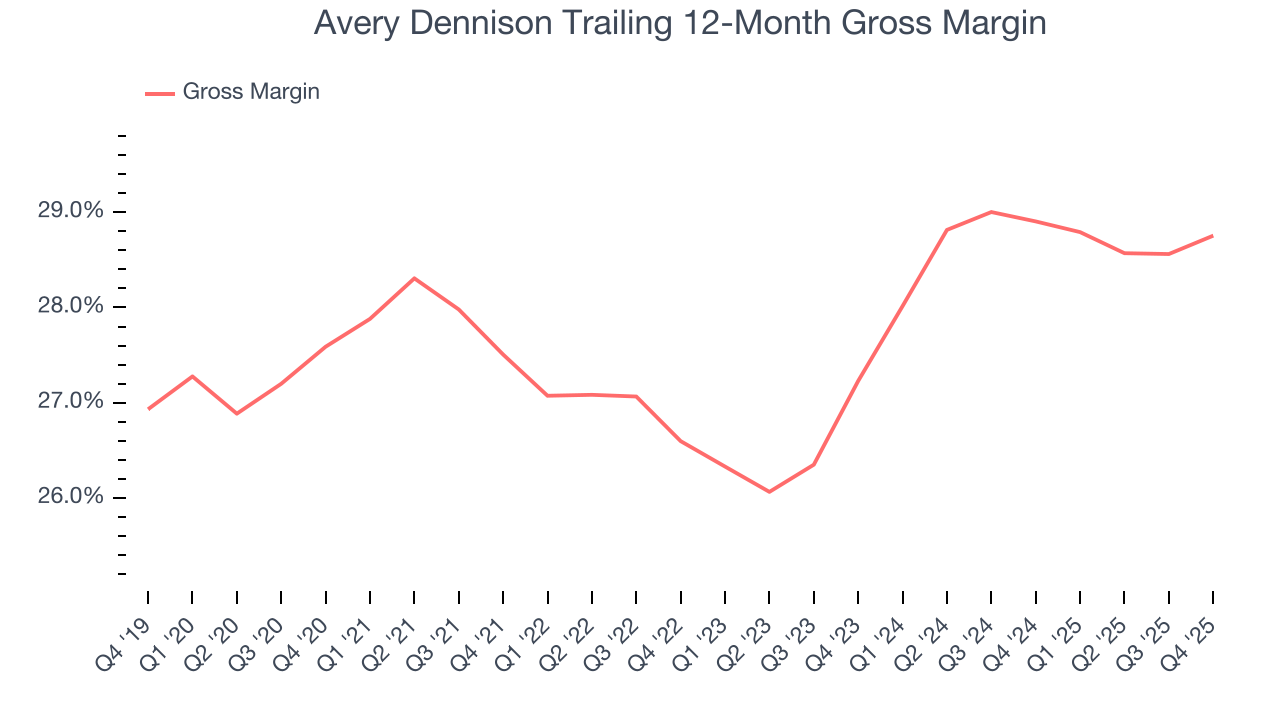

Avery Dennison’s gross margin is slightly below the average industrials company, giving it less room to invest in areas such as research and development. As you can see below, it averaged a 27.8% gross margin over the last five years. Said differently, Avery Dennison had to pay a chunky $72.20 to its suppliers for every $100 in revenue.

Avery Dennison’s gross profit margin came in at 28.7% this quarter, in line with the same quarter last year. On a wider time horizon, the company’s full-year margin has remained steady over the past four quarters, suggesting its input costs (such as raw materials and manufacturing expenses) have been stable and it isn’t under pressure to lower prices.

7. Operating Margin

Avery Dennison’s operating margin might fluctuated slightly over the last 12 months but has remained more or less the same, averaging 11.5% over the last five years. This profitability was solid for an industrials business and shows it’s an efficient company that manages its expenses well. This result was particularly impressive because of its low gross margin, which is mostly a factor of what it sells and takes huge shifts to move meaningfully. Companies have more control over their operating margins, and it’s a show of well-managed operations if they’re high when gross margins are low.

Looking at the trend in its profitability, Avery Dennison’s operating margin might fluctuated slightly but has generally stayed the same over the last five years. We like to see margin expansion, but we’re still happy with Avery Dennison’s performance considering most Industrial Packaging companies saw their margins plummet.

This quarter, Avery Dennison generated an operating margin profit margin of 10.6%, down 1.4 percentage points year on year. Since Avery Dennison’s operating margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, R&D, and administrative overhead increased.

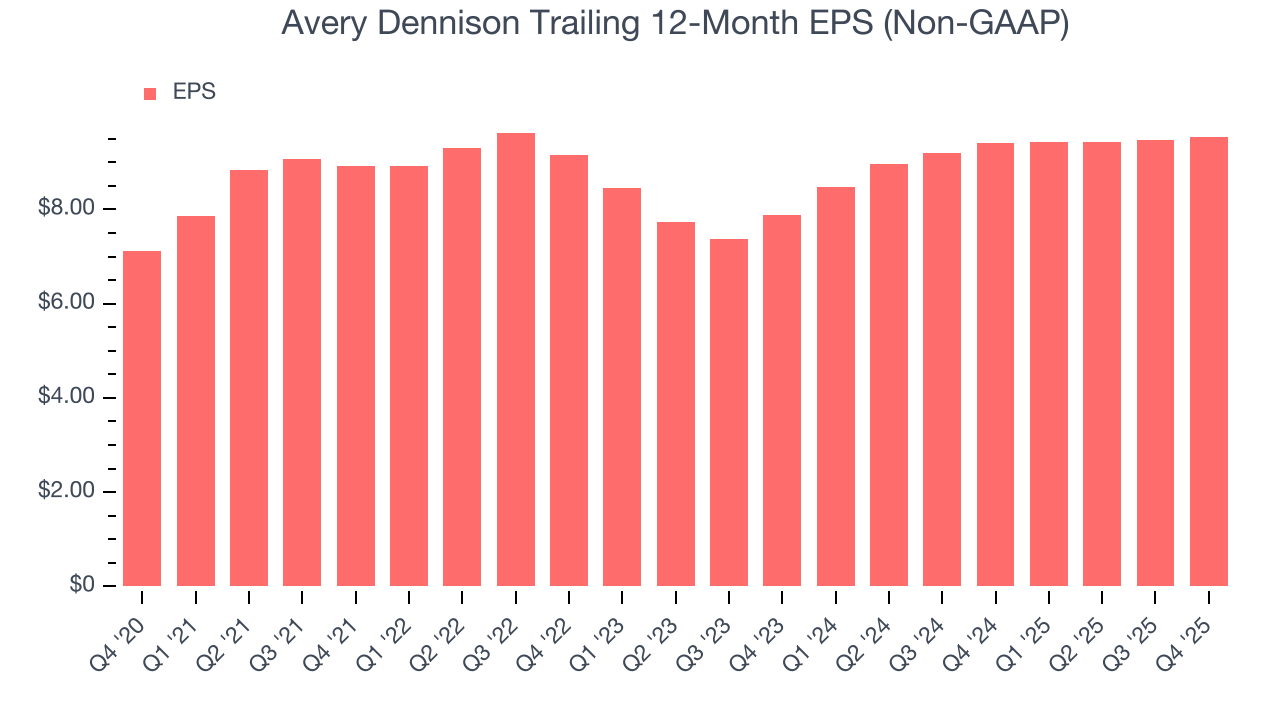

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Avery Dennison’s unimpressive 6.1% annual EPS growth over the last five years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

Avery Dennison’s two-year annual EPS growth of 10% was good and topped its 2.9% two-year revenue growth.

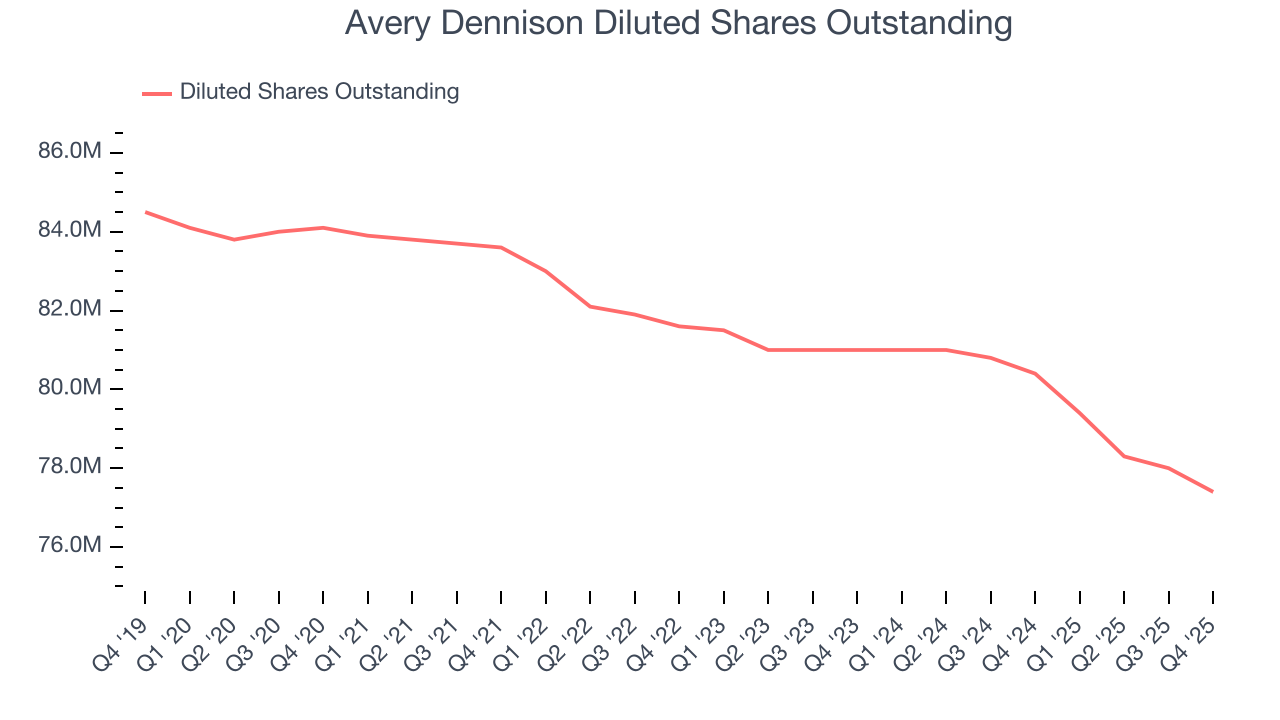

We can take a deeper look into Avery Dennison’s earnings to better understand the drivers of its performance. A two-year view shows that Avery Dennison has repurchased its stock, shrinking its share count by 4.4%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

In Q4, Avery Dennison reported adjusted EPS of $2.45, up from $2.38 in the same quarter last year. This print beat analysts’ estimates by 2.9%. Over the next 12 months, Wall Street expects Avery Dennison’s full-year EPS of $9.54 to grow 6.9%.

9. Cash Is King

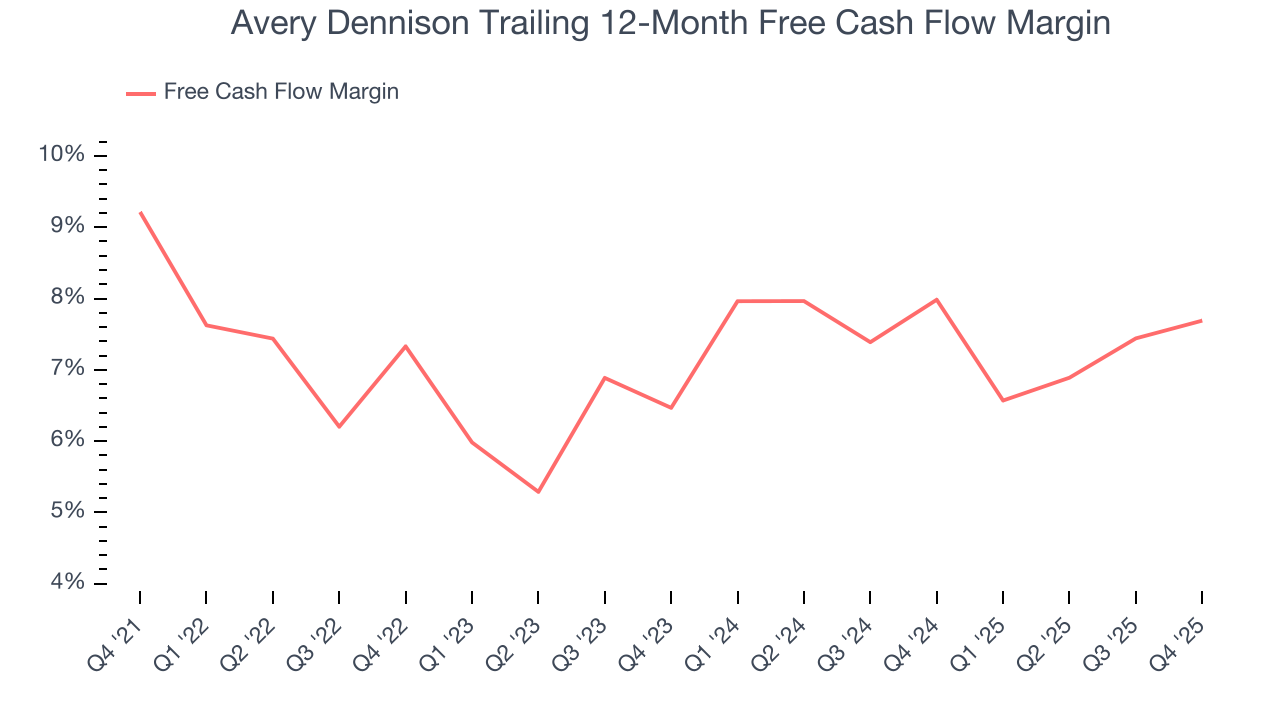

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Avery Dennison has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 7.7% over the last five years, slightly better than the broader industrials sector.

Taking a step back, we can see that Avery Dennison’s margin dropped by 1.5 percentage points during that time. Continued declines could signal it is in the middle of an investment cycle.

Avery Dennison’s free cash flow clocked in at $301.2 million in Q4, equivalent to a 13.3% margin. This cash profitability was in line with the comparable period last year and above its five-year average.

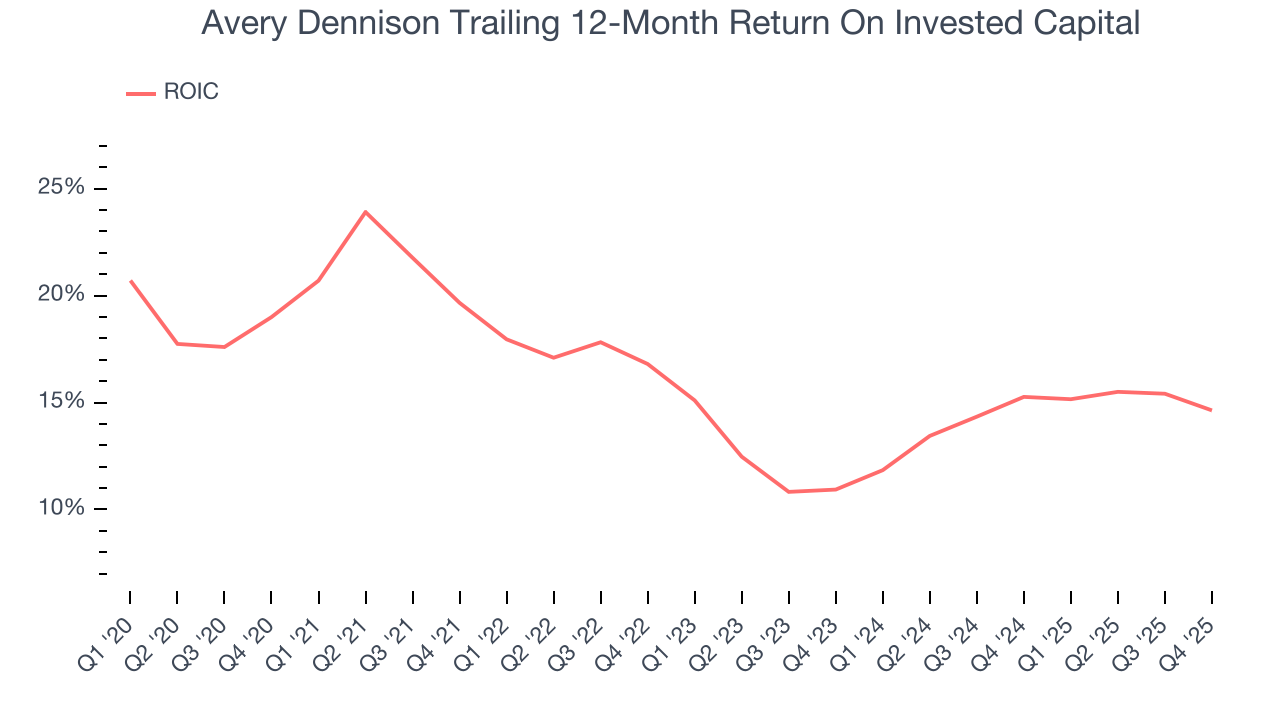

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Although Avery Dennison hasn’t been the highest-quality company lately, it historically found a few growth initiatives that worked out well. Its five-year average ROIC was 15.5%, impressive for an industrials business.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. On average, Avery Dennison’s ROIC decreased by 3.3 percentage points annually over the last few years. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

11. Balance Sheet Assessment

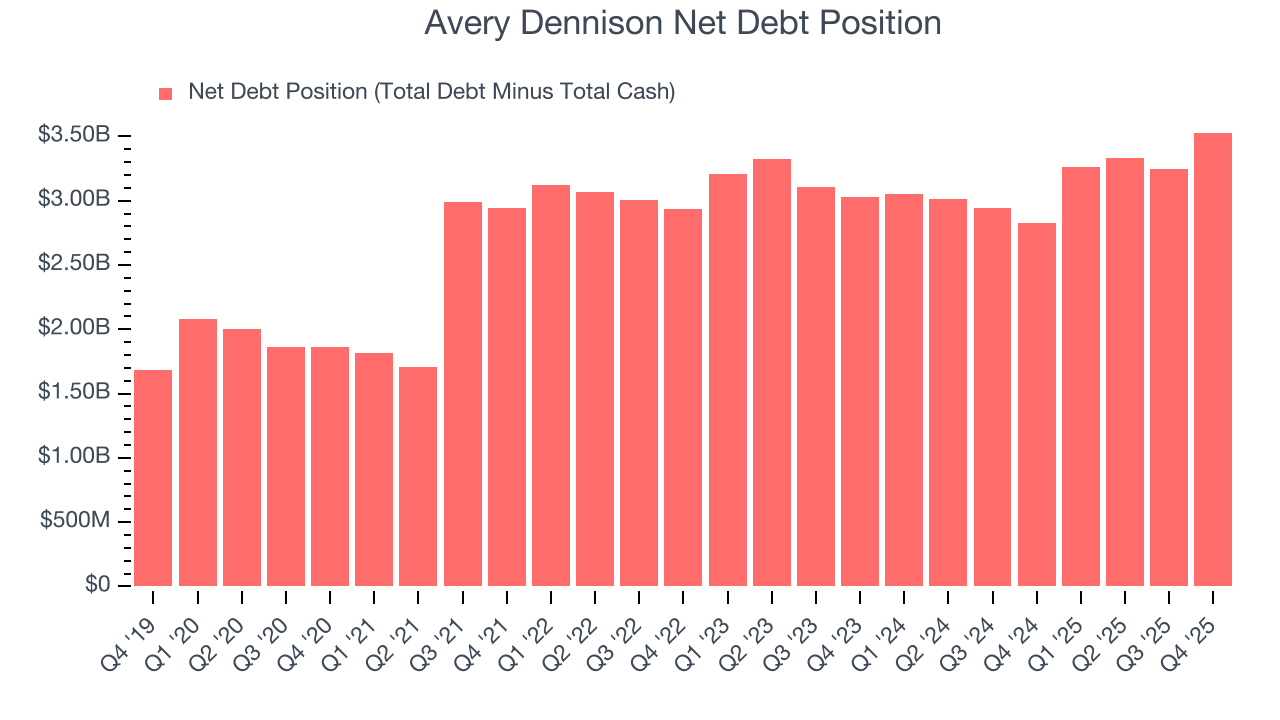

Avery Dennison reported $202.8 million of cash and $3.73 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $1.45 billion of EBITDA over the last 12 months, we view Avery Dennison’s 2.4× net-debt-to-EBITDA ratio as safe. We also see its $61 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Avery Dennison’s Q4 Results

It was good to see Avery Dennison provide EPS guidance for next quarter that slightly beat analysts’ expectations. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its revenue slightly missed. Overall, this quarter was mixed. Still the stock traded up 4.4% to $195.08 immediately after reporting.

13. Is Now The Time To Buy Avery Dennison?

Updated: March 14, 2026 at 11:51 PM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Avery Dennison.

Avery Dennison isn’t a terrible business, but it isn’t one of our picks. To kick things off, its revenue growth was uninspiring over the last five years, and analysts don’t see anything changing over the next 12 months. While its market-beating ROIC suggests it has been a well-managed company historically, the downside is its organic revenue growth has disappointed. On top of that, its diminishing returns show management's prior bets haven't worked out.

Avery Dennison’s P/E ratio based on the next 12 months is 16.9x. This valuation is reasonable, but the company’s shakier fundamentals present too much downside risk. We're pretty confident there are more exciting stocks to buy at the moment.

Wall Street analysts have a consensus one-year price target of $211.90 on the company (compared to the current share price of $170.73).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.