Cadre (CDRE)

Cadre catches our eye. Its estimated revenue growth for the next 12 months is great.― StockStory Analyst Team

1. News

2. Summary

Why Cadre Is Interesting

Originally known as Safariland, Cadre (NYSE:CDRE) specializes in manufacturing and distributing safety and survivability equipment for first responders.

- Exciting sales outlook for the upcoming 12 months calls for 22.5% growth, an acceleration from its two-year trend

- Earnings per share have outperformed the peer group average over the last four years, increasing by 14.3% annually

- The stock is trading at a reasonable price if you like its story and growth prospects

Cadre has the potential to be a high-quality business. If you like the stock, the price seems reasonable.

Why Is Now The Time To Buy Cadre?

At $32.11 per share, Cadre trades at 24.6x forward P/E. Scanning the industrials peers, we conclude that Cadre’s valuation is warranted for the business quality.

If you think the market is not giving the company enough credit for its fundamentals, now could be a good time to invest.

3. Cadre (CDRE) Research Report: Q4 CY2025 Update

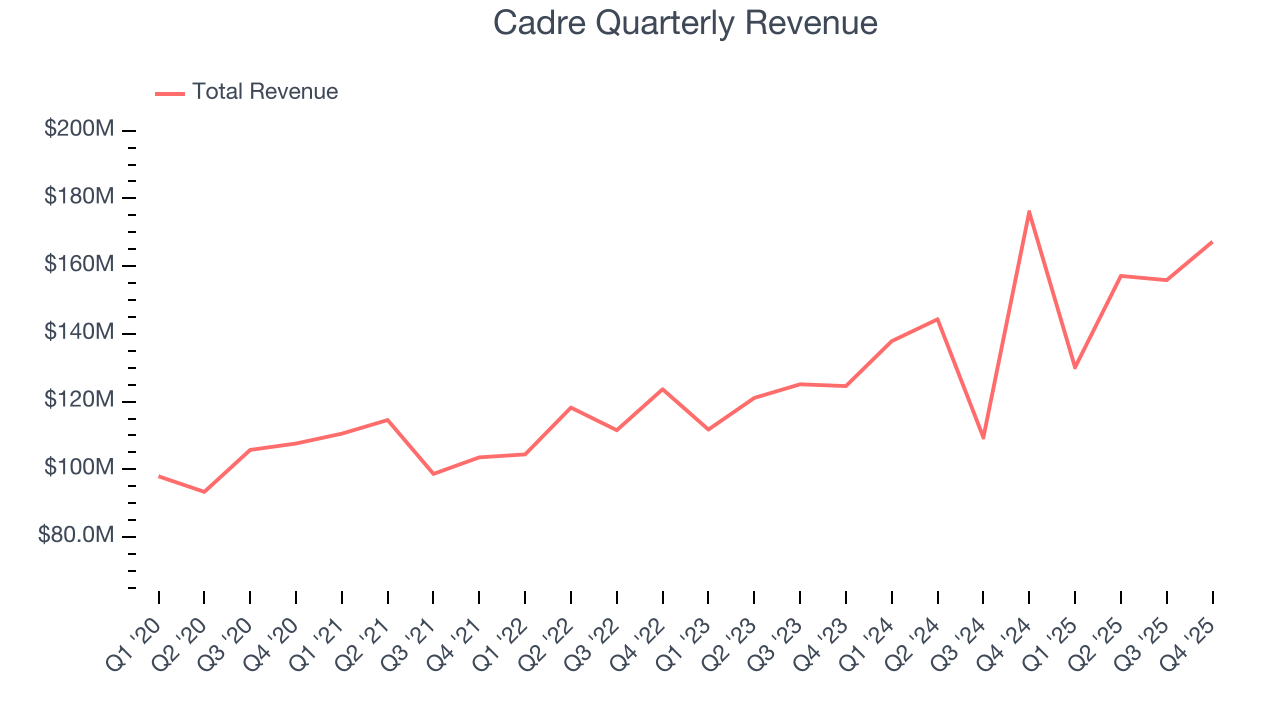

Aerospace and defense company Cadre (NYSE:CDRE) fell short of the market’s revenue expectations in Q4 CY2025, with sales falling 5% year on year to $167.2 million. On the other hand, the company’s full-year revenue guidance of $747 million at the midpoint came in 2.5% above analysts’ estimates. Its GAAP profit of $0.27 per share was 32.5% below analysts’ consensus estimates.

Cadre (CDRE) Q4 CY2025 Highlights:

- Revenue: $167.2 million vs analyst estimates of $184.3 million (5% year-on-year decline, 9.3% miss)

- EPS (GAAP): $0.27 vs analyst expectations of $0.40 (32.5% miss)

- Adjusted EBITDA: $34.4 million vs analyst estimates of $37.29 million (20.6% margin, 7.7% miss)

- EBITDA guidance for the upcoming financial year 2026 is $138.5 million at the midpoint, below analyst estimates of $139.9 million

- Operating Margin: 12.2%, down from 16.7% in the same quarter last year

- Free Cash Flow Margin: 10.7%, down from 12.7% in the same quarter last year

- Market Capitalization: $1.81 billion

Company Overview

Originally known as Safariland, Cadre (NYSE:CDRE) specializes in manufacturing and distributing safety and survivability equipment for first responders.

Cadre was founded in 1964 by Neale Perkins who began by crafting custom holsters in his garage. Named after the African safari excursions he cherished with his father, Safariland quickly grew from a small operation to a prominent manufacturer producing thousands of holsters monthly. Over the years, through strategic acquisitions and expansions, Safariland transformed into Cadre, broadening its scope to include advanced protective gear and tactical solutions for law enforcement, military, and nuclear safety sectors.

Today, Cadre’s product lineup ranges from highly protective body armor for law enforcement and first responders, to advanced Explosive Ordnance Disposal (EOD) equipment like the ICOR robots, which are integral to bomb disposal and tactical law enforcement operations. Furthermore, Cadre extends its product line to the nuclear safety sector with products and services tailored for environments with critical safety requirements. The company’s offerings include products for radiation protection and nuclear facility safety, supporting government and commercial clients such as the Department of Energy.

Cadre generates a significant portion of its revenue from government contracts, primarily through supplying safety and tactical equipment to various U.S. and international government agencies. These contracts are typically secured via competitive bidding processes and often result in long-term agreements, creating a stable flow of income from year to year.

The company's end markets include law enforcement, military, and nuclear safety sectors, which are areas with high demand for continuous advancements in safety and operational efficiency. These sectors often have stringent replacement and upgrade cycles due to the critical nature of the equipment provided. This leads to recurring revenue streams for Cadre, as products typically require regular updates or replacements to adhere to evolving safety standards and technological improvements.

4. Law Enforcement Suppliers

Many law enforcement suppliers companies require licensing and clearance to manufacture products such as firearms. These companies can enjoy long-term contracts with law enforcement and corrections bodies, leading to more predictable revenue. It is still unclear how the recent focus on excessive force and police accountability will impact longer-term demand. On the one hand, lethal force products could become less popular. On the other hand, products such as body cams that aid in the transparency of policing could become standard. Generally, the sector’s fate will also ebb and flow with state or local budgets, and there is high reputational risk, as one mishap or bad headline can change a company’s fortunes.

Cadre's competitors include Apogee Enterprises (NASDAQ:APOG), Helios Technologies (NYSE:HLIO)

5. Revenue Growth

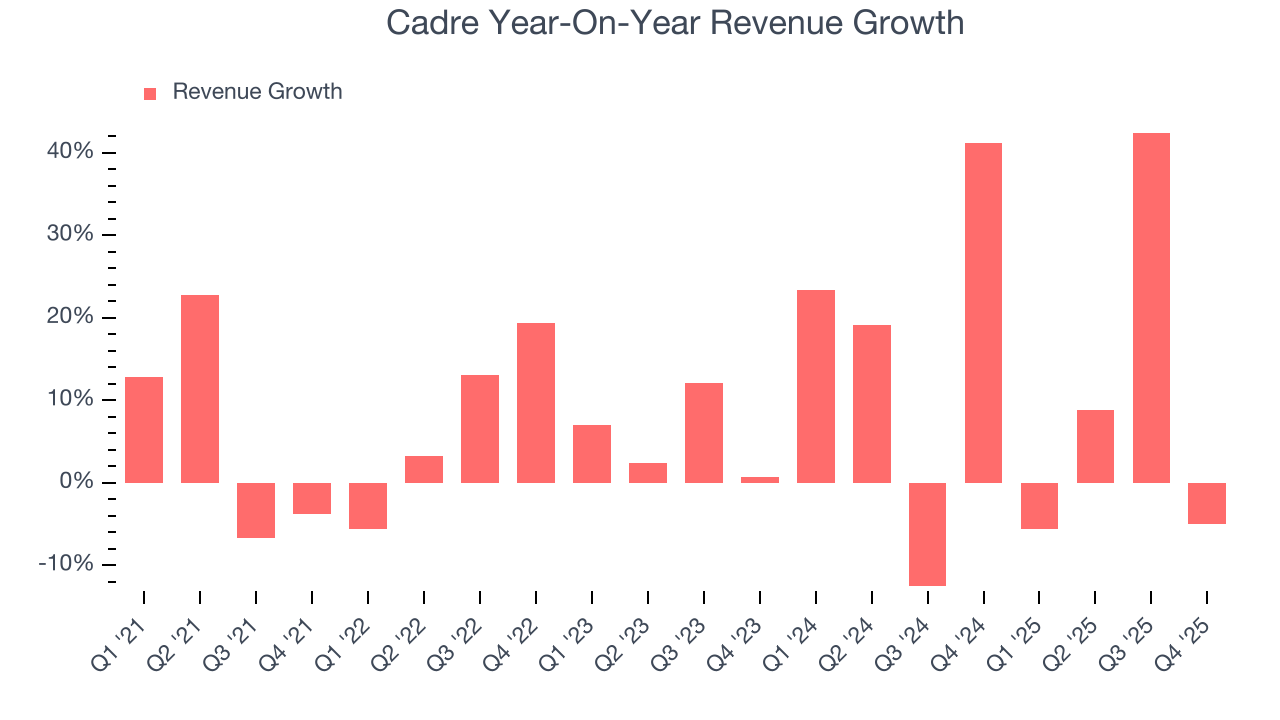

A company’s long-term sales performance can indicate its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Thankfully, Cadre’s 8.6% annualized revenue growth over the last five years was decent. Its growth was slightly above the average industrials company and shows its offerings resonate with customers.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Cadre’s annualized revenue growth of 12.5% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

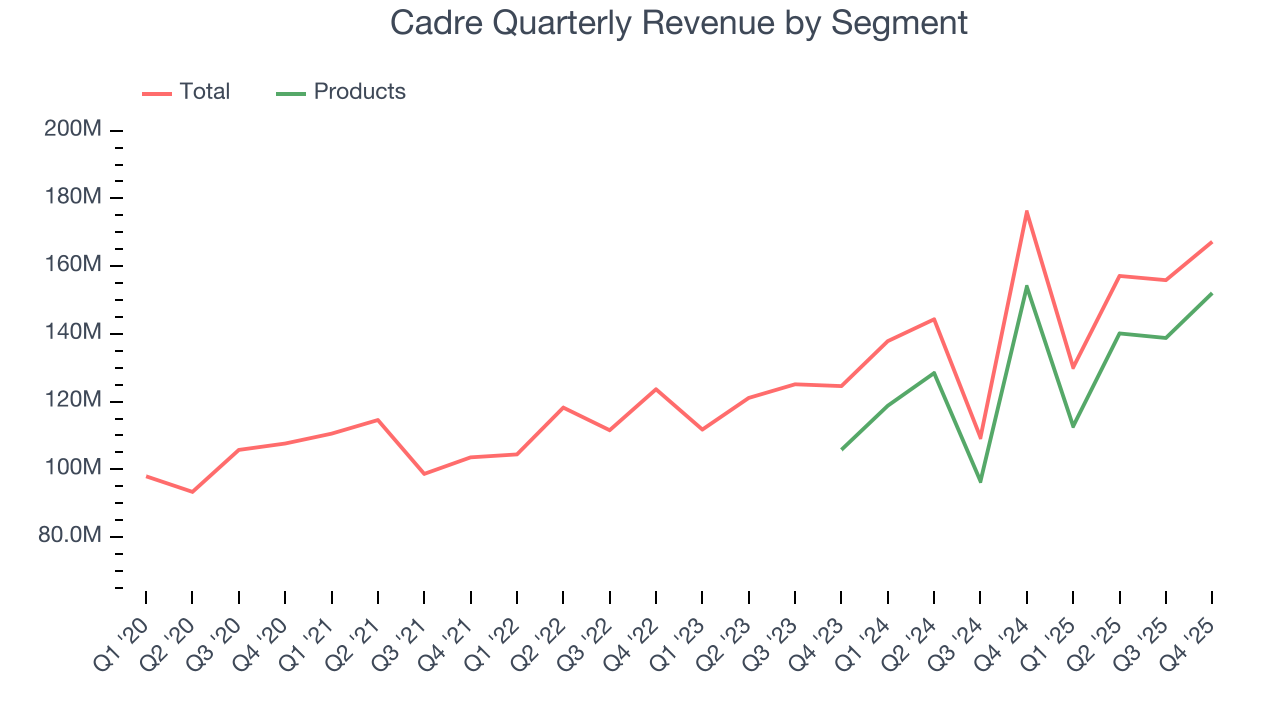

We can dig further into the company’s revenue dynamics by analyzing its most important segment, Products. Over the last two years, Cadre’s Products revenue (body armor, corrections tools, sensors) averaged 18.4% year-on-year growth. This segment has outperformed its total sales during the same period, lifting the company’s performance.

This quarter, Cadre missed Wall Street’s estimates and reported a rather uninspiring 5% year-on-year revenue decline, generating $167.2 million of revenue.

Looking ahead, sell-side analysts expect revenue to grow 23.1% over the next 12 months, an improvement versus the last two years. This projection is eye-popping and suggests its newer products and services will catalyze better top-line performance.

6. Operating Margin

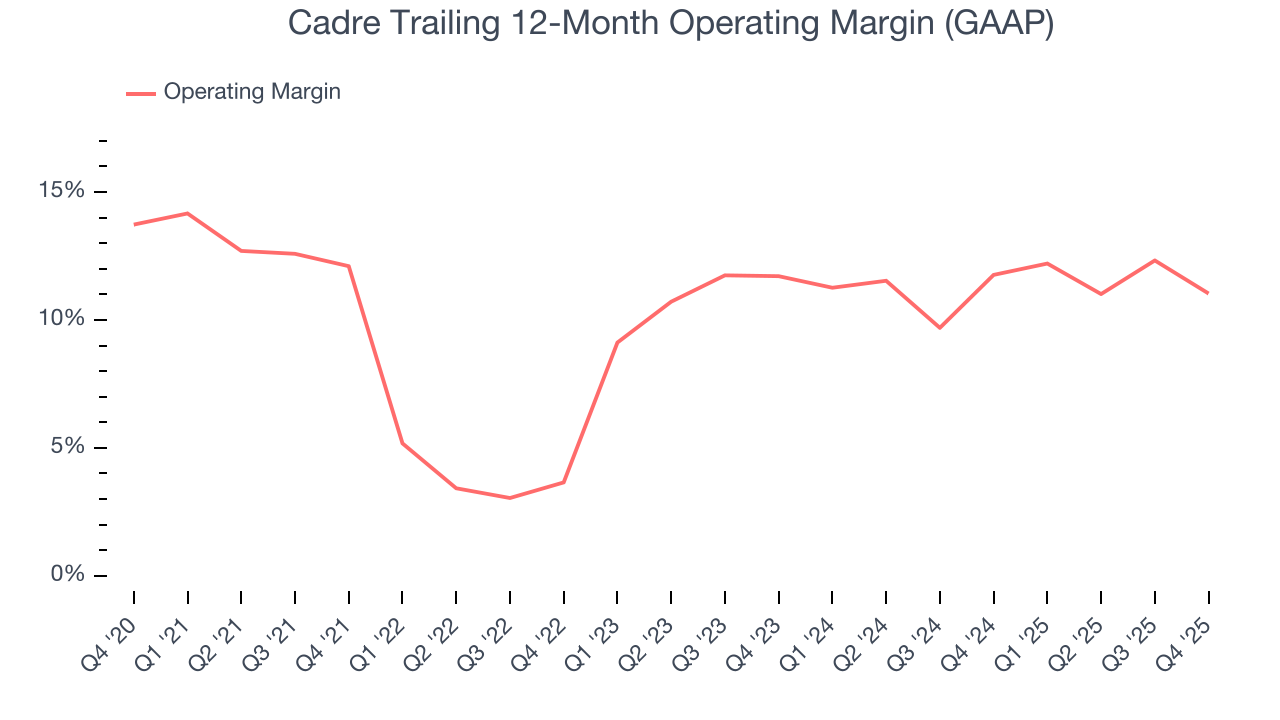

Cadre has managed its cost base well over the last five years. It demonstrated solid profitability for an industrials business, producing an average operating margin of 10.2%.

Analyzing the trend in its profitability, Cadre’s operating margin decreased by 1.1 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, Cadre generated an operating margin profit margin of 12.2%, down 4.5 percentage points year on year. This contraction shows it was less efficient because its expenses increased relative to its revenue.

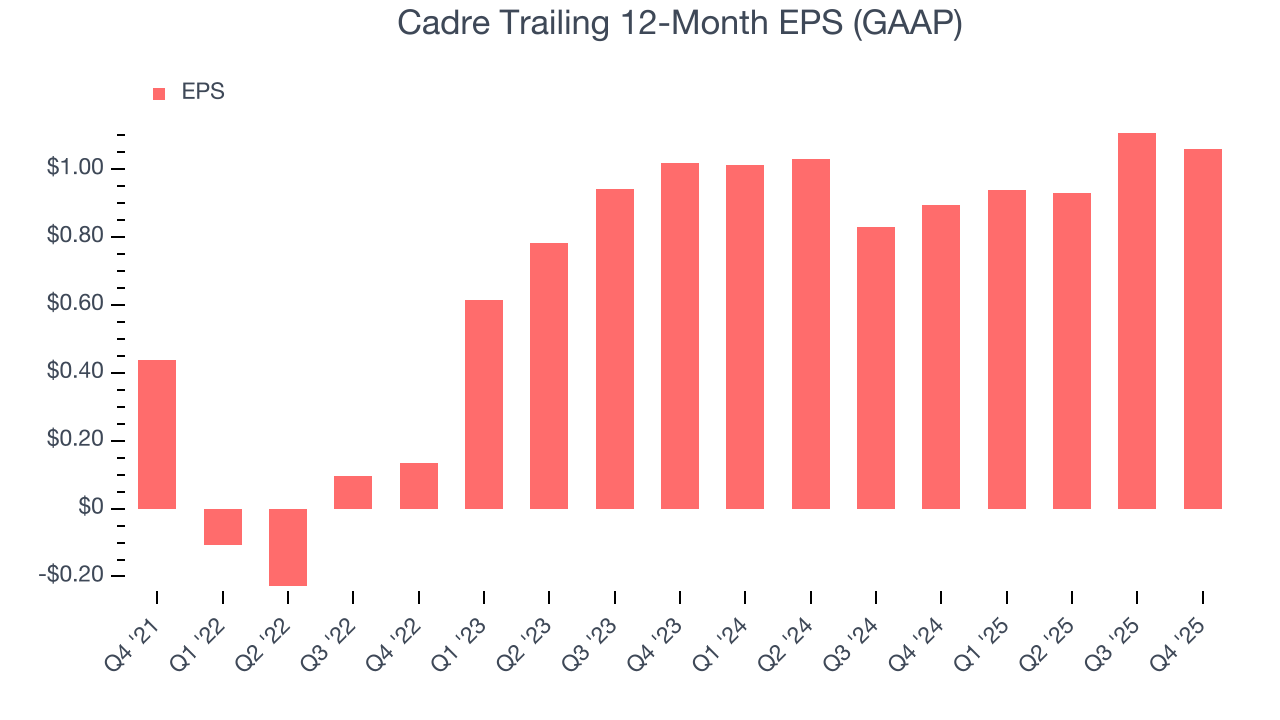

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Cadre’s full-year EPS grew at an astounding 24.7% compounded annual growth rate over the last four years, better than the broader industrials sector.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

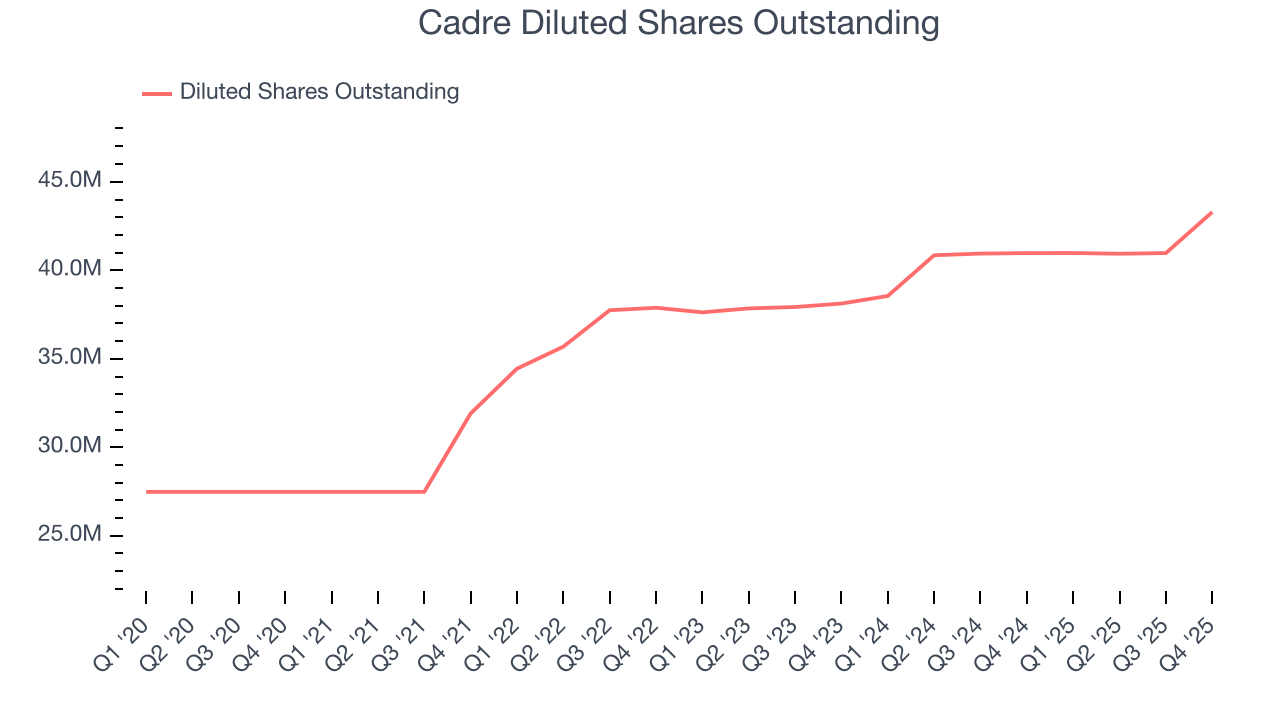

Cadre’s EPS grew at a weak 2% compounded annual growth rate over the last two years, lower than its 12.5% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

Diving into the nuances of Cadre’s earnings can give us a better understanding of its performance. A two-year view shows Cadre has diluted its shareholders, growing its share count by 13.6%. This dilution overshadowed its increased operational efficiency and has led to lower per share earnings.

In Q4, Cadre reported EPS of $0.27, down from $0.32 in the same quarter last year. This print missed analysts’ estimates, but we care more about long-term EPS growth than short-term movements. Over the next 12 months, Wall Street expects Cadre’s full-year EPS of $1.06 to grow 37.4%.

8. Cash Is King

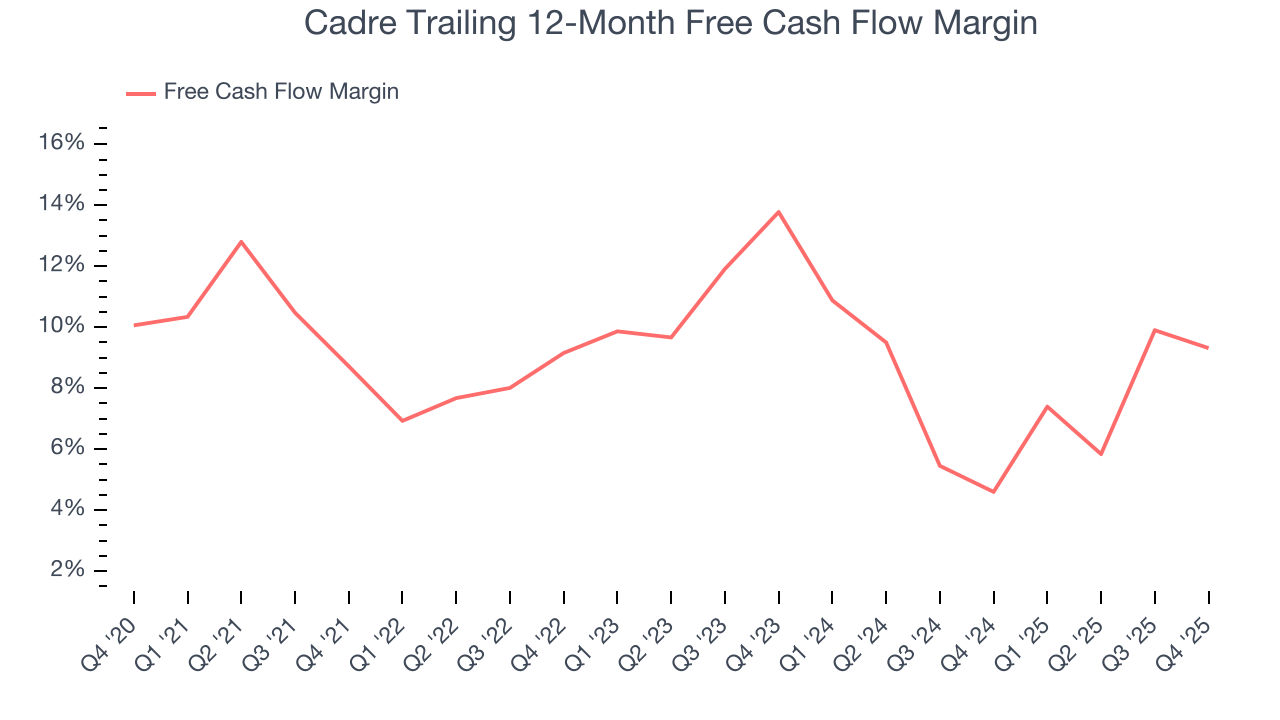

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Cadre has shown impressive cash profitability, enabling it to ride out cyclical downturns more easily while maintaining its investments in new and existing offerings. The company’s free cash flow margin averaged 9% over the last five years, better than the broader industrials sector.

Cadre’s free cash flow clocked in at $17.98 million in Q4, equivalent to a 10.7% margin. The company’s cash profitability regressed as it was 2 percentage points lower than in the same quarter last year, but it’s still above its five-year average. We wouldn’t read too much into this quarter’s decline because capital expenditures can be seasonal and companies often stockpile inventory in anticipation of higher demand, causing short-term swings. Long-term trends carry greater meaning.

9. Return on Invested Capital (ROIC)

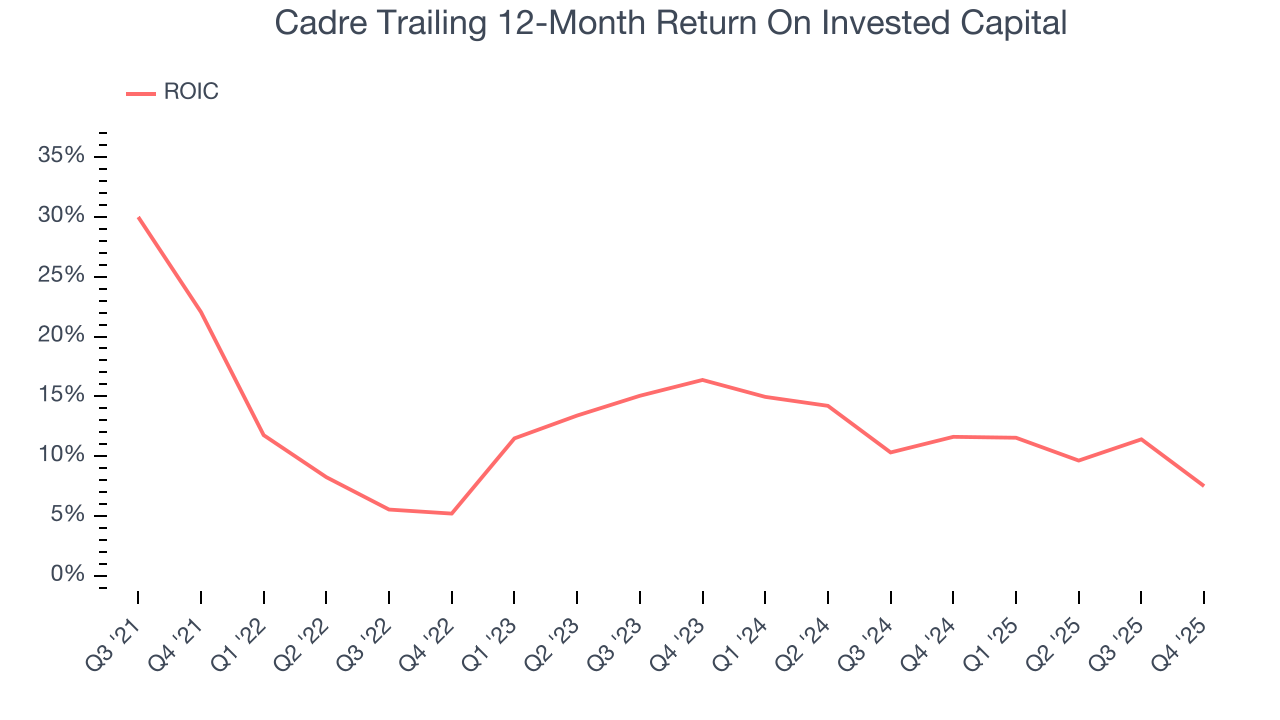

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Cadre’s five-year average ROIC was 12.5%, higher than most industrials businesses. This illustrates its management team’s ability to invest in profitable growth opportunities and generate value for shareholders.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. On average, Cadre’s ROIC decreased by 4.1 percentage points annually each year over the last few years. Only time will tell if its new bets can bear fruit and potentially reverse the trend.

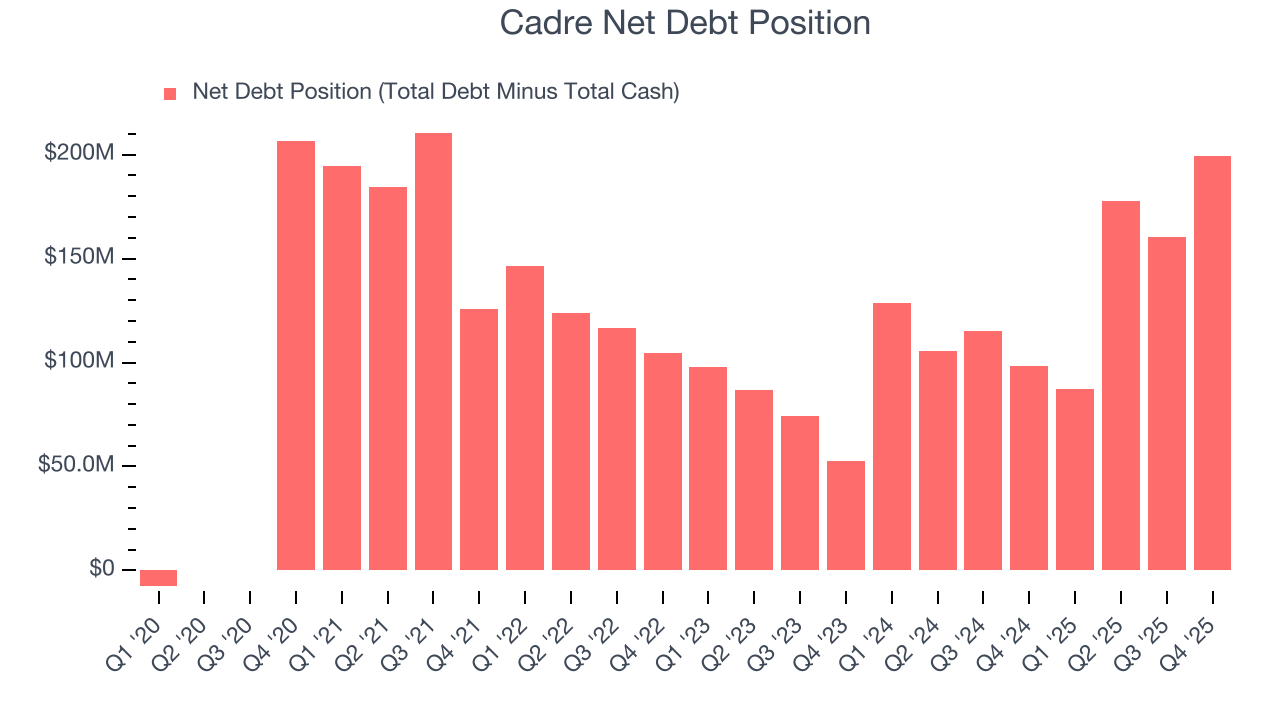

10. Balance Sheet Assessment

Cadre reported $122.9 million of cash and $322.3 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $111.7 million of EBITDA over the last 12 months, we view Cadre’s 1.8× net-debt-to-EBITDA ratio as safe. We also see its $5.22 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from Cadre’s Q4 Results

It was great to see Cadre’s full-year revenue guidance top analysts’ expectations. On the other hand, its revenue missed and its EBITDA fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 1.7% to $40 immediately following the results.

12. Is Now The Time To Buy Cadre?

Updated: March 14, 2026 at 11:09 PM EDT

Before investing in or passing on Cadre, we urge you to understand the company’s business quality (or lack thereof), valuation, and the latest quarterly results - in that order.

There are things to like about Cadre. First off, its revenue growth was good over the last five years and is expected to accelerate over the next 12 months. And while Cadre’s diminishing returns show management's prior bets haven't worked out, its remarkable EPS growth over the last four years shows its profits are trickling down to shareholders.

Cadre’s P/E ratio based on the next 12 months is 24.6x. Looking at the industrials space right now, Cadre trades at a compelling valuation. If you believe in the company and its growth potential, now is an opportune time to buy shares.

Wall Street analysts have a consensus one-year price target of $50.80 on the company (compared to the current share price of $32.11), implying they see 58.2% upside in buying Cadre in the short term.