ChargePoint (CHPT)

ChargePoint catches our eye, but its negative EBITDA and debt balance put it in a tough position.― StockStory Analyst Team

1. News

2. Summary

Why ChargePoint Is Not Exciting

The most prominent EV charging company during the COVID bull market, ChargePoint (NYSE:CHPT) is a provider of electric vehicle charging technology solutions in North America and Europe.

- Historical operating margin losses point to an inefficient cost structure

- Cash burn makes us question whether it can achieve sustainable long-term growth

- Unprofitable operations could lead to additional rounds of dilutive equity financing if the credit window closes

ChargePoint shows some potential. However, we’d hold off on buying the stock until its EBITDA can comfortably service its debt.

Why There Are Better Opportunities Than ChargePoint

ChargePoint is trading at $5.33 per share, or 0.3x forward price-to-sales. The market typically values companies like ChargePoint based on their anticipated profits for the next 12 months, but it expects the business to lose money. We also think the upside isn’t great compared to the potential downside here - there are more exciting stocks to buy.

We’d rather pay a premium for quality. Cheap stocks can look like a great deal at first glance, but they can be value traps. Less earnings power means more reliance on a re-rating to generate good returns; this can be an unlikely scenario for low-quality companies.

3. ChargePoint (CHPT) Research Report: Q4 CY2025 Update

EV charging solutions provider ChargePoint Holdings (NYSE:CHPT) reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 7.3% year on year to $109.3 million. On the other hand, next quarter’s revenue guidance of $95 million was less impressive, coming in 8.5% below analysts’ estimates. Its GAAP loss of $1.85 per share was 6.8% above analysts’ consensus estimates.

ChargePoint (CHPT) Q4 CY2025 Highlights:

- Revenue: $109.3 million vs analyst estimates of $104.7 million (7.3% year-on-year growth, 4.4% beat)

- EPS (GAAP): -$1.85 vs analyst estimates of -$1.98 (6.8% beat)

- Adjusted EBITDA: -$18.39 million (-16.8% margin, 6.2% year-on-year decline)

- Revenue Guidance for Q1 CY2026 is $95 million at the midpoint, below analyst estimates of $103.8 million

- Adjusted EBITDA Margin: -16.8%, in line with the same quarter last year

- Free Cash Flow was -$1.97 million compared to -$4.62 million in the same quarter last year

- Market Capitalization: $153 million

Company Overview

The most prominent EV charging company during the COVID bull market, ChargePoint (NYSE:CHPT) is a provider of electric vehicle charging technology solutions in North America and Europe.

ChargePoint's business model focuses on selling networked charging hardware combined with cloud-based software services. The company typically does not own or operate EV charging assets, nor does it monetize drivers or rely on profits from electricity sales.

The company's product portfolio includes Level 2 AC and DC fast charging equipment, cloud services for station management and driver interfaces, and extended warranty solutions. ChargePoint's latest charging station family, the CP6000 series, is designed for commercial and fleet applications, offering up to 19.2kW per port and compatibility with various connector standards. The company also provides DC fast charging solutions capable of delivering up to 500kW per port, depending on configuration.

ChargePoint's cloud services enable customers to manage charging operations, set pricing, control access, and optimize energy use. The company has recently launched a Network Operations Center to address network reliability through 24/7 proactive station monitoring and predictive analytics.

The company serves three different verticals: commercial, fleet, and residential. Commercial customers include various businesses and organizations looking to provide EV charging as an amenity or service. Fleet customers range from delivery and logistics companies to shared transit operators. In the residential sector, ChargePoint offers solutions for both single-family homes and multi-family dwellings.

4. Renewable Energy

Renewable energy companies are buoyed by the secular trend of green energy that is upending traditional power generation. Those who innovate and evolve with this dynamic market can win share while those who continue to rely on legacy technologies can see diminishing demand, which includes headwinds from increasing regulation against “dirty” energy. Additionally, these companies are at the whim of economic cycles, as interest rates can impact the willingness to invest in renewable energy projects.

Competitors in the electric vehicle charging industry include Blink Charging (NASDAQ:BLNK), EVgo (NASDAQ:EVGO), and Wallbox (NYSE:WBX).

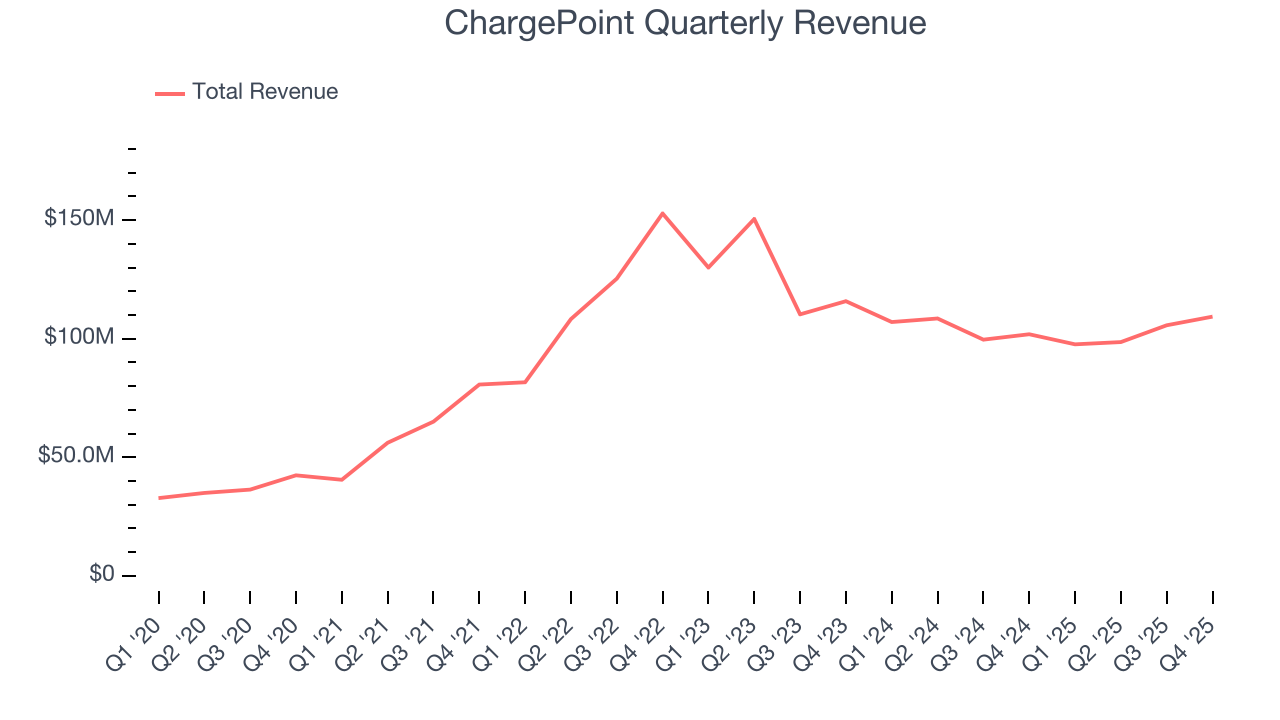

5. Revenue Growth

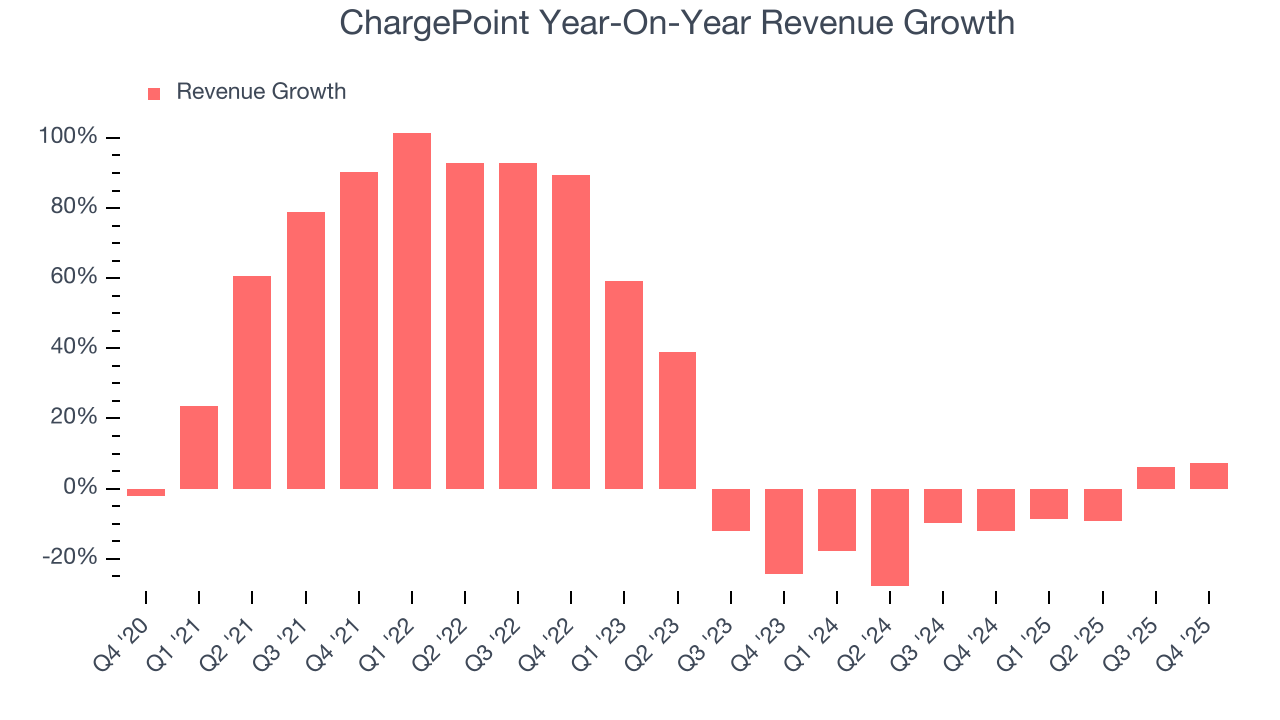

Examining a company’s long-term performance can provide clues about its quality. Any business can have short-term success, but a top-tier one grows for years. Thankfully, ChargePoint’s 22.9% annualized revenue growth over the last five years was incredible. Its growth beat the average industrials company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. ChargePoint’s recent performance marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 9.9% over the last two years.

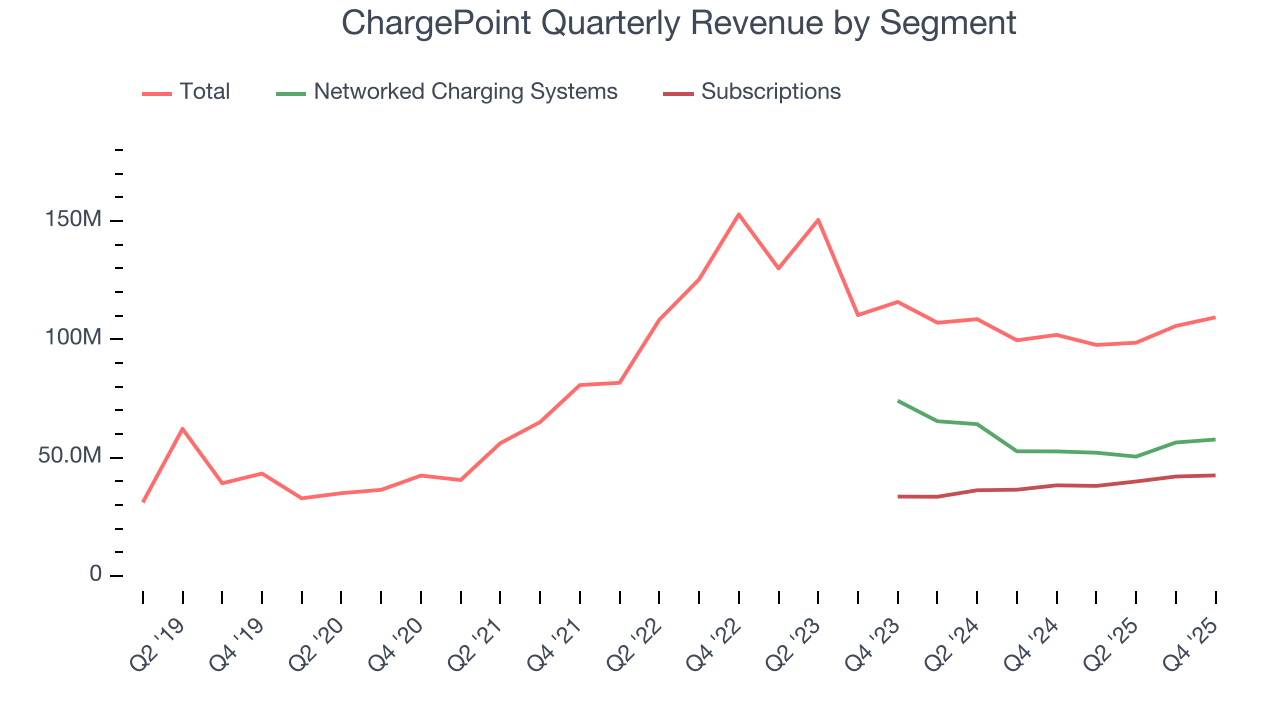

We can better understand the company’s revenue dynamics by analyzing its most important segments, Networked Charging Systems and Subscriptions, which are 52.7% and 38.8% of revenue. Over the last two years, ChargePoint’s Networked Charging Systems revenue (hardware) averaged 10.8% year-on-year declines. On the other hand, its Subscriptions revenue (software) averaged 12.9% growth.

This quarter, ChargePoint reported year-on-year revenue growth of 7.3%, and its $109.3 million of revenue exceeded Wall Street’s estimates by 4.4%. Company management is currently guiding for a 2.7% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 5.9% over the next 12 months. Although this projection indicates its newer products and services will spur better top-line performance, it is still below the sector average.

6. Gross Margin & Pricing Power

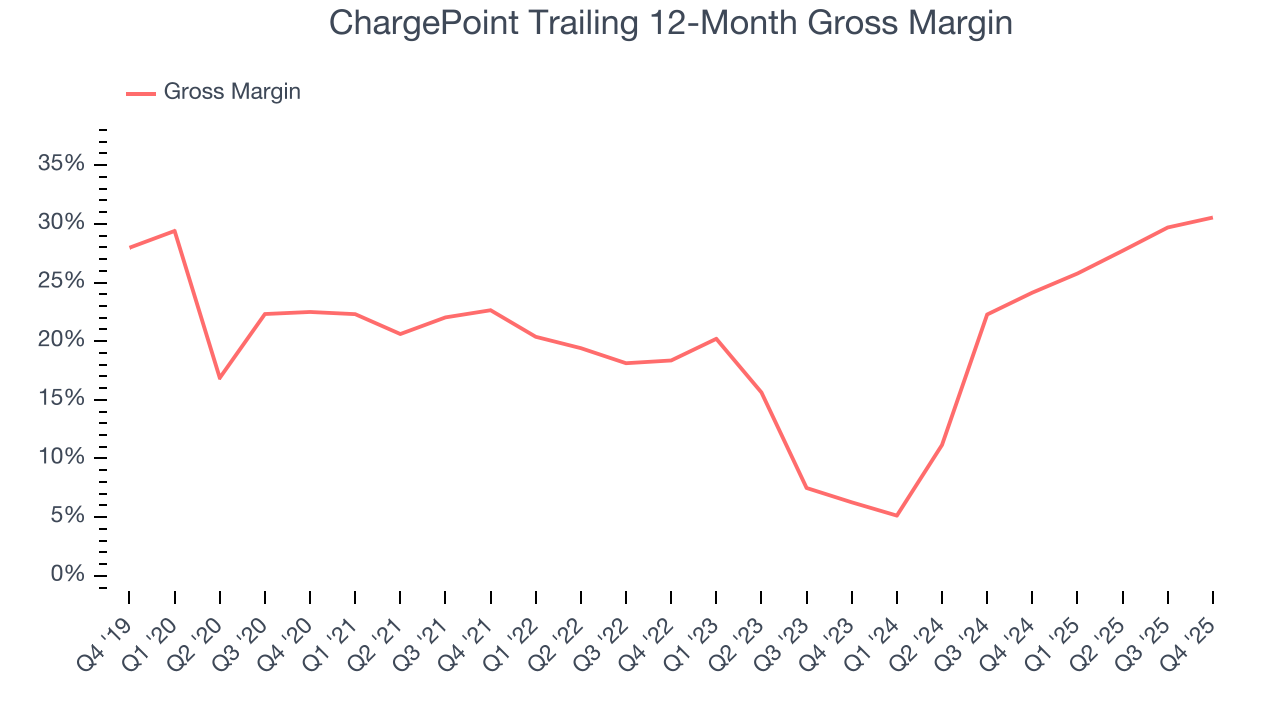

All else equal, we prefer higher gross margins because they usually indicate that a company sells more differentiated products and commands stronger pricing power.

ChargePoint has bad unit economics for an industrials business, signaling it operates in a competitive market. As you can see below, it averaged a 19.5% gross margin over the last five years. That means ChargePoint paid its suppliers a lot of money ($80.50 for every $100 in revenue) to run its business.

In Q4, ChargePoint produced a 31.5% gross profit margin , marking a 3.3 percentage point increase from 28.2% in the same quarter last year. ChargePoint’s full-year margin has also been trending up over the past 12 months, increasing by 6.4 percentage points. If this move continues, it could suggest a less competitive environment where the company has better pricing power and leverage from its growing sales on the fixed portion of its cost of goods sold (such as manufacturing expenses).

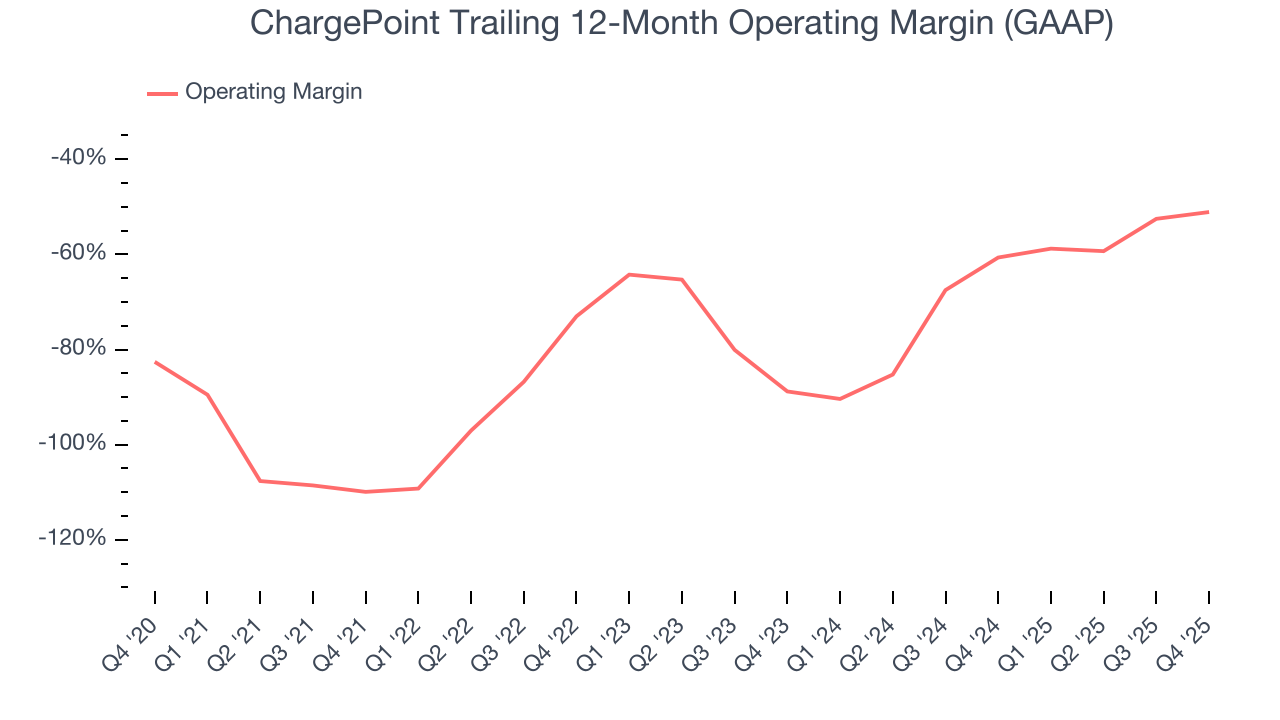

7. Operating Margin

ChargePoint’s high expenses have contributed to an average operating margin of negative 74.4% over the last five years. Unprofitable industrials companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

On the plus side, ChargePoint’s operating margin rose by 58.8 percentage points over the last five years, as its sales growth gave it operating leverage. Still, it will take much more for the company to reach long-term profitability.

This quarter, ChargePoint generated a negative 48.5% operating margin.

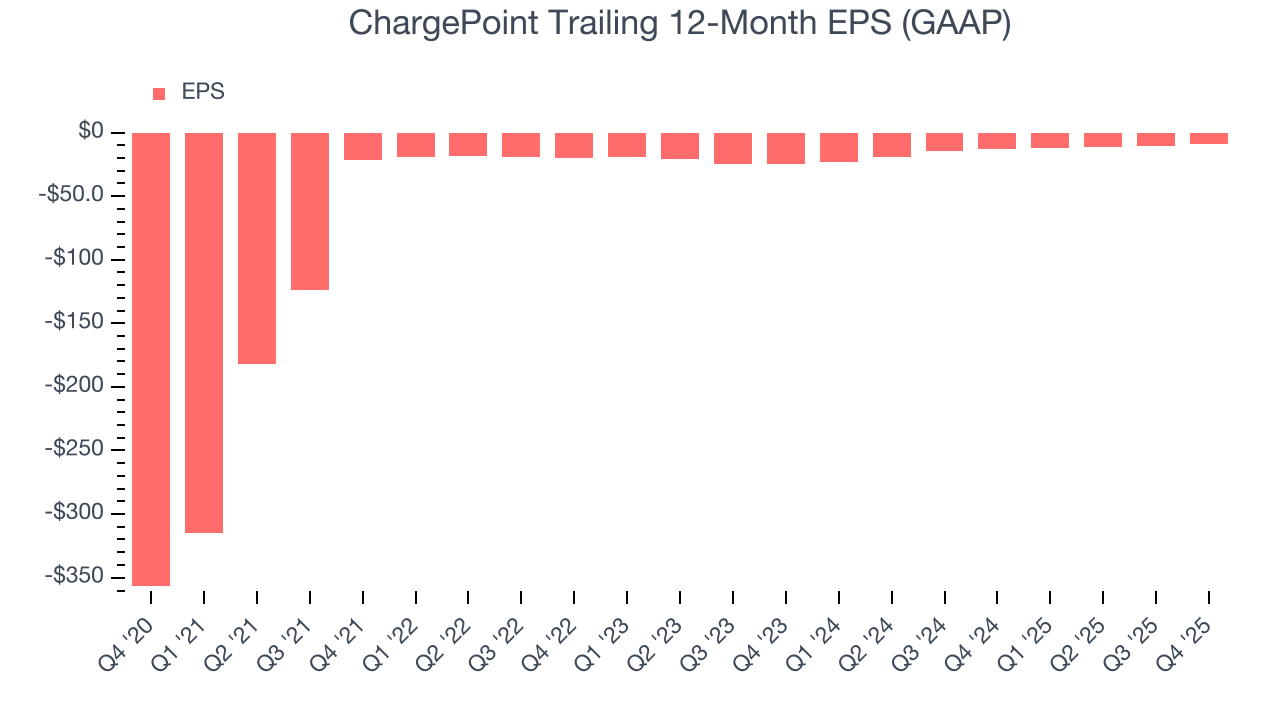

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Although ChargePoint’s full-year earnings are still negative, it reduced its losses and improved its EPS by 51.8% annually over the last five years. The next few quarters will be critical for assessing its long-term profitability. We hope to see an inflection point soon.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For ChargePoint, its two-year annual EPS growth of 38.4% was lower than its five-year trend. We still think its growth was good and hope it can accelerate in the future.

In Q4, ChargePoint reported EPS of negative $1.85, up from negative $2.89 in the same quarter last year. This print beat analysts’ estimates by 6.8%. Over the next 12 months, Wall Street expects ChargePoint to improve its earnings losses. Analysts forecast its full-year EPS of negative $9.30 will advance to negative $6.65.

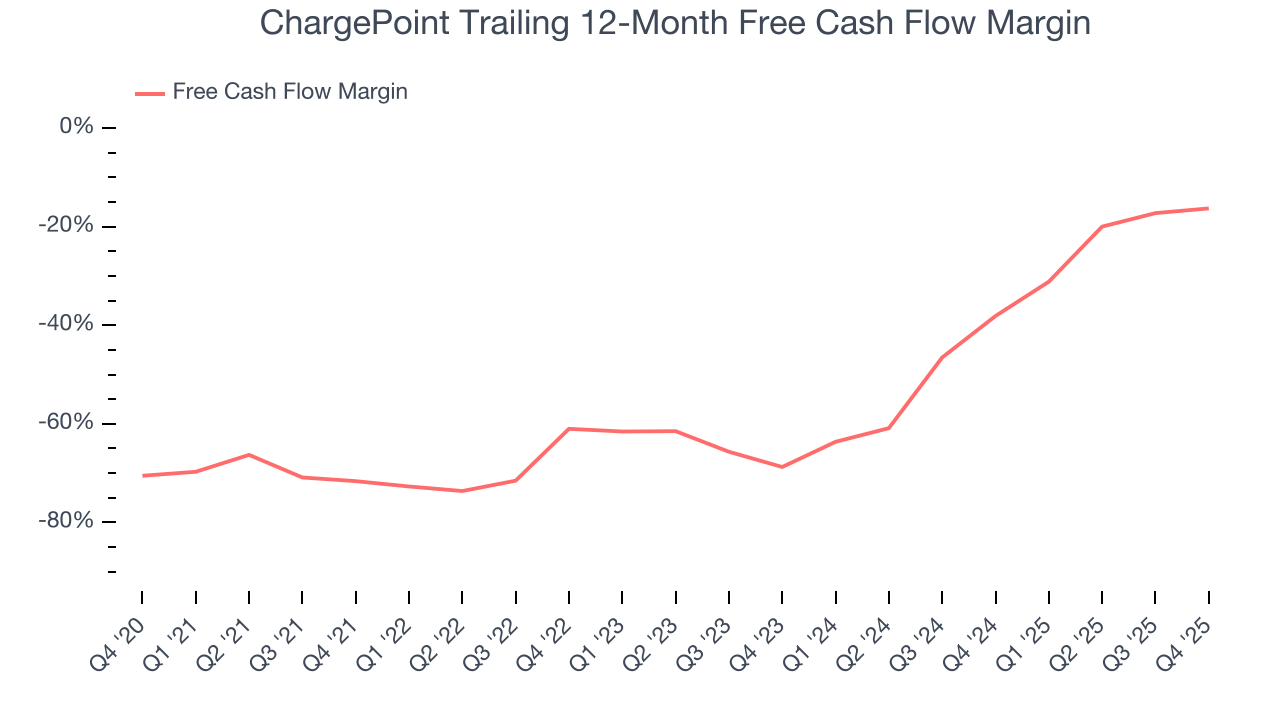

9. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

ChargePoint’s demanding reinvestments have drained its resources over the last five years, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 50.5%, meaning it lit $50.53 of cash on fire for every $100 in revenue.

Taking a step back, an encouraging sign is that ChargePoint’s margin expanded by 55.3 percentage points during that time. In light of its glaring cash burn, however, this improvement is a bucket of hot water in a cold ocean.

ChargePoint burned through $1.97 million of cash in Q4, equivalent to a negative 1.8% margin. The company’s cash burn was similar to its $4.62 million of lost cash in the same quarter last year.

10. Balance Sheet Risk

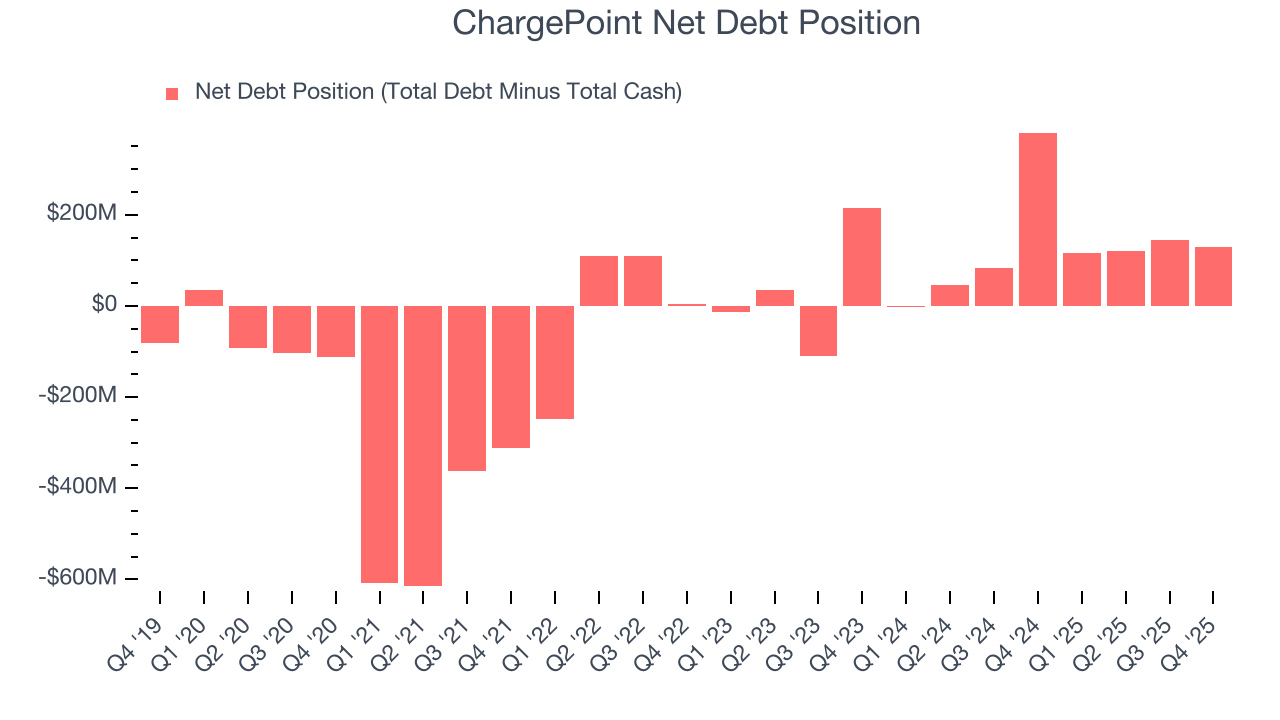

Debt is a tool that can boost company returns but presents risks if used irresponsibly. As long-term investors, we aim to avoid companies taking excessive advantage of this instrument because it could lead to insolvency.

ChargePoint posted negative $82.7 million of EBITDA over the last 12 months, and its $271.5 million of debt exceeds the $142 million of cash on its balance sheet. This is a deal breaker for us because indebted loss-making companies spell trouble.

We implore our readers to tread carefully because credit agencies could downgrade ChargePoint if its unprofitable ways continue, making incremental borrowing more expensive and restricting growth prospects. The company could also be backed into a corner if the market turns unexpectedly. We hope ChargePoint can improve its profitability and remain cautious until then.

11. Key Takeaways from ChargePoint’s Q4 Results

We were impressed by how significantly ChargePoint blew past analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its revenue guidance for next quarter missed and its EBITDA fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 5.1% to $6.20 immediately following the results.

12. Is Now The Time To Buy ChargePoint?

Updated: March 21, 2026 at 11:15 PM EDT

Before deciding whether to buy ChargePoint or pass, we urge investors to consider business quality, valuation, and the latest quarterly results.

Aside from its balance sheet, ChargePoint is a pretty decent company. To kick things off, its revenue growth was exceptional over the last five years. And while its operating margins reveal poor profitability compared to other industrials companies, its rising cash profitability gives it more optionality. On top of that, its expanding operating margin shows the business has become more efficient.

ChargePoint’s forward price-to-sales ratio is 0.3x. Certain aspects of its fundamentals are attractive, but we aren’t investing at the moment because its balance sheet makes us uneasy. We think a potential buyer of the stock should wait until the company generates sufficient cash flows or raises money.

Wall Street analysts have a consensus one-year price target of $6.14 on the company (compared to the current share price of $5.33).