Torrid (CURV)

Torrid keeps us up at night. Not only are its sales cratering but also its low returns on capital suggest it struggles to generate profits.― StockStory Analyst Team

1. News

2. Summary

Why We Think Torrid Will Underperform

Promoting a message of body positivity and inclusiveness, Torrid Holdings (NYSE:CURV) is a plus-size women’s apparel and accessories retailer.

- Store closures and disappointing same-store sales suggest demand is sluggish and it’s rightsizing its operations

- Products have few die-hard fans as sales have declined by 8.1% annually over the last three years

- Limited cash reserves may force the company to seek unfavorable financing terms that could dilute shareholders

Torrid doesn’t pass our quality test. There are more rewarding stocks elsewhere.

Why There Are Better Opportunities Than Torrid

At $1.53 per share, Torrid trades at 7.4x forward EV-to-EBITDA. This is a cheap valuation multiple, but for good reason. You get what you pay for.

Cheap stocks can look like great bargains at first glance, but you often get what you pay for. These mediocre businesses often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. Torrid (CURV) Research Report: Q4 CY2025 Update

Women’s plus-size apparel retailer Torrid Holdings (NYSE:CURV) beat Wall Street’s revenue expectations in Q4 CY2025, but sales fell by 14.3% year on year to $236.2 million. Guidance for next quarter’s revenue was better than expected at $240 million at the midpoint, 0.9% above analysts’ estimates. Its GAAP loss of $0.08 per share was 36% above analysts’ consensus estimates.

Torrid (CURV) Q4 CY2025 Highlights:

- Revenue: $236.2 million vs analyst estimates of $231.1 million (14.3% year-on-year decline, 2.2% beat)

- EPS (GAAP): -$0.08 vs analyst estimates of -$0.13 (36% beat)

- Adjusted EBITDA: $5.15 million vs analyst estimates of $2.30 million (2.2% margin, significant beat)

- Revenue Guidance for Q1 CY2026 is $240 million at the midpoint, above analyst estimates of $237.7 million

- EBITDA guidance for the upcoming financial year 2026 is $70 million at the midpoint, above analyst estimates of $69.08 million

- Operating Margin: -2.1%, down from 1.3% in the same quarter last year

- Free Cash Flow was -$9.32 million, down from $10.25 million in the same quarter last year

- Locations: 483 at quarter end, down from 634 in the same quarter last year

- Same-Store Sales fell 10% year on year (-0.8% in the same quarter last year)

- Market Capitalization: $126 million

Company Overview

Promoting a message of body positivity and inclusiveness, Torrid Holdings (NYSE:CURV) is a plus-size women’s apparel and accessories retailer.

Specifically, the company sells tops, bottoms, dresses, lingerie, shoes, and accessories, in sizes ranging from 10 to 30 under its namesake brand. The Torrid aesthetic is trendy, fashionable, and body-positive. The brand offers clothing and accessories that are designed to flatter a larger frame, while also keeping up with the latest fashion trends. Bold prints, bright colors, and unique designs are common.

Torrid clothing is mid-priced. It’s more expensive than fast fashion, which reflects higher-quality fabrics and construction. However, Torrid items are much more affordable than comparable luxury brand merchandise. The core customer is therefore a plus-size, middle income woman who may be underserved by traditional apparel retailers and brands.

The average Torrid store is approximately 3,000 square feet and is located in a mall or shopping center. The entrance usually features new arrivals and promotions while the center features sections such as dresses, tops, and bottoms. The back is usually devoted to accessories, shoes, and sale items. Torrid has an ecommerce presence that was launched in 2005. The company's website also features a blog and social media accounts that provide customers with fashion inspiration and body-positive messaging.

4. Apparel Retailer

Apparel sales are not driven so much by personal needs but by seasons, trends, and innovation, and over the last few decades, the category has shifted meaningfully online. Retailers that once only had brick-and-mortar stores are responding with omnichannel presences. The online shopping experience continues to improve and retail foot traffic in places like shopping malls continues to stall, so the evolution of clothing sellers marches on.

Retail competitors offering some selection of plus-size women’s apparel and accessories include department stores such as Macy’s (NYSE:M) and Kohl’s (NYSE:KSS) as well as off-price concepts such as TJX (NYSE:TJX) and Ross Stores (NASDAQ:ROST).

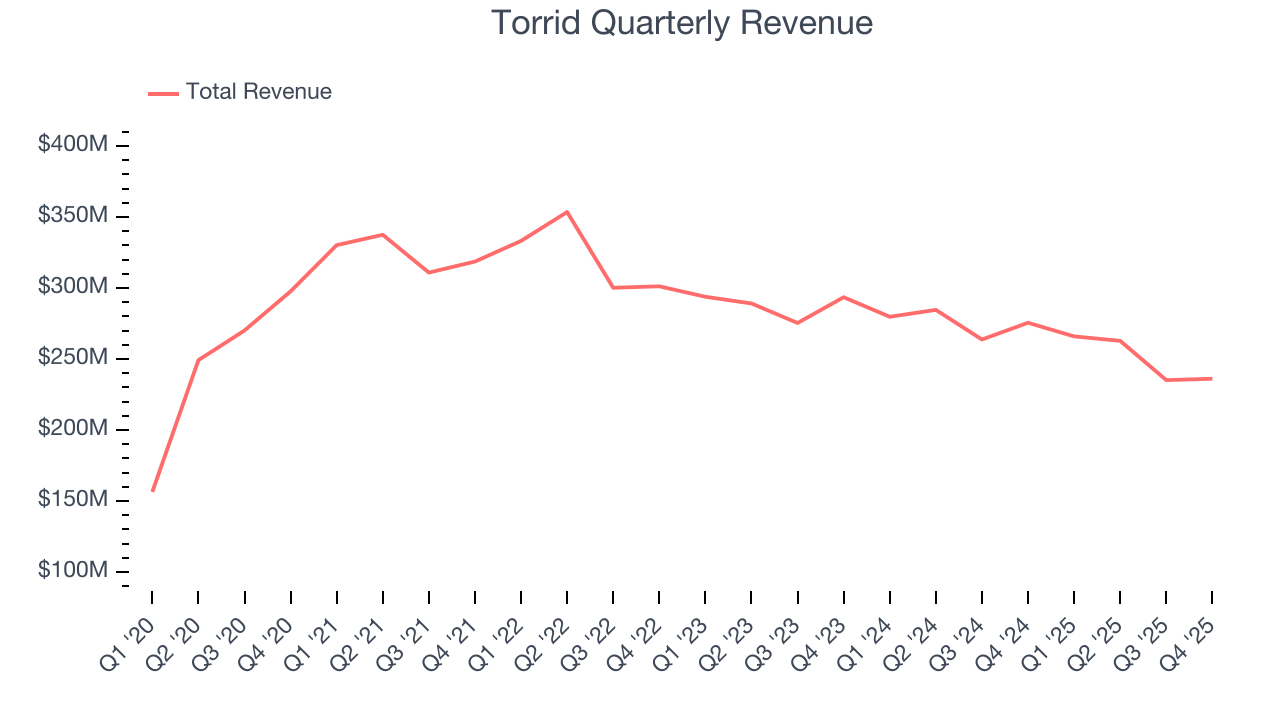

5. Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $1 billion in revenue over the past 12 months, Torrid is a small retailer, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with suppliers.

As you can see below, Torrid’s revenue declined by 8.1% per year over the last three years as it closed stores and observed lower sales at existing, established locations.

This quarter, Torrid’s revenue fell by 14.3% year on year to $236.2 million but beat Wall Street’s estimates by 2.2%. Company management is currently guiding for a 9.8% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to decline by 5.6% over the next 12 months. it’s tough to feel optimistic about a company facing demand difficulties.

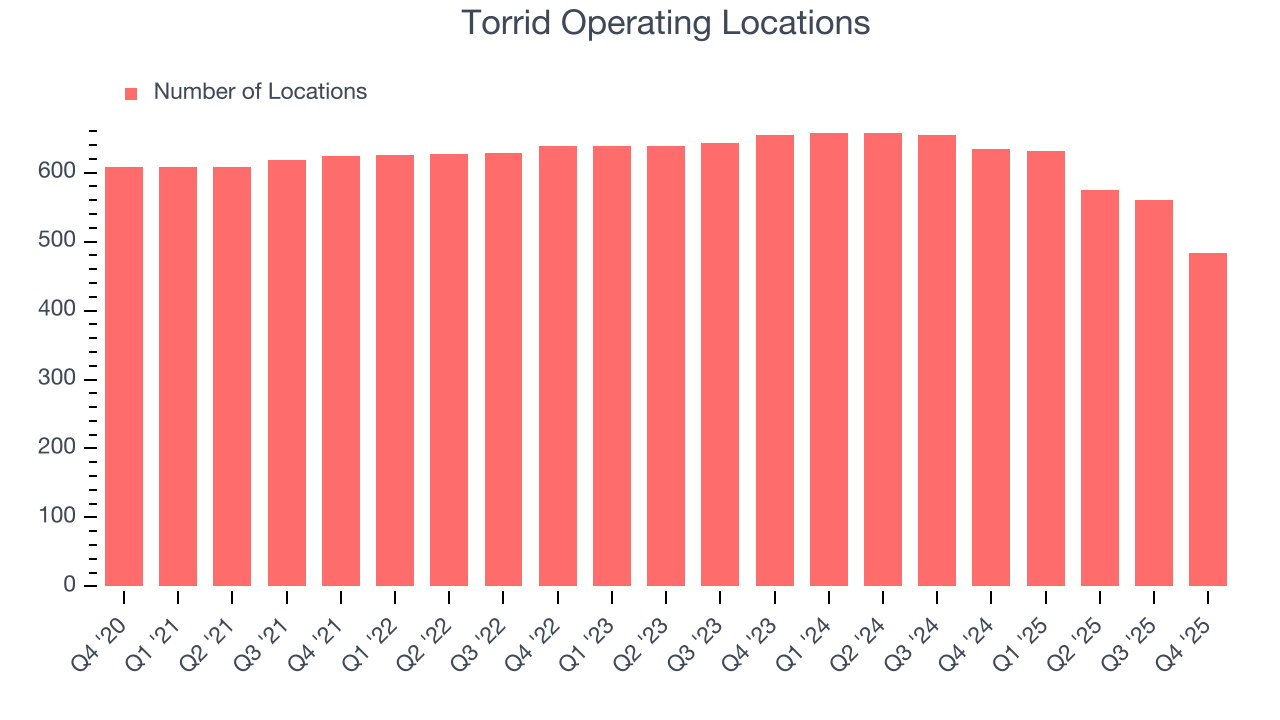

6. Store Performance

Number of Stores

The number of stores a retailer operates is a critical driver of how quickly company-level sales can grow.

Torrid operated 483 locations in the latest quarter. Over the last two years, the company has generally closed its stores, averaging 6.3% annual declines.

When a retailer shutters stores, it usually means that brick-and-mortar demand is less than supply, and it is responding by closing underperforming locations to improve profitability.

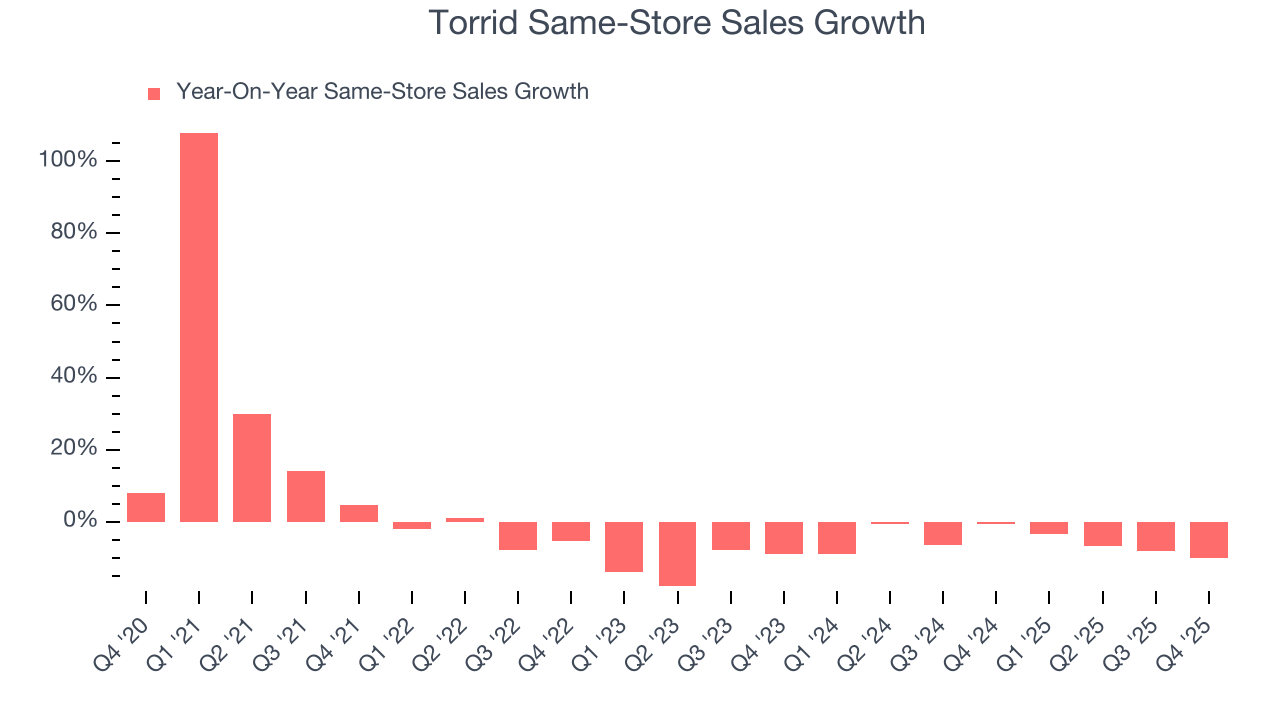

Same-Store Sales

A company's store base only paints one part of the picture. When demand is high, it makes sense to open more. But when demand is low, it’s prudent to close some locations and use the money in other ways. Same-store sales is an industry measure of whether revenue is growing at those existing stores and is driven by customer visits (often called traffic) and the average spending per customer (ticket).

Torrid’s demand has been shrinking over the last two years as its same-store sales have averaged 5.7% annual declines. This performance isn’t ideal, and Torrid is attempting to boost same-store sales by closing stores (fewer locations sometimes lead to higher same-store sales).

In the latest quarter, Torrid’s same-store sales fell by 10% year on year. This decrease represents a further deceleration from its historical levels. We hope the business can get back on track.

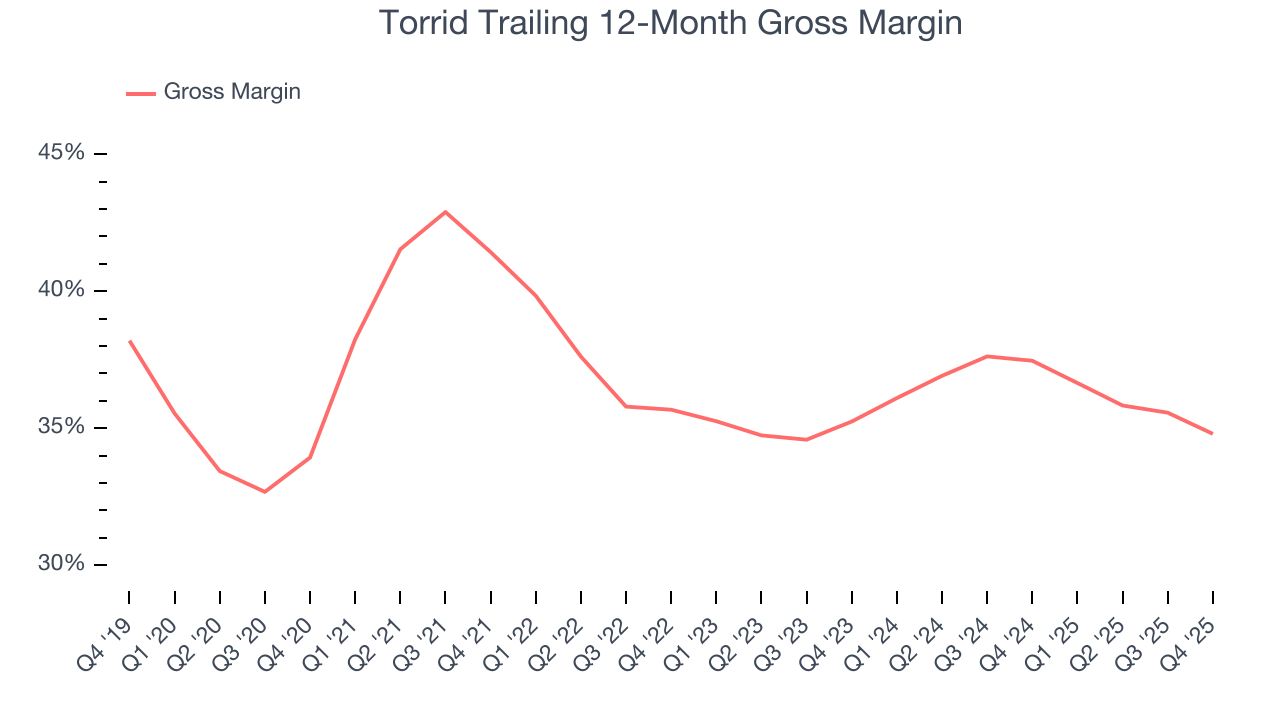

7. Gross Margin & Pricing Power

Gross profit margins are an important measure of a retailer’s pricing power, product differentiation, and negotiating leverage.

Torrid has bad unit economics for a retailer, giving it less room to reinvest and grow its presence. As you can see below, it averaged a 36.2% gross margin over the last two years. That means Torrid paid its suppliers a lot of money ($63.81 for every $100 in revenue) to run its business.

In Q4, Torrid produced a 30% gross profit margin , marking a 3.6 percentage point decrease from 33.6% in the same quarter last year. Torrid’s full-year margin has also been trending down over the past 12 months, decreasing by 2.7 percentage points. If this move continues, it could suggest a more competitive environment with some pressure to discount products and higher input costs (such as labor and freight expenses to transport goods).

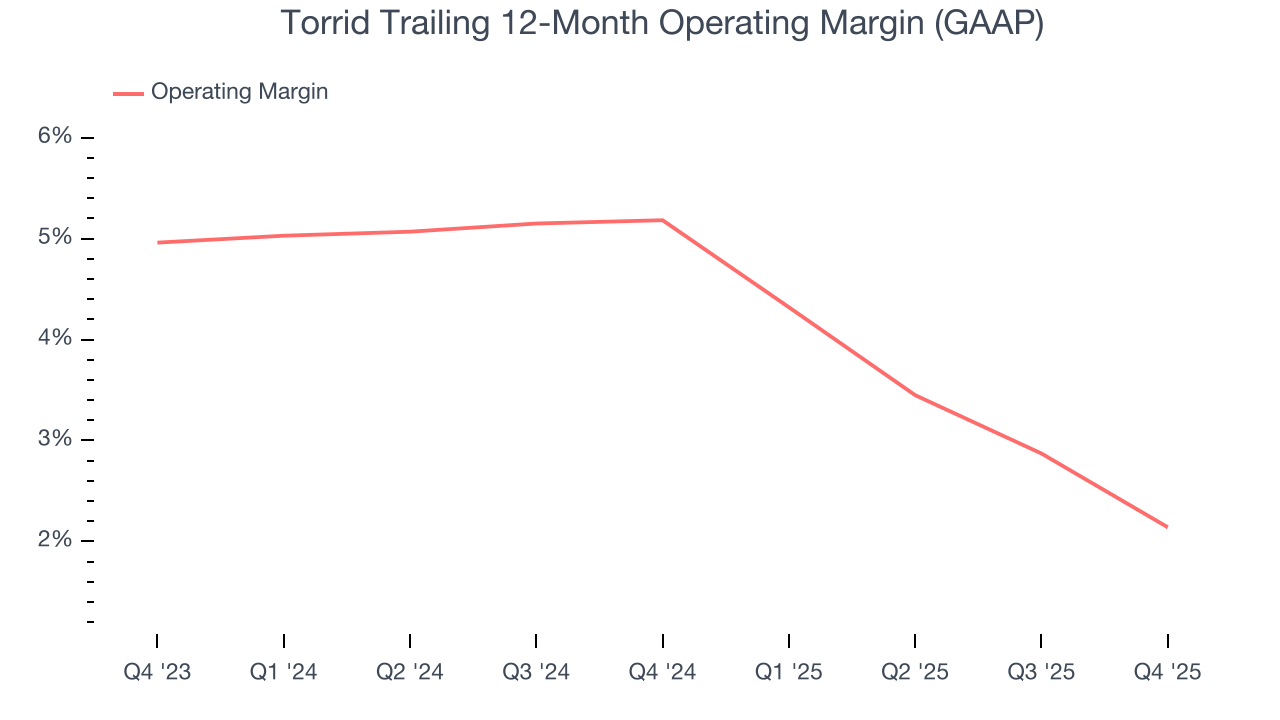

8. Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Torrid was profitable over the last two years but held back by its large cost base. Its average operating margin of 3.7% was weak for a consumer retail business. This result isn’t too surprising given its low gross margin as a starting point.

Analyzing the trend in its profitability, Torrid’s operating margin decreased by 3 percentage points over the last year. Torrid’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

This quarter, Torrid generated an operating margin profit margin of negative 2.1%, down 3.4 percentage points year on year. Since Torrid’s gross margin decreased more than its operating margin, we can assume its recent inefficiencies were driven more by weaker leverage on its cost of sales rather than increased marketing, and administrative overhead expenses.

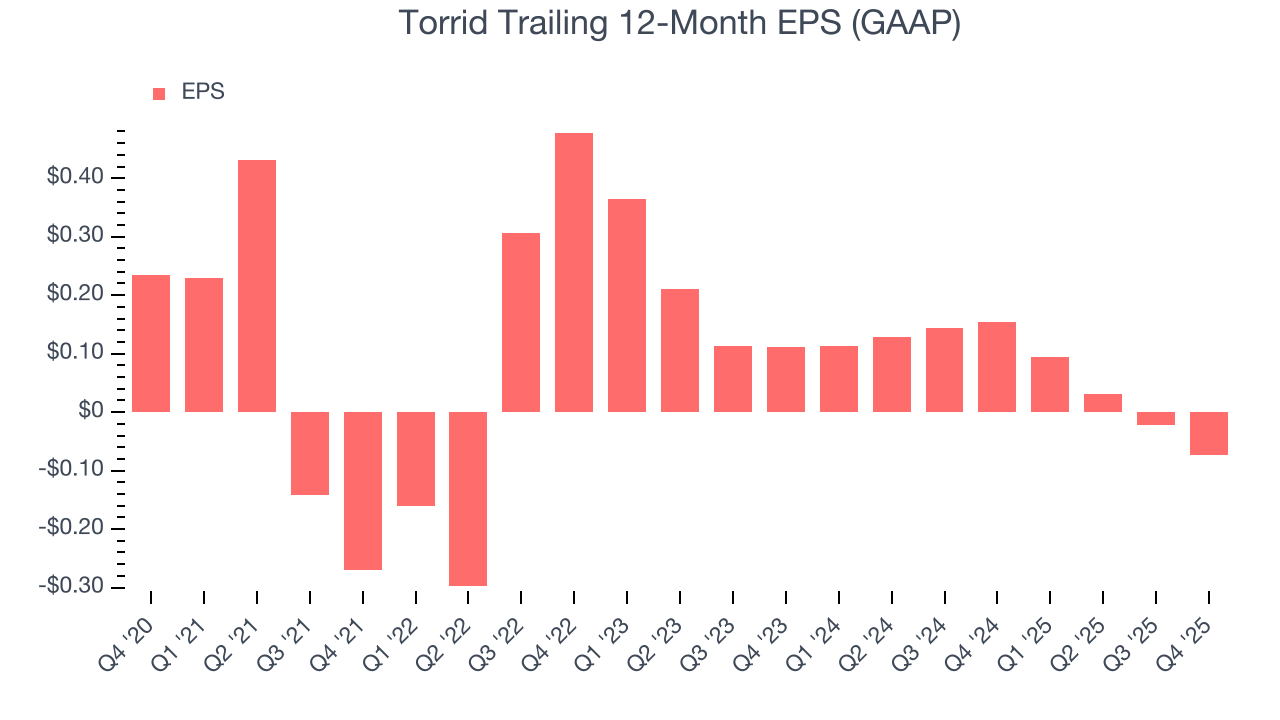

9. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Torrid, its EPS declined by 29.1% annually over the last three years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

In Q4, Torrid reported EPS of negative $0.08, down from negative $0.03 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Torrid to improve its earnings losses. Analysts forecast its full-year EPS of negative $0.07 will advance to negative $0.04.

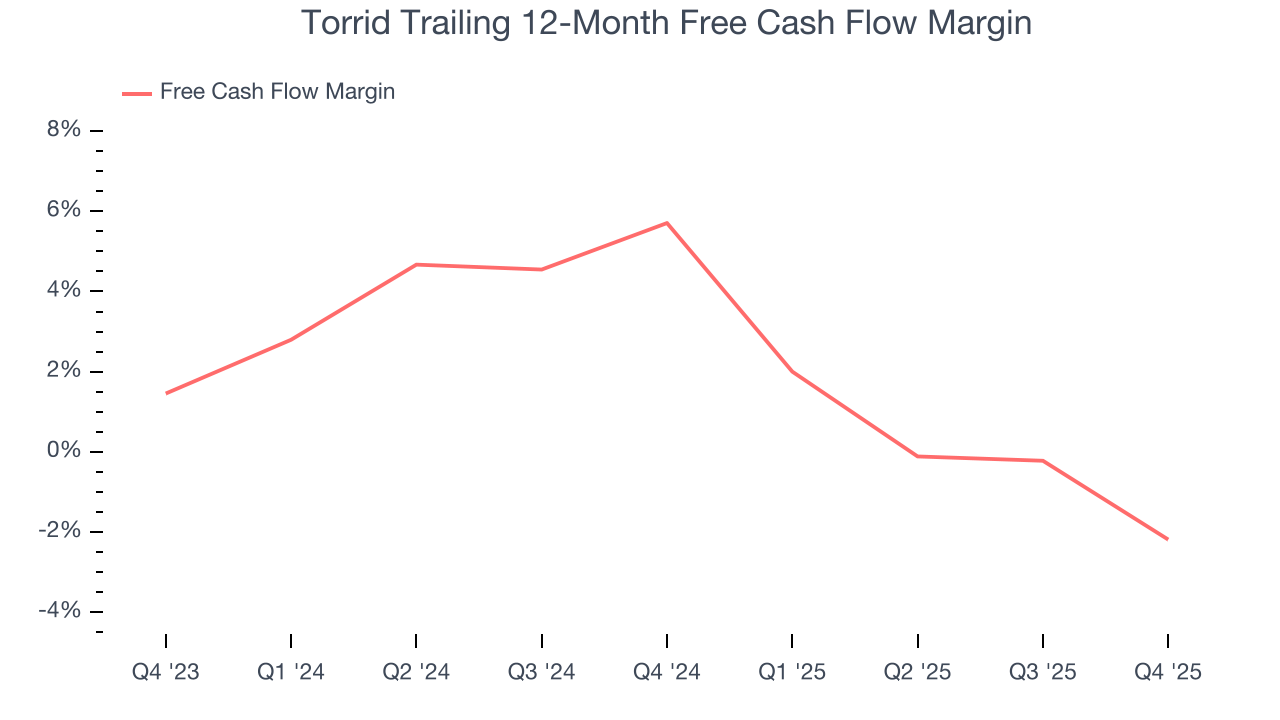

10. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Torrid has shown mediocre cash profitability relative to peers over the last two years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 2%, below what we’d expect for a consumer retail business.

Taking a step back, we can see that Torrid’s margin dropped by 7.9 percentage points over the last year. This decrease warrants extra caution because Torrid failed to grow its same-store sales. Its cash profitability could decay further if it tries to reignite growth by opening new stores.

Torrid burned through $9.32 million of cash in Q4, equivalent to a negative 3.9% margin. The company’s cash flow turned negative after being positive in the same quarter last year, suggesting its historical struggles have dragged on.

11. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Torrid historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 11.3%, somewhat low compared to the best consumer retail companies that consistently pump out 25%+.

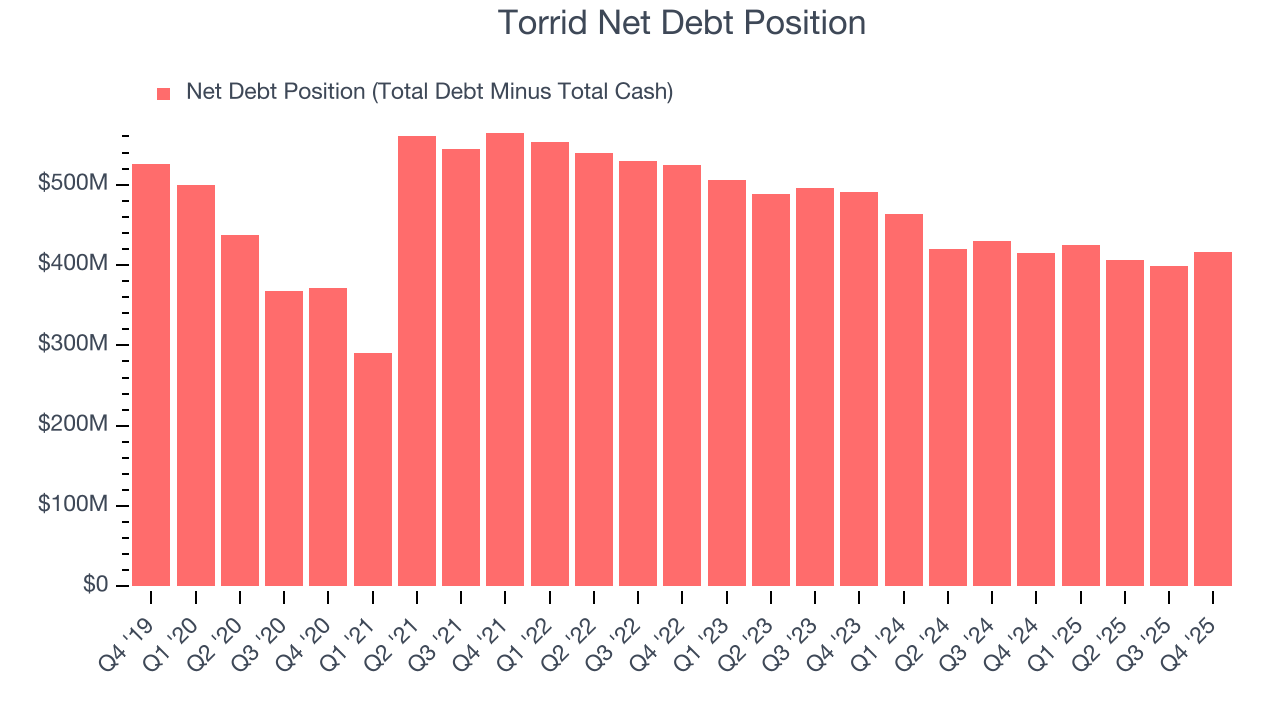

12. Balance Sheet Risk

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

Torrid burned through $21.87 million of cash over the last year, and its $436.5 million of debt exceeds the $20.44 million of cash on its balance sheet. This is a deal breaker for us because indebted loss-making companies spell trouble.

Unless the Torrid’s fundamentals change quickly, it might find itself in a position where it must raise capital from investors to continue operating. Whether that would be favorable is unclear because dilution is a headwind for shareholder returns.

We remain cautious of Torrid until it generates consistent free cash flow or any of its announced financing plans materialize on its balance sheet.

13. Key Takeaways from Torrid’s Q4 Results

It was good to see Torrid beat analysts’ EPS expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. On the other hand, its gross margin missed and its EBITDA guidance for next quarter fell short of Wall Street’s estimates. Overall, this print was mixed but still had some key positives. The stock traded up 23.2% to $1.55 immediately after reporting.

14. Is Now The Time To Buy Torrid?

Updated: March 22, 2026 at 10:51 PM EDT

When considering an investment in Torrid, investors should account for its valuation and business qualities as well as what’s happened in the latest quarter.

We see the value of companies helping consumers, but in the case of Torrid, we’re out. First off, its revenue has declined over the last three years. While its projected EPS for the next year implies the company’s fundamentals will improve, the downside is its declining EPS over the last three years makes it a less attractive asset to the public markets. On top of that, its declining physical locations suggests its demand is falling.

Torrid’s EV-to-EBITDA ratio based on the next 12 months is 7.4x. While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are better investments elsewhere.

Wall Street analysts have a consensus one-year price target of $1.58 on the company (compared to the current share price of $1.53).