Enovis (ENOV)

We wouldn’t buy Enovis. Its falling revenue and negative returns on capital suggest it’s destroying value as demand fizzles out.― StockStory Analyst Team

1. News

2. Summary

Why We Think Enovis Will Underperform

With a focus on helping patients regain or maintain their natural motion, Enovis (NYSE:ENOV) develops and manufactures medical devices for orthopedic care, from injury prevention and pain management to joint replacement and rehabilitation.

- Push for growth has led to negative returns on capital, signaling value destruction, and its falling returns suggest its earlier profit pools are drying up

- Falling earnings per share over the last five years has some investors worried as stock prices ultimately follow EPS over the long term

- Products and services are facing significant end-market challenges during this cycle as sales have declined by 6% annually over the last five years

Enovis’s quality doesn’t meet our expectations. We’ve identified better opportunities elsewhere.

Why There Are Better Opportunities Than Enovis

At $21.92 per share, Enovis trades at 6.4x forward P/E. This sure is a cheap multiple, but you get what you pay for.

Our advice is to pay up for elite businesses whose advantages are tailwinds to earnings growth. Don’t get sucked into lower-quality businesses just because they seem like bargains. These mediocre businesses often never achieve a higher multiple as hoped, a phenomenon known as a “value trap”.

3. Enovis (ENOV) Research Report: Q4 CY2025 Update

Medical technology company Enovis Corporation (NYSE:ENOV) missed Wall Street’s revenue expectations in Q4 CY2025 as sales rose 2.6% year on year to $575.8 million. The company’s full-year revenue guidance of $2.34 billion at the midpoint came in 0.7% below analysts’ estimates. Its non-GAAP profit of $0.95 per share was 13.1% above analysts’ consensus estimates.

Enovis (ENOV) Q4 CY2025 Highlights:

- Revenue: $575.8 million vs analyst estimates of $583.8 million (2.6% year-on-year growth, 1.4% miss)

- Adjusted EPS: $0.95 vs analyst estimates of $0.84 (13.1% beat)

- Adjusted EBITDA: $111.9 million vs analyst estimates of $109.2 million (19.4% margin, 2.5% beat)

- Adjusted EPS guidance for the upcoming financial year 2026 is $3.63 at the midpoint, beating analyst estimates by 6.1%

- EBITDA guidance for the upcoming financial year 2026 is $430 million at the midpoint, in line with analyst expectations

- Operating Margin: -87.2%, up from -118% in the same quarter last year

- Free Cash Flow Margin: 5.6%, similar to the same quarter last year

- Market Capitalization: $1.28 billion

Company Overview

With a focus on helping patients regain or maintain their natural motion, Enovis (NYSE:ENOV) develops and manufactures medical devices for orthopedic care, from injury prevention and pain management to joint replacement and rehabilitation.

Enovis operates through two main segments: Prevention & Recovery and Reconstructive. The Prevention & Recovery segment offers products used by healthcare professionals to treat patients with musculoskeletal conditions. These include rigid and soft orthopedic braces, hot and cold therapy devices, bone growth stimulators, compression garments, therapeutic footwear, and electrical stimulators for pain management. For example, an athlete recovering from an ACL tear might use an Enovis knee brace during rehabilitation, while a patient with chronic pain might utilize one of their electrical stimulation devices as part of their therapy regimen.

The Reconstructive segment provides a comprehensive suite of joint replacement products for hips, knees, shoulders, elbows, feet, ankles, and fingers, along with surgical productivity tools. A patient suffering from severe osteoarthritis might receive an Enovis knee implant to reduce pain and improve mobility when conservative treatments have failed.

Enovis reaches its customers through multiple distribution channels, including independent distributors and direct sales representatives. Its products are used by orthopedic specialists, surgeons, physical therapists, athletic trainers, and other healthcare professionals across various treatment settings. The company also sells directly to retail consumers for at-home physical therapy and injury prevention.

The company employs its "Enovis Growth eXcellence" (EGX) business system—a set of tools, processes, and cultural elements—to continuously improve patient outcomes and drive growth. This system helps Enovis standardize best practices across its operations and focus on innovation.

While the United States represents Enovis's largest market, approximately one-third of its sales come from international operations, primarily in Europe with additional presence in the Asia-Pacific region. Like other medical device manufacturers, Enovis operates in a highly regulated environment, with products subject to FDA oversight in the United States and similar regulatory bodies internationally.

4. Medical Devices & Supplies - Specialty

The medical devices industry operates a business model that balances steady demand with significant investments in innovation and regulatory compliance. The industry benefits from recurring revenue streams tied to consumables, maintenance services, and incremental upgrades to the latest technologies, although specialty devices are more niche. The capital-intensive nature of product development, coupled with lengthy regulatory pathways and the need for clinical validation, can weigh on profitability and timelines. In addition, there are constant pricing pressures from healthcare systems and insurers maximizing cost efficiency. Over the next several years, one tailwind is demographic–aging populations means rising chronic disease rates that drive greater demand for medical interventions and monitoring solutions. Advances in digital health, such as remote patient monitoring and smart devices, are also expected to unlock new demand by shortening upgrade cycles. On the other hand, the industry faces headwinds from pricing and reimbursement pressures as healthcare providers increasingly adopt value-based care models. Additionally, the integration of cybersecurity for connected devices adds further risk and complexity for device manufacturers.

Enovis competes with several major medical device companies, including Össur and Breg in the Prevention & Recovery segment, and orthopedic giants like Stryker, Zimmer Biomet, and DePuy Synthes (a Johnson & Johnson company) in the Reconstructive segment.

5. Revenue Scale

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With just $2.25 billion in revenue over the past 12 months, Enovis lacks scale in an industry where it matters. This makes it difficult to build trust with customers because healthcare is heavily regulated, complex, and resource-intensive.

6. Revenue Growth

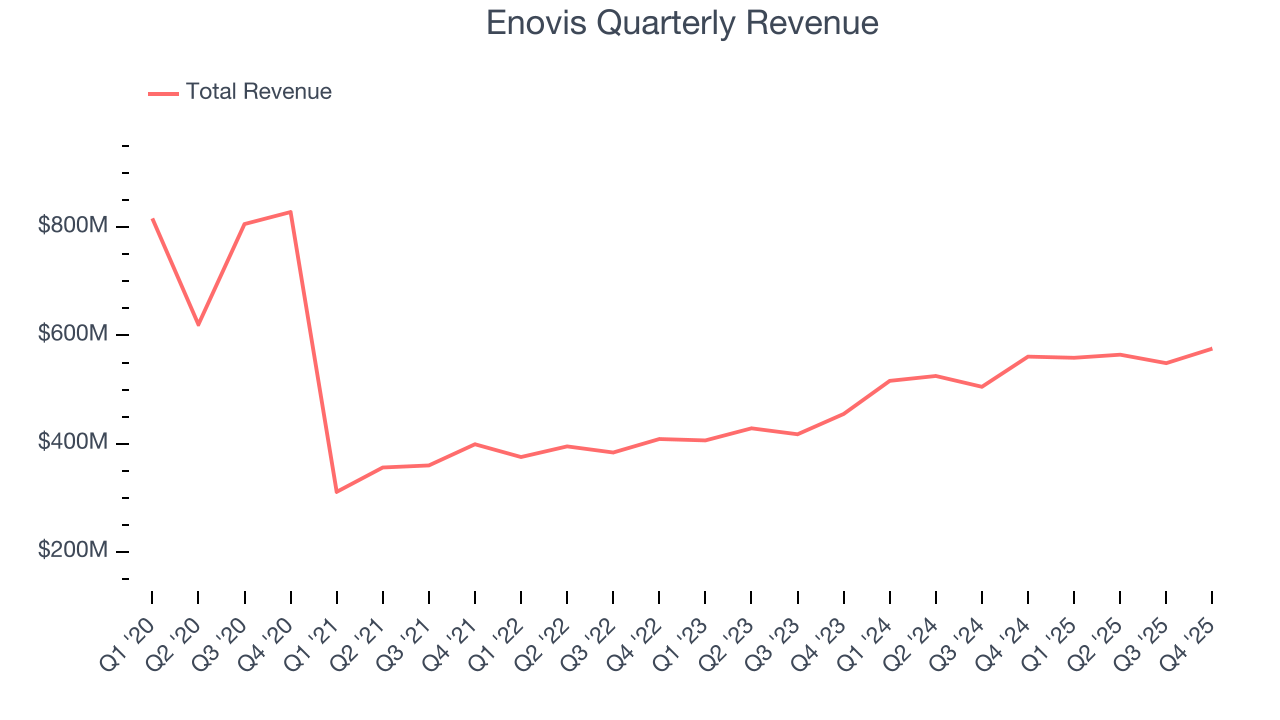

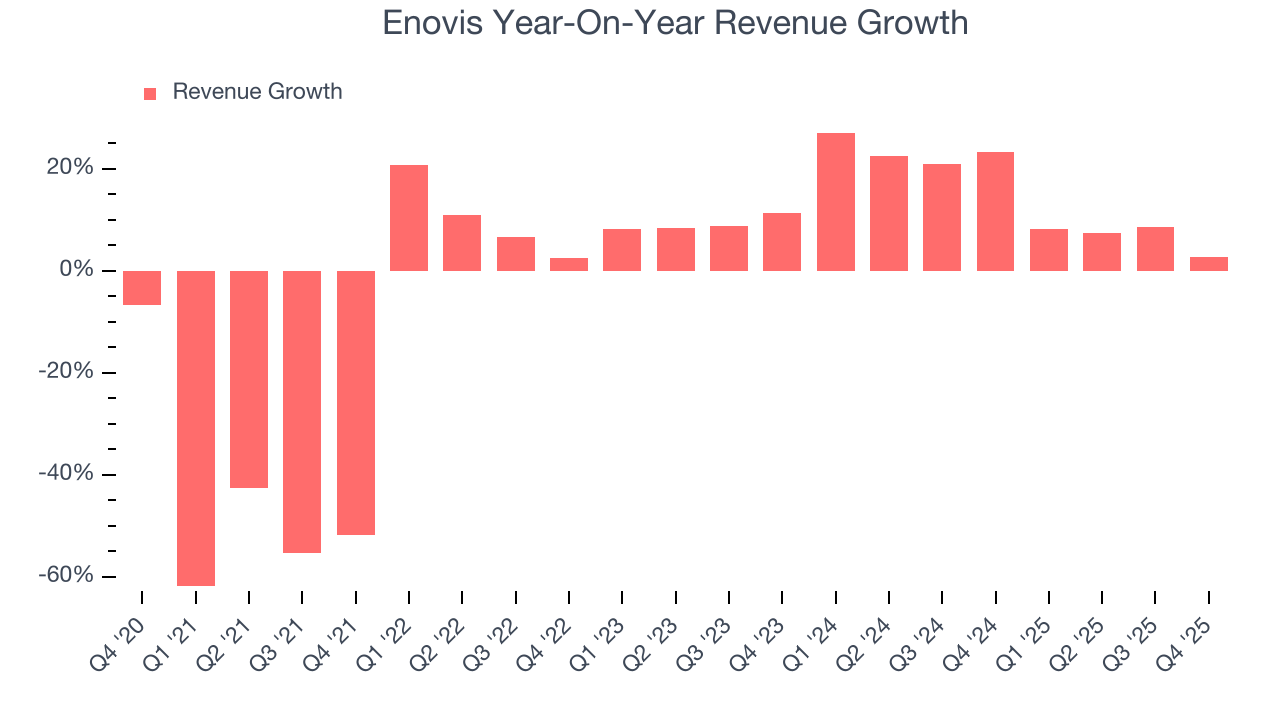

A company’s long-term performance is an indicator of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Enovis’s demand was weak over the last five years as its sales fell at a 6% annual rate. This was below our standards and suggests it’s a low quality business.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Enovis’s annualized revenue growth of 14.8% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

This quarter, Enovis’s revenue grew by 2.6% year on year to $575.8 million, falling short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 5% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and indicates its products and services will face some demand challenges.

7. Operating Margin

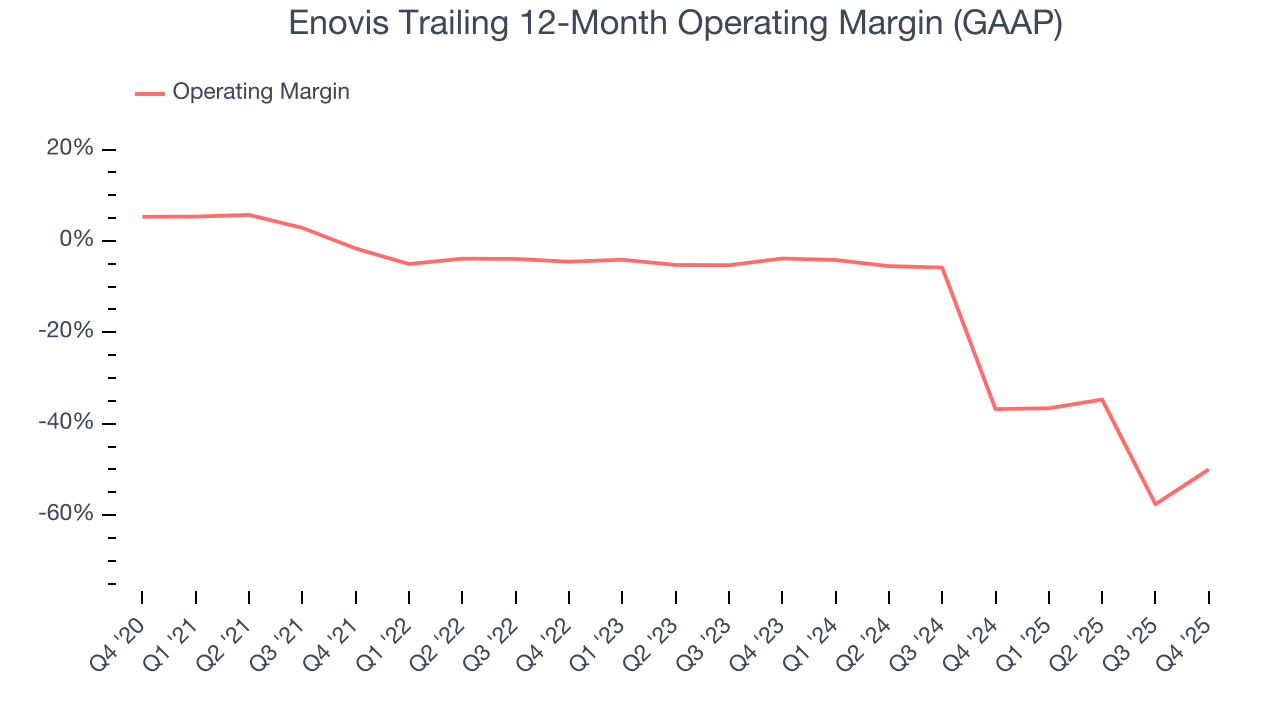

Enovis’s high expenses have contributed to an average operating margin of negative 22.8% over the last five years. Unprofitable healthcare companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

Analyzing the trend in its profitability, Enovis’s operating margin decreased by 48.4 percentage points over the last five years. The company’s two-year trajectory also shows it failed to get its profitability back to the peak as its margin fell by 46.2 percentage points. This performance was poor no matter how you look at it - it shows its expenses were rising and it couldn’t pass those costs onto its customers.

In Q4, Enovis generated a negative 87.2% operating margin. The company's consistent lack of profits raise a flag.

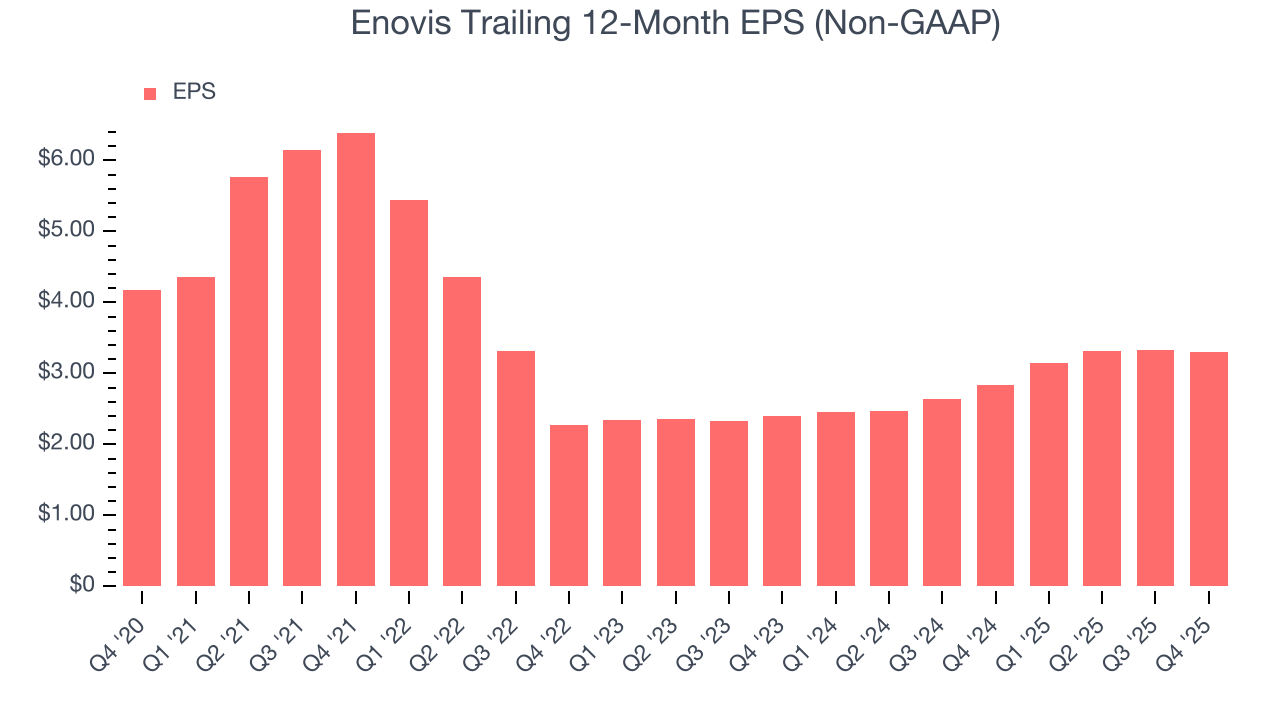

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Enovis, its EPS and revenue declined by 4.6% and 6% annually over the last five years. We tend to steer our readers away from companies with falling revenue and EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, Enovis’s low margin of safety could leave its stock price susceptible to large downswings.

In Q4, Enovis reported adjusted EPS of $0.95, down from $0.98 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Enovis’s full-year EPS of $3.30 to grow 3%.

9. Cash Is King

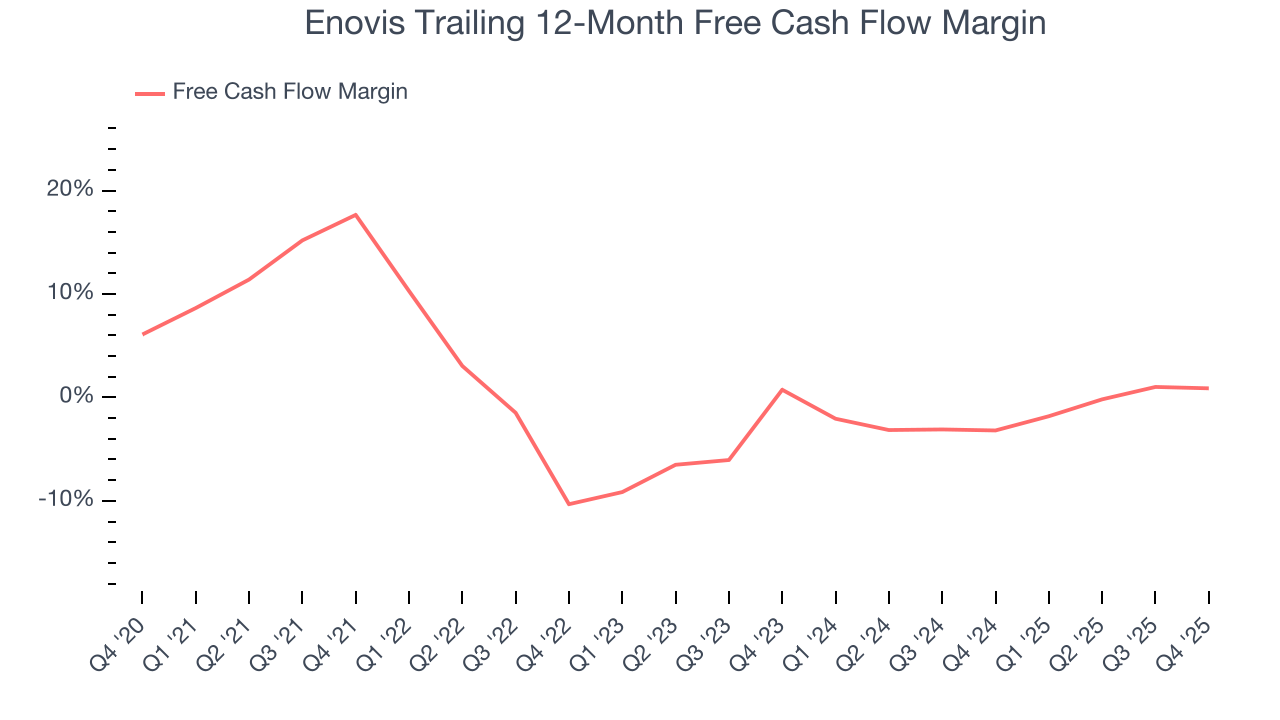

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Enovis broke even from a free cash flow perspective over the last five years, giving the company limited opportunities to return capital to shareholders.

Taking a step back, we can see that Enovis’s margin dropped by 16.8 percentage points during that time. It may have ticked higher more recently, but shareholders are likely hoping for its margin to at least revert to its historical level. Almost any movement in the wrong direction is undesirable because of its already low cash conversion. If the longer-term trend returns, it could signal it’s in the middle of a big investment cycle.

Enovis’s free cash flow clocked in at $32.29 million in Q4, equivalent to a 5.6% margin. This cash profitability was in line with the comparable period last year and above its five-year average.

10. Return on Invested Capital (ROIC)

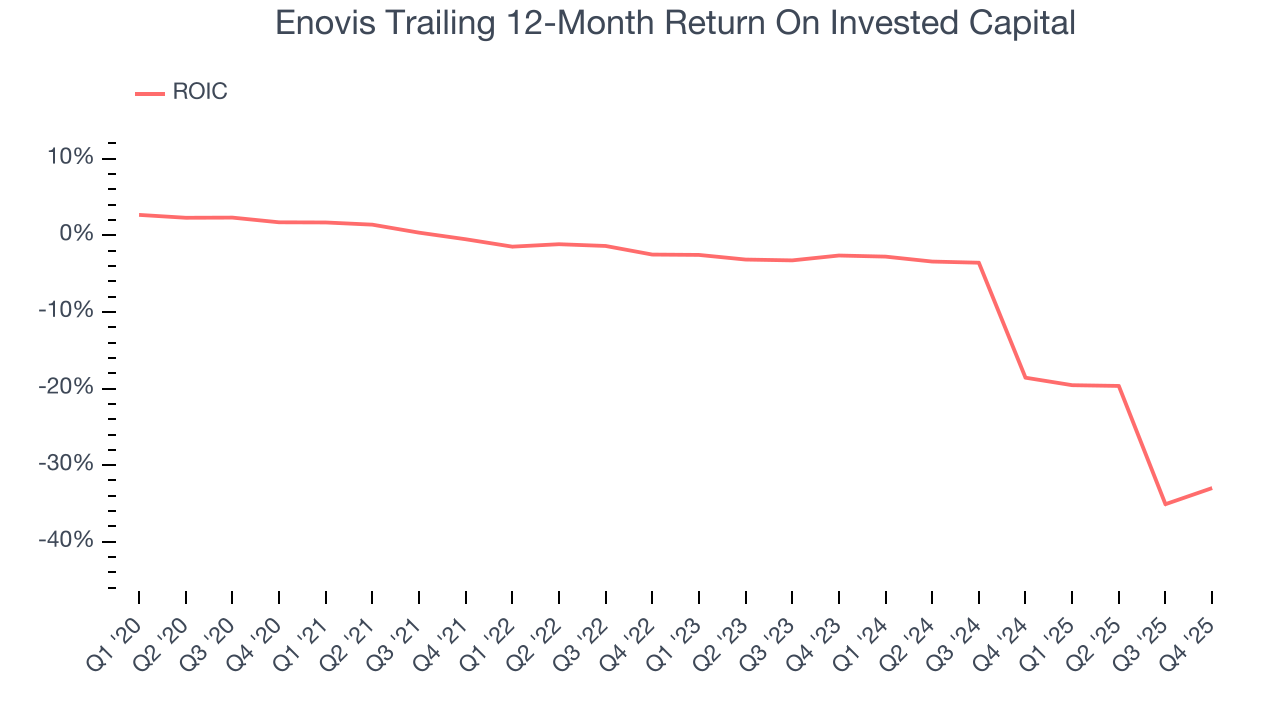

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Enovis’s five-year average ROIC was negative 11.4%, meaning management lost money while trying to expand the business. Its returns were among the worst in the healthcare sector.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Enovis’s ROIC has unfortunately decreased significantly. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

11. Balance Sheet Assessment

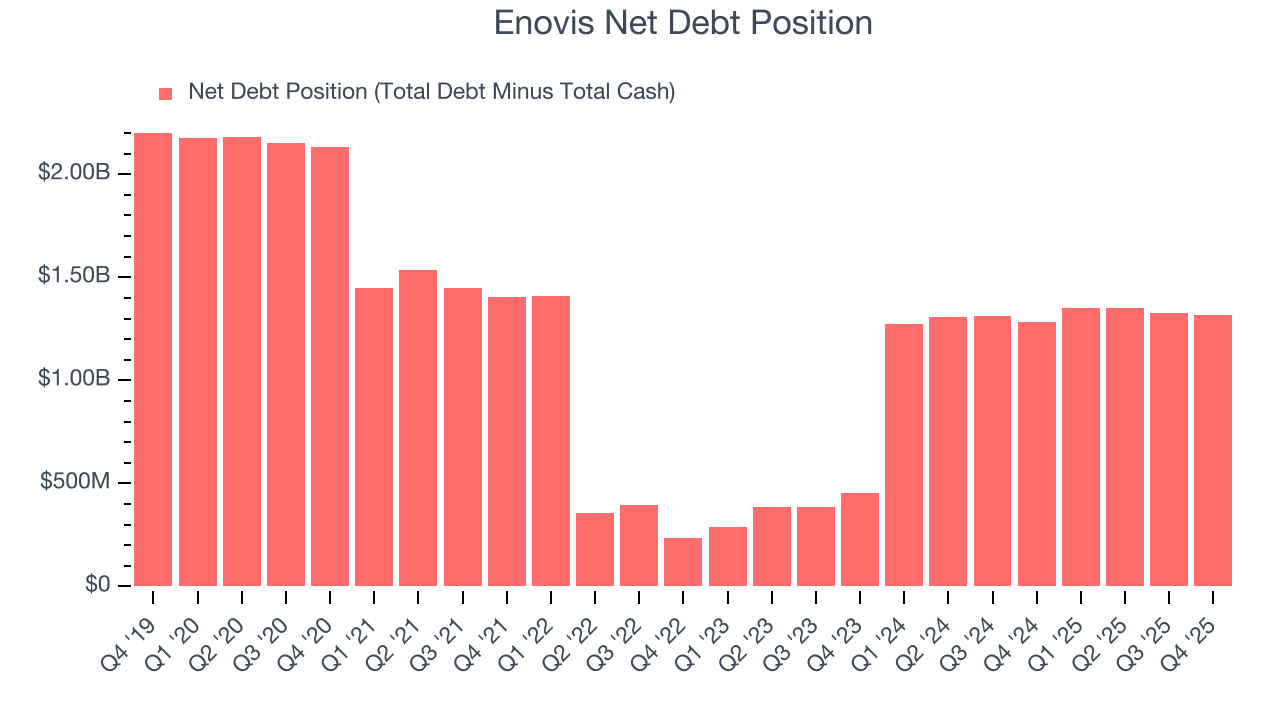

Enovis reported $36.39 million of cash and $1.35 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $403 million of EBITDA over the last 12 months, we view Enovis’s 3.3× net-debt-to-EBITDA ratio as safe. We also see its $19.8 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Enovis’s Q4 Results

We were impressed by how significantly Enovis blew past analysts’ full-year EPS guidance expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its revenue slightly missed and its full-year revenue guidance fell slightly short of Wall Street’s estimates. Zooming out, we think this was a mixed quarter. The stock remained flat at $22.34 immediately following the results.

13. Is Now The Time To Buy Enovis?

Updated: March 30, 2026 at 12:02 AM EDT

Before making an investment decision, investors should account for Enovis’s business fundamentals and valuation in addition to what happened in the latest quarter.

We cheer for all companies helping people live better, but in the case of Enovis, we’ll be cheering from the sidelines. To kick things off, its revenue has declined over the last five years. While its expanding adjusted operating margin shows the business has become more efficient, the downside is its diminishing returns show management's prior bets haven't worked out. On top of that, its relatively low ROIC suggests management has struggled to find compelling investment opportunities.

Enovis’s P/E ratio based on the next 12 months is 6.4x. While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are more exciting stocks to buy at the moment.

Wall Street analysts have a consensus one-year price target of $45.18 on the company (compared to the current share price of $21.92).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.