Hilton Grand Vacations (HGV)

Hilton Grand Vacations keeps us up at night. Its weak sales growth and low returns on capital show it struggled to generate demand and profits.― StockStory Analyst Team

1. News

2. Summary

Why We Think Hilton Grand Vacations Will Underperform

Spun off from Hilton Worldwide in 2017, Hilton Grand Vacations (NYSE:HGV) is a global timeshare company that provides travel experiences for its customers through its timeshare resorts and club membership programs.

- Sales trends were unexciting over the last two years as its 12.6% annual growth was below the typical consumer discretionary company

- Operating margin falls short of the industry average, and the smaller profit dollars make it harder to react to unexpected market developments

- High net-debt-to-EBITDA ratio of 10× could force the company to raise capital at unfavorable terms if market conditions deteriorate

Hilton Grand Vacations falls below our quality standards. You should search for better opportunities.

Why There Are Better Opportunities Than Hilton Grand Vacations

Hilton Grand Vacations’s stock price of $40.24 implies a valuation ratio of 9.6x forward P/E. This certainly seems like a cheap stock, but we think there are valid reasons why it trades this way.

It’s better to pay up for high-quality businesses with higher long-term earnings potential rather than to buy lower-quality stocks because they appear cheap. These challenged businesses often don’t re-rate, a phenomenon known as a “value trap”.

3. Hilton Grand Vacations (HGV) Research Report: Q4 CY2025 Update

Timeshare vacation company Hilton Grand Vacations (NYSE:HGV) missed Wall Street’s revenue expectations in Q4 CY2025 as sales rose 3.8% year on year to $1.33 billion. Its non-GAAP profit of $0.88 per share was 24% below analysts’ consensus estimates.

Hilton Grand Vacations (HGV) Q4 CY2025 Highlights:

- Revenue: $1.33 billion vs analyst estimates of $1.37 billion (3.8% year-on-year growth, 2.9% miss)

- Adjusted EPS: $0.88 vs analyst expectations of $1.16 (24% miss)

- Adjusted EBITDA: $292 million vs analyst estimates of $306.4 million (21.9% margin, 4.7% miss)

- Operating Margin: 9.5%, in line with the same quarter last year

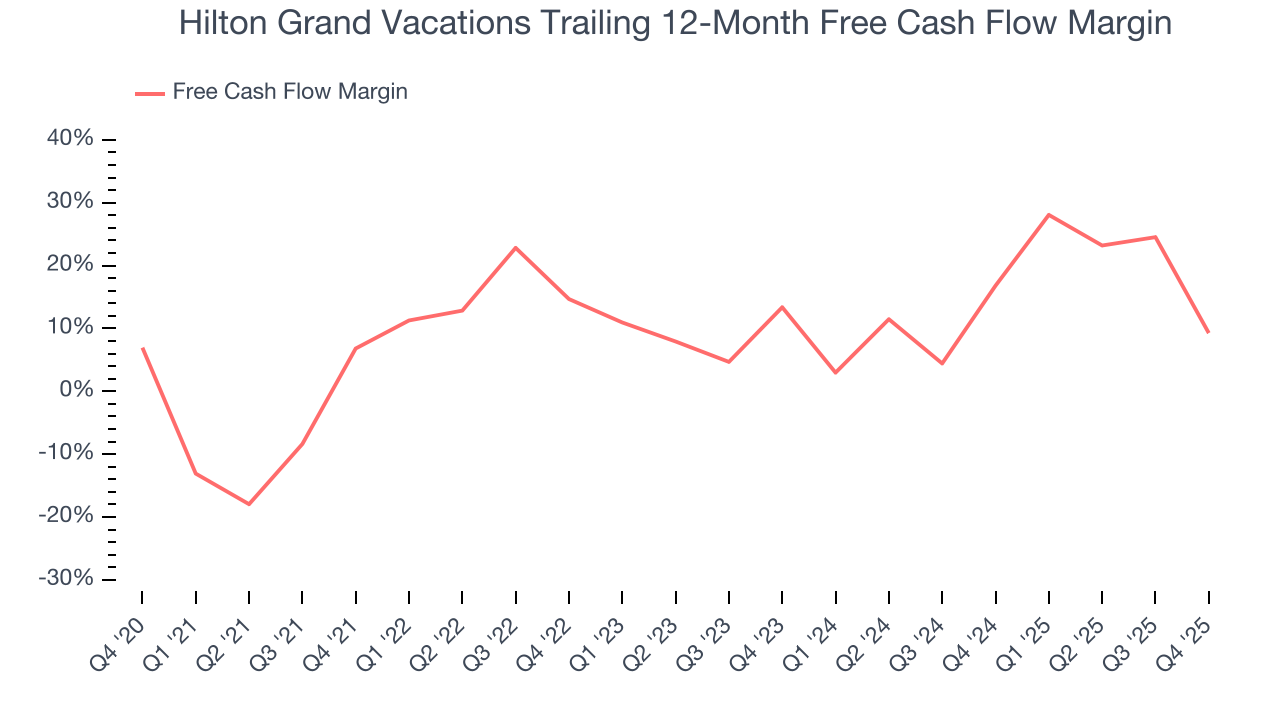

- Free Cash Flow Margin: 9.4%, down from 68.8% in the same quarter last year

- Members: 722,874, in line with the same quarter last year

- Market Capitalization: $4.16 billion

Company Overview

Spun off from Hilton Worldwide in 2017, Hilton Grand Vacations (NYSE:HGV) is a global timeshare company that provides travel experiences for its customers through its timeshare resorts and club membership programs.

Hilton Grand Vacations develops, markets, and operates high-quality vacation resorts in prime destinations worldwide. These resorts are located in highly sought-after vacation spots, including urban centers like New York City, beachfront areas in Hawaii and Florida, and scenic destinations like Colorado and Scotland. HGV’s portfolio holds more than 55 resort properties, offering a range of accommodations, from studios to multi-bedroom units.

The core of HGV's business is its timeshare model, where customers purchase a share of a property that entitles them to spend a set amount of time there annually. This model is bolstered by the Hilton Grand Vacations Club, a points-based membership system that allows member to use their points to book stays at various HGV resorts and thousands of hotels in the Hilton Worldwide network.

To maintain market relevance, the company invests in new facilities and services to enhance the vacation experience. This includes well-appointed accommodations, on-site dining and leisure activities, and customer service. HGV also incorporates digital technology to streamline the booking and customer service processes for greater convenience.

4. Consumer Discretionary - Travel and Vacation Providers

The Consumer Discretionary sector, by definition, is made up of companies selling non-essential goods and services. When economic conditions deteriorate or tastes shift, consumers can easily cut back or eliminate these purchases. For long-term investors with five-year holding periods, this creates a structural challenge: the sector is inherently hit-driven, with low switching costs and fickle customers. As a result, only a handful of companies can reliably grow demand and compound earnings over long periods, which is why our bar is high and High Quality ratings are rare.

Travel and vacation providers operate tour packages, cruise lines, online travel agencies, and vacation rental platforms, connecting consumers with leisure and business travel experiences. Tailwinds include robust post-pandemic travel demand, a consumer preference shift toward experiences over goods, and technology-enabled personalization improving conversion and loyalty. However, headwinds are significant: the industry is acutely sensitive to macroeconomic cycles, geopolitical instability, and fuel price volatility. Low switching costs mean fierce price competition, while capacity additions in segments like cruises can lead to oversupply. Regulatory burdens, weather disruptions, and public health risks further create episodic but potentially severe demand shocks.

Hilton Grand Vacations's primary competitors include Marriott Vacations Worldwide (NYSE:VAC), Wyndham Destinations (NYSE:WYND), Bluegreen Vacations (NYSE:BXG), Hyatt Residence Club (owned by Hyatt Hotels NYSE:H) and Diamond Resorts (owned by Apollo NYSE:APO).

5. Revenue Growth

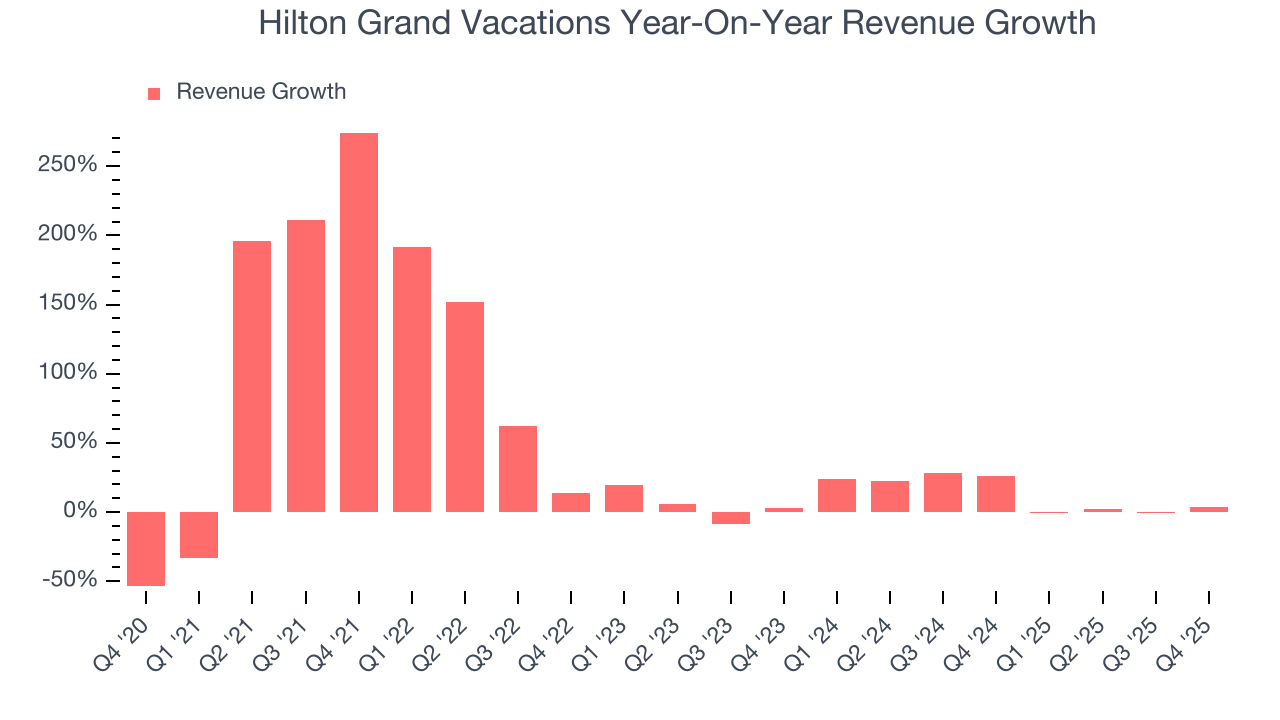

Examining a company’s long-term performance can provide clues about its quality. Any business can have short-term success, but a top-tier one grows for years. Over the last five years, Hilton Grand Vacations grew its sales at a 38.8% compounded annual growth rate. Though this growth is acceptable on an absolute basis, we need to see more than just topline growth for the consumer discretionary sector, which can display significant earnings volatility. This means our bar for the sector is particularly high, reflecting the non-essential and hit-driven nature of the products and services offered. Additionally, five-year CAGR starts around Covid, when revenue was depressed then rebounded.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new property or trend. Hilton Grand Vacations’s recent performance shows its demand has slowed as its annualized revenue growth of 12.6% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

Hilton Grand Vacations also discloses its number of members and conducted tours, which clocked in at 722,874 and 224,894 in the latest quarter. Over the last two years, Hilton Grand Vacations’s members averaged 7.6% year-on-year growth while its conducted tours averaged 2.6% year-on-year growth.

This quarter, Hilton Grand Vacations’s revenue grew by 3.8% year on year to $1.33 billion, falling short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 10.2% over the next 12 months, a slight deceleration versus the last two years. This projection is underwhelming and implies its products and services will face some demand challenges.

6. Operating Margin

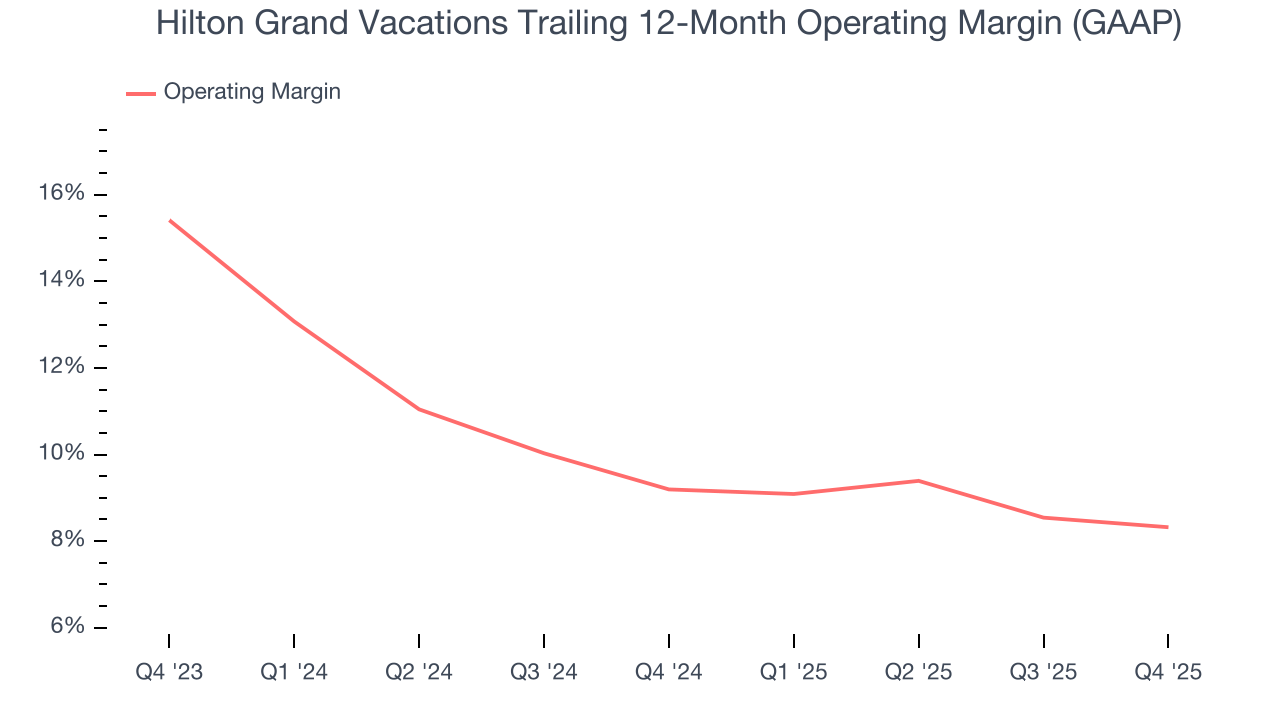

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Hilton Grand Vacations’s operating margin might fluctuated slightly over the last 12 months but has generally stayed the same, averaging 8.8% over the last two years. This profitability was inadequate for a consumer discretionary business and caused by its suboptimal cost structure.

This quarter, Hilton Grand Vacations generated an operating margin profit margin of 9.5%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

7. Earnings Per Share

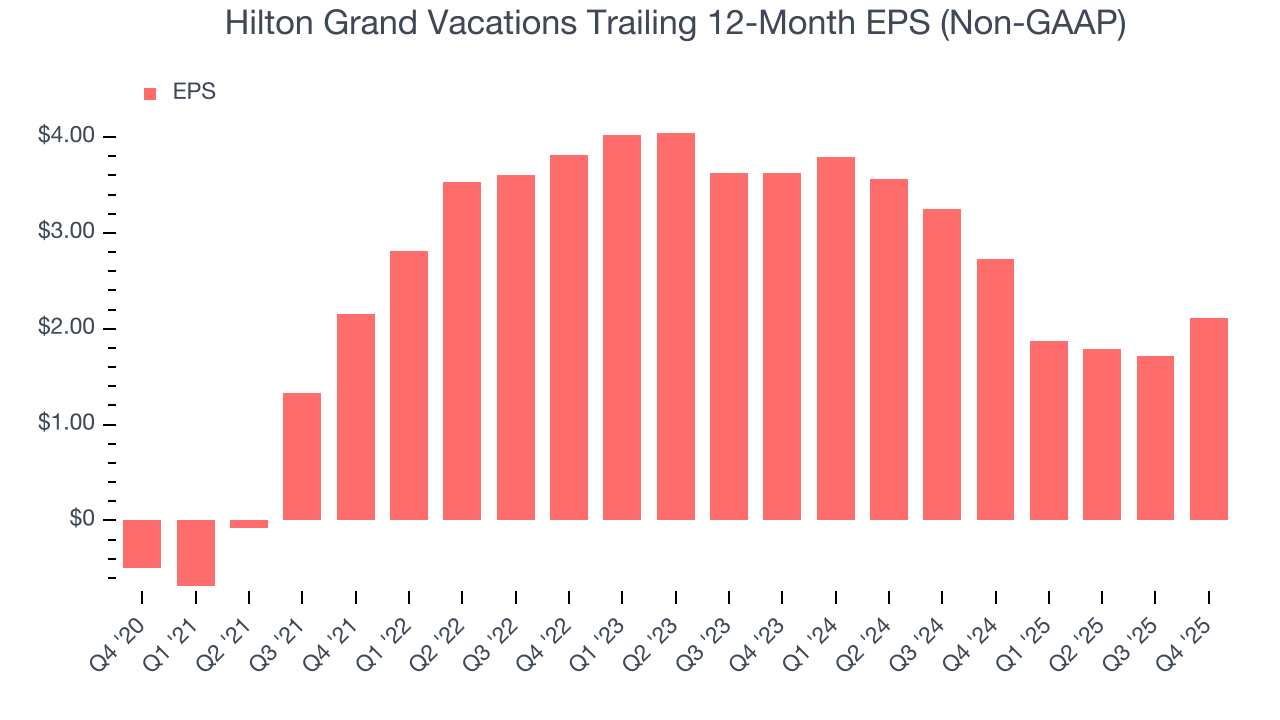

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Hilton Grand Vacations’s full-year EPS flipped from negative to positive over the last five years. This is encouraging and shows it’s at a critical moment in its life.

In Q4, Hilton Grand Vacations reported adjusted EPS of $0.88, up from $0.49 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates, but we care more about long-term adjusted EPS growth than short-term movements. Over the next 12 months, Wall Street expects Hilton Grand Vacations’s full-year EPS of $2.11 to grow 106%.

8. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Hilton Grand Vacations has shown poor cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 13%, lousy for a consumer discretionary business.

Hilton Grand Vacations’s free cash flow clocked in at $125 million in Q4, equivalent to a 9.4% margin. The company’s cash profitability regressed as it was 59.4 percentage points lower than in the same quarter last year, prompting us to pay closer attention. Short-term fluctuations typically aren’t a big deal because investment needs can be seasonal, but we’ll be watching to see if the trend extrapolates into future quarters.

Over the next year, analysts’ consensus estimates show they’re expecting Hilton Grand Vacations’s free cash flow margin of 9.3% for the last 12 months to remain the same.

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Hilton Grand Vacations historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 5.7%, somewhat low compared to the best consumer discretionary companies that consistently pump out 25%+.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, Hilton Grand Vacations’s ROIC has decreased over the last few years. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

10. Balance Sheet Risk

Debt is a tool that can boost company returns but presents risks if used irresponsibly. As long-term investors, we aim to avoid companies taking excessive advantage of this instrument because it could lead to insolvency.

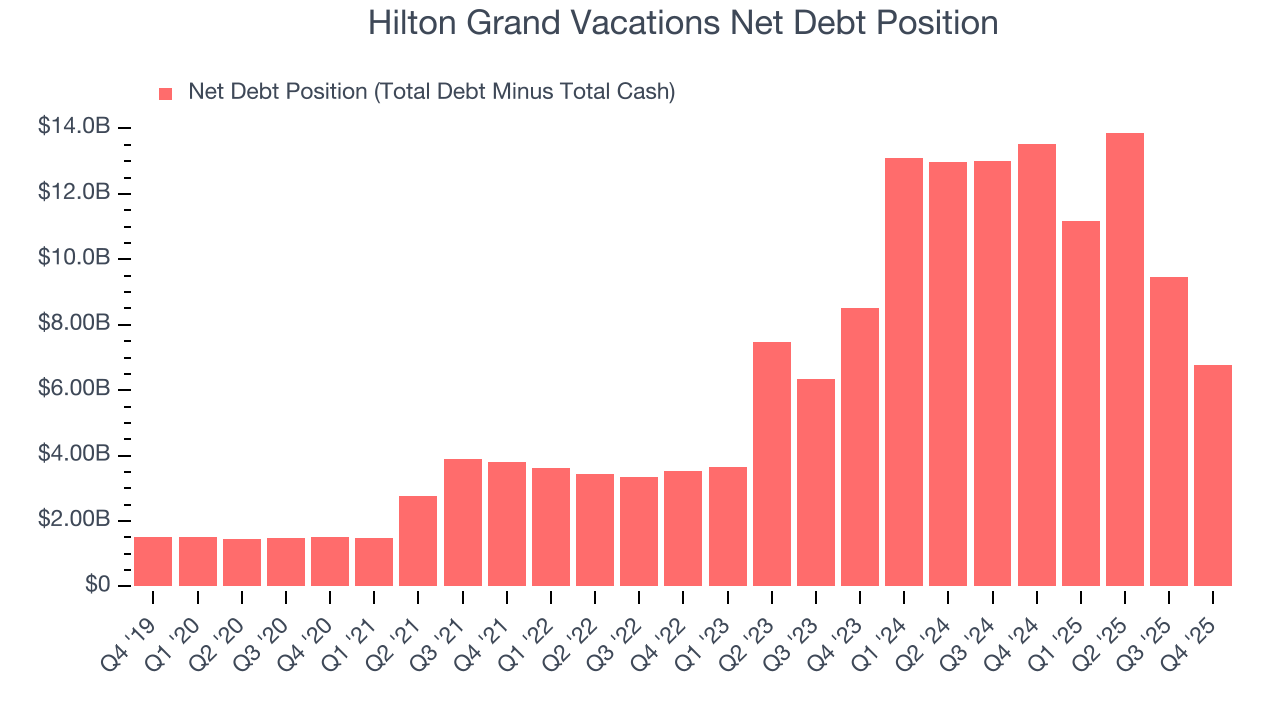

Hilton Grand Vacations’s $7.35 billion of debt exceeds the $571 million of cash on its balance sheet. Furthermore, its 7× net-debt-to-EBITDA ratio (based on its EBITDA of $950 million over the last 12 months) shows the company is overleveraged.

At this level of debt, incremental borrowing becomes increasingly expensive and credit agencies could downgrade the company’s rating if profitability falls. Hilton Grand Vacations could also be backed into a corner if the market turns unexpectedly – a situation we seek to avoid as investors in high-quality companies.

We hope Hilton Grand Vacations can improve its balance sheet and remain cautious until it increases its profitability or pays down its debt.

11. Key Takeaways from Hilton Grand Vacations’s Q4 Results

We struggled to find many positives in these results. Its EPS missed and its revenue fell short of Wall Street’s estimates. Overall, this was a softer quarter. Still, the stock traded up 1.6% to $49.40 immediately after reporting.

12. Is Now The Time To Buy Hilton Grand Vacations?

Updated: March 22, 2026 at 10:49 PM EDT

We think that the latest earnings result is only one piece of the bigger puzzle. If you’re deciding whether to own Hilton Grand Vacations, you should also grasp the company’s longer-term business quality and valuation.

Hilton Grand Vacations falls short of our quality standards. While its projected EPS for the next year implies the company’s fundamentals will improve, the downside is its number of members has disappointed. On top of that, its Forecasted free cash flow margin suggests the company will ramp up its investments next year.

Hilton Grand Vacations’s P/E ratio based on the next 12 months is 9.6x. While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are superior stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $54.70 on the company (compared to the current share price of $40.24).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.