Sealed Air (SEE)

Sealed Air is in for a bumpy ride. Its weak sales growth and declining returns on capital show its demand and profits are shrinking.― StockStory Analyst Team

1. News

2. Summary

Why We Think Sealed Air Will Underperform

Founded in 1960, Sealed Air Corporation (NYSE: SEE) specializes in the development and production of protective and food packaging solutions, serving a variety of industries.

- Annual sales declines of 1.2% for the past two years show its products and services struggled to connect with the market during this cycle

- Earnings per share were flat over the last five years and fell short of the peer group average

- Projected sales growth of 1.2% for the next 12 months suggests sluggish demand

Sealed Air lacks the business quality we seek. There are superior stocks for sale in the market.

Why There Are Better Opportunities Than Sealed Air

Sealed Air is trading at $41.84 per share, or 12.2x forward P/E. Sealed Air’s multiple may seem like a great deal among industrials peers, but we think there are valid reasons why it’s this cheap.

Cheap stocks can look like a great deal at first glance, but they can be value traps. They often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. Sealed Air (SEE) Research Report: Q4 CY2025 Update

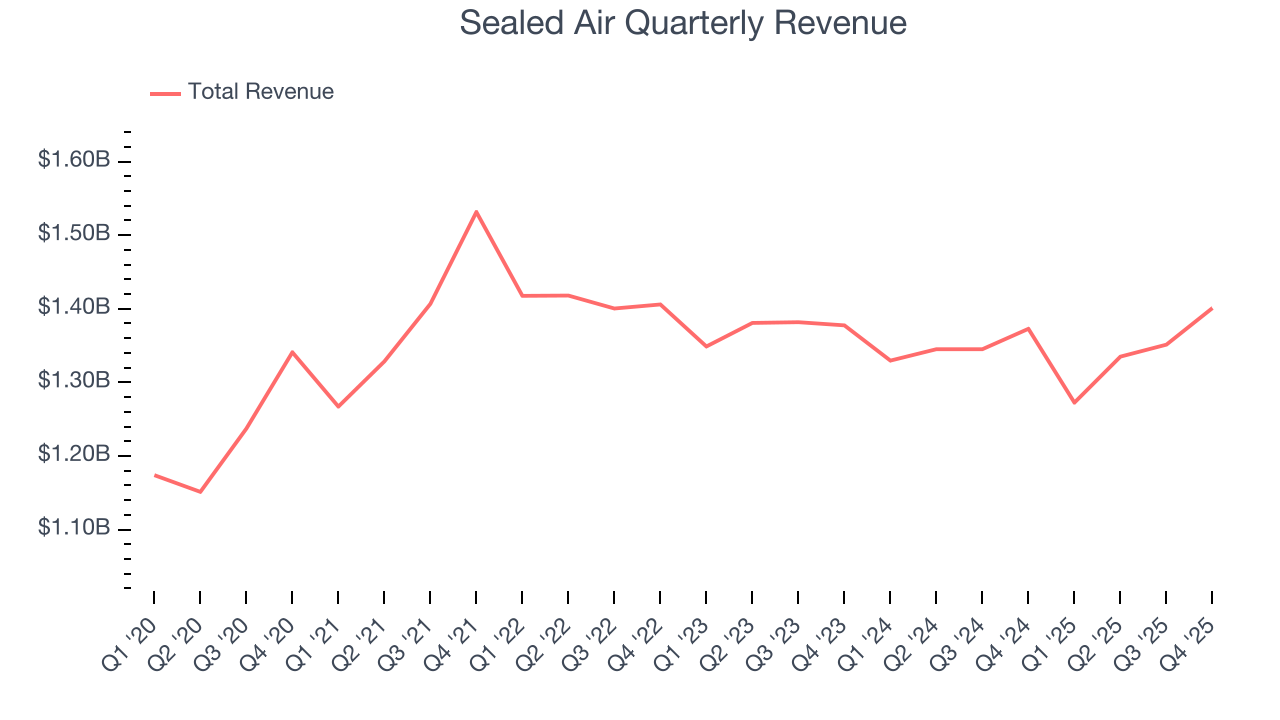

Integrated packaging solutions provider Sealed Air Corporation (NYSE:SEE) reported revenue ahead of Wall Street’s expectations in Q4 CY2025, with sales up 2.1% year on year to $1.4 billion. Its non-GAAP profit of $0.77 per share was 5.4% above analysts’ consensus estimates.

Sealed Air (SEE) Q4 CY2025 Highlights:

- Revenue: $1.4 billion vs analyst estimates of $1.35 billion (2.1% year-on-year growth, 3.8% beat)

- Adjusted EPS: $0.77 vs analyst estimates of $0.73 (5.4% beat)

- Adjusted EBITDA: $278 million vs analyst estimates of $272.2 million (19.8% margin, 2.1% beat)

- Operating Margin: 11.4%, in line with the same quarter last year

- Free Cash Flow Margin: 18.4%, up from 13.5% in the same quarter last year

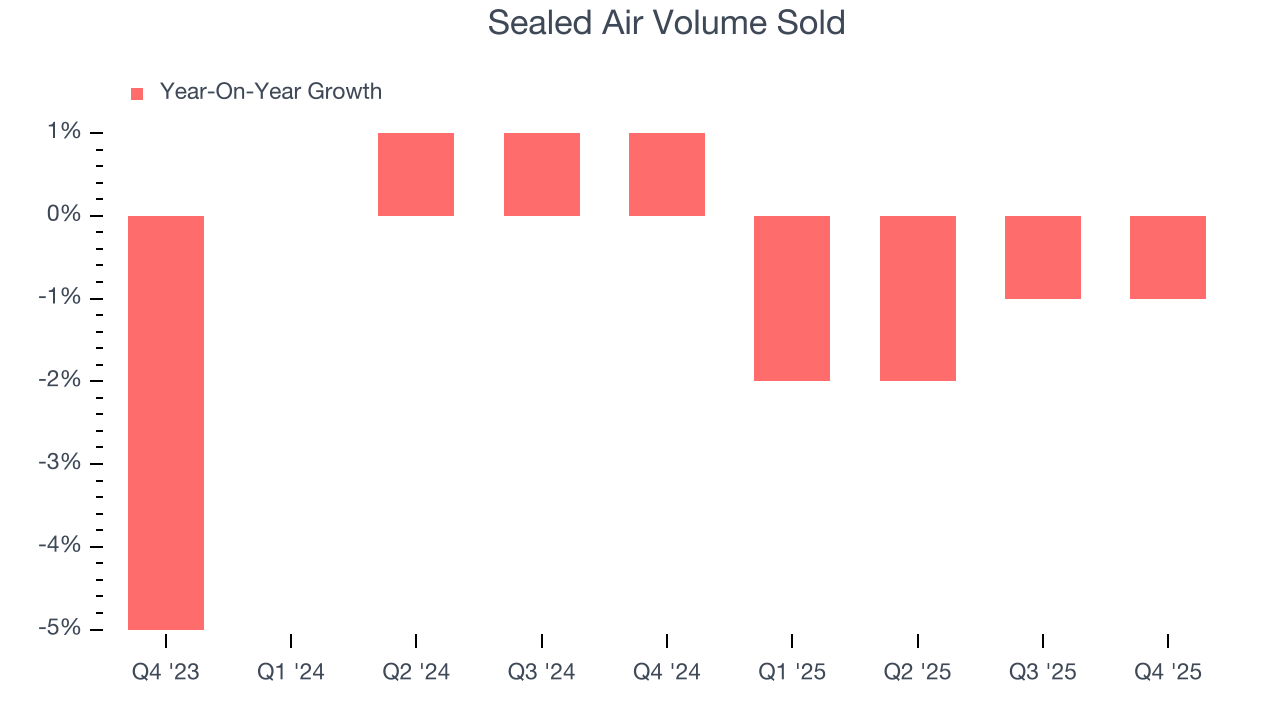

- Sales Volumes fell 1% year on year (1% in the same quarter last year)

- Market Capitalization: $6.17 billion

Company Overview

Founded in 1960, Sealed Air Corporation (NYSE: SEE) specializes in the development and production of protective and food packaging solutions, serving a variety of industries.

Founded in 1960 and headquartered in Charlotte, North Carolina, the company has established itself in the packaging industry, serving end markets including fresh proteins, foods, fluids and liquids, medical and life sciences, e-commerce retail, logistics and omnichannel fulfillment operations, and industrials. SEE operates through two primary reportable segments: Food and Protective.

The Food segment focuses on providing packaging solutions for fresh proteins, foods, fluids, and liquids. This segment expanded its offerings in early 2023 with the acquisition of Liquibox, enhancing its capabilities in liquid packaging and dispensing solutions for food, beverage, consumer goods, and industrial end markets. The Protective segment caters to e-commerce retail, logistics, and industrial markets, offering solutions designed to prevent product damage, increase order fulfillment velocity, and generate savings through waste reduction.

The company's portfolio includes several well-known brands such as CRYOVAC for food packaging, LIQUIBOX for liquids systems, SEALED AIR for protective packaging, AUTOBAG for automated packaging systems, and the BUBBLE WRAP brand. Additionally, the company has a presence in 45+ countries and territories, operating through numerous subsidiaries worldwide.

4. Industrial Packaging

Industrial packaging companies have built competitive advantages from economies of scale that lead to advantaged purchasing and capital investments that are difficult and expensive to replicate. Recently, eco-friendly packaging and conservation are driving customers preferences and innovation. For example, plastic is not as desirable a material as it once was. Despite being integral to consumer goods ranging from beer to toothpaste to laundry detergent, these companies are still at the whim of the macro, especially consumer health and consumer willingness to spend.

Competitors in the packaging industry include Crown Holdings (NYSE:CCK), Ardagh Group (NYSE:ARD), and Silgan Holdings (NASDAQ:SLGN)

5. Revenue Growth

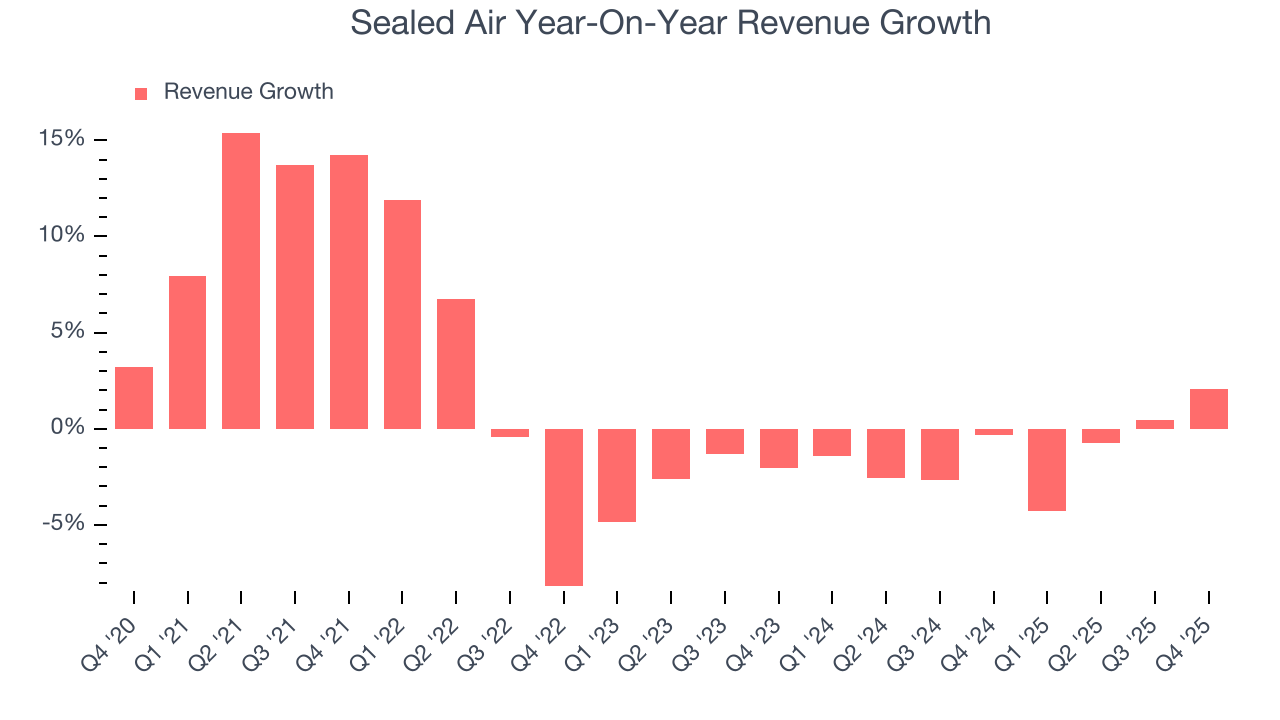

A company’s long-term performance is an indicator of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Over the last five years, Sealed Air grew its sales at a sluggish 1.8% compounded annual growth rate. This fell short of our benchmarks and is a tough starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Sealed Air’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 1.2% annually.

Sealed Air also reports its number of units sold. Over the last two years, Sealed Air’s units sold were flat. Because this number is in line with its revenue growth, we can see the company kept its prices fairly consistent.

This quarter, Sealed Air reported modest year-on-year revenue growth of 2.1% but beat Wall Street’s estimates by 3.8%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months. Although this projection implies its newer products and services will catalyze better top-line performance, it is still below the sector average.

6. Gross Margin & Pricing Power

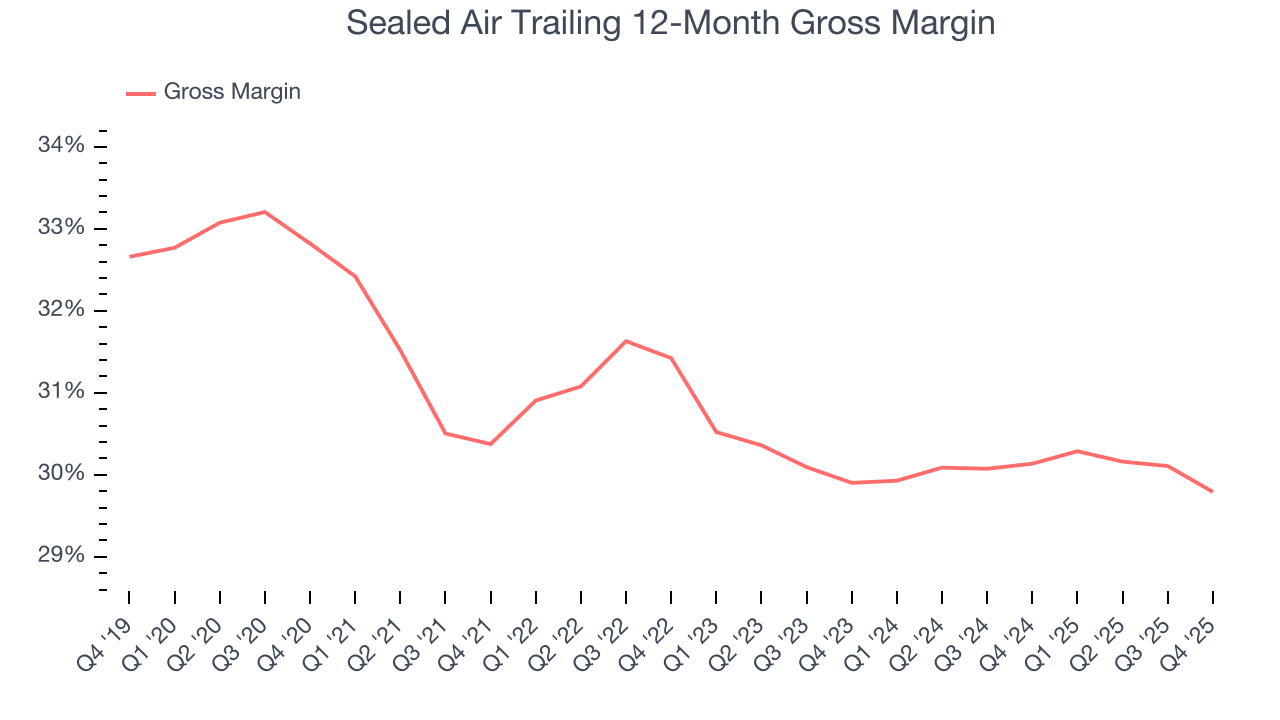

Sealed Air’s unit economics are better than the typical industrials business, signaling its products are somewhat differentiated through quality or brand.As you can see below, it averaged a decent 30.3% gross margin over the last five years. Said differently, Sealed Air paid its suppliers $69.66 for every $100 in revenue.

In Q4, Sealed Air produced a 28.4% gross profit margin , marking a 1.2 percentage point decrease from 29.6% in the same quarter last year. Zooming out, the company’s full-year margin has remained steady over the past 12 months, suggesting its input costs (such as raw materials and manufacturing expenses) have been stable and it isn’t under pressure to lower prices.

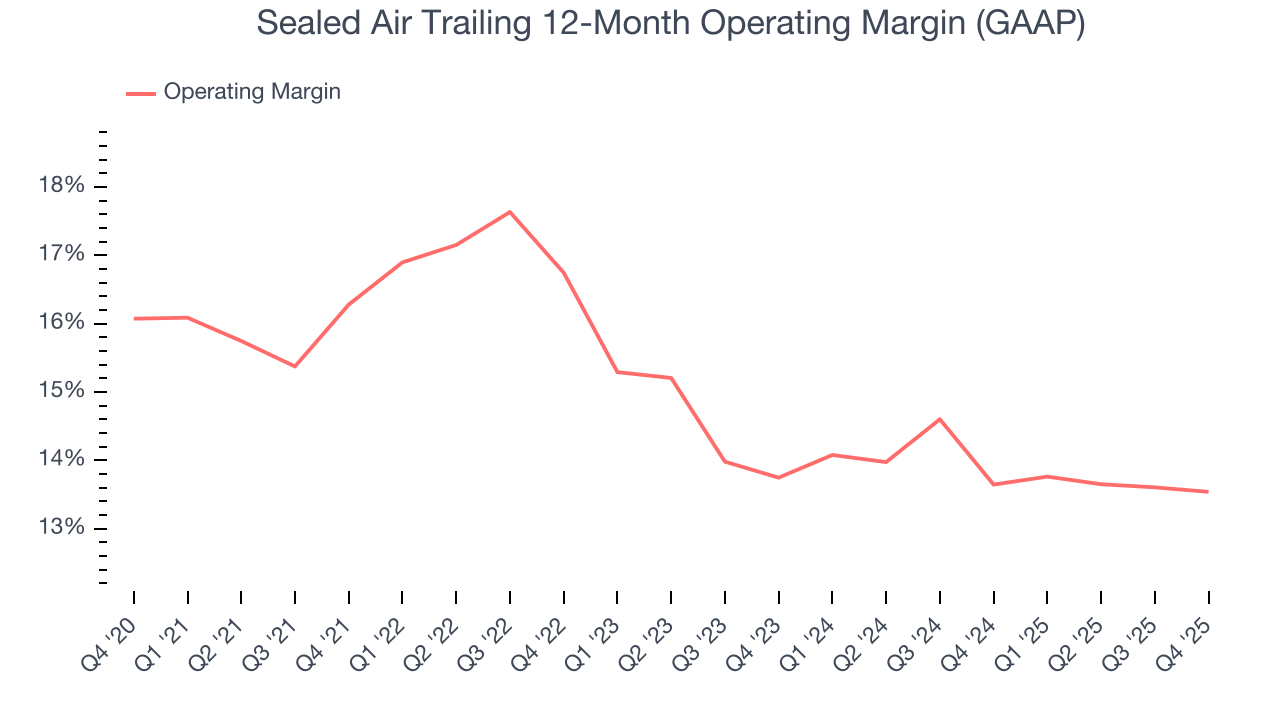

7. Operating Margin

Sealed Air has been an efficient company over the last five years. It was one of the more profitable businesses in the industrials sector, boasting an average operating margin of 14.8%.

Analyzing the trend in its profitability, Sealed Air’s operating margin decreased by 2.7 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, Sealed Air generated an operating margin profit margin of 11.4%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

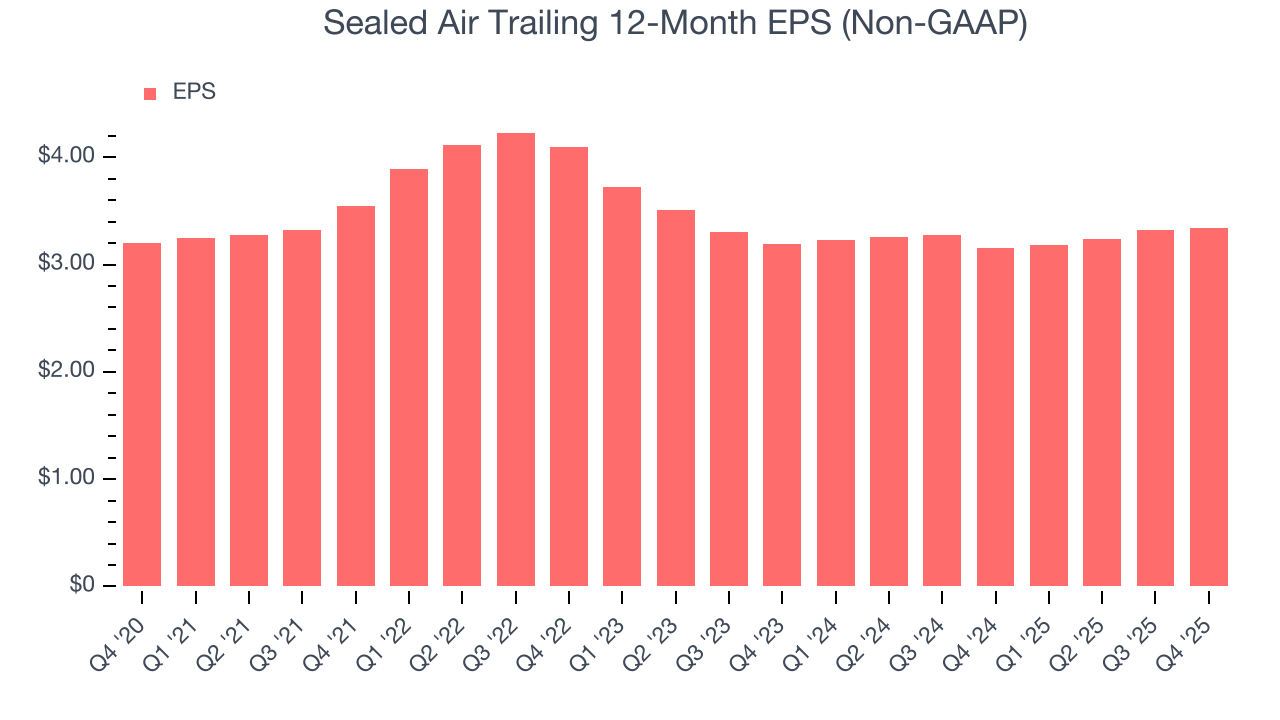

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sealed Air’s flat EPS over the last five years was below its 1.8% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded due to non-fundamental factors such as interest expenses and taxes.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Sealed Air, its two-year annual EPS growth of 2.3% was higher than its five-year trend. Accelerating earnings growth is almost always an encouraging data point.

In Q4, Sealed Air reported adjusted EPS of $0.77, up from $0.75 in the same quarter last year. This print beat analysts’ estimates by 5.4%. Over the next 12 months, Wall Street expects Sealed Air’s full-year EPS of $3.34 to grow 1.1%.

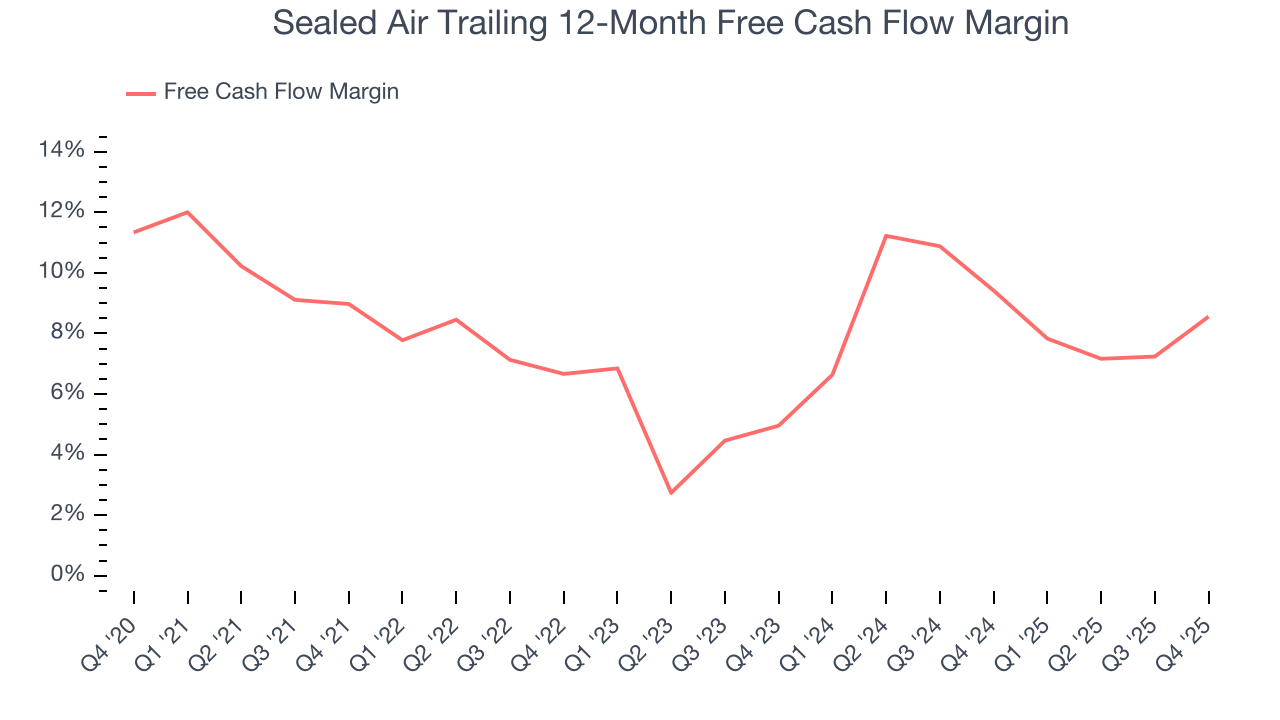

9. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Sealed Air has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 7.7% over the last five years, slightly better than the broader industrials sector.

Sealed Air’s free cash flow clocked in at $257.7 million in Q4, equivalent to a 18.4% margin. This result was good as its margin was 4.9 percentage points higher than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, leading to temporary swings. Long-term trends trump fluctuations.

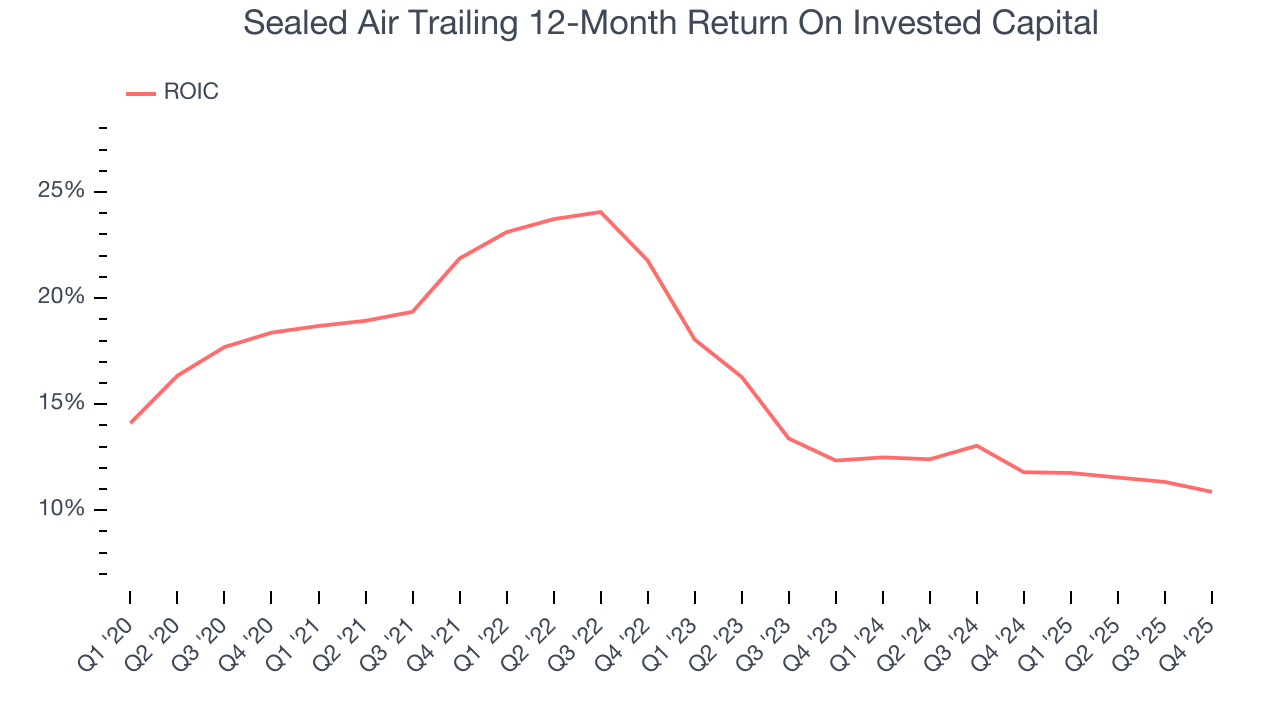

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Although Sealed Air hasn’t been the highest-quality company lately because of its poor revenue and EPS performance, it historically found a few growth initiatives that worked out well. Its five-year average ROIC was 15.7%, impressive for an industrials business.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, Sealed Air’s ROIC has decreased significantly over the last few years. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

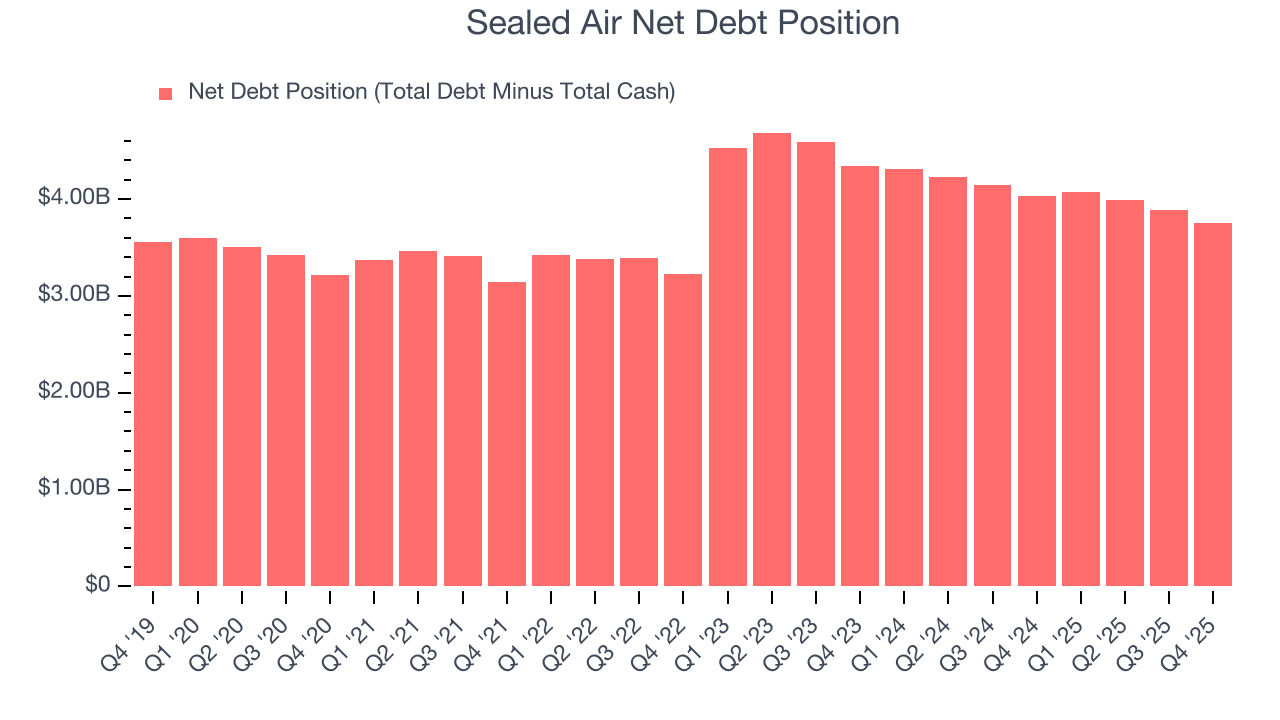

11. Balance Sheet Assessment

Sealed Air reported $344 million of cash and $4.1 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $1.13 billion of EBITDA over the last 12 months, we view Sealed Air’s 3.3× net-debt-to-EBITDA ratio as safe. We also see its $218.9 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Sealed Air’s Q4 Results

We were impressed by how significantly Sealed Air blew past analysts’ revenue expectations this quarter. We were also happy its EBITDA outperformed Wall Street’s estimates. Zooming out, we think this was a good print with some key areas of upside. The stock remained flat at $42.00 immediately following the results.

13. Is Now The Time To Buy Sealed Air?

Updated: March 14, 2026 at 11:28 PM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Sealed Air.

Sealed Air falls short of our quality standards. To kick things off, its revenue growth was weak over the last five years, and analysts don’t see anything changing over the next 12 months. While its strong operating margins show it’s a well-run business, the downside is its diminishing returns show management's prior bets haven't worked out. On top of that, its flat unit sales disappointed.

Sealed Air’s P/E ratio based on the next 12 months is 12.2x. This valuation is reasonable, but the company’s shaky fundamentals present too much downside risk. There are superior stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $45.36 on the company (compared to the current share price of $41.84).