The Toro Company (TTC)

We’re skeptical of The Toro Company. Its poor sales growth and falling returns on capital suggest its growth opportunities are shrinking.― StockStory Analyst Team

1. News

2. Summary

Why We Think The Toro Company Will Underperform

Ceasing all production to support the war effort during World War II, Toro (NYSE:TTC) offers outdoor equipment for residential, commercial, and agricultural use.

- Demand will likely be soft over the next 12 months as Wall Street’s estimates imply tepid growth of 4.8%

- Sales trends were unexciting over the last five years as its 5.5% annual growth was below the typical industrials company

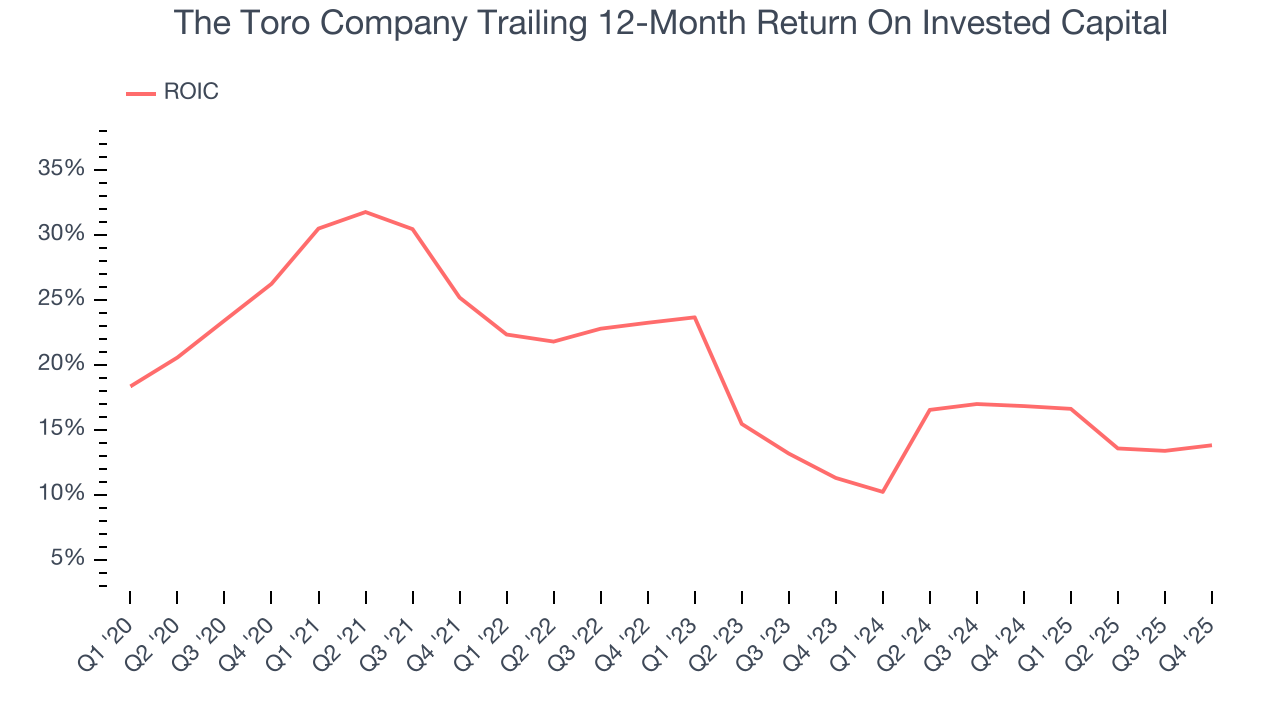

- A consolation is that its industry-leading 18.1% return on capital demonstrates management’s skill in finding high-return investments

The Toro Company doesn’t measure up to our expectations. You should search for better opportunities.

Why There Are Better Opportunities Than The Toro Company

At $95.50 per share, The Toro Company trades at 20.2x forward P/E. The Toro Company’s valuation may seem like a bargain, especially when stacked up against other industrials companies. We remind you that you often get what you pay for, though.

Cheap stocks can look like great bargains at first glance, but you often get what you pay for. These mediocre businesses often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. The Toro Company (TTC) Research Report: Q4 CY2025 Update

Outdoor equipment company Toro (NYSE:TTC) reported Q4 CY2025 results exceeding the market’s revenue expectations, with sales up 4.2% year on year to $1.04 billion. Its non-GAAP profit of $0.74 per share was 14.2% above analysts’ consensus estimates.

The Toro Company (TTC) Q4 CY2025 Highlights:

- Revenue: $1.04 billion vs analyst estimates of $1 billion (4.2% year-on-year growth, 3.5% beat)

- Adjusted EPS: $0.74 vs analyst estimates of $0.65 (14.2% beat)

- Management raised its full-year Adjusted EPS guidance to $4.50 at the midpoint, a 1.7% increase

- Operating Margin: 8.4%, in line with the same quarter last year

- Free Cash Flow was $14.6 million, up from -$67.7 million in the same quarter last year

- Market Capitalization: $9.82 billion

Company Overview

Ceasing all production to support the war effort during World War II, Toro (NYSE:TTC) offers outdoor equipment for residential, commercial, and agricultural use.

Toro has a rich history dating back to its founding in 1914. The company initially gained traction in the agricultural sector by manufacturing engines for the Bull Tractor Company before pivoting to produce motorized golf course mowers years later. This set the stage for its expansion into a wide array of outdoor products.

Toro has acquired various companies throughout the years which fueled its growth, primarily focusing on supplementing its core competencies in outdoor equipment. Specifically, its 2014 acquisition of snow removal equipment company Boss Products and 2019 acquisition of underground construction machinery company, The Charles Machine Works, added new products to its portfolio.

Today, Toro's product portfolio includes lawn mowers, irrigation systems, snow blowers, landscaping equipment, and other outdoor equipment. Its equipment is designed for residential and commercial use intended to maintain outdoor spaces. Within the commercial space, it primarily sells to companies in golf course management, landscaping, and agriculture.

Toro engages in both direct sales to end-users and through contract sales, particularly with municipalities, golf courses, and commercial landscapers who require ongoing equipment maintenance and support. These contracts typically span three to five years and often include provisions for regular servicing, parts replacement, and equipment upgrades.

Going forward, the company has a vision to grow the number of robotics equipment that it offers by investing in research and development or making acquisitions. For example, it launched its robotic lawn mower in 2023 and acquired Left Hand Robotics in 2021.

4. Agricultural Machinery

Agricultural machinery companies are investing to develop and produce more precise machinery, automated systems, and connected equipment that collects analyzable data to help farmers and other customers improve yields and increase efficiency. On the other hand, agriculture is seasonal and natural disasters or bad weather can impact the entire industry. Additionally, macroeconomic factors such as commodity prices or changes in interest rates–which dictate the willingness of these companies or their customers to invest–can impact demand for agricultural machinery.

Competitors offering similar products include Deere (NYSE:DE), Alamo (NYSE:ALG), and Lindsay (NYS:LNN).

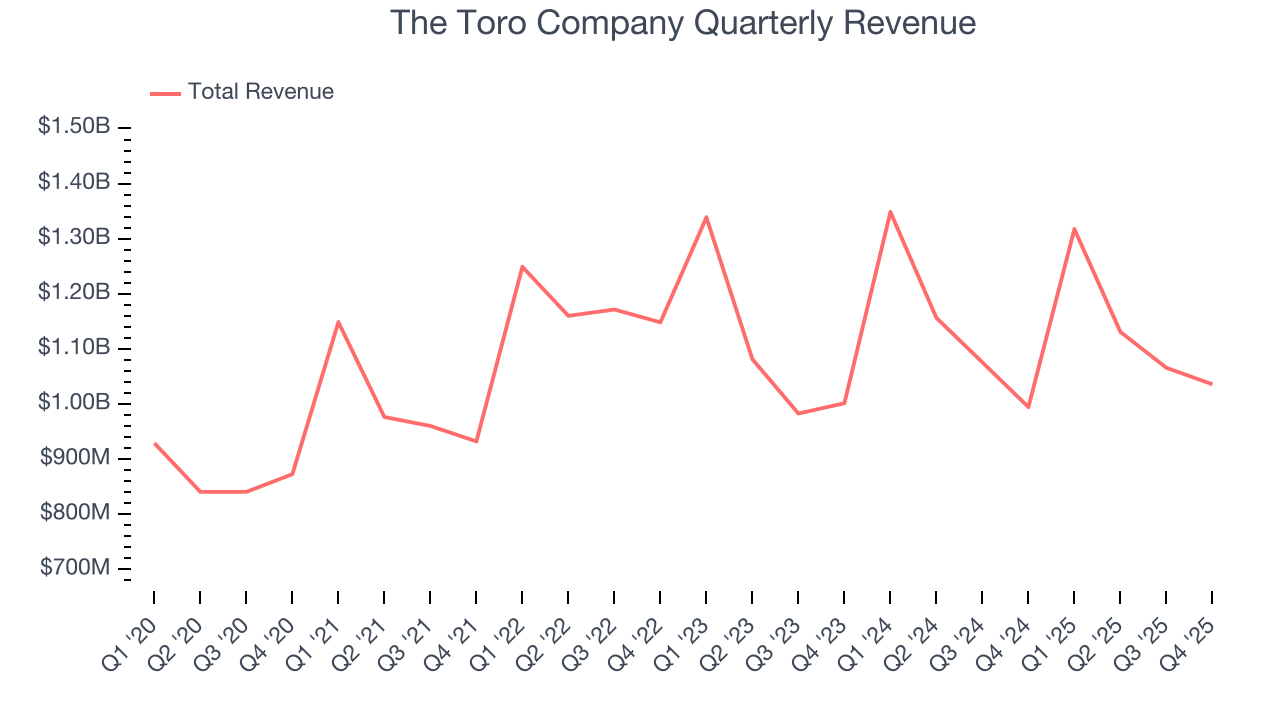

5. Revenue Growth

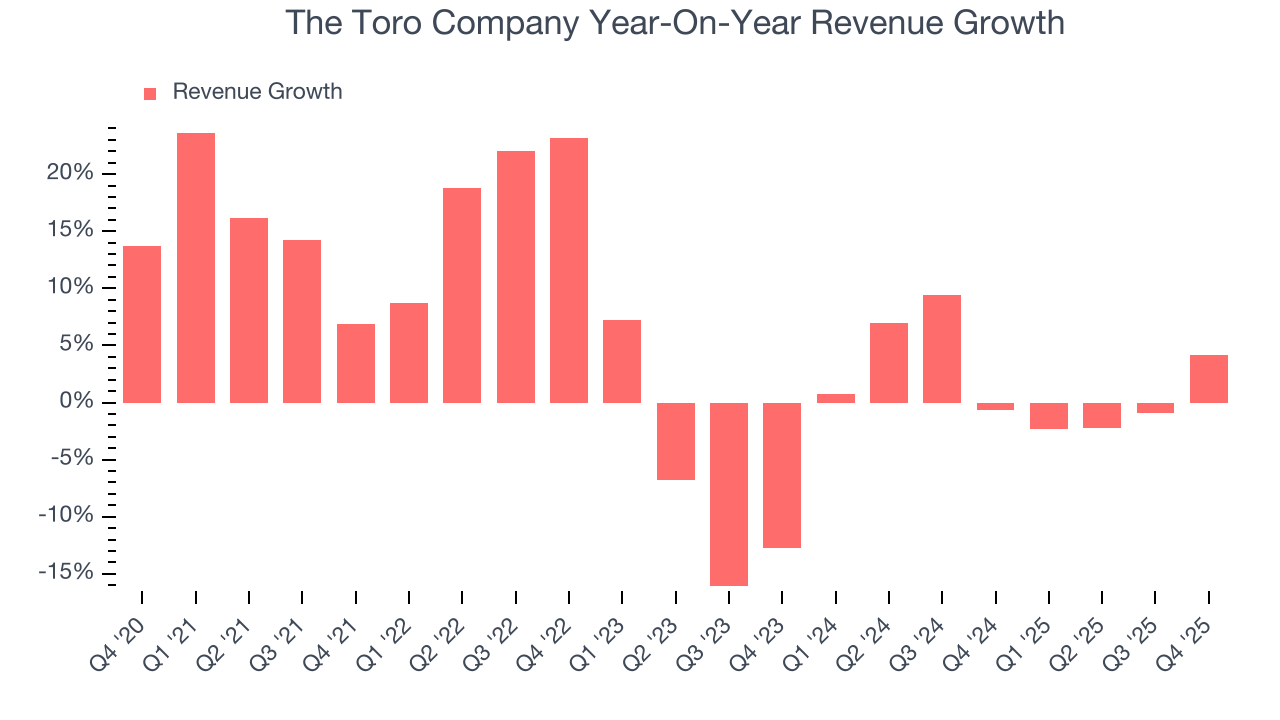

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, The Toro Company grew its sales at a tepid 5.5% compounded annual growth rate. This fell short of our benchmark for the industrials sector and is a tough starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. The Toro Company’s recent performance shows its demand has slowed as its annualized revenue growth of 1.6% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

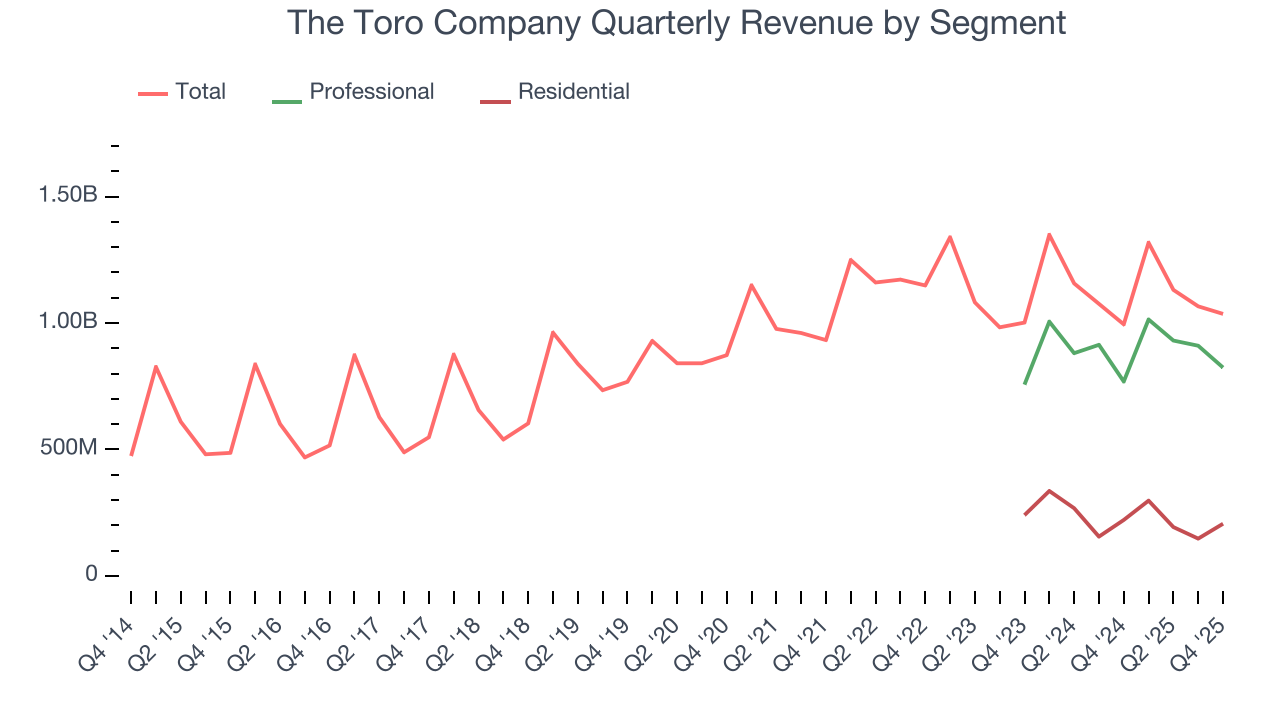

The Toro Company also breaks out the revenue for its most important segments, Professional and Residential , which are 79.5% and 19.9% of revenue. Over the last two years, The Toro Company’s Professional revenue (sales to contractors) averaged 3% year-on-year growth. On the other hand, its Residential revenue (sales to homeowners) averaged 11.8% declines.

This quarter, The Toro Company reported modest year-on-year revenue growth of 4.2% but beat Wall Street’s estimates by 3.5%.

Looking ahead, sell-side analysts expect revenue to grow 3.3% over the next 12 months. Although this projection implies its newer products and services will spur better top-line performance, it is still below the sector average.

6. Gross Margin & Pricing Power

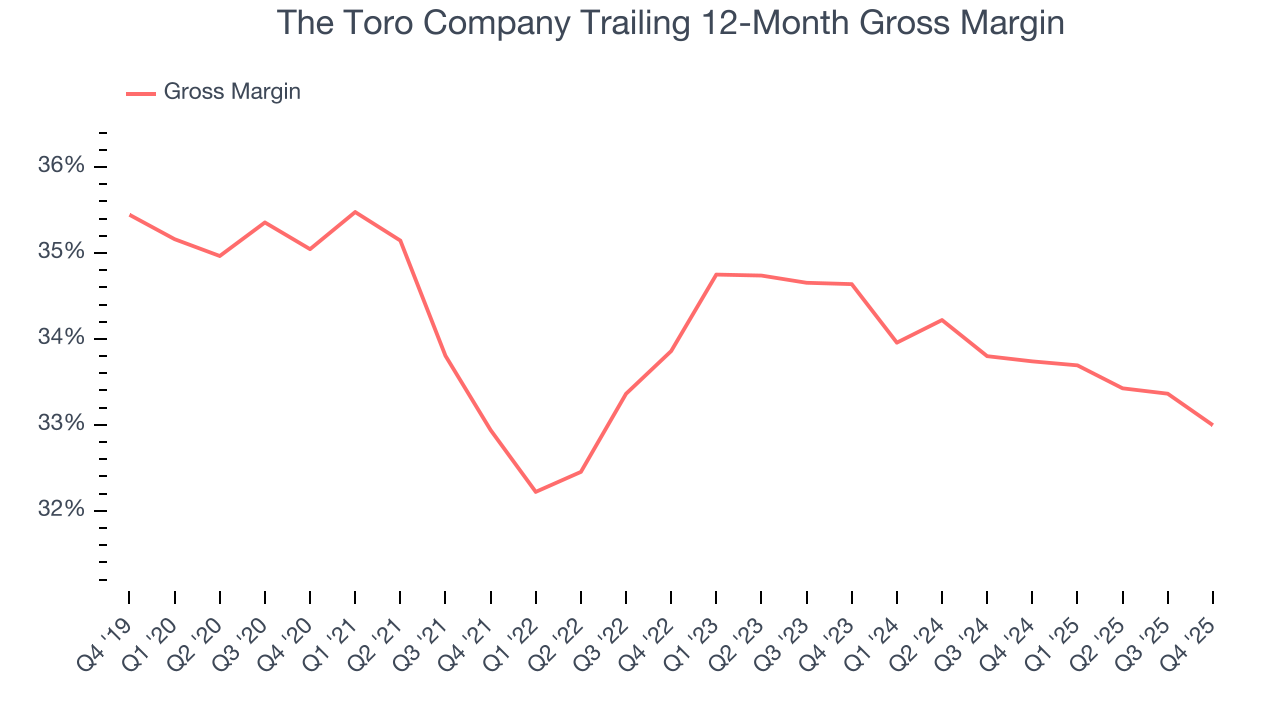

The Toro Company’s gross margin is good compared to other industrials businesses and signals it sells differentiated products, not commodities. As you can see below, it averaged an impressive 33.6% gross margin over the last five years. That means for every $100 in revenue, roughly $33.65 was left to spend on selling, marketing, R&D, and general administrative overhead.

This quarter, The Toro Company’s gross profit margin was 32.5%, down 1.6 percentage points year on year. Zooming out, the company’s full-year margin has remained steady over the past 12 months, suggesting its input costs (such as raw materials and manufacturing expenses) have been stable and it isn’t under pressure to lower prices.

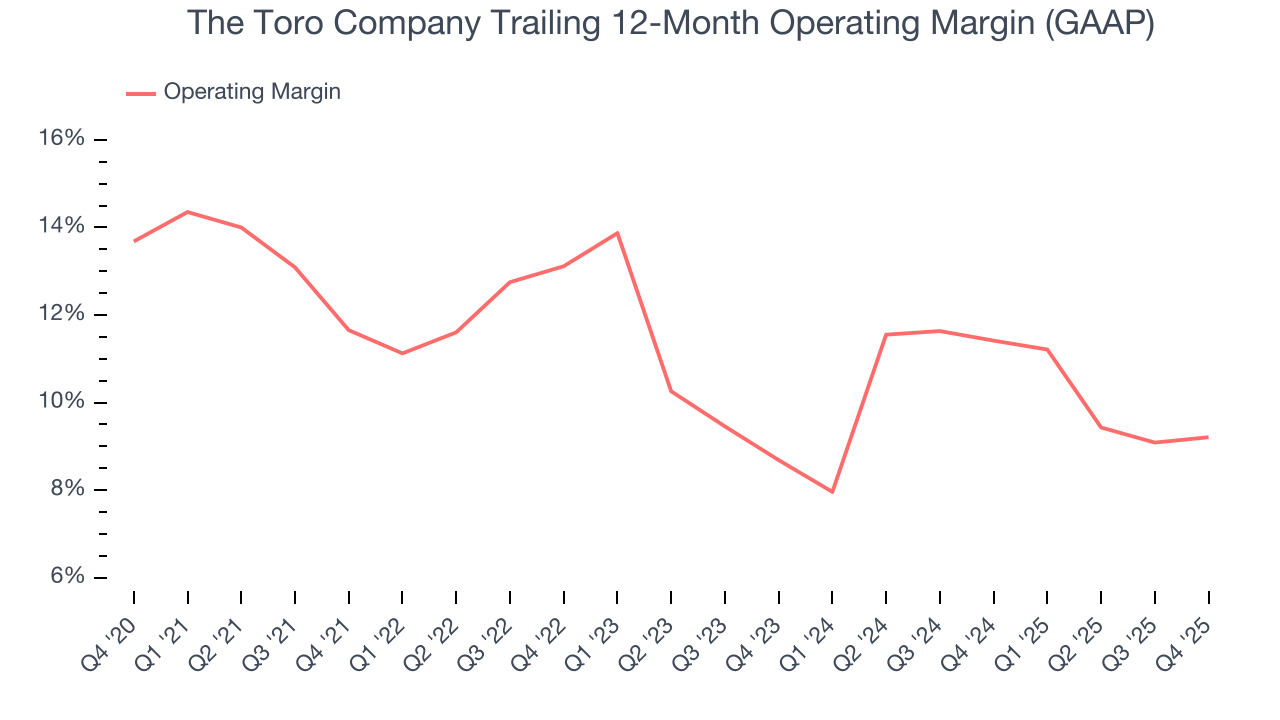

7. Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

The Toro Company has managed its cost base well over the last five years. It demonstrated solid profitability for an industrials business, producing an average operating margin of 10.8%. This result isn’t too surprising as its gross margin gives it a favorable starting point.

Looking at the trend in its profitability, The Toro Company’s operating margin decreased by 2.4 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q4, The Toro Company generated an operating margin profit margin of 8.4%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

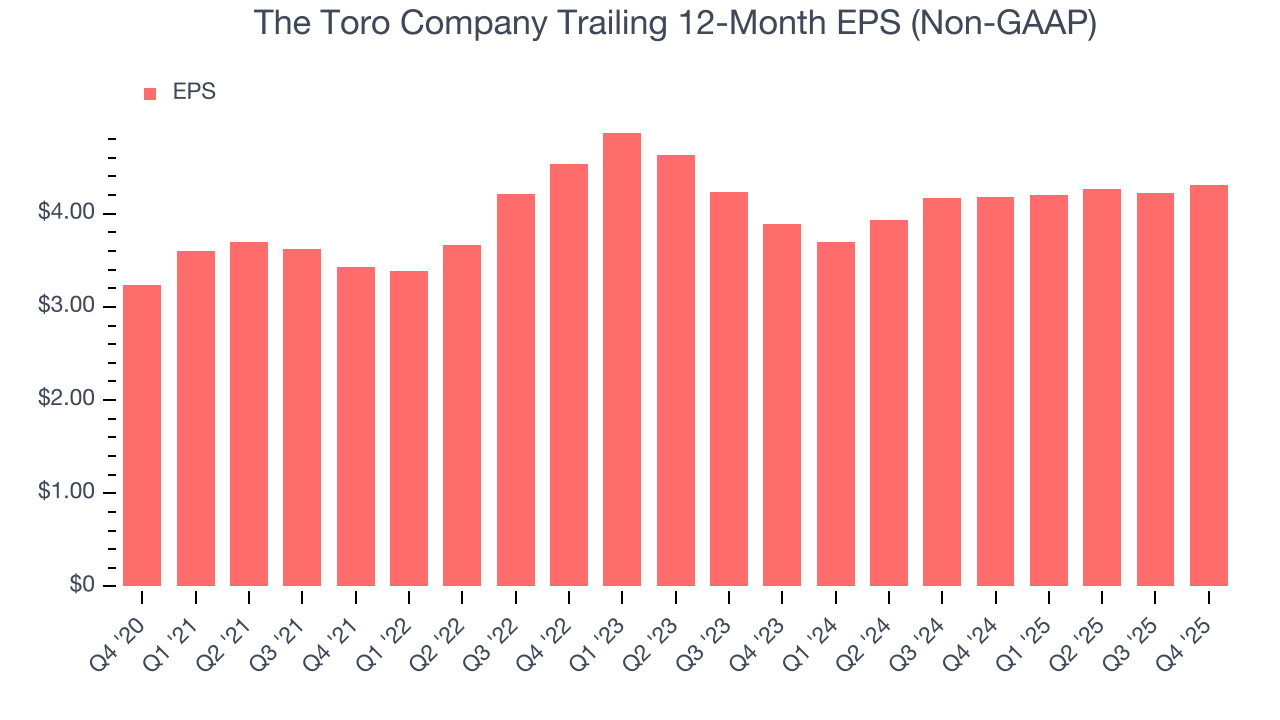

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

The Toro Company’s unimpressive 5.9% annual EPS growth over the last five years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

Although it wasn’t great, The Toro Company’s two-year annual EPS growth of 5.3% topped its 1.6% two-year revenue growth.

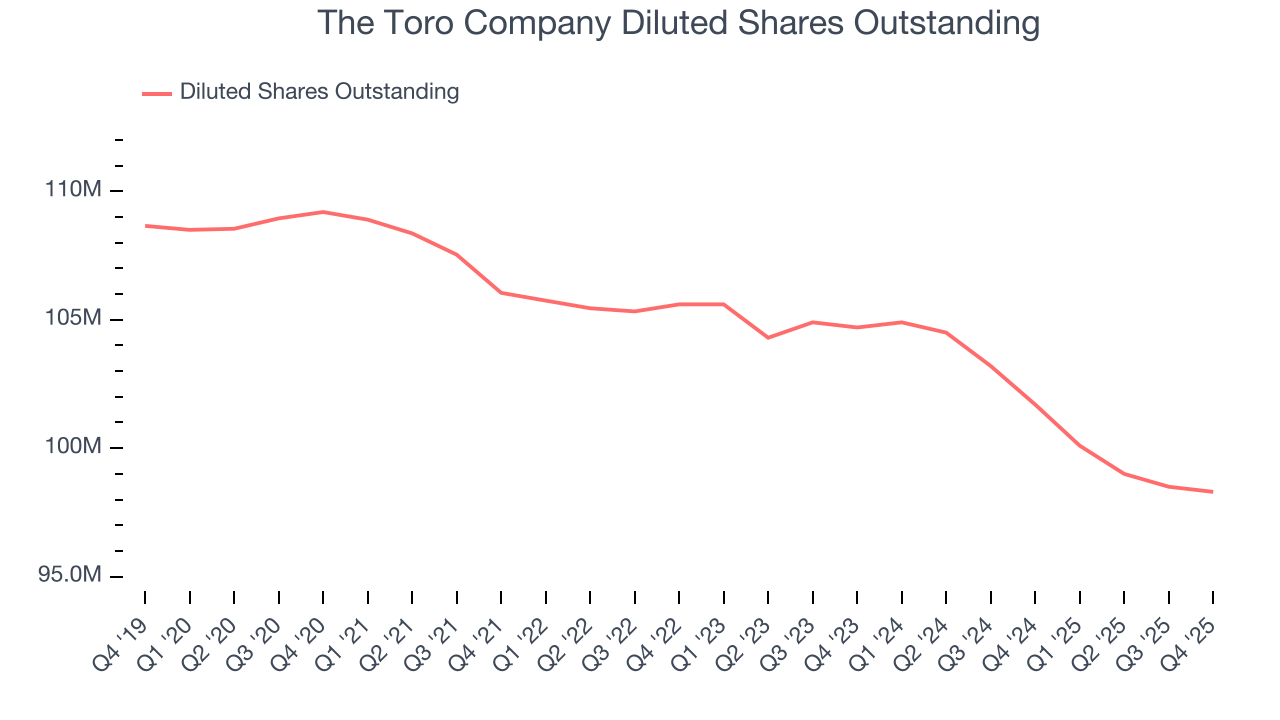

We can take a deeper look into The Toro Company’s earnings to better understand the drivers of its performance. A two-year view shows that The Toro Company has repurchased its stock, shrinking its share count by 6.1%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

In Q4, The Toro Company reported adjusted EPS of $0.74, up from $0.65 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects The Toro Company’s full-year EPS of $4.31 to grow 5.7%.

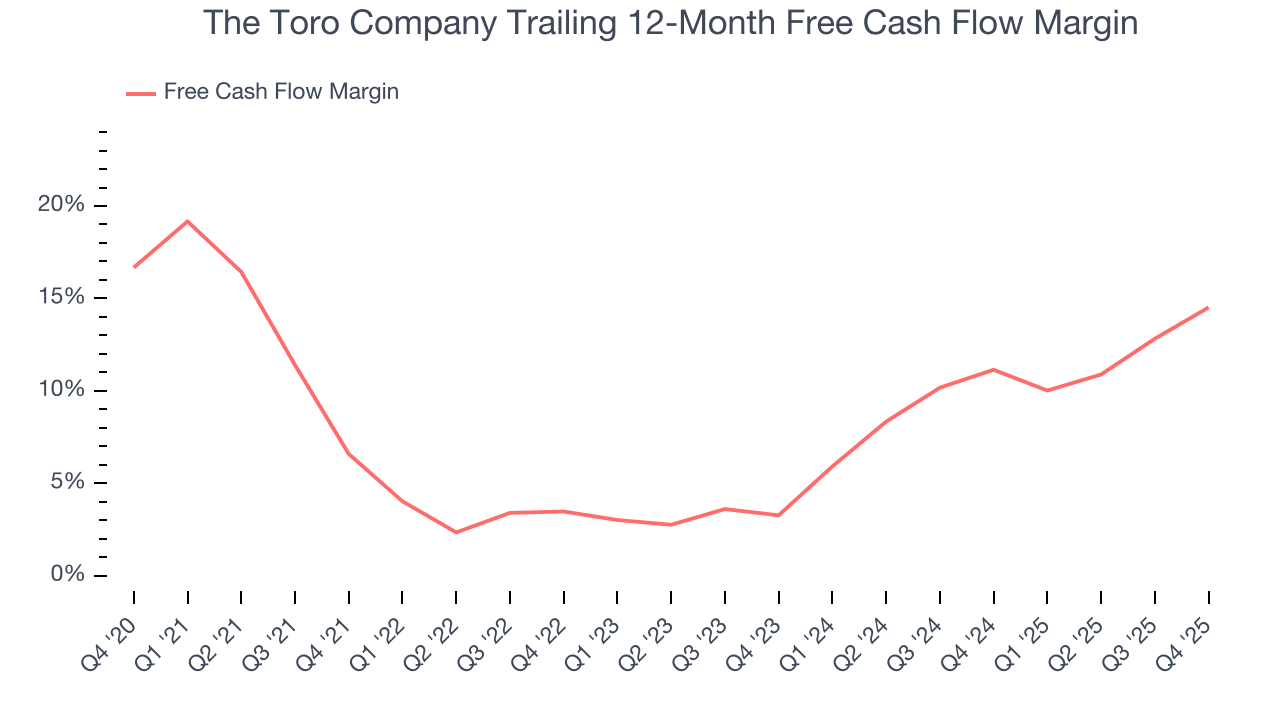

9. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

The Toro Company has shown impressive cash profitability, enabling it to ride out cyclical downturns more easily while maintaining its investments in new and existing offerings. The company’s free cash flow margin averaged 7.8% over the last five years, better than the broader industrials sector. The Toro Company has shown impressive cash profitability relative to peers over the last five years, giving the company fewer opportunities to return capital to shareholders.

Taking a step back, we can see that The Toro Company’s margin expanded by 7.9 percentage points during that time. This is encouraging, and we can see it became a less capital-intensive business because its free cash flow profitability rose while its operating profitability fell.

The Toro Company’s free cash flow clocked in at $14.6 million in Q4, equivalent to a 1.4% margin. Its cash flow turned positive after being negative in the same quarter last year, building on its favorable historical trend.

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Although The Toro Company hasn’t been the highest-quality company lately, it found a few growth initiatives in the past that worked out wonderfully. Its five-year average ROIC was 18.1%, splendid for an industrials business.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, The Toro Company’s ROIC has decreased over the last few years. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

11. Balance Sheet Assessment

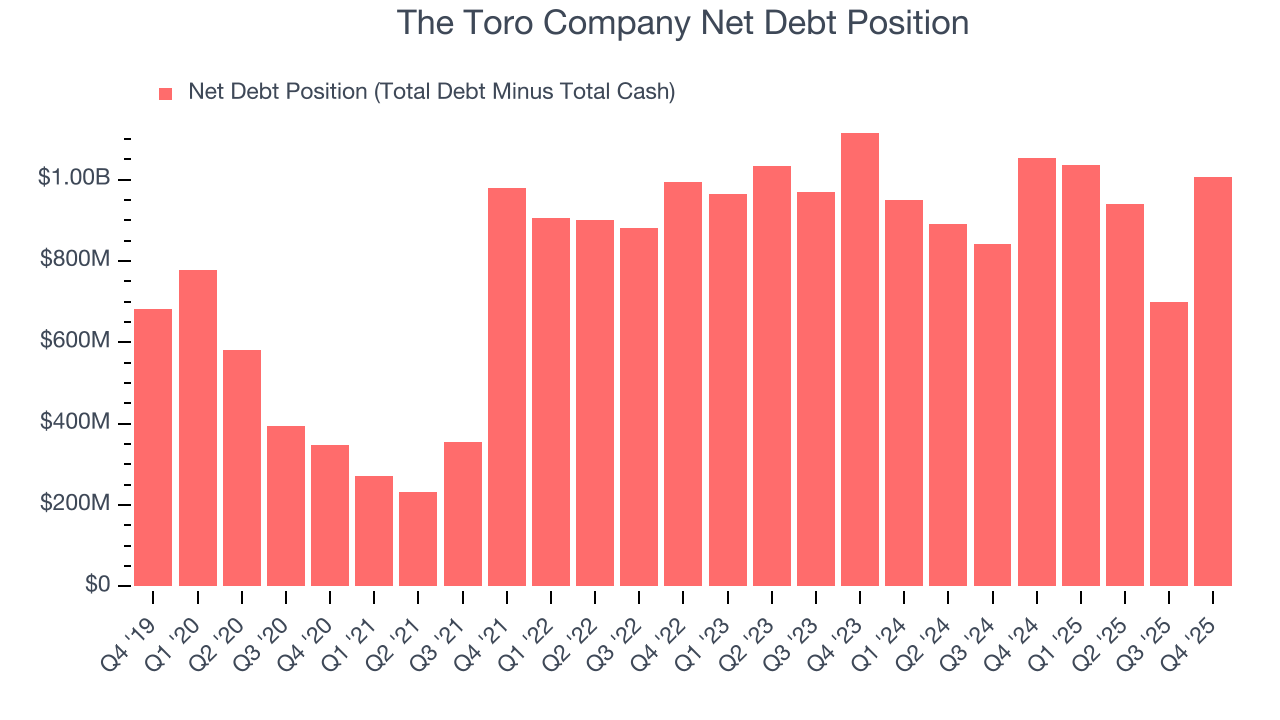

The Toro Company reported $189 million of cash and $1.2 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $698.9 million of EBITDA over the last 12 months, we view The Toro Company’s 1.4× net-debt-to-EBITDA ratio as safe. We also see its $29.9 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from The Toro Company’s Q4 Results

We were impressed by how significantly The Toro Company blew past analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. Overall, this print had some key positives. The stock remained flat at $101.60 immediately following the results.

13. Is Now The Time To Buy The Toro Company?

Updated: March 15, 2026 at 11:38 PM EDT

Before making an investment decision, investors should account for The Toro Company’s business fundamentals and valuation in addition to what happened in the latest quarter.

The Toro Company isn’t a terrible business, but it doesn’t pass our quality test. To kick things off, its revenue growth was uninspiring over the last five years, and analysts don’t see anything changing over the next 12 months. While its rising cash profitability gives it more optionality, the downside is its diminishing returns show management's prior bets haven't worked out. On top of that, its declining operating margin shows the business has become less efficient.

The Toro Company’s P/E ratio based on the next 12 months is 20.2x. Investors with a higher risk tolerance might like the company, but we think the potential downside is too great. We're fairly confident there are better investments elsewhere.

Wall Street analysts have a consensus one-year price target of $110.50 on the company (compared to the current share price of $95.50).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.