Agilysys (AGYS)

We’re not sold on Agilysys. Its weak revenue growth and gross margin show it not only lacks demand but also decent unit economics.― StockStory Analyst Team

1. News

2. Summary

Why Agilysys Is Not Exciting

With a tech stack that powers everything from check-in to checkout at some of the world's top hospitality venues, Agilysys (NASDAQ:AGYS) develops and provides cloud-based and on-premise software solutions for hotels, resorts, casinos, and restaurants to manage operations and enhance guest experiences.

- High servicing costs result in a relatively inferior gross margin of 61.7% that must be offset through increased usage

- Operating profits and efficiency rose over the last year as it benefited from some fixed cost leverage

- On the bright side, its user-friendly software enables clients to ramp up spending quickly, leading to the speedy recovery of customer acquisition costs

Agilysys doesn’t fulfill our quality requirements. There are more profitable opportunities elsewhere.

Why There Are Better Opportunities Than Agilysys

Agilysys is trading at $70.87 per share, or 5.6x forward price-to-sales. While valuation is appropriate for the quality you get, we’re still on the sidelines for now.

There are stocks out there featuring similar valuation multiples with better fundamentals. We prefer to invest in those.

3. Agilysys (AGYS) Research Report: Q4 CY2025 Update

Hospitality software provider Agilysys (NASDAQ:AGYS) reported Q4 CY2025 results exceeding the market’s revenue expectations, with sales up 15.6% year on year to $80.39 million. The company expects the full year’s revenue to be around $318 million, close to analysts’ estimates. Its non-GAAP profit of $0.42 per share was 7.8% below analysts’ consensus estimates.

Agilysys (AGYS) Q4 CY2025 Highlights:

- Revenue: $80.39 million vs analyst estimates of $79.28 million (15.6% year-on-year growth, 1.4% beat)

- Adjusted EPS: $0.42 vs analyst expectations of $0.46 (7.8% miss)

- Adjusted Operating Income: $17.15 million vs analyst estimates of $9.66 million (21.3% margin, 77.6% beat)

- The company slightly lifted its revenue guidance for the full year to $318 million at the midpoint from $316.5 million

- Operating Margin: 14.6%, up from 10.7% in the same quarter last year

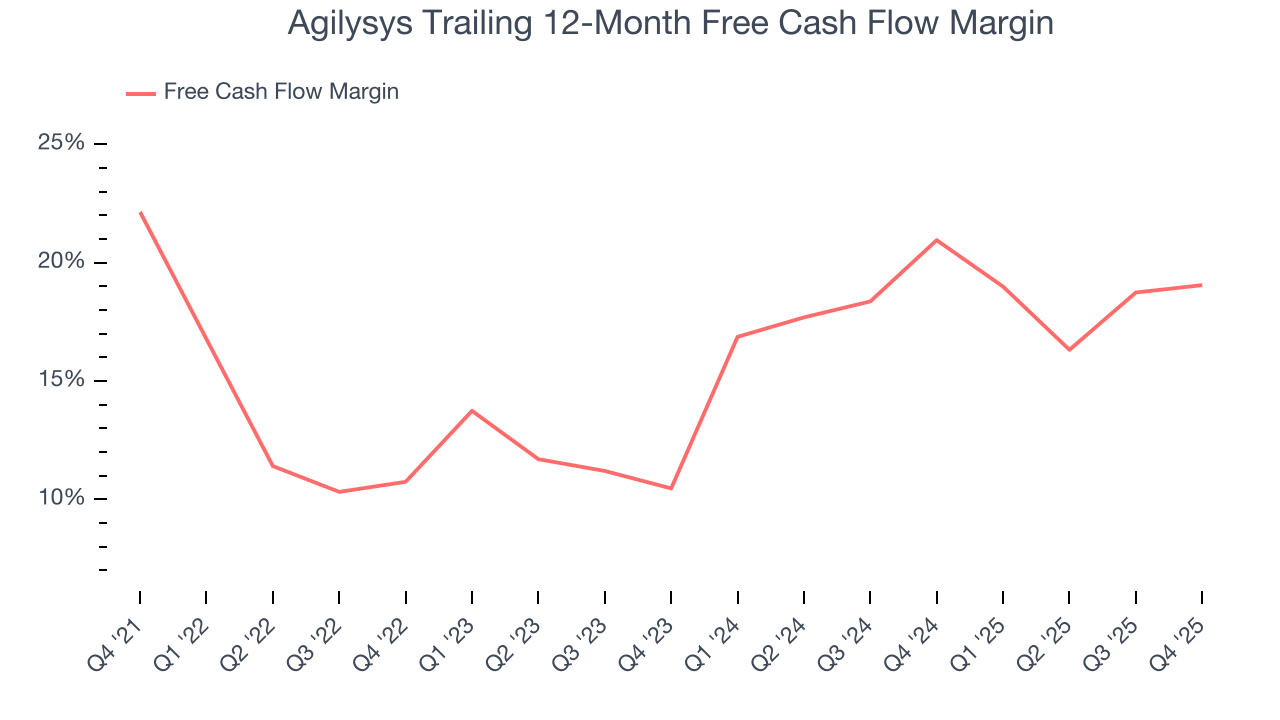

- Free Cash Flow Margin: 28.3%, up from 18.9% in the previous quarter

- Market Capitalization: $3.00 billion

Company Overview

With a tech stack that powers everything from check-in to checkout at some of the world's top hospitality venues, Agilysys (NASDAQ:AGYS) develops and provides cloud-based and on-premise software solutions for hotels, resorts, casinos, and restaurants to manage operations and enhance guest experiences.

Agilysys offers three integrated ecosystems of hospitality software: Property Management Systems (PMS), Point-of-Sale (POS), and Inventory & Procurement solutions. The company's comprehensive suite includes over 20 specialized applications that handle various aspects of hospitality operations, from managing room bookings and guest profiles to processing food orders and tracking inventory.

The company's customers use these systems to streamline their operations, increase revenue, and create personalized experiences for guests. For example, a resort might use Agilysys Stay PMS to manage room bookings and guest profiles, InfoGenesis POS for restaurant orders, and IG OnDemand to allow guests to order food from their mobile devices anywhere on the property. These integrated solutions help properties create a seamless experience while gathering valuable guest data for personalization and marketing.

Agilysys generates revenue through software licensing, subscription services, hardware sales, and professional services. The company has been shifting its business model toward recurring subscription and maintenance revenue, which provides more stable income than one-time product sales. This strategic focus on Software-as-a-Service (SaaS) has been driving its growth as the hospitality industry increasingly embraces cloud technology.

Operating across North America, Europe, the Middle East, Asia-Pacific, and India, Agilysys serves diverse clients ranging from luxury resorts and casino operators to universities, corporate foodservice, and healthcare facilities seeking to modernize their hospitality offerings.

4. Hospitality & Restaurant Software

Enterprise resource planning (ERP) and customer relationship management (CRM) are two of the largest software categories dominated by the likes of Microsoft, Oracle, and Salesforce.com. Today, the secular trend of mass customization is driving vertical software that customizes ERP and CRM functions for specific industry requirements. Restaurants are a prime example where a set of customized software providers have sprung up in recent years to create unique operating systems that blend tax and accounting software, order management and delivery, along with supply chain management. Hotels and other hospitality providers are another example.

Agilysys competes with larger enterprise software providers like Oracle Corp., Shiji Group, Amadeus IT Group, and Infor that offer bundled hospitality solutions. The company also faces competition from smaller specialized software providers like Maestro PMS and from custom in-house systems developed by large hotel chains.

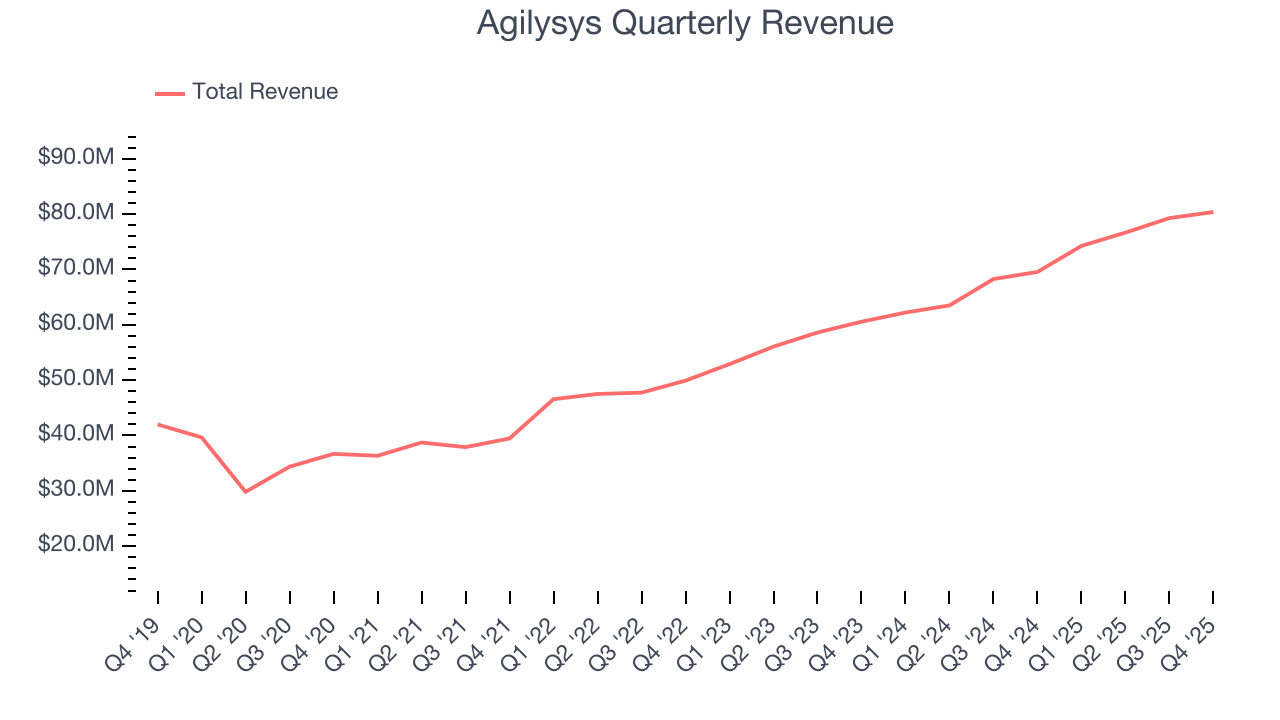

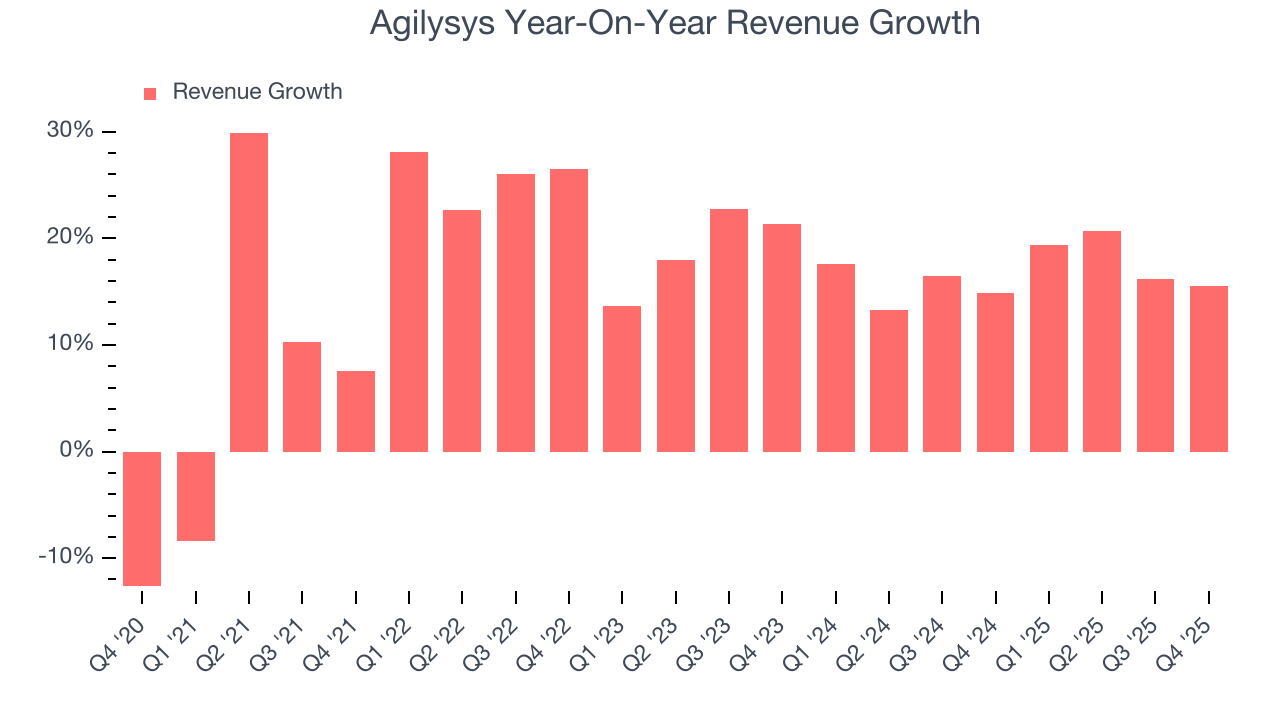

5. Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can have short-term success, but a top-tier one grows for years. Over the last five years, Agilysys grew its sales at a 17.2% annual rate. Although this growth is acceptable on an absolute basis, it fell slightly short of our standards for the software sector, which enjoys a number of secular tailwinds.

Long-term growth is the most important, but within software, a half-decade historical view may miss new innovations or demand cycles. Agilysys’s annualized revenue growth of 16.7% over the last two years aligns with its five-year trend, suggesting its demand was stable.

This quarter, Agilysys reported year-on-year revenue growth of 15.6%, and its $80.39 million of revenue exceeded Wall Street’s estimates by 1.4%.

Looking ahead, sell-side analysts expect revenue to grow 13.1% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and implies its products and services will face some demand challenges.

6. Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

Agilysys is very efficient at acquiring new customers, and its CAC payback period checked in at 22.8 months this quarter. The company’s rapid recovery of its customer acquisition costs indicates it has a highly differentiated product offering and a strong brand reputation. These dynamics give Agilysys more resources to pursue new product initiatives while maintaining the flexibility to increase its sales and marketing investments.

7. Gross Margin & Pricing Power

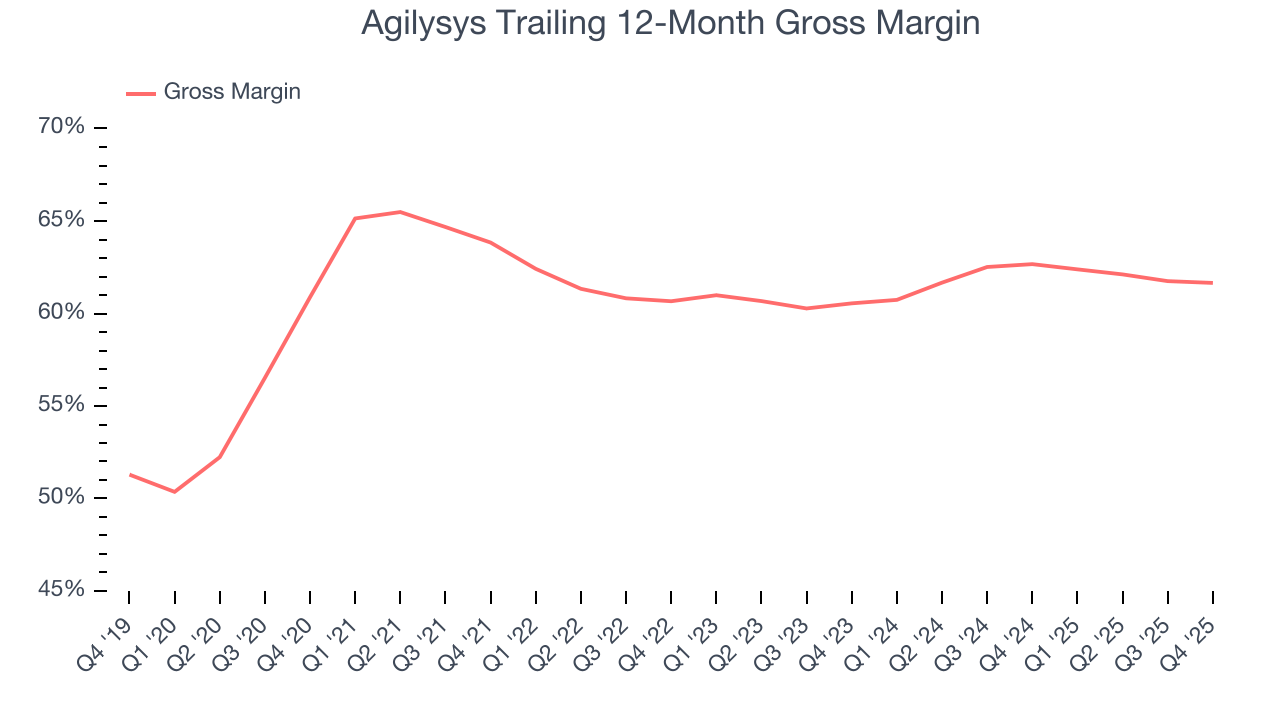

For software companies like Agilysys, gross profit tells us how much money remains after paying for the base cost of products and services (typically servers, licenses, and certain personnel). These costs are usually low as a percentage of revenue, explaining why software is more lucrative than other sectors.

Agilysys’s gross margin is substantially worse than most software businesses, signaling it has relatively high infrastructure costs compared to asset-lite businesses like ServiceNow. As you can see below, it averaged a 61.7% gross margin over the last year. That means Agilysys paid its providers a lot of money ($38.33 for every $100 in revenue) to run its business.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. Agilysys has seen gross margins improve by 1.1 percentage points over the last 2 year, which is slightly better than average for software.

Agilysys’s gross profit margin came in at 62.5% this quarter, in line with the same quarter last year. Zooming out, Agilysys’s full-year margin has been trending down over the past 12 months, decreasing by 1 percentage points. If this move continues, it could suggest a more competitive environment with some pressure to lower prices and higher input costs.

8. Operating Margin

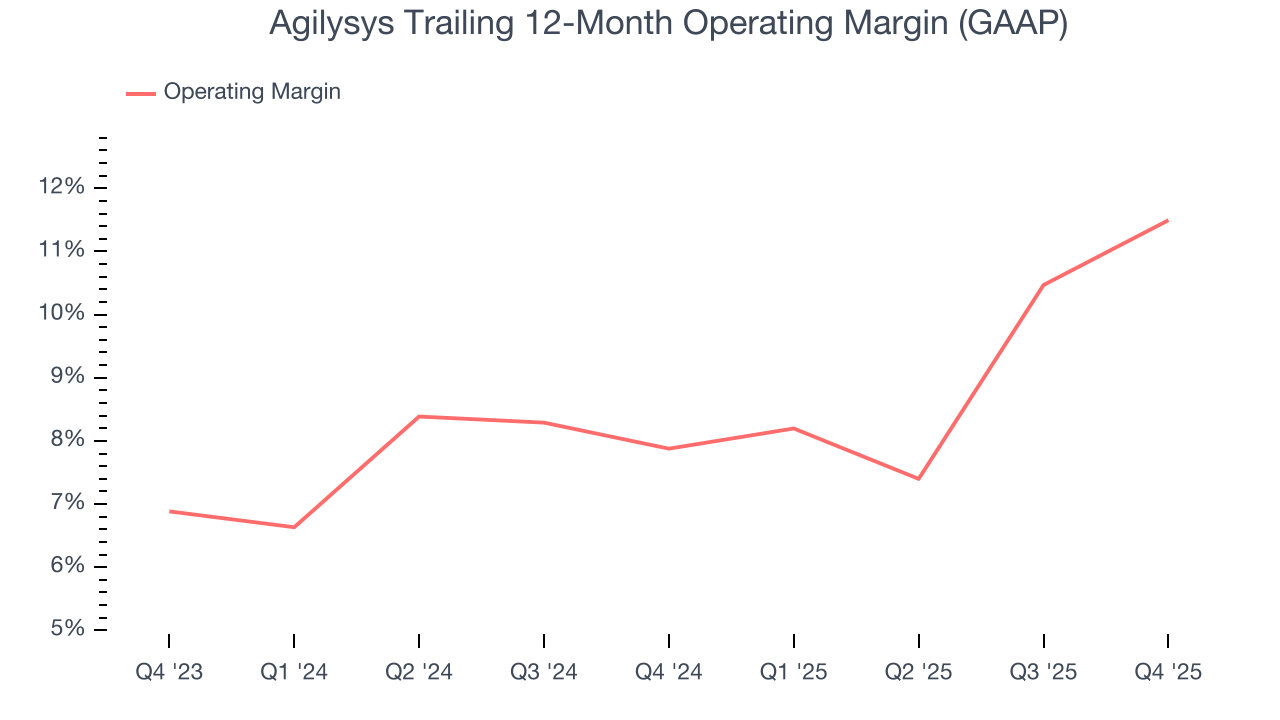

While many software businesses point investors to their adjusted profits, which exclude stock-based compensation (SBC), we prefer GAAP operating margin because SBC is a legitimate expense used to attract and retain talent. This metric shows how much revenue remains after accounting for all core expenses – everything from the cost of goods sold to sales and R&D.

Agilysys has been an efficient company over the last year. It was one of the more profitable businesses in the software sector, boasting an average operating margin of 11.5%. This result was particularly impressive because of its low gross margin, which is mostly a factor of what it sells and takes huge shifts to move meaningfully. Companies have more control over their operating margins, and it’s a show of well-managed operations if they’re high when gross margins are low.

Looking at the trend in its profitability, Agilysys’s operating margin rose by 3.6 percentage points over the last two years, as its sales growth gave it operating leverage.

This quarter, Agilysys generated an operating margin profit margin of 14.6%, up 3.9 percentage points year on year. The increase was encouraging, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

9. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Agilysys has shown impressive cash profitability, driven by its cost-effective customer acquisition strategy that gives it the option to invest in new products and services rather than sales and marketing. The company’s free cash flow margin averaged 19.1% over the last year, better than the broader software sector.

Agilysys’s free cash flow clocked in at $22.72 million in Q4, equivalent to a 28.3% margin. This cash profitability was in line with the comparable period last year and above its one-year average.

Over the next year, analysts’ consensus estimates show they’re expecting Agilysys’s free cash flow margin of 19.1% for the last 12 months to remain the same.

10. Balance Sheet Assessment

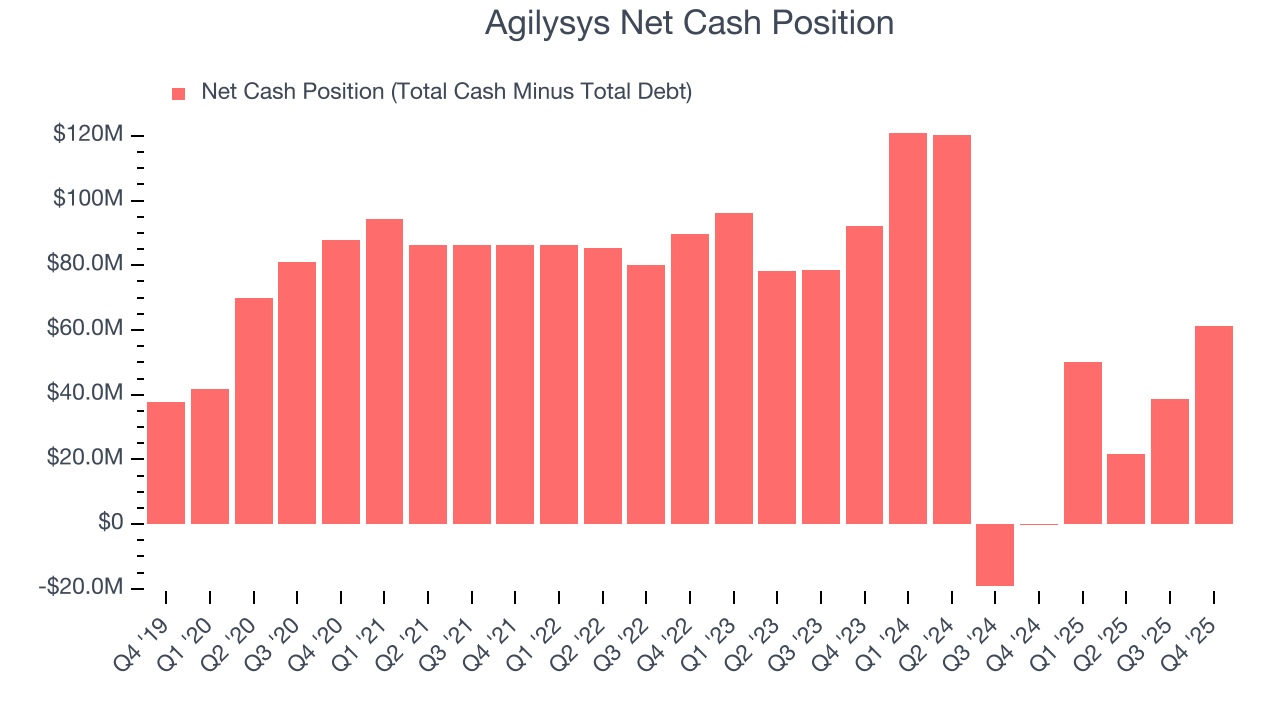

Companies with more cash than debt have lower bankruptcy risk.

Agilysys is a profitable, well-capitalized company with $81.45 million of cash and $20.3 million of debt on its balance sheet. This $61.15 million net cash position is 2% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

11. Key Takeaways from Agilysys’s Q4 Results

It was encouraging to see Agilysys beat analysts’ EBITDA expectations this quarter. We were also happy its revenue narrowly outperformed Wall Street’s estimates. Overall, this print had some key positives. Investors were likely hoping for more, and shares traded down 12.3% to $99.68 immediately after reporting.

12. Is Now The Time To Buy Agilysys?

Updated: March 22, 2026 at 10:34 PM EDT

Are you wondering whether to buy Agilysys or pass? We urge investors to not only consider the latest earnings results but also longer-term business quality and valuation as well.

Agilysys doesn’t top our investment wishlist, but we understand that it’s not a bad business. Although its revenue growth was mediocre over the last five years and analysts expect growth to slow over the next 12 months, its efficient sales strategy allows it to target and onboard new users at scale. Tread carefully with this one, however, as its gross margins show its business model is much less lucrative than other companies.

Agilysys’s price-to-sales ratio based on the next 12 months is 5.6x. While this valuation is reasonable, we don’t really see a big opportunity at the moment. We're fairly confident there are better investments elsewhere.

Wall Street analysts have a consensus one-year price target of $138 on the company (compared to the current share price of $70.87).