American Outdoor Brands (AOUT)

American Outdoor Brands is in for a bumpy ride. Its falling revenue and negative returns on capital suggest it’s destroying value as demand fizzles out.― StockStory Analyst Team

1. News

2. Summary

Why We Think American Outdoor Brands Will Underperform

Spun off from Smith and Wesson in 2020, American Outdoor Brands (NASDAQ:AOUT) is an outdoor and recreational products company that offers outdoor and shooting sports products but does not sell firearms themselves.

- Products and services have few die-hard fans as sales have declined by 4.3% annually over the last five years

- Sales were less profitable over the last five years as its earnings per share fell by 40.1% annually, worse than its revenue declines

- Sales are projected to remain flat over the next 12 months as demand decelerates from its two-year trend

American Outdoor Brands falls short of our quality standards. There’s a wealth of better opportunities.

Why There Are Better Opportunities Than American Outdoor Brands

American Outdoor Brands is trading at $8.01 per share, or 32.9x forward P/E. Not only is American Outdoor Brands’s multiple richer than most consumer discretionary peers, but it’s also expensive for its revenue characteristics.

There are stocks out there similarly priced with better business quality. We prefer owning these.

3. American Outdoor Brands (AOUT) Research Report: Q4 CY2025 Update

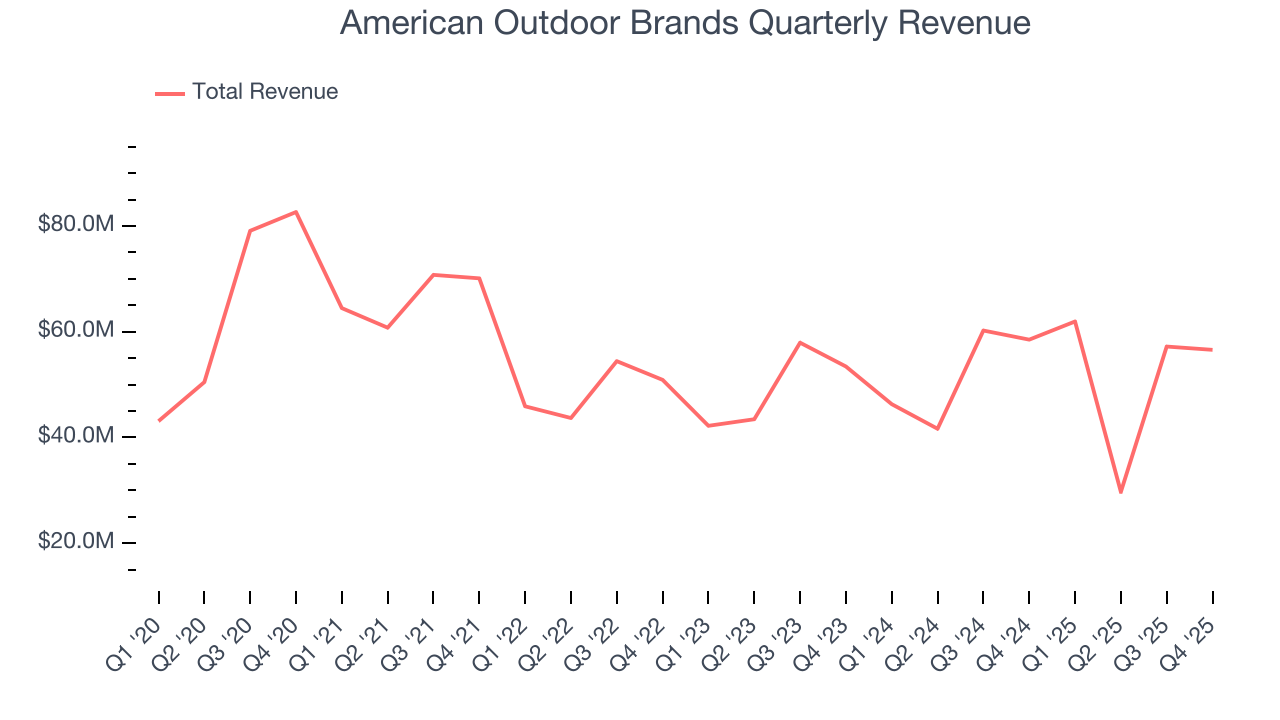

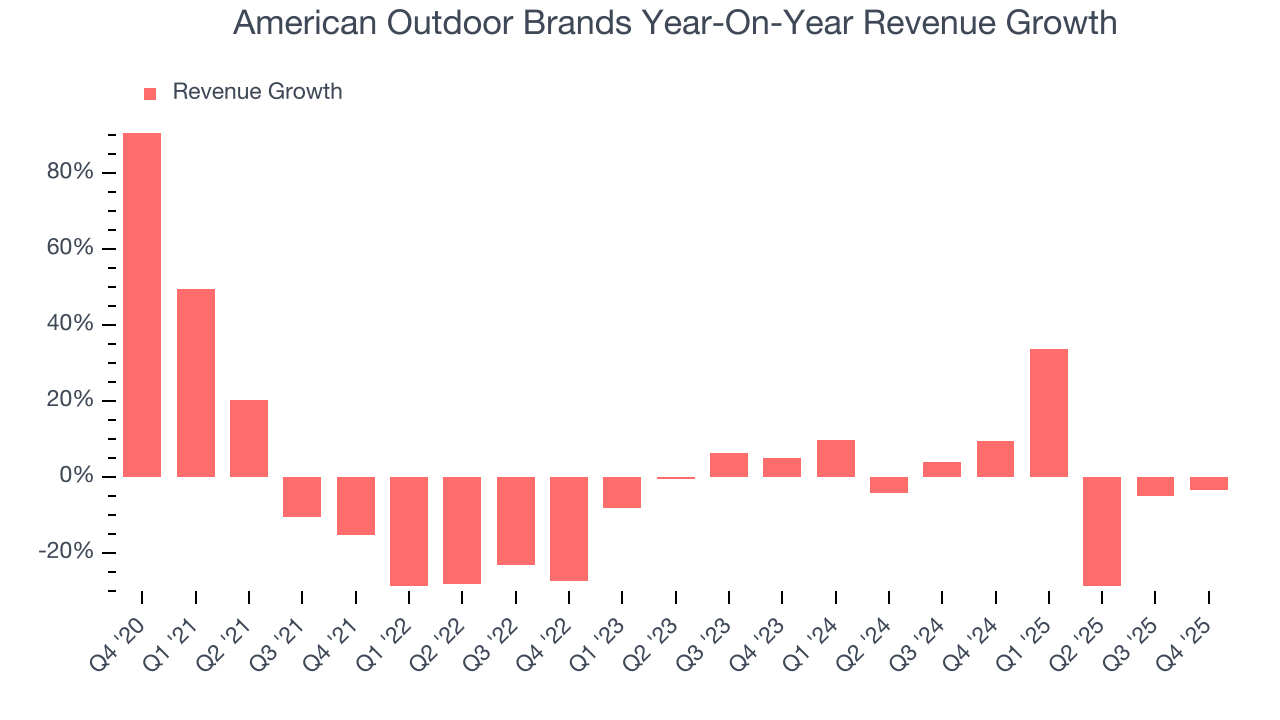

Recreational products manufacturer American Outdoor Brands (NASDAQ:AOUT) announced better-than-expected revenue in Q4 CY2025, but sales fell by 3.3% year on year to $56.58 million. Its non-GAAP profit of $0.12 per share was 41.2% above analysts’ consensus estimates.

American Outdoor Brands (AOUT) Q4 CY2025 Highlights:

- Revenue: $56.58 million vs analyst estimates of $53.81 million (3.3% year-on-year decline, 5.1% beat)

- Adjusted EPS: $0.12 vs analyst estimates of $0.09 (41.2% beat)

- Adjusted EBITDA: $3.30 million vs analyst estimates of $2.88 million (5.8% margin, relatively in line)

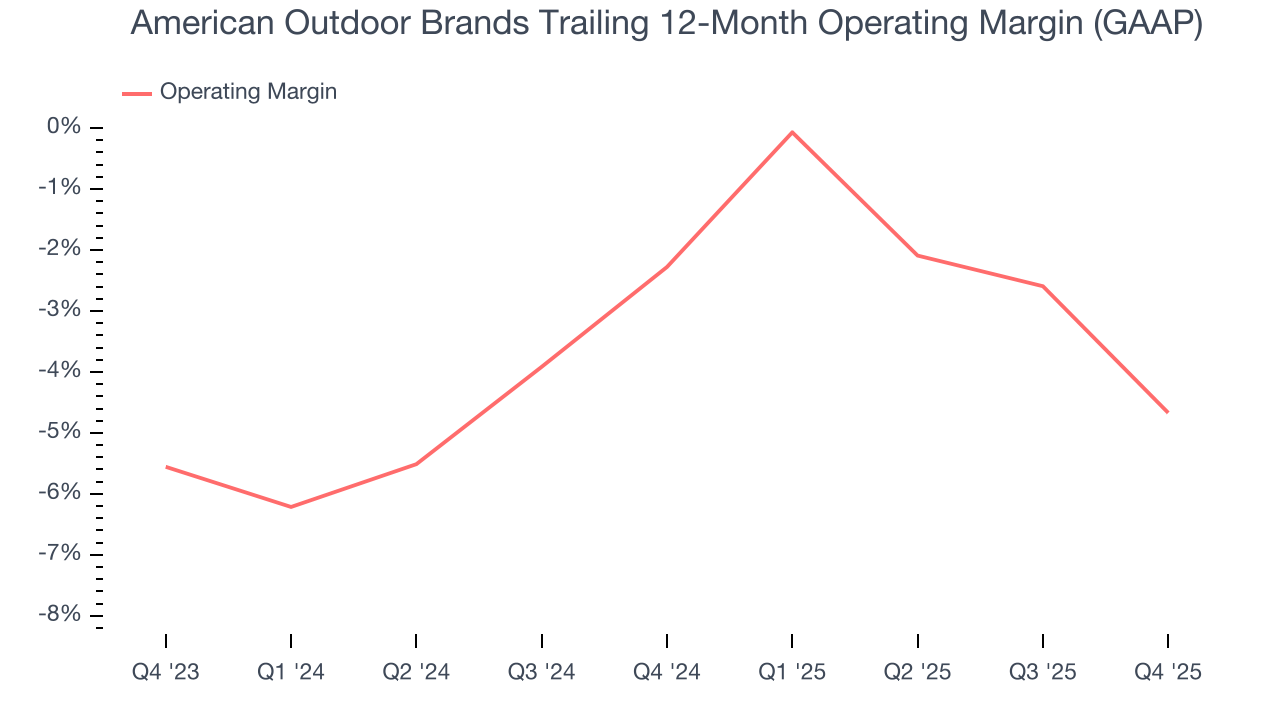

- Operating Margin: -6.9%, down from 0.5% in the same quarter last year

- Free Cash Flow Margin: 15.4%, up from 7.2% in the same quarter last year

- Market Capitalization: $108.9 million

Company Overview

Spun off from Smith and Wesson in 2020, American Outdoor Brands (NASDAQ:AOUT) is an outdoor and recreational products company that offers outdoor and shooting sports products but does not sell firearms themselves.

The company is a manufacturer and marketer of outdoor lifestyle, shooting sports, and rugged adventure products. The company operates through two major segments: Shooting Sports and Outdoor Lifestyle, each catering to enthusiasts, professionals, and outdoor adventurers.

The Shooting Sports segment includes firearm-related accessories such as gun cleaning kits, reloading supplies, and optics, with brands like Tipton and Caldwell. The Outdoor Lifestyle segment offers hunting, camping, fishing, and survival gear, including knives, cooking equipment, and backpacks, sold under brands like BUBBA and Schrade.

Customers range from hunters, recreational shooters, and law enforcement to outdoor adventurers and anglers. Notable products include BUBBA fillet knives, Frankford Arsenal reloading tools, and Hooyman tree saws.

4. Consumer Discretionary - Leisure Products

The Consumer Discretionary sector, by definition, is made up of companies selling non-essential goods and services. When economic conditions deteriorate or tastes shift, consumers can easily cut back or eliminate these purchases. For long-term investors with five-year holding periods, this creates a structural challenge: the sector is inherently hit-driven, with low switching costs and fickle customers. As a result, only a handful of companies can reliably grow demand and compound earnings over long periods, which is why our bar is high and High Quality ratings are rare.

Leisure products companies manufacture recreational goods such as bicycles, marine vessels, fitness equipment, camping gear, and musical instruments. Tailwinds include heightened outdoor-activity participation, health-and-wellness awareness, and periodic innovation cycles that drive trade-up purchases. Headwinds are pronounced: demand is highly discretionary and sensitive to economic cycles—consumers readily defer big-ticket leisure purchases during downturns. Post-pandemic normalization has created excess channel inventory after demand surged then retreated. Raw-material and shipping cost inflation squeezes margins, while competition from low-cost imports and a fragmented market make pricing power elusive for most players.

Other companies offering shooting sports and outdoor products include Ruger (NYSE:RGR) and private companies O.F. Mossberg & Sons and the Remington Arms Company.

5. Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, American Outdoor Brands’s demand was weak and its revenue declined by 4.3% per year. This wasn’t a great result and suggests it’s a low quality business.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. American Outdoor Brands’s annualized revenue growth of 2.1% over the last two years is above its five-year trend, which is encouraging.

This quarter, American Outdoor Brands’s revenue fell by 3.3% year on year to $56.58 million but beat Wall Street’s estimates by 5.1%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months, a slight deceleration versus the last two years. This projection doesn't excite us and indicates its products and services will see some demand headwinds.

6. Operating Margin

American Outdoor Brands’s operating margin has shrunk over the last 12 months and averaged negative 3.5% over the last two years. Unprofitable consumer discretionary companies with falling margins deserve extra scrutiny because they’re spending loads of money to stay relevant, an unsustainable practice.

American Outdoor Brands’s operating margin was negative 6.9% this quarter. The company's consistent lack of profits raise a flag.

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

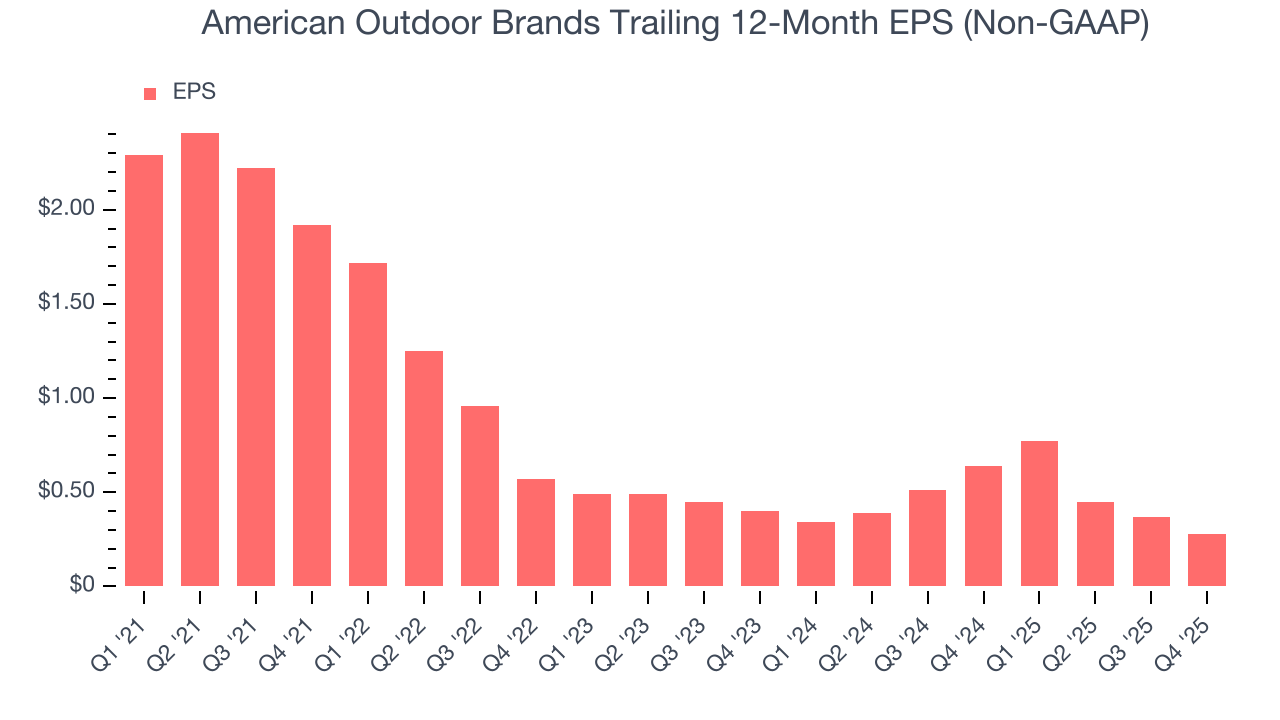

Sadly for American Outdoor Brands, its EPS declined by 40.1% annually over the last five years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

In Q4, American Outdoor Brands reported adjusted EPS of $0.12, down from $0.21 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects American Outdoor Brands’s full-year EPS of $0.28 to grow 7.1%.

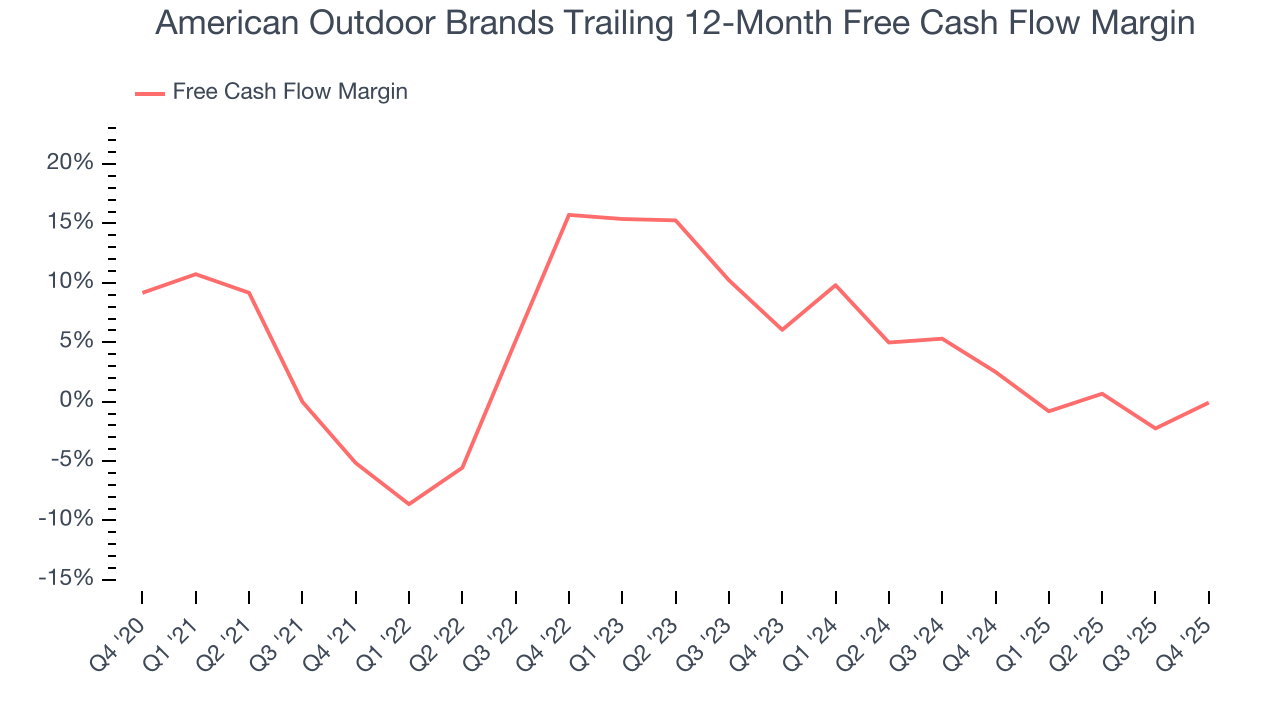

8. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

American Outdoor Brands has shown poor cash profitability relative to peers over the last two years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 1.2%, below what we’d expect for a consumer discretionary business.

American Outdoor Brands’s free cash flow clocked in at $8.72 million in Q4, equivalent to a 15.4% margin. This result was good as its margin was 8.2 percentage points higher than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, leading to temporary swings. Long-term trends trump fluctuations.

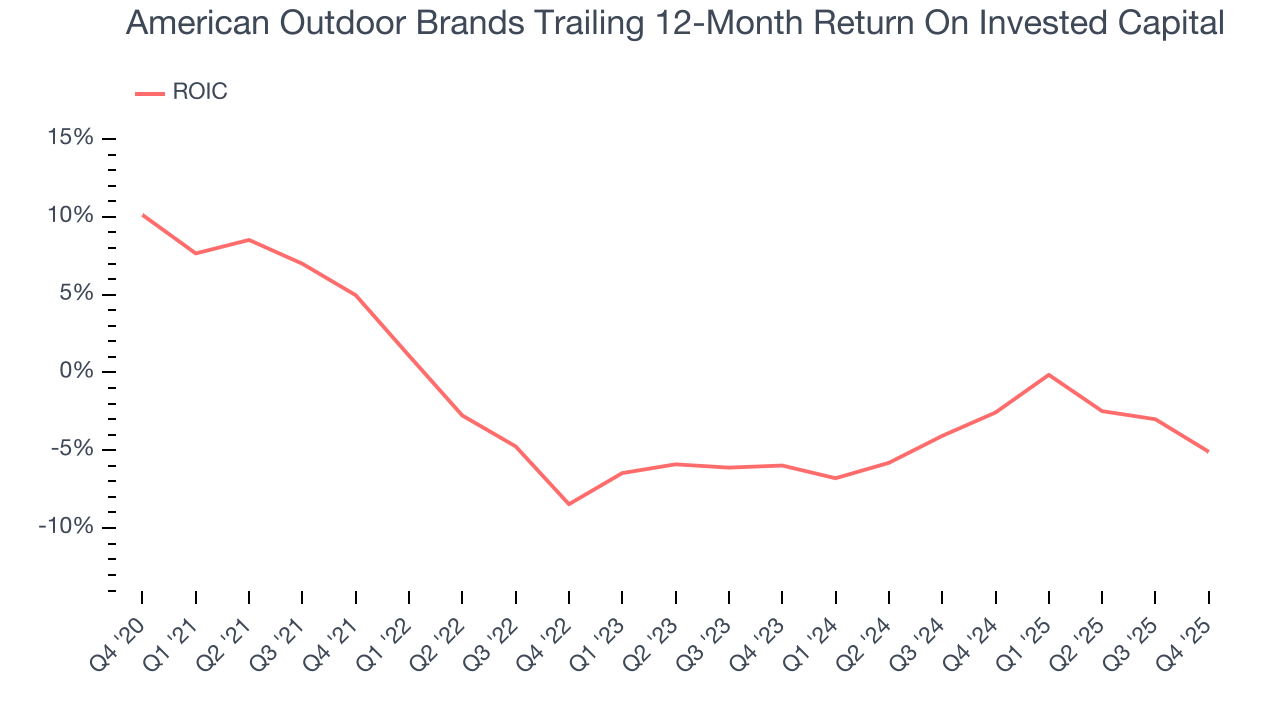

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

American Outdoor Brands’s five-year average ROIC was negative 3.4%, meaning management lost money while trying to expand the business. Its returns were among the worst in the consumer discretionary sector.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, American Outdoor Brands’s ROIC averaged 2.1 percentage point decreases each year over the last few years. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

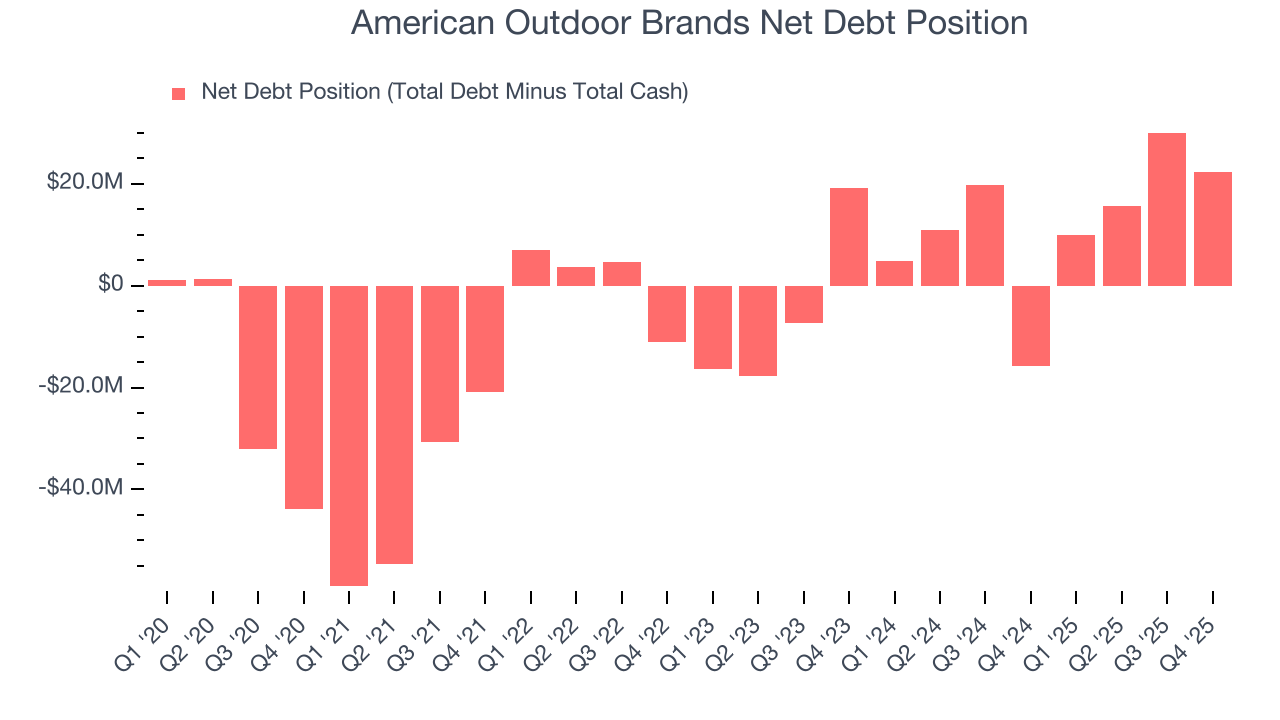

10. Balance Sheet Assessment

American Outdoor Brands reported $10.4 million of cash and $32.77 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $10.12 million of EBITDA over the last 12 months, we view American Outdoor Brands’s 2.2× net-debt-to-EBITDA ratio as safe. We also see its $192,000 of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from American Outdoor Brands’s Q4 Results

It was good to see American Outdoor Brands beat analysts’ EPS expectations this quarter. We were also glad its revenue outperformed Wall Street’s estimates. Zooming out, we think this quarter featured some important positives. Investors were likely hoping for more, and shares traded down 9.3% to $7.77 immediately following the results.

12. Is Now The Time To Buy American Outdoor Brands?

Updated: March 15, 2026 at 12:05 AM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in American Outdoor Brands.

We see the value of companies helping consumers, but in the case of American Outdoor Brands, we’re out. On top of that, American Outdoor Brands’s declining EPS over the last five years makes it a less attractive asset to the public markets, and its projected EPS for the next year is lacking.

American Outdoor Brands’s P/E ratio based on the next 12 months is 32.9x. At this valuation, there’s a lot of good news priced in - we think there are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $12.50 on the company (compared to the current share price of $8.01).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.