Health Catalyst (HCAT)

Health Catalyst faces an uphill battle. Its poor revenue growth shows demand is soft and its cash burn makes us question its business model.― StockStory Analyst Team

1. News

2. Summary

Why We Think Health Catalyst Will Underperform

Built on its "Health Catalyst Flywheel" methodology that emphasizes measurable outcomes, Health Catalyst (NASDAQ:HCAT) provides data and analytics technology and services that help healthcare organizations manage their data and drive measurable clinical, financial, and operational improvements.

- Muted 2.5% annual revenue growth over the last two years shows its demand lagged behind its software peers

- Projected sales decline of 9.7% for the next 12 months points to a tough demand environment ahead

- Gross margin of 48.7% reflects its high servicing costs

Health Catalyst is in the doghouse. Better businesses are for sale in the market.

Why There Are Better Opportunities Than Health Catalyst

Health Catalyst’s stock price of $1.33 implies a valuation ratio of 0.5x forward price-to-sales. This sure is a cheap multiple, but you get what you pay for.

Cheap stocks can look like a great deal at first glance, but they can be value traps. They often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. Health Catalyst (HCAT) Research Report: Q4 CY2025 Update

Healthcare data analytics company Health Catalyst (NASDAQ:HCAT) reported Q4 CY2025 results exceeding the market’s revenue expectations, but sales fell by 6.2% year on year to $74.68 million. On the other hand, next quarter’s revenue guidance of $69 million was less impressive, coming in 7.9% below analysts’ estimates. Its non-GAAP profit of $0.08 per share was 16.1% below analysts’ consensus estimates.

Health Catalyst (HCAT) Q4 CY2025 Highlights:

- Revenue: $74.68 million vs analyst estimates of $74.04 million (6.2% year-on-year decline, 0.9% beat)

- Adjusted EPS: $0.08 vs analyst expectations of $0.10 (16.1% miss)

- Adjusted EBITDA: $13.79 million vs analyst estimates of $13.37 million (18.5% margin, 3.1% beat)

- Revenue Guidance for Q1 CY2026 is $69 million at the midpoint, below analyst estimates of $74.91 million

- EBITDA guidance for Q1 CY2026 is $7.5 million at the midpoint, below analyst estimates of $11.26 million

- Operating Margin: -115%, down from -22% in the same quarter last year

- Free Cash Flow was $4.50 million, up from -$5.27 million in the previous quarter

- Market Capitalization: $131.6 million

Company Overview

Built on its "Health Catalyst Flywheel" methodology that emphasizes measurable outcomes, Health Catalyst (NASDAQ:HCAT) provides data and analytics technology and services that help healthcare organizations manage their data and drive measurable clinical, financial, and operational improvements.

At the core of Health Catalyst's solution is its Data Operating System (DOS), a healthcare-specific, cloud-based platform that integrates and organizes data from disparate healthcare systems, creating a unified source of truth for analytics. This platform is enhanced by pre-built analytics applications targeting common healthcare challenges across clinical quality, population health, and financial operations.

The company complements its technology with a team of analytics and healthcare domain experts who help clients implement solutions and achieve measurable improvements. These professionals include data analysts, data scientists, physicians, nurses, and healthcare administrators who provide services ranging from data governance and quality improvement strategies to cost accounting and population health initiatives.

Health Catalyst primarily serves healthcare providers through subscription-based contracts. Its diverse client base includes academic medical centers, integrated delivery networks, community hospitals, physician practices, Accountable Care Organizations, and health insurers. A typical client might use Health Catalyst's platform to identify clinical variations in care, reduce readmission rates, optimize staffing levels, or improve revenue cycle management—all supported by the company's technology and domain expertise. By documenting over 1,600 client-verified improvements, Health Catalyst has built a reputation for delivering tangible results in an industry often challenged by data fragmentation and complexity.

4. Data Analytics

Organizations generate a lot of data that is stored in silos, often in incompatible formats, making it slow and costly to extract actionable insights, which in turn drives demand for modern cloud-based data analysis platforms that can efficiently analyze the siloed data.

Health Catalyst's competitors include industry-agnostic analytics companies like IBM, Microsoft, Snowflake, and Tableau CRM; EHR providers such as Cerner Systems and Epic Systems; and healthcare-specific analytics vendors including Optum Analytics, Premier, Arcadia.io, Strata Decision Technology, Craneware, Innovaccer, and Intersystems.

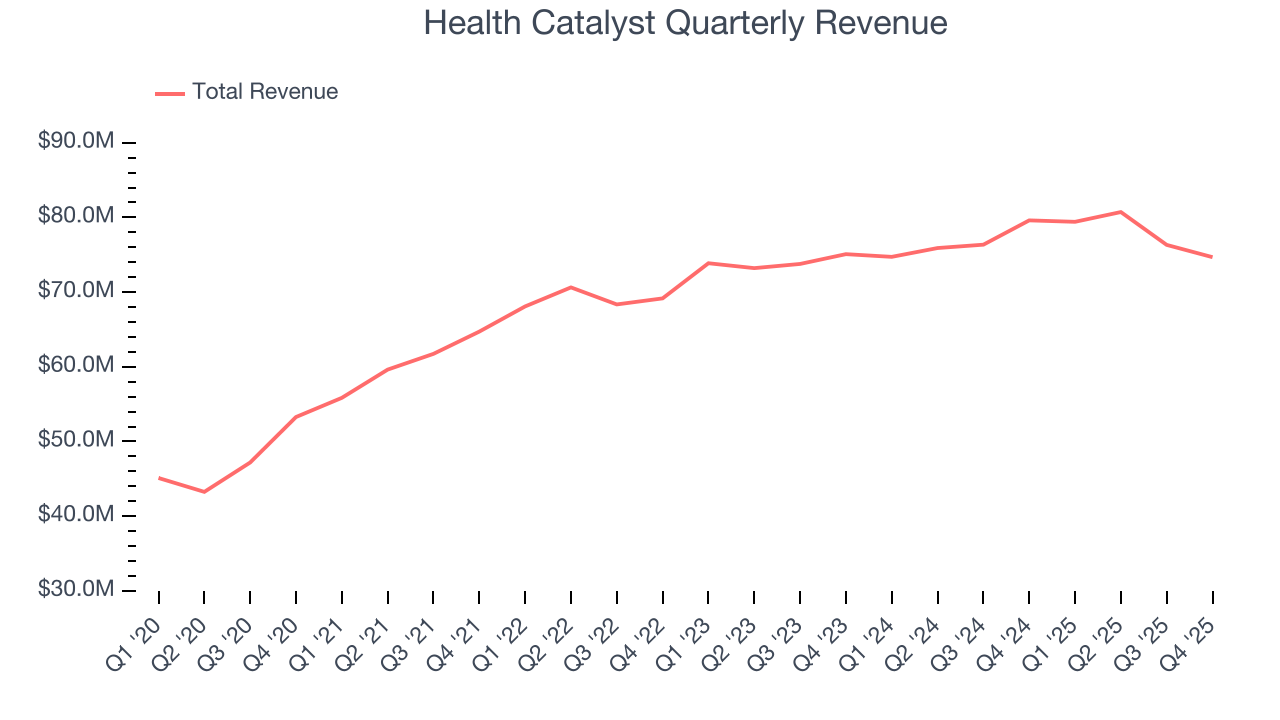

5. Revenue Growth

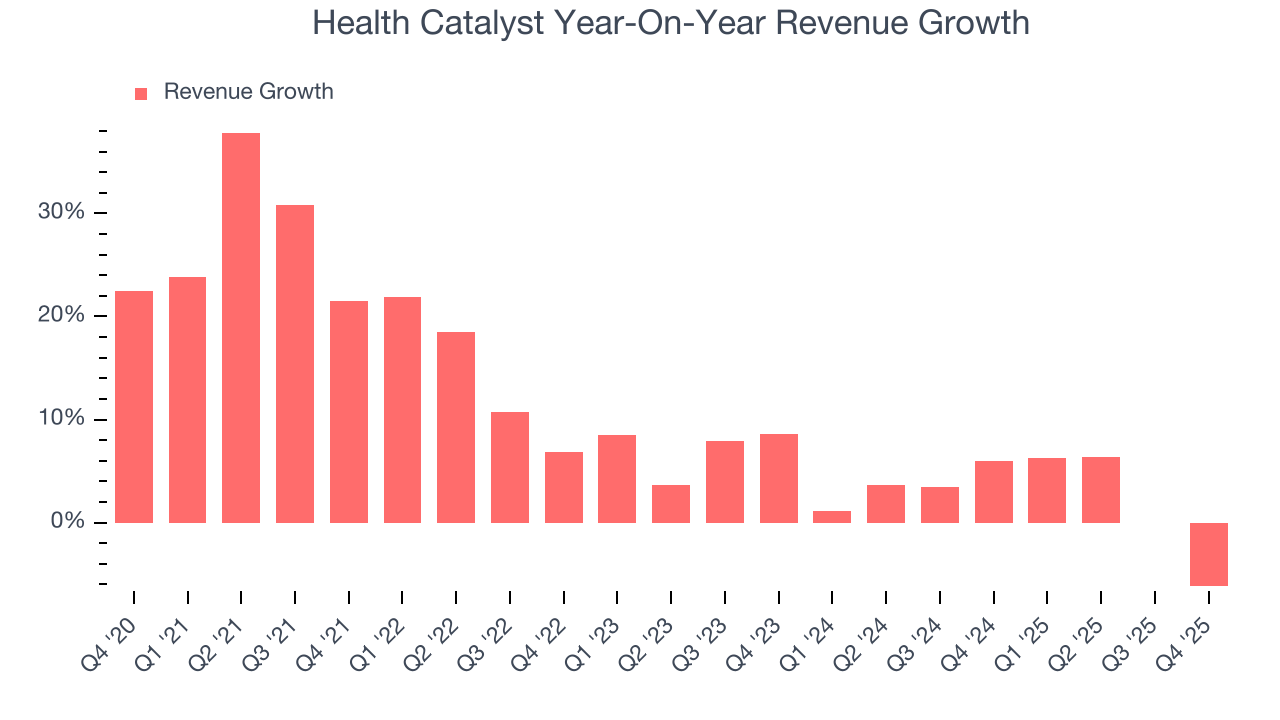

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Health Catalyst grew its sales at a 10.5% annual rate. Though this growth is acceptable on an absolute basis, we need to see more than just topline growth for the software sector, which can display significant earnings volatility. This means our bar for the sector is particularly high, reflecting the non-essential and hit-driven nature of the products and services offered. Additionally, five-year CAGR starts around Covid, when revenue was depressed then rebounded.

We at StockStory place the most emphasis on long-term growth, but within software, a half-decade historical view may miss recent innovations or disruptive industry trends. Health Catalyst’s recent performance shows its demand has slowed as its annualized revenue growth of 2.5% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

This quarter, Health Catalyst’s revenue fell by 6.2% year on year to $74.68 million but beat Wall Street’s estimates by 0.9%. Company management is currently guiding for a 13.1% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to decline by 2.9% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and indicates its products and services will see some demand headwinds.

6. Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

Health Catalyst’s recent customer acquisition efforts haven’t yielded returns as its CAC payback period was negative this quarter, meaning its incremental sales and marketing investments outpaced its revenue. The company’s inefficiency indicates it operates in a highly competitive environment where there is little differentiation between Health Catalyst’s products and its peers.

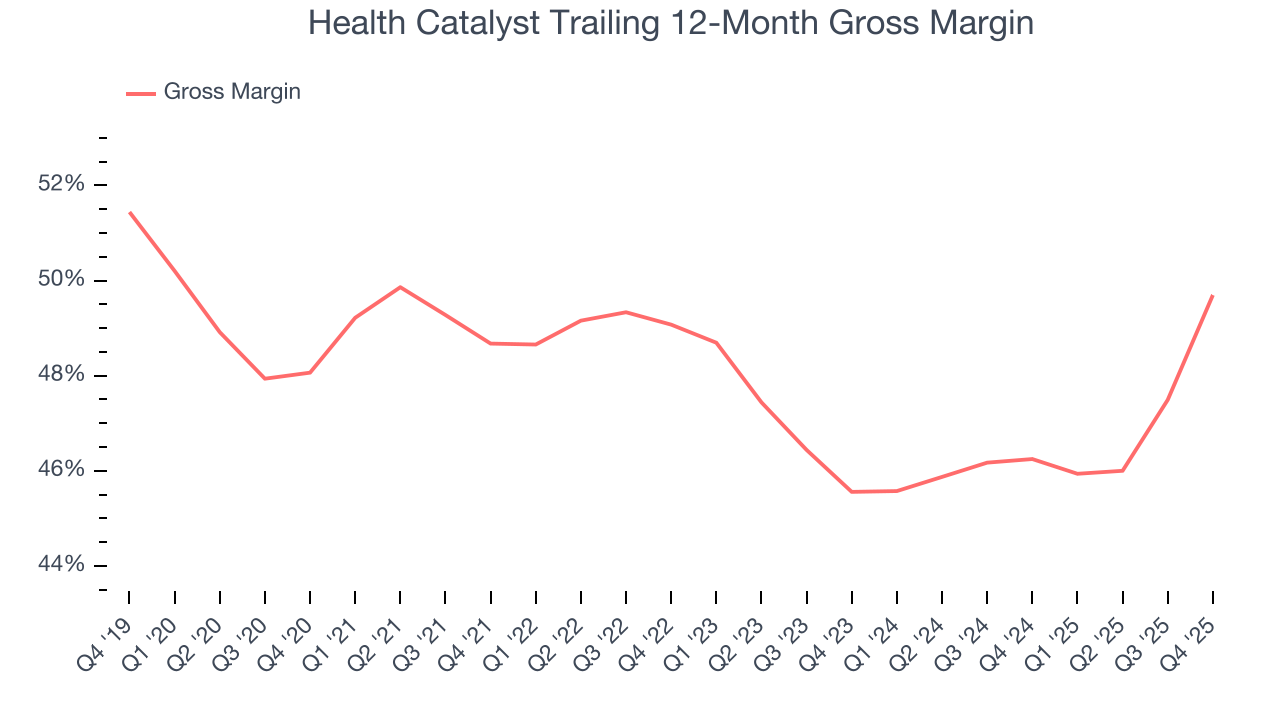

7. Gross Margin & Pricing Power

For software companies like Health Catalyst, gross profit tells us how much money remains after paying for the base cost of products and services (typically servers, licenses, and certain personnel). These costs are usually low as a percentage of revenue, explaining why software is more lucrative than other sectors.

Health Catalyst’s gross margin is substantially worse than most software businesses, signaling it has relatively high infrastructure costs compared to asset-lite businesses like ServiceNow. As you can see below, it averaged a 49.7% gross margin over the last year. That means Health Catalyst paid its providers a lot of money ($50.30 for every $100 in revenue) to run its business.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. Health Catalyst has seen gross margins improve by 4.1 percentage points over the last 2 year, which is very good in the software space.

Health Catalyst produced a 52.7% gross profit margin in Q4, up 8.9 percentage points year on year. Health Catalyst’s full-year margin has also been trending up over the past 12 months, increasing by 3.4 percentage points. If this move continues, it could suggest better unit economics due to some combination of stable to improving pricing power and input costs.

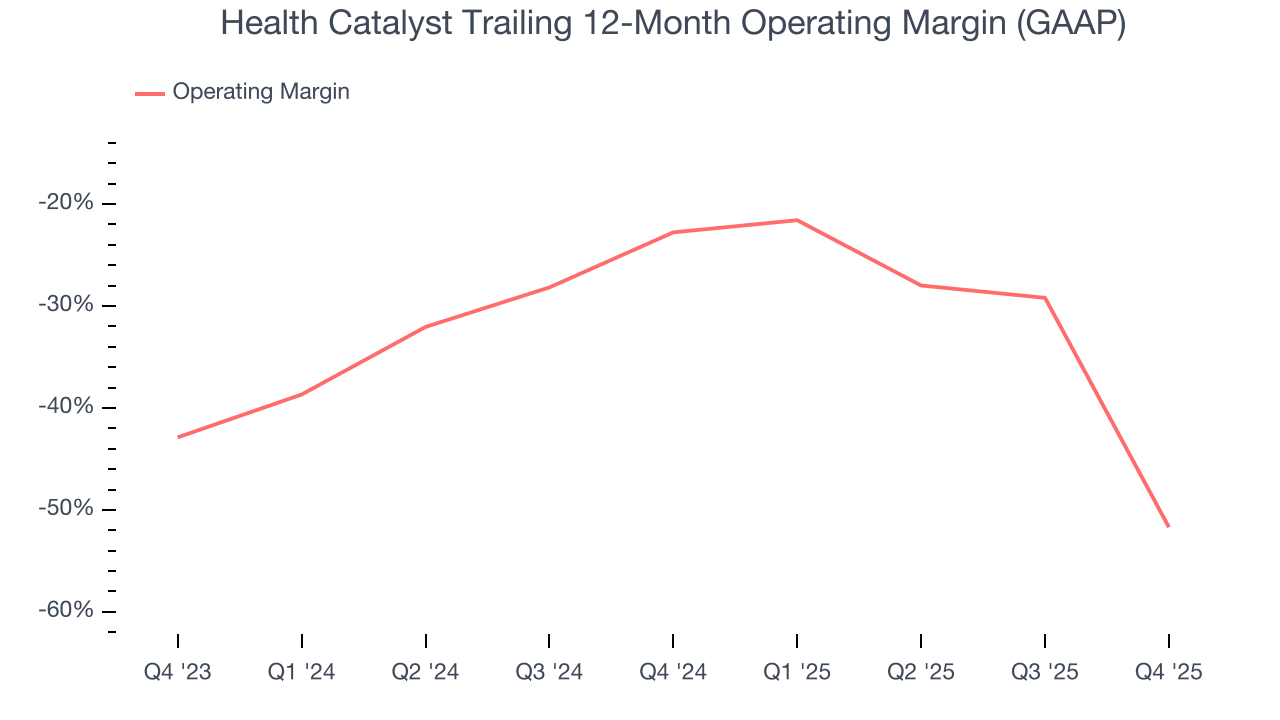

8. Operating Margin

Health Catalyst’s expensive cost structure has contributed to an average operating margin of negative 51.7% over the last year. Unprofitable software companies require extra attention because they spend heaps of money to capture market share. As seen in its historically underwhelming revenue performance, this strategy hasn’t worked so far, and it’s unclear what would happen if Health Catalyst reeled back its investments. Wall Street seems to think it will face some obstacles, and we tend to agree.

Looking at the trend in its profitability, Health Catalyst’s operating margin decreased by 28.9 percentage points over the last two years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Health Catalyst’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

In Q4, Health Catalyst generated a negative 115% operating margin. The company's consistent lack of profits raise a flag.

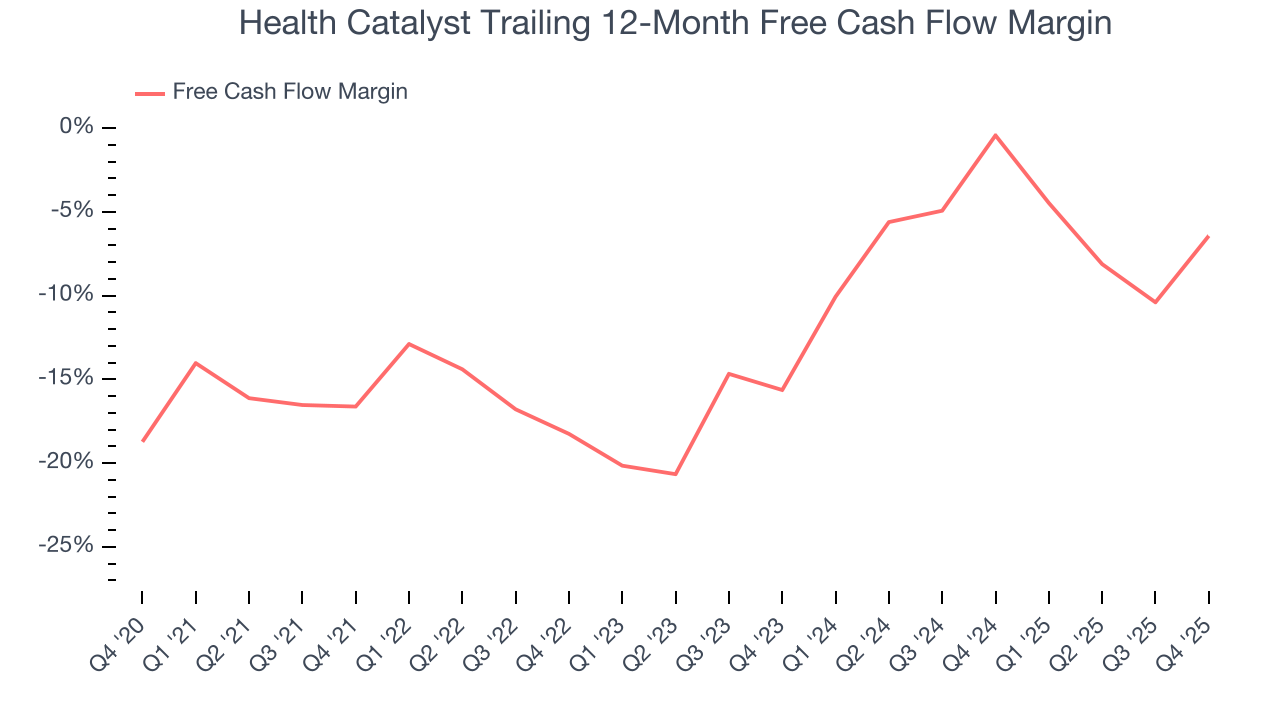

9. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

While Health Catalyst posted positive free cash flow this quarter, the broader story hasn’t been so clean. Health Catalyst’s demanding reinvestments have drained its resources over the last year, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 6.4%, meaning it lit $6.43 of cash on fire for every $100 in revenue.

Health Catalyst’s free cash flow clocked in at $4.50 million in Q4, equivalent to a 6% margin. Its cash flow turned positive after being negative in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, causing temporary swings. Long-term trends trump fluctuations.

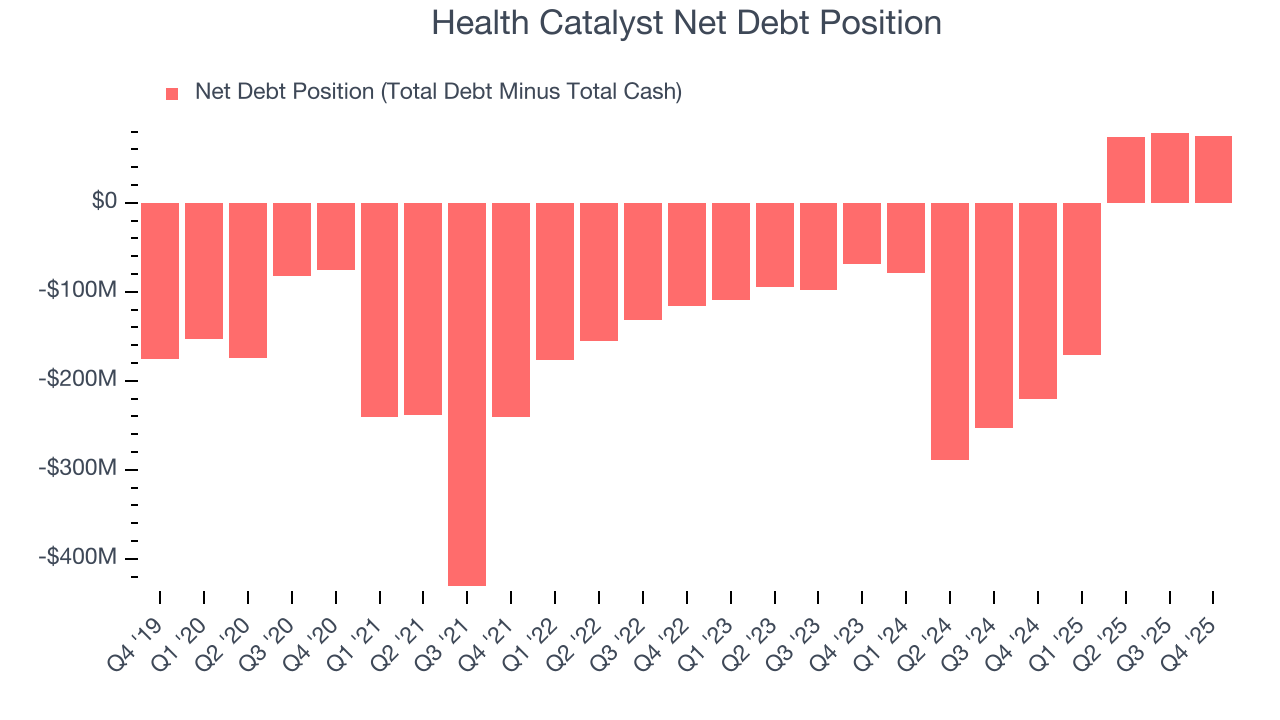

10. Balance Sheet Assessment

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

Health Catalyst burned through $20.02 million of cash over the last year. Although the company has $171.2 million of debt on its balance sheet, we think its $95.73 million of cash gives it enough runway (we typically look for at least two years) to prioritize growth over profitability.

11. Key Takeaways from Health Catalyst’s Q4 Results

It was encouraging to see Health Catalyst beat analysts’ EBITDA expectations this quarter. On the other hand, its revenue guidance for next quarter missed and its EBITDA guidance for next quarter fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 10.4% to $1.60 immediately after reporting.

12. Is Now The Time To Buy Health Catalyst?

Updated: March 13, 2026 at 10:21 PM EDT

A common mistake we notice when investors are deciding whether to buy a stock or not is that they simply look at the latest earnings results. Business quality and valuation matter more, so we urge you to understand these dynamics as well.

We cheer for all companies solving complex business issues, but in the case of Health Catalyst, we’ll be cheering from the sidelines. For starters, its revenue growth was uninspiring over the last five years, and analysts expect its demand to deteriorate over the next 12 months. On top of that, Health Catalyst’s declining operating margin shows it’s becoming less efficient at building and selling its software, and its operating margins reveal poor profitability compared to other software companies.

Health Catalyst’s price-to-sales ratio based on the next 12 months is 0.5x. While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $2.84 on the company (compared to the current share price of $1.33).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.