Lucid (LCID)

Lucid catches our eye, but its cash burn shows it only has 5 months of runway left.― StockStory Analyst Team

1. News

2. Summary

Why Lucid Is Not Exciting

Founded by a former Tesla Vice President, Lucid Group (NASDAQ:LCID) designs, manufactures, and sells luxury electric vehicles with long-range capabilities.

- Negative 138% gross margin means it loses money on every sale and must pivot or scale quickly to survive

- Historical operating margin losses point to an inefficient cost structure

- Unfavorable liquidity position could lead to additional equity financing that dilutes shareholders

Lucid shows some promise. However, we wouldn’t buy the stock until its EBITDA can comfortably service its debt.

Why There Are Better Opportunities Than Lucid

Lucid is trading at $10.27 per share, or 1.4x forward price-to-sales. The market typically values companies like Lucid based on their anticipated profits for the next 12 months, but it expects the business to lose money. We also think the upside isn’t great compared to the potential downside here - there are more exciting stocks to buy.

We’d rather pay up for companies with elite fundamentals than get a decent price on a poor one. High-quality businesses often have more durable earnings power, helping us sleep well at night.

3. Lucid (LCID) Research Report: Q4 CY2025 Update

Luxury electric car manufacturer Lucid (NASDAQ:LCID) announced better-than-expected revenue in Q4 CY2025, with sales up 123% year on year to $522.7 million. Its non-GAAP loss of $3.08 per share was 15.2% below analysts’ consensus estimates.

Lucid (LCID) Q4 CY2025 Highlights:

- Revenue: $522.7 million vs analyst estimates of $445.5 million (123% year-on-year growth, 17.3% beat)

- Adjusted EPS: -$3.08 vs analyst expectations of -$2.67 (15.2% miss)

- Adjusted EBITDA: -$874.7 million (-167% margin, 51.5% year-on-year decline)

- Adjusted EBITDA Margin: -167%, up from -246% in the same quarter last year

- Free Cash Flow was -$1.24 billion compared to -$824.8 million in the same quarter last year

- Sales Volumes rose 72% year on year (79% in the same quarter last year)

- Market Capitalization: $3.06 billion

Company Overview

Founded by a former Tesla Vice President, Lucid Group (NASDAQ:LCID) designs, manufactures, and sells luxury electric vehicles with long-range capabilities.

The company was founded in 2007 as Atieva, initially focusing on battery technology and electric powertrains for other automakers. In 2016, the company rebranded as Lucid Motors, shifting its focus to luxury electric vehicles. Led by former Tesla executive Peter Rawlinson as CEO, Lucid went public in 2021 via a merger with Churchill Capital Corp IV, a special purpose acquisition company (SPAC).

Lucid’s product portfolio is centered around luxury electric sedans, with its flagship model being the Lucid Air, which is positioned to compete with high-end EVs like Tesla's Model S. The Lucid Air boasts an EPA-estimated range of 500+ miles on a single charge. The company takes a vertically integrated approach to manufacturing its vehicles, giving it control over its technology roadmap while ensuring quality and potentially higher margins at scale. The company currently operates manufacturing facilities in Arizona and Saudi Arabia.

Lucid primarily generates revenue through direct sales of its electric vehicles to consumers, both online and through its own retail "Studios." This direct-to-consumer model allows Lucid to capture full retail value and control the customer experience. Additional revenue streams include vehicle leasing through Lucid Financial Services, technology sales to other automakers, and potential sales of regulatory credits.

4. Automobile Manufacturing

Much capital investment and technical know-how are needed to manufacture functional, safe, and aesthetically pleasing automobiles for the mass market. Barriers to entry are therefore high, and auto manufacturers with economies of scale can boast strong economic moats. However, this doesn’t insulate them from new entrants, as electric vehicles (EVs) have entered the market and are upending it. This has forced established manufacturers to not only contend with emerging EV-first competitors but also decide how much they want to invest in these disruptive technologies, which will likely cannibalize their legacy offerings.

Lucid's competitors in the electric vehicle market include Tesla (NASDAQ:TSLA), Rivian (NASDAQ:RIVN), Porsche's Electric Division (XETRA:PAH3), and Mercedes-Benz Group's EV Division (OTC:MBGAF).

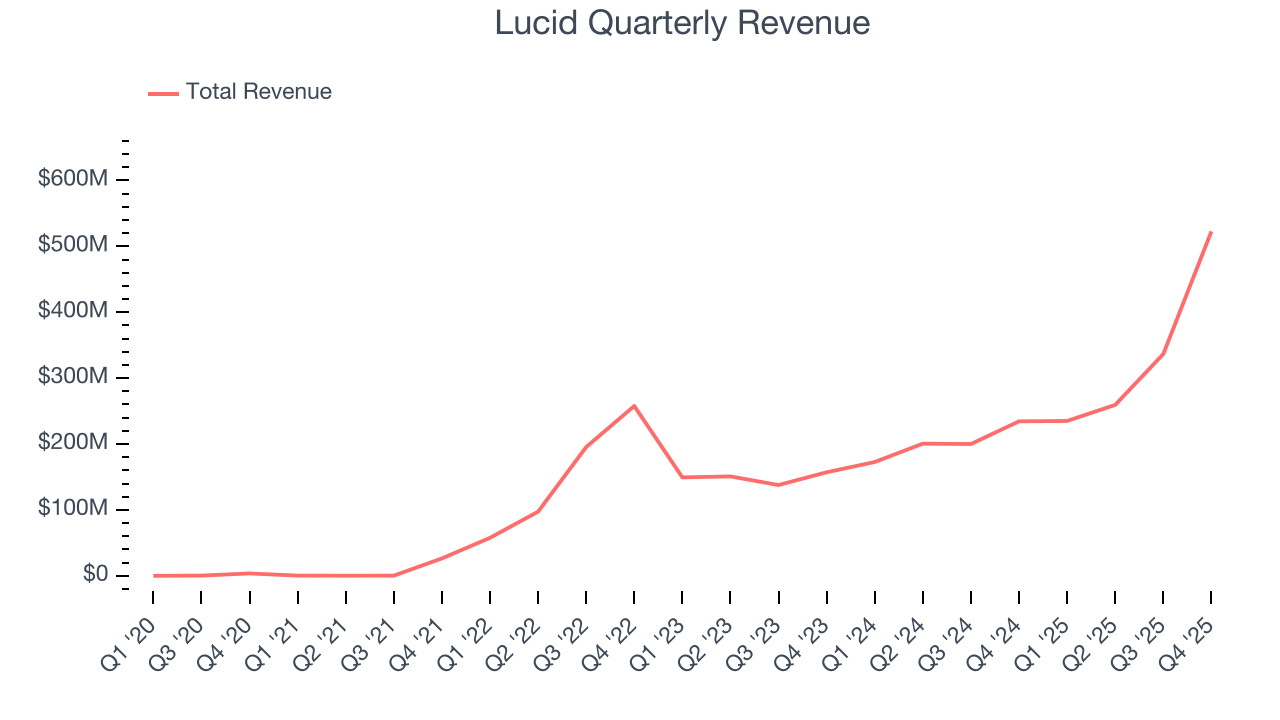

5. Revenue Growth

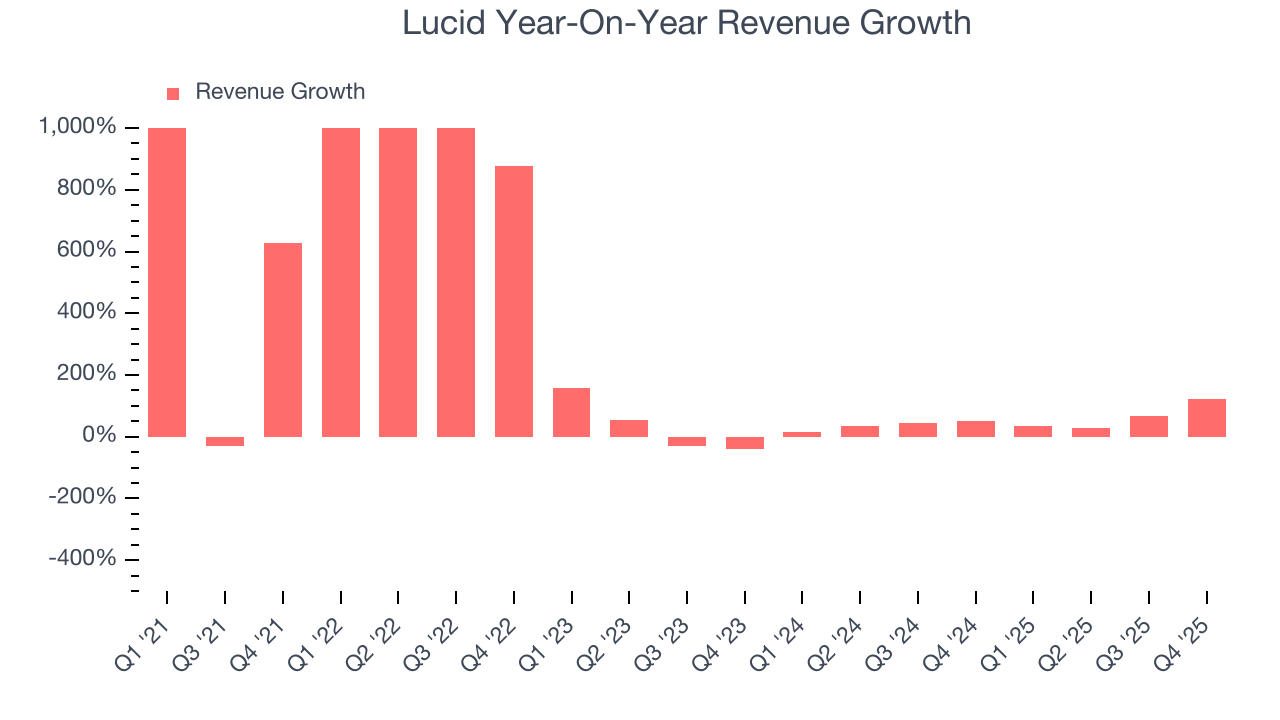

A company’s long-term sales performance can indicate its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Thankfully, Lucid’s 208% annualized revenue growth over the last five years was incredible. Its growth beat the average industrials company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Lucid’s annualized revenue growth of 50.8% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

We can dig further into the company’s revenue dynamics by analyzing its number of units sold, which reached 5,345 in the latest quarter. Over the last two years, Lucid’s units sold grew by 47.2% annually. Because this number is lower than its revenue growth, we can see the company benefited from price increases.

This quarter, Lucid reported magnificent year-on-year revenue growth of 123%, and its $522.7 million of revenue beat Wall Street’s estimates by 17.3%.

Looking ahead, sell-side analysts expect revenue to grow 89.2% over the next 12 months, an improvement versus the last two years. This projection is eye-popping and suggests its newer products and services will spur better top-line performance.

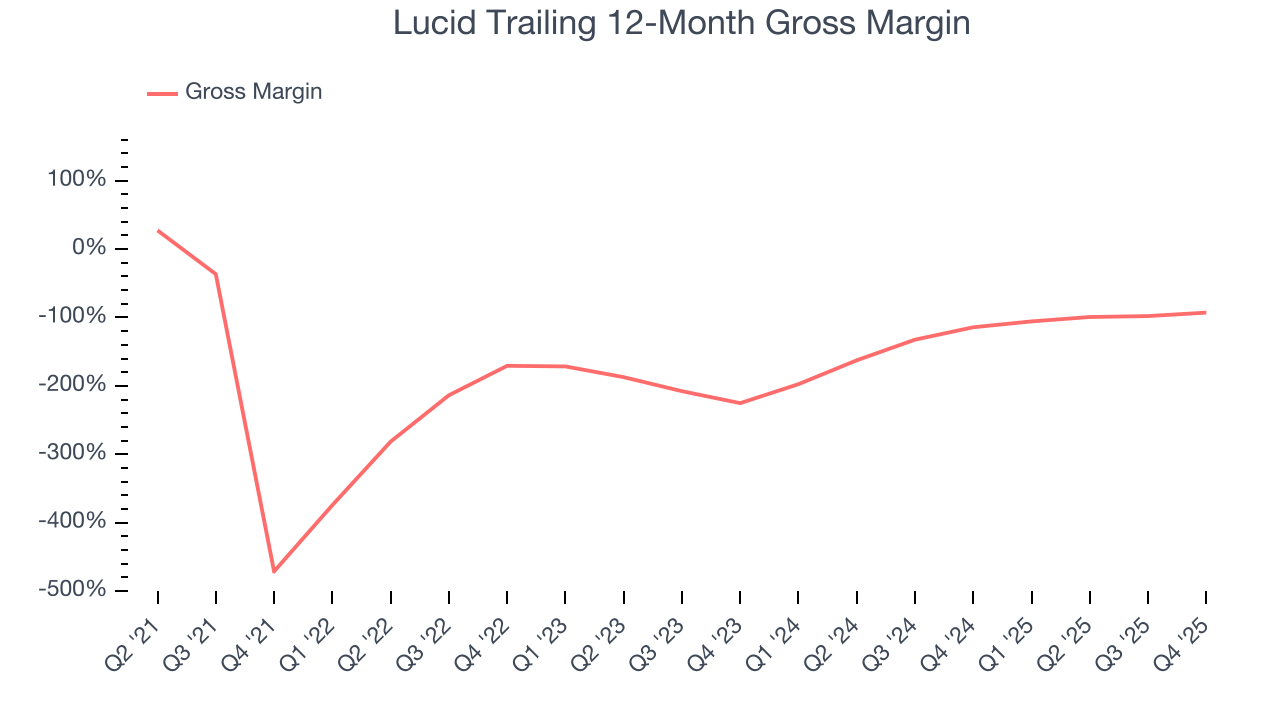

6. Gross Margin & Pricing Power

All else equal, we prefer higher gross margins because they usually indicate that a company sells more differentiated products and commands stronger pricing power.

Lucid has bad unit economics for an industrials business, signaling it operates in a competitive market. This is also because it’s an automobile manufacturer.

Automobile manufacturers have structurally lower profitability as they often break even on the initial sale of vehicles and instead make money on parts and servicing, which come many years later - this explains why new entrants whose fleets are too young to generate substantial aftermarket revenues have negative gross margins. As you can see below, these dynamics culminated in an average negative 138% gross margin for Lucid over the last five years.

This quarter, Lucid’s gross profit margin was negative 80.7%. The company’s full-year margin was also negative, suggesting it needs to change its business model quickly.

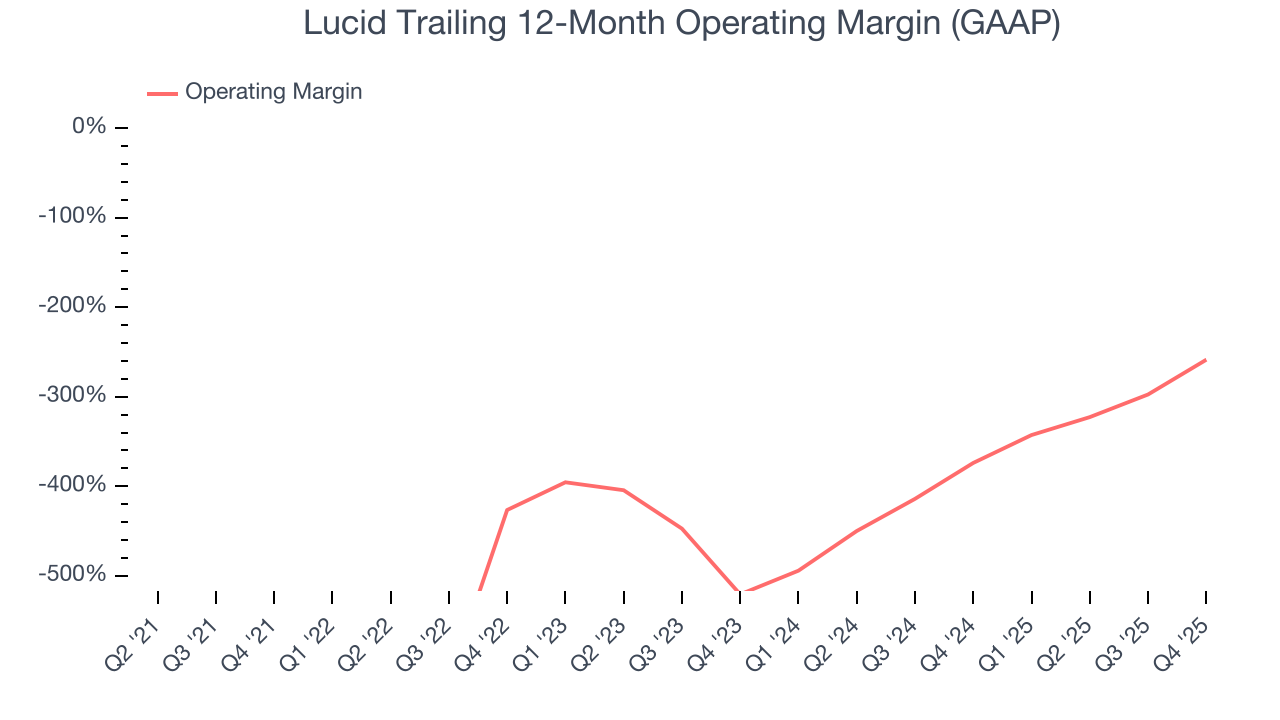

7. Operating Margin

Lucid’s high expenses have contributed to an average operating margin of negative 405% over the last five years. Unprofitable industrials companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

On the plus side, Lucid’s operating margin rose over the last five years, as its sales growth gave it operating leverage. Still, it will take much more for the company to reach long-term profitability.

In Q4, Lucid generated a negative 204% operating margin.

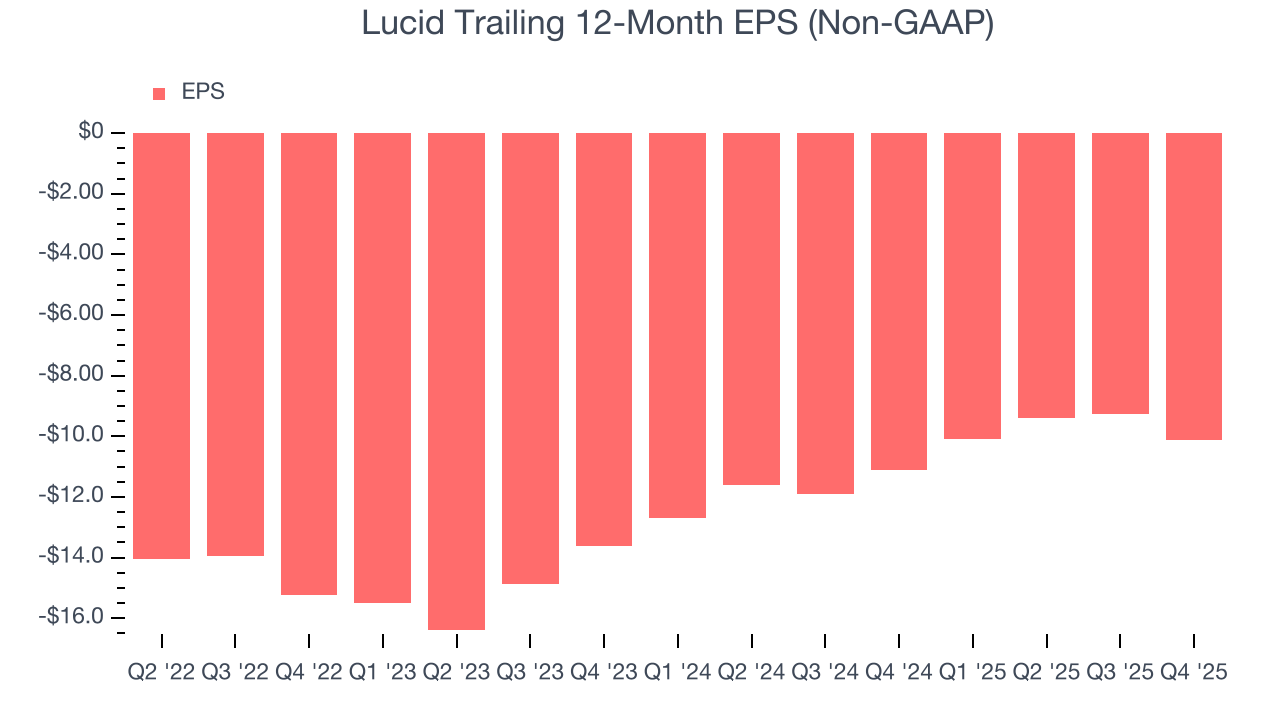

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Although Lucid’s full-year earnings are still negative, it reduced its losses and improved its EPS by 5.1% annually over the last four years. The next few quarters will be critical for assessing its long-term profitability. We hope to see an inflection point soon.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Lucid, its two-year annual EPS growth of 13.7% was higher than its four-year trend. Its improving earnings is an encouraging data point, but a caveat is that its EPS is still in the red.

In Q4, Lucid reported adjusted EPS of negative $3.08, down from negative $2.20 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects Lucid to improve its earnings losses. Analysts forecast its full-year EPS of negative $10.13 will advance to negative $7.55.

9. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Lucid’s demanding reinvestments have drained its resources over the last five years, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 439%, meaning it lit $438.79 of cash on fire for every $100 in revenue.

Taking a step back, an encouraging sign is that Lucid’s margin expanded during that time. In light of its glaring cash burn, however, this improvement is a bucket of hot water in a cold ocean.

Lucid burned through $1.24 billion of cash in Q4, equivalent to a negative 238% margin. The company’s cash burn increased from $824.8 million of lost cash in the same quarter last year.

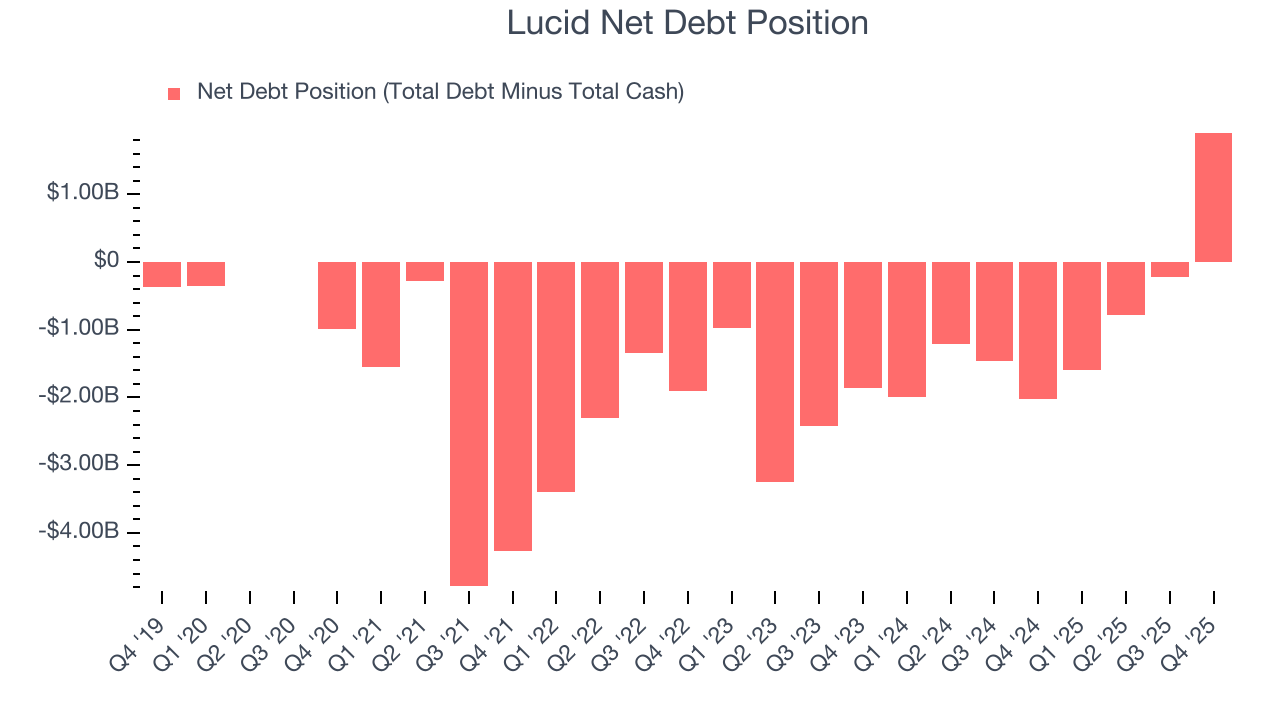

10. Balance Sheet Risk

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

Lucid burned through $3.8 billion of cash over the last year, and its $2.91 billion of debt exceeds the $997.8 million of cash on its balance sheet. This is a deal breaker for us because indebted loss-making companies spell trouble.

Unless the Lucid’s fundamentals change quickly, it might find itself in a position where it must raise capital from investors to continue operating. Whether that would be favorable is unclear because dilution is a headwind for shareholder returns.

We remain cautious of Lucid until it generates consistent free cash flow or any of its announced financing plans materialize on its balance sheet.

11. Key Takeaways from Lucid’s Q4 Results

We were impressed by how significantly Lucid blew past analysts’ revenue expectations this quarter. On the other hand, its EBITDA missed and its EPS fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 6.4% to $9.33 immediately after reporting.

12. Is Now The Time To Buy Lucid?

Updated: March 17, 2026 at 11:19 PM EDT

Before making an investment decision, investors should account for Lucid’s business fundamentals and valuation in addition to what happened in the latest quarter.

Aside from its balance sheet, Lucid is a pretty good company. For starters, its revenue growth was exceptional over the last five years. And while its operating margins reveal poor profitability compared to other industrials companies, its rising cash profitability gives it more optionality. Additionally, Lucid’s expanding operating margin shows the business has become more efficient.

Lucid’s forward price-to-sales ratio is 1.4x. Certain aspects of its fundamentals are attractive, but we aren’t investing at the moment because its balance sheet makes us uneasy. Interested in this company and its prospects? We recommend you wait until its debt load falls or its profits increase.

Wall Street analysts have a consensus one-year price target of $13.95 on the company (compared to the current share price of $10.27).