Lincoln Educational (LINC)

We wouldn’t buy Lincoln Educational. Its sales have underperformed and its low returns on capital show it has few growth opportunities.― StockStory Analyst Team

1. News

2. Summary

Why We Think Lincoln Educational Will Underperform

Established in 1946, Lincoln Educational (NASDAQ:LINC) is a provider of specialized technical training in the United States, offering career-oriented programs to provide practical skills required in the workforce.

- Annual revenue growth of 12.1% over the last five years was below our standards for the consumer discretionary sector

- Earnings per share fell by 15.5% annually over the last five years while its revenue grew, showing its incremental sales were much less profitable

- Subpar operating margin constrains its ability to invest in process improvements or effectively respond to new competitive threats

Lincoln Educational falls short of our expectations. We’d rather invest in businesses with stronger moats.

Why There Are Better Opportunities Than Lincoln Educational

Lincoln Educational’s stock price of $39.61 implies a valuation ratio of 52.7x forward P/E. This valuation multiple seems a bit much considering the tepid revenue growth profile.

There are stocks out there featuring similar valuation multiples with better fundamentals. We prefer to invest in those.

3. Lincoln Educational (LINC) Research Report: Q4 CY2025 Update

Education company Lincoln Educational (NASDAQ:LINC) reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 19.7% year on year to $142.9 million. The company’s full-year revenue guidance of $585 million at the midpoint came in 5.4% above analysts’ estimates. Its GAAP profit of $0.40 per share was 17.6% above analysts’ consensus estimates.

Lincoln Educational (LINC) Q4 CY2025 Highlights:

- Revenue: $142.9 million vs analyst estimates of $133.6 million (19.7% year-on-year growth, 6.9% beat)

- EPS (GAAP): $0.40 vs analyst estimates of $0.34 (17.6% beat)

- Adjusted EBITDA: $29.08 million vs analyst estimates of $27.53 million (20.4% margin, 5.6% beat)

- EPS (GAAP) guidance for the upcoming financial year 2026 is $0.69 at the midpoint, missing analyst estimates by 9.5%

- EBITDA guidance for the upcoming financial year 2026 is $74 million at the midpoint, above analyst estimates of $69.8 million

- Operating Margin: 12.4%, up from 9.2% in the same quarter last year

- Free Cash Flow Margin: 17.5%, up from 4.6% in the same quarter last year

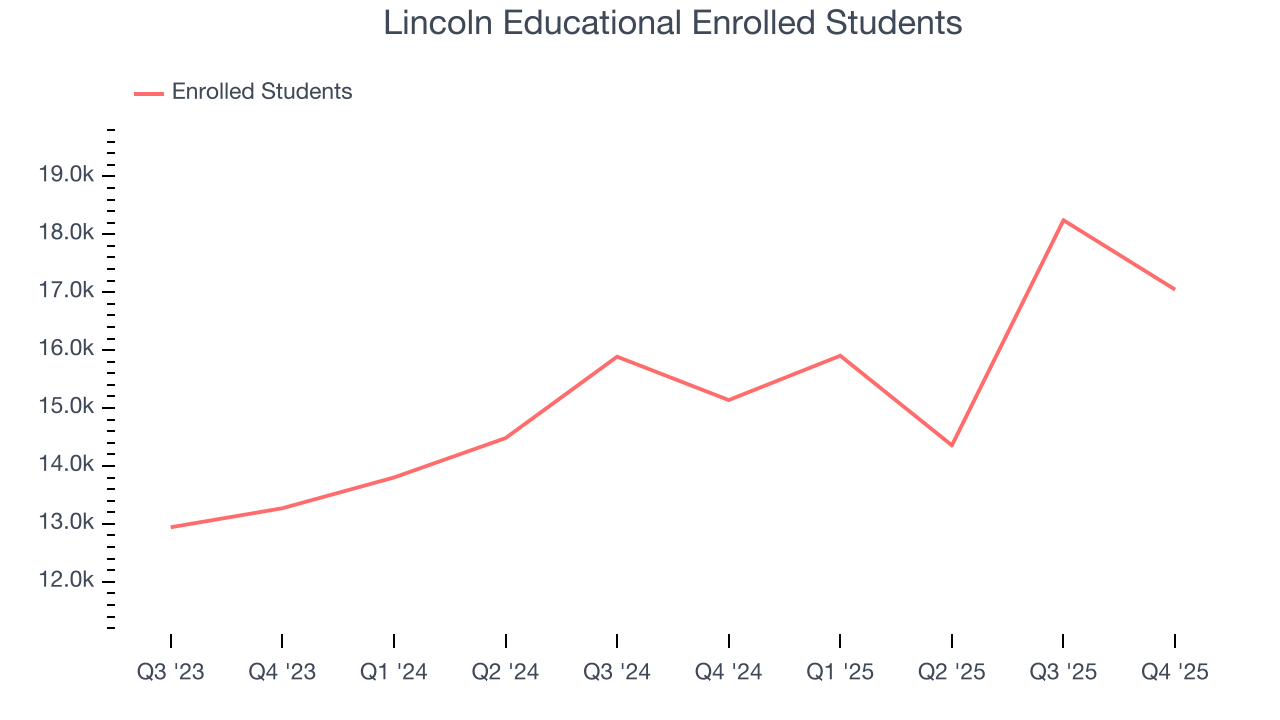

- Enrolled Students: 17,046, up 1,908 year on year

- Market Capitalization: $948.4 million

Company Overview

Established in 1946, Lincoln Educational (NASDAQ:LINC) is a provider of specialized technical training in the United States, offering career-oriented programs to provide practical skills required in the workforce.

The company primarily operates through Lincoln Technical Institute, Lincoln College of Technology, and Euphoria Institute of Beauty Arts and Sciences. These institutions are spread across 14 states and offer a variety of diploma, degree, and certificate programs.

Lincoln Educational focuses on five core areas: Automotive Technology, Health Sciences, Skilled Trades, Hospitality Services, and Business and IT. Each program is designed to equip students with hands-on experience and skills relevant to their chosen field.

Automotive and Skilled Trades programs partner with leading companies, ensuring students receive education aligned with industry standards and have access to advanced technologies. Partnerships with companies like Audi and BMW not only enhance the curriculum but also create pathways for student internships and employment.

In the Health Sciences sector, Lincoln Education offers programs in Nursing, Medical Assistant, Dental Assistant, and other allied health professions. The Euphoria Institute focuses on beauty and wellness programs, providing training in cosmetology, esthetics, and massage therapy.

Lincoln Educational places a strong emphasis on career services, assisting students with job searching, resume writing, and interview preparation.

4. Consumer Discretionary - Education Services

The Consumer Discretionary sector, by definition, is made up of companies selling non-essential goods and services. When economic conditions deteriorate or tastes shift, consumers can easily cut back or eliminate these purchases. For long-term investors with five-year holding periods, this creates a structural challenge: the sector is inherently hit-driven, with low switching costs and fickle customers. As a result, only a handful of companies can reliably grow demand and compound earnings over long periods, which is why our bar is high and High Quality ratings are rare.

Education services companies provide postsecondary instruction, professional certifications, test preparation, and corporate training, both online and in-person. Tailwinds include lifelong-learning demand driven by rapid technological change, employer-sponsored upskilling programs, and growing acceptance of online credentials. Headwinds are substantial: heavy regulatory oversight—particularly around student-loan eligibility and enrollment practices—can abruptly alter business models. Reputational risk from scrutiny over student outcomes and debt burdens constrains marketing strategies. Competition from free or low-cost digital alternatives (MOOCs, employer-built academies) pressures pricing.

Lincoln Educational's primary competitors include Universal Technical Institute (NYSE:UTI), Strayer Education (NASDAQ:STRA), Adtalem Global Education (NYSE:ATGE), and Grand Canyon Education (NASDAQ:LOPE).

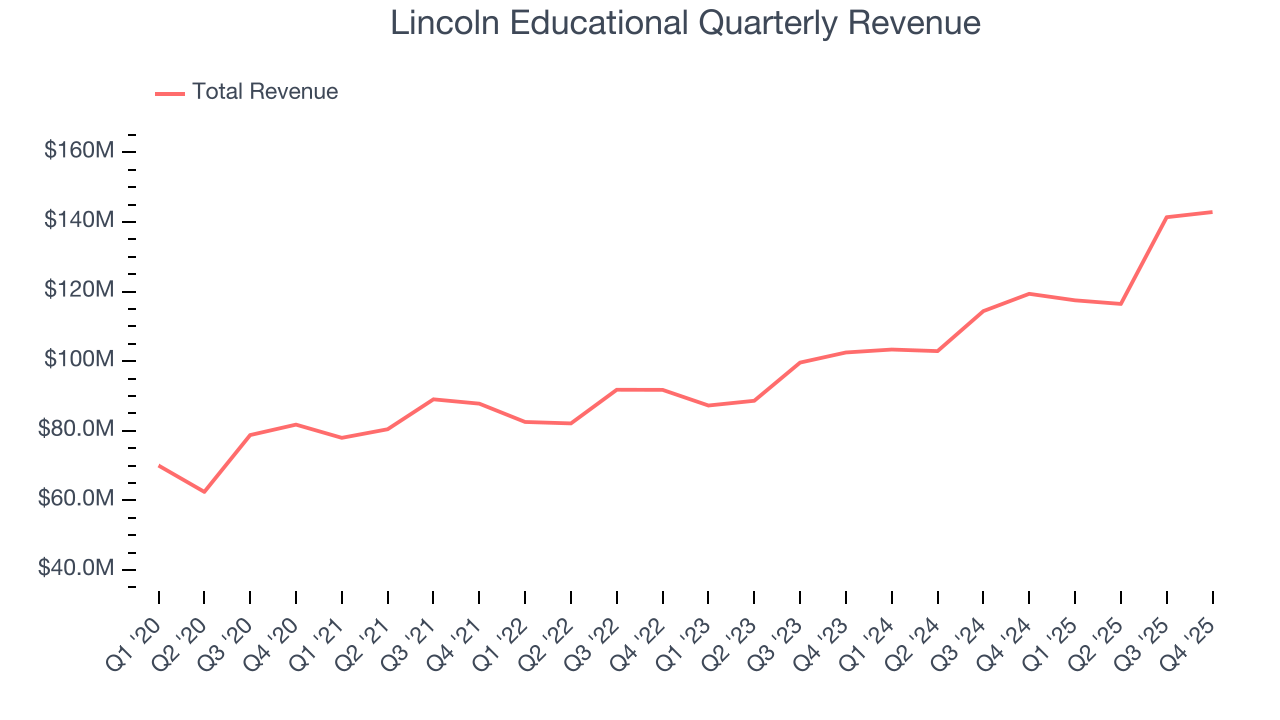

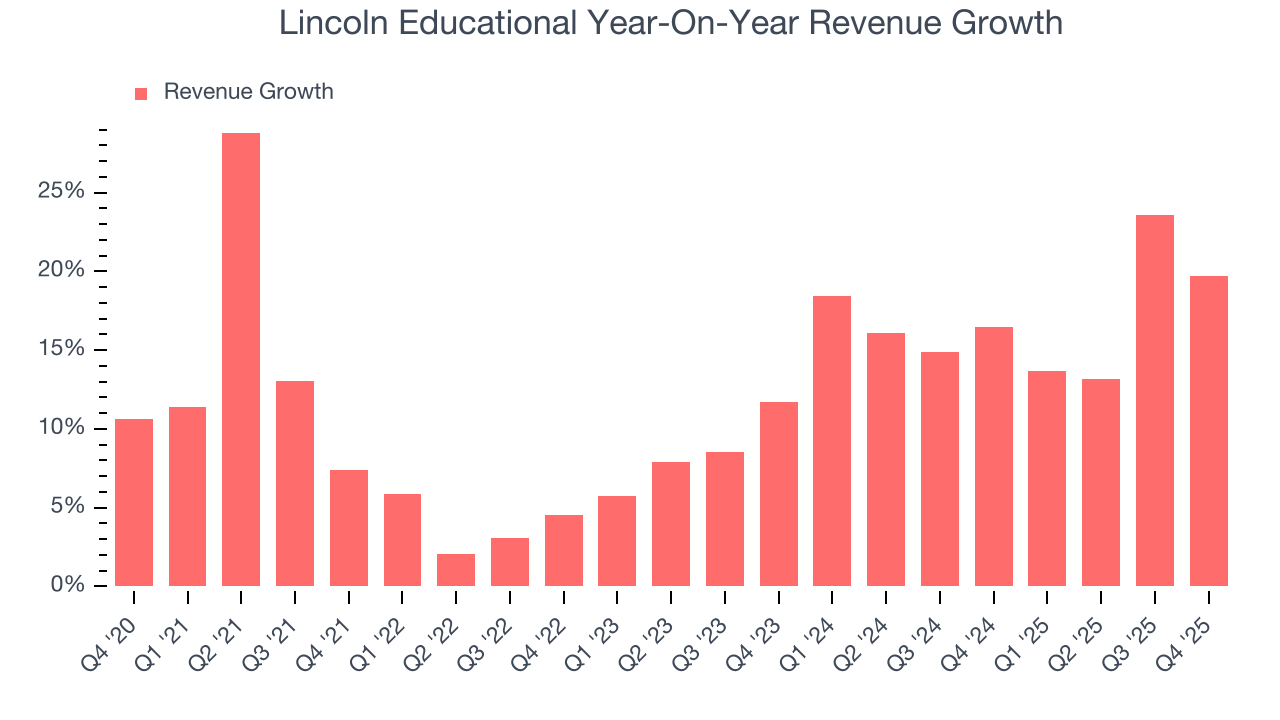

5. Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Over the last five years, Lincoln Educational grew its sales at a 12.1% compounded annual growth rate. Though this growth is acceptable on an absolute basis, we need to see more than just topline growth for the consumer discretionary sector, which can display significant earnings volatility. This means our bar for the sector is particularly high, reflecting the non-essential and hit-driven nature of the products and services offered. Additionally, five-year CAGR starts around Covid, when revenue was depressed then rebounded.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Lincoln Educational’s annualized revenue growth of 17.1% over the last two years is above its five-year trend, which is encouraging.

Lincoln Educational also discloses its number of enrolled students, which reached 17,046 in the latest quarter. Over the last two years, Lincoln Educational’s enrolled students averaged 13.1% year-on-year growth. Because this number is lower than its revenue growth during the same period, we can see the company’s monetization has risen.

This quarter, Lincoln Educational reported year-on-year revenue growth of 19.7%, and its $142.9 million of revenue exceeded Wall Street’s estimates by 6.9%.

Looking ahead, sell-side analysts expect revenue to grow 7.6% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and implies its products and services will face some demand challenges.

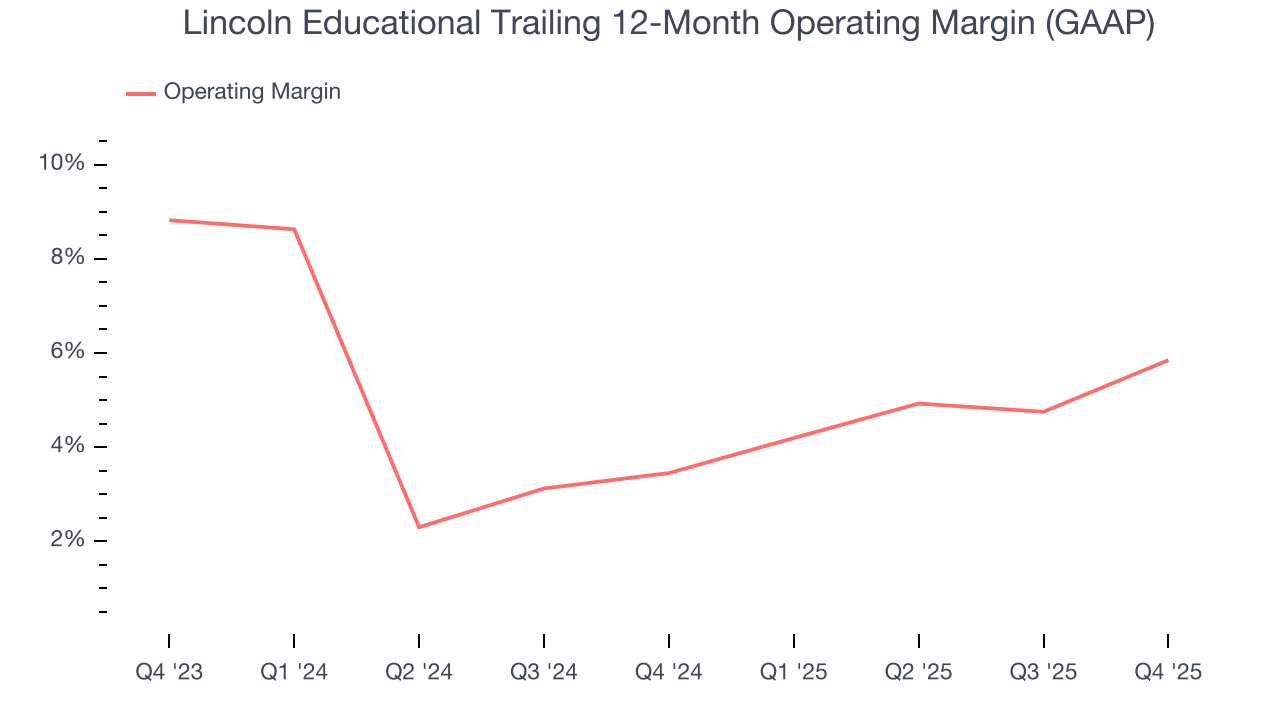

6. Operating Margin

Lincoln Educational’s operating margin has been trending up over the last 12 months and averaged 4.7% over the last two years. The company’s higher efficiency is a breath of fresh air, but its suboptimal cost structure means it still sports inadequate profitability for a consumer discretionary business.

This quarter, Lincoln Educational generated an operating margin profit margin of 12.4%, up 3.3 percentage points year on year. This increase was a welcome development and shows it was more efficient.

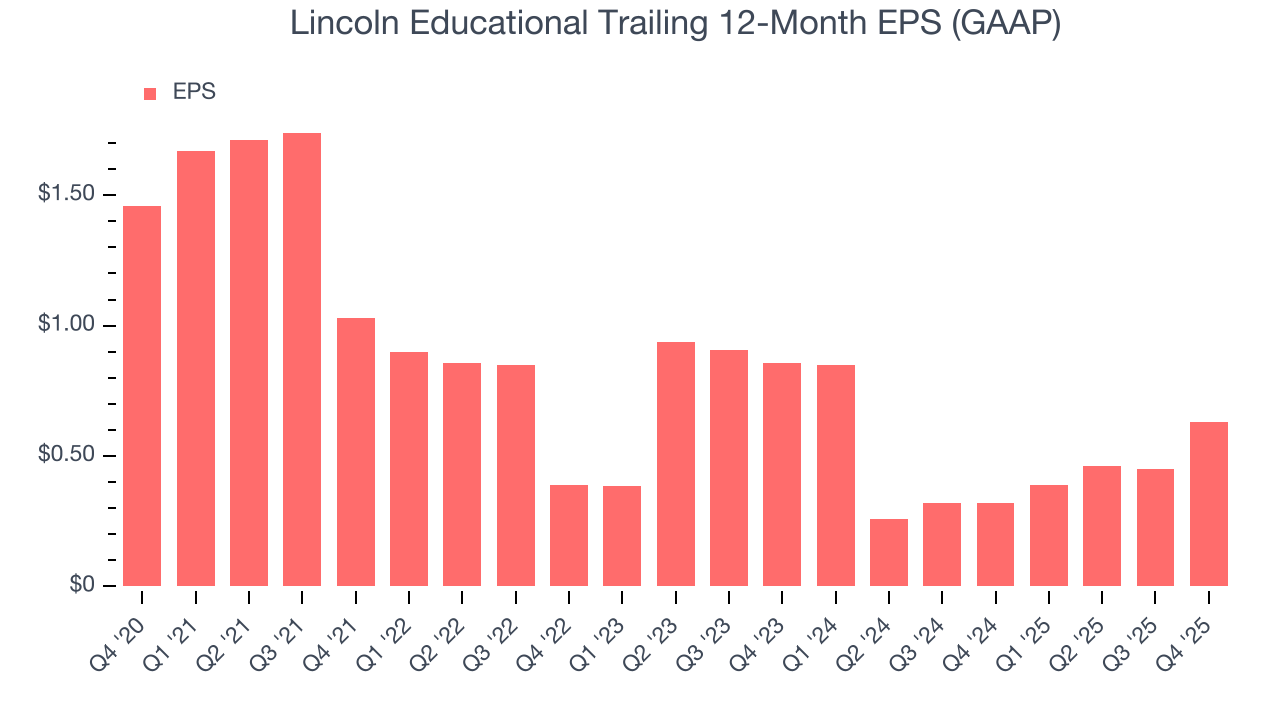

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Lincoln Educational, its EPS declined by 15.5% annually over the last five years while its revenue grew by 12.1%. This tells us the company became less profitable on a per-share basis as it expanded.

In Q4, Lincoln Educational reported EPS of $0.40, up from $0.22 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Lincoln Educational’s full-year EPS of $0.63 to grow 21%.

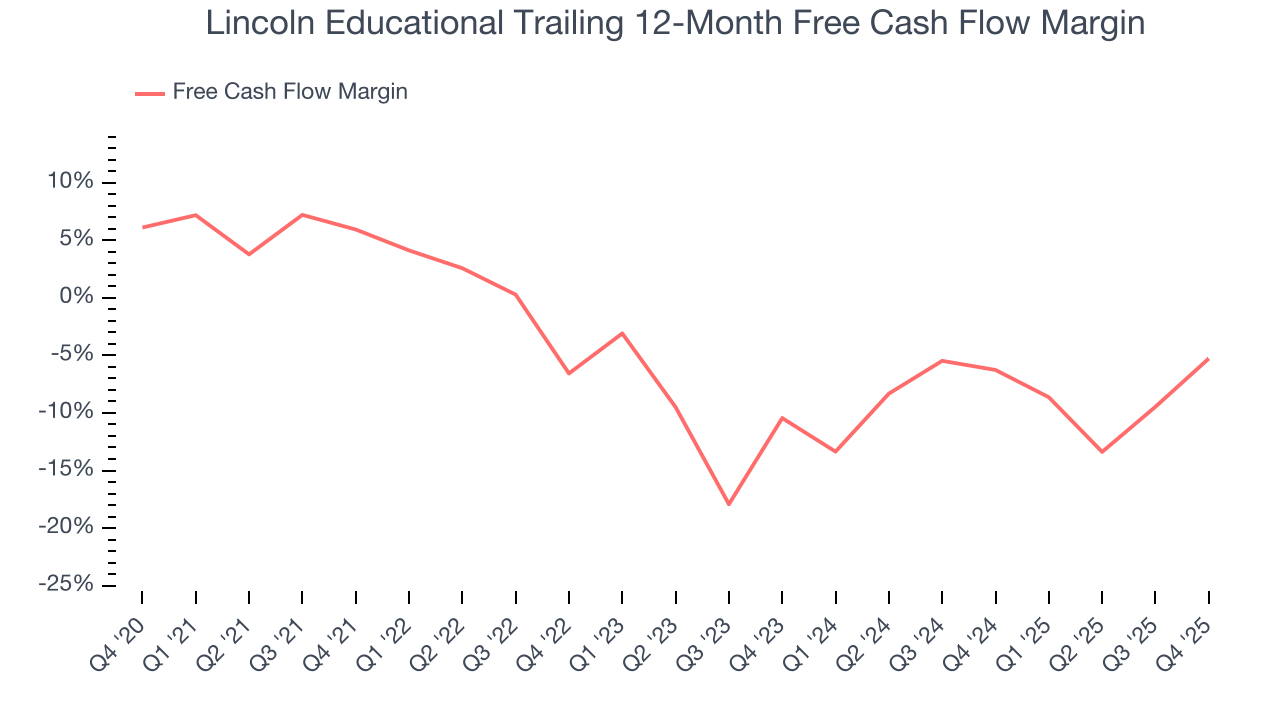

8. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

While Lincoln Educational posted positive free cash flow this quarter, the broader story hasn’t been so clean. Over the last two years, Lincoln Educational’s demanding reinvestments to stay relevant have drained its resources, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 5.7%, meaning it lit $5.73 of cash on fire for every $100 in revenue.

Lincoln Educational’s free cash flow clocked in at $25 million in Q4, equivalent to a 17.5% margin. This result was good as its margin was 12.9 percentage points higher than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, leading to temporary swings. Long-term trends trump fluctuations.

Looking forward, analysts predict Lincoln Educational will generate cash on a full-year basis. Their consensus estimates imply its free cash flow margin of negative 5.3% for the last 12 months will increase to positive 1.5%, giving it more optionality.

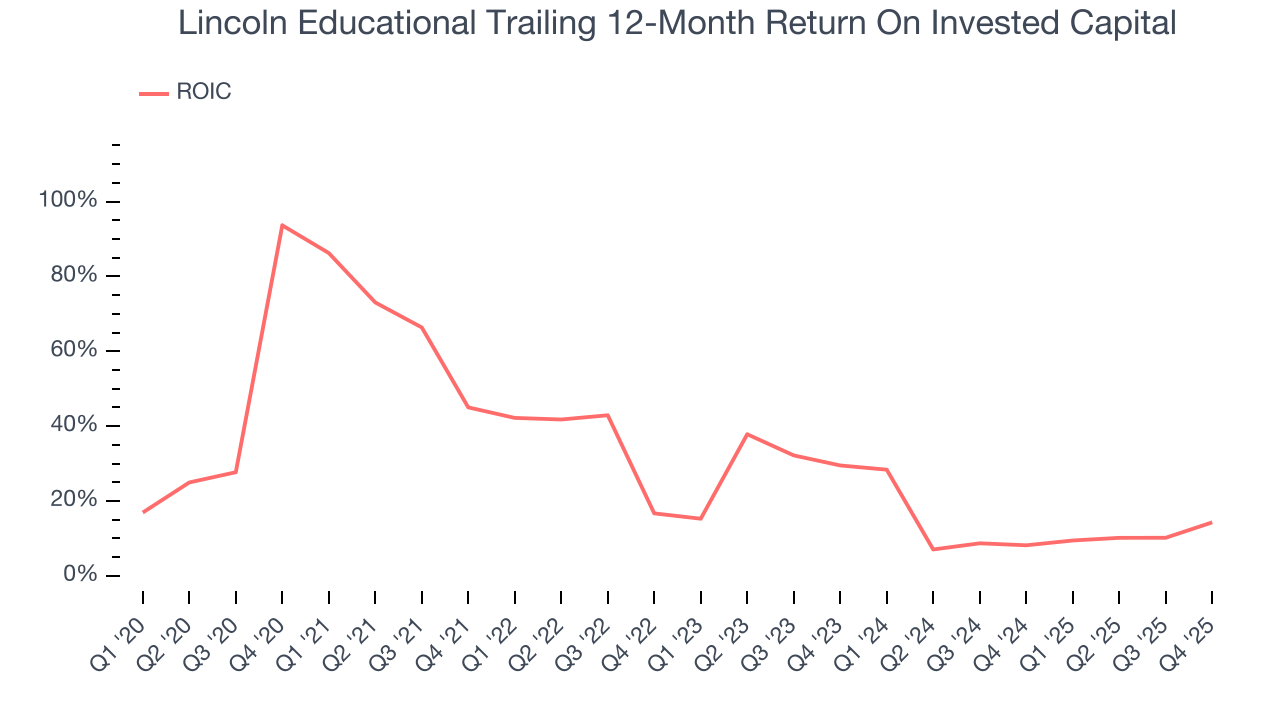

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Lincoln Educational historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 22.7%, somewhat low compared to the best consumer discretionary companies that consistently pump out 25%+.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Lincoln Educational’s ROIC has unfortunately decreased significantly. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

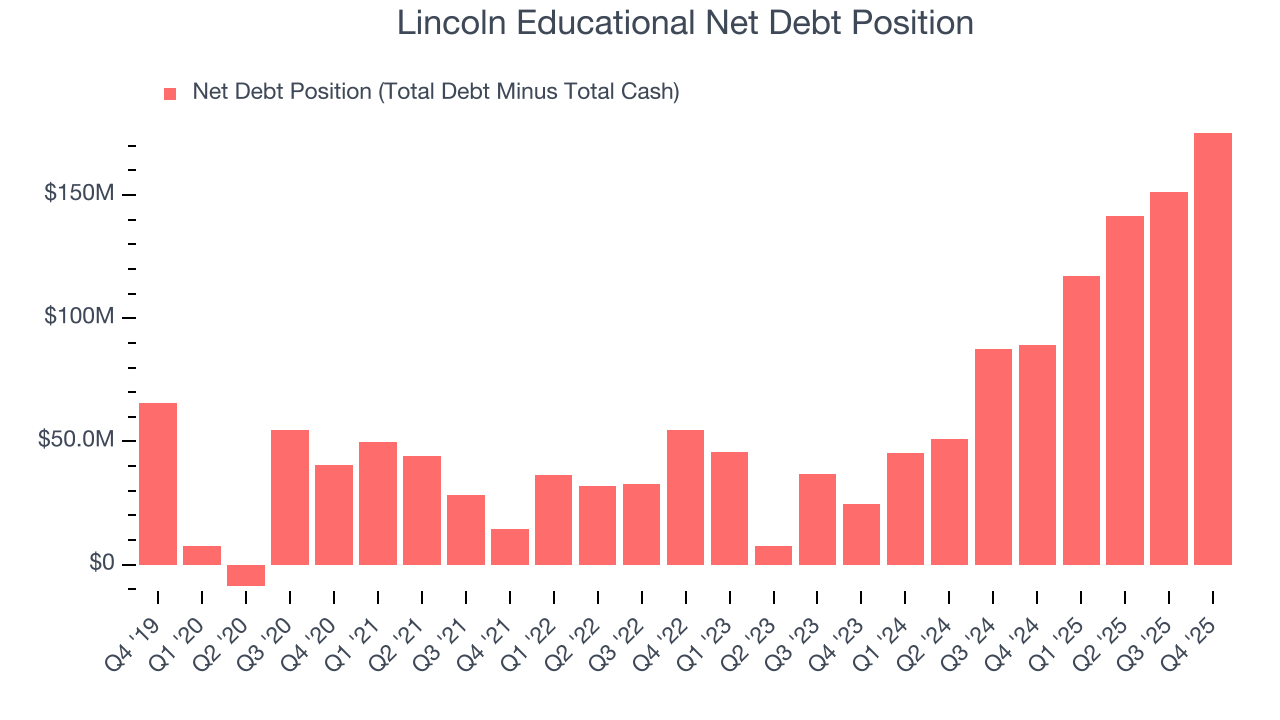

10. Balance Sheet Assessment

Lincoln Educational reported $28.52 million of cash and $203.9 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $67.13 million of EBITDA over the last 12 months, we view Lincoln Educational’s 2.6× net-debt-to-EBITDA ratio as safe. We also see its $1.49 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from Lincoln Educational’s Q4 Results

We were impressed by Lincoln Educational’s optimistic full-year revenue guidance, which blew past analysts’ expectations. We were also glad its revenue outperformed Wall Street’s estimates. Zooming out, we think this quarter featured some important positives. The stock remained flat at $29.99 immediately following the results.

12. Is Now The Time To Buy Lincoln Educational?

Updated: March 23, 2026 at 10:05 PM EDT

When considering an investment in Lincoln Educational, investors should account for its valuation and business qualities as well as what’s happened in the latest quarter.

Lincoln Educational doesn’t pass our quality test. On top of that, Lincoln Educational’s number of enrolled students has disappointed, and its declining EPS over the last five years makes it a less attractive asset to the public markets.

Lincoln Educational’s P/E ratio based on the next 12 months is 52.7x. At this valuation, there’s a lot of good news priced in - we think there are better opportunities elsewhere.

Wall Street analysts have a consensus one-year price target of $44.40 on the company (compared to the current share price of $39.61).