Nature's Sunshine (NATR)

We’re cautious of Nature's Sunshine. Its weak sales growth and declining returns on capital show its demand and profits are shrinking.― StockStory Analyst Team

1. News

2. Summary

Why Nature's Sunshine Is Not Exciting

Started on a kitchen table in Utah, Nature’s Sunshine (NASDAQ:NATR) manufactures and sells nutritional and personal care products.

- Smaller revenue base of $480.1 million means it hasn’t achieved the economies of scale that some industry juggernauts enjoy

- Lackluster 4.4% annual revenue growth over the last three years indicates the company is losing ground to competitors

- A positive is that its differentiated product offerings are difficult to replicate at scale and result in a best-in-class gross margin of 72%

Nature's Sunshine’s quality is lacking. There’s a wealth of better opportunities.

Why There Are Better Opportunities Than Nature's Sunshine

Nature's Sunshine is trading at $24.48 per share, or 24.6x forward P/E. This multiple is higher than that of consumer staples peers; it’s also rich for the top-line growth of the company. Not a great combination.

There are stocks out there similarly priced with better business quality. We prefer owning these.

3. Nature's Sunshine (NATR) Research Report: Q4 CY2025 Update

Wellness products company Nature’s Sunshine (NASDAQ:NATR) reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 4.7% year on year to $123.8 million. The company’s full-year revenue guidance of $507.5 million at the midpoint came in 2.6% above analysts’ estimates. Its non-GAAP profit of $0.30 per share was 57.9% above analysts’ consensus estimates.

Nature's Sunshine (NATR) Q4 CY2025 Highlights:

- Revenue: $123.8 million vs analyst estimates of $121.6 million (4.7% year-on-year growth, 1.8% beat)

- Adjusted EPS: $0.30 vs analyst estimates of $0.19 (57.9% beat)

- Adjusted EBITDA: $11.93 million vs analyst estimates of $10.47 million (9.6% margin, 14% beat)

- EBITDA guidance for the upcoming financial year 2026 is $52 million at the midpoint, above analyst estimates of $51.22 million

- Operating Margin: 4.3%, in line with the same quarter last year

- Free Cash Flow Margin: 6.1%, down from 8.5% in the same quarter last year

- Market Capitalization: $439.7 million

Company Overview

Started on a kitchen table in Utah, Nature’s Sunshine (NASDAQ:NATR) manufactures and sells nutritional and personal care products.

Today, the company offers a broad portfolio of vitamins and supplements related to bone health, cellular health, cognitive function, joint health, and mood, among others. In addition, Nature’s Sunshine boasts a portfolio of personal care products such as lotion, aloe vera gel, herbal shampoo, and toothpaste.

The Nature’s Sunshine core customer is someone who cares about health and nutrition. These individuals are willing to spend a little extra to achieve their wellness goals, whether that is weight loss or improved overall health.

While Nature’s Sunshine products are available in some health stores, the company’s distribution largely relies on a multi-level marketing model. This means that individual customers who are passionate about the products sell directly to other end consumers. Given its multi-level marketing approach, Nature’s Sunshine customers are typically connected to someone who has had a good experience with the products.

However, many are skeptical about multi-level marketing approaches. Some say that these companies rely on recruitment to sustain themselves rather than actual demand for products, which could be very low.

4. Personal Care

While personal care products products may seem more discretionary than food, consumers tend to maintain or even boost their spending on the category during tough times. This phenomenon is known as "the lipstick effect" by economists, which states that consumers still want some semblance of affordable luxuries like beauty and wellness when the economy is sputtering. Consumer tastes are constantly changing, and personal care companies are currently responding to the public’s increased desire for ethically produced goods by featuring natural ingredients in their products.

Competitors offering health and wellness supplements and products include Herbalife (NYSE:HLF), USANA Health Sciences (NYSE:USNA), Bellring Brands (NYSE:BRBR), and The Simply Good Foods Company (NASDAQ:SMPL).

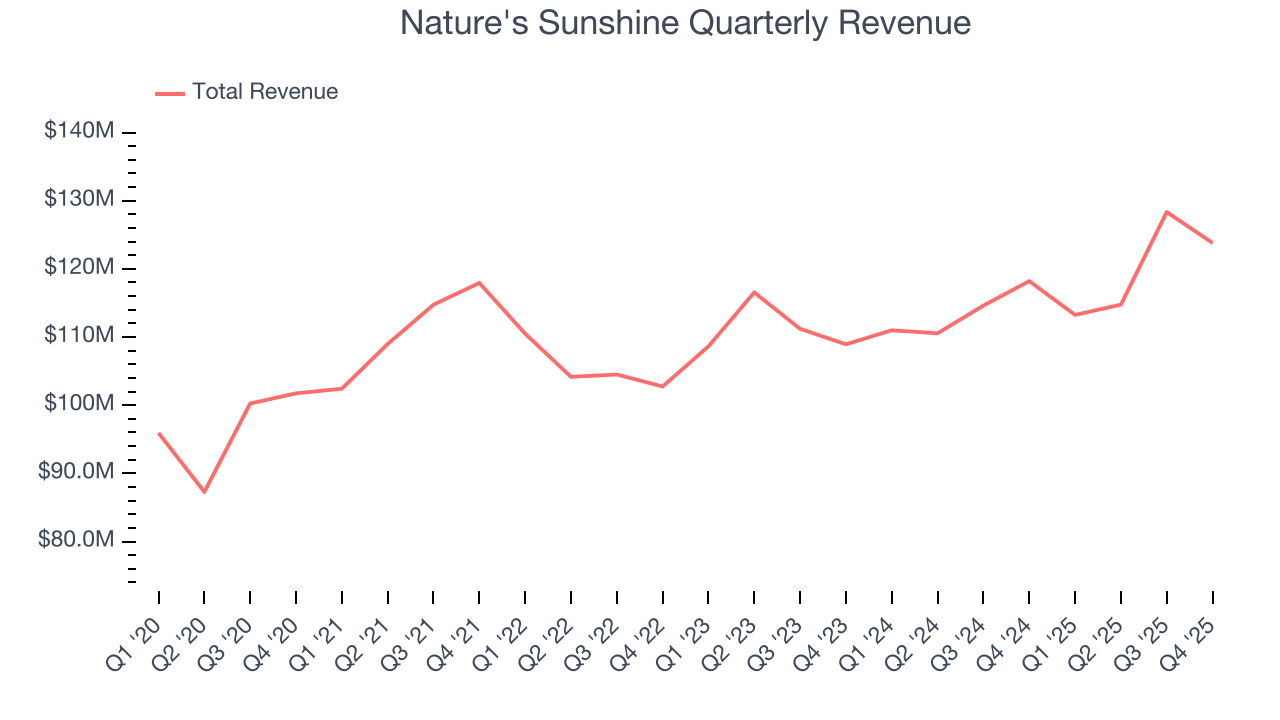

5. Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $480.1 million in revenue over the past 12 months, Nature's Sunshine is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers.

As you can see below, Nature's Sunshine’s sales grew at a tepid 4.4% compounded annual growth rate over the last three years. This shows it failed to generate demand in any major way and is a rough starting point for our analysis.

This quarter, Nature's Sunshine reported modest year-on-year revenue growth of 4.7% but beat Wall Street’s estimates by 1.8%.

Looking ahead, sell-side analysts expect revenue to grow 3.1% over the next 12 months, similar to its three-year rate. This projection doesn't excite us and indicates its products will see some demand headwinds.

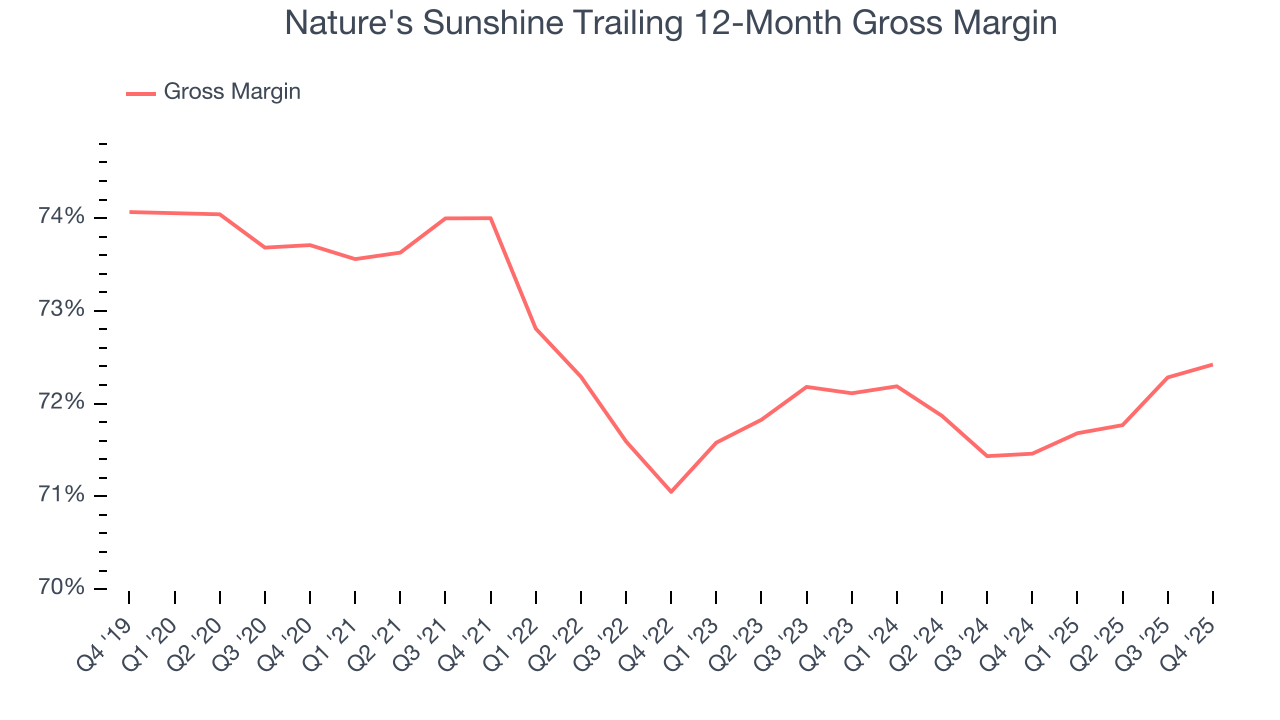

6. Gross Margin & Pricing Power

At StockStory, we prefer high gross margin businesses because they indicate pricing power or differentiated products, giving the company a chance to generate higher operating profits.

Nature's Sunshine has best-in-class unit economics for a consumer staples company, enabling it to invest in areas such as marketing and talent to grow its brand. As you can see below, it averaged an elite 72% gross margin over the last two years. That means Nature's Sunshine only paid its suppliers $28.05 for every $100 in revenue.

In Q4, Nature's Sunshine produced a 72.5% gross profit margin, in line with the same quarter last year. Zooming out, the company’s full-year margin has remained steady over the past 12 months, suggesting its input costs (such as raw materials and manufacturing expenses) have been stable and it isn’t under pressure to lower prices.

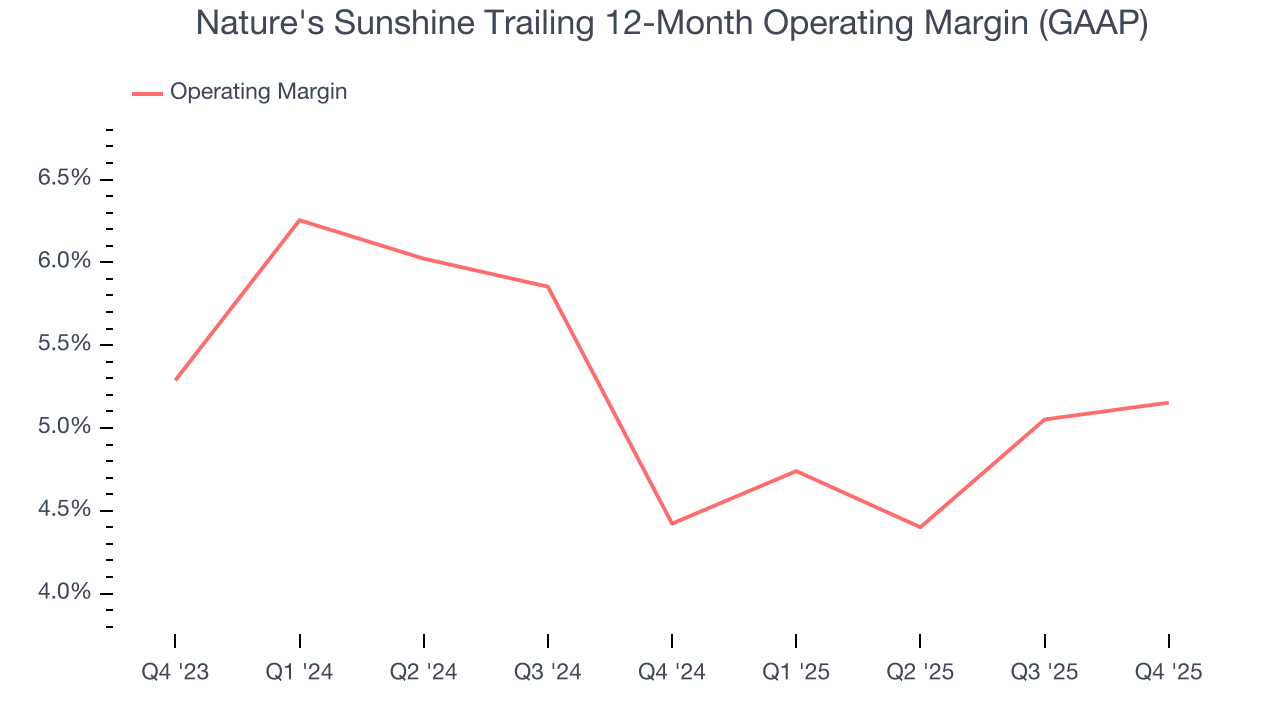

7. Operating Margin

Operating margin is a key profitability metric because it accounts for all expenses enabling a business to operate smoothly, including marketing and advertising, IT systems, wages, and other administrative costs.

Nature's Sunshine’s operating margin has generally stayed the same over the last 12 months, averaging 4.8% over the last two years. This profitability was paltry for a consumer staples business and caused by its suboptimal cost structure.

Looking at the trend in its profitability, Nature's Sunshine’s operating margin might fluctuated slightly but has generally stayed the same over the last year. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, Nature's Sunshine generated an operating margin profit margin of 4.3%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

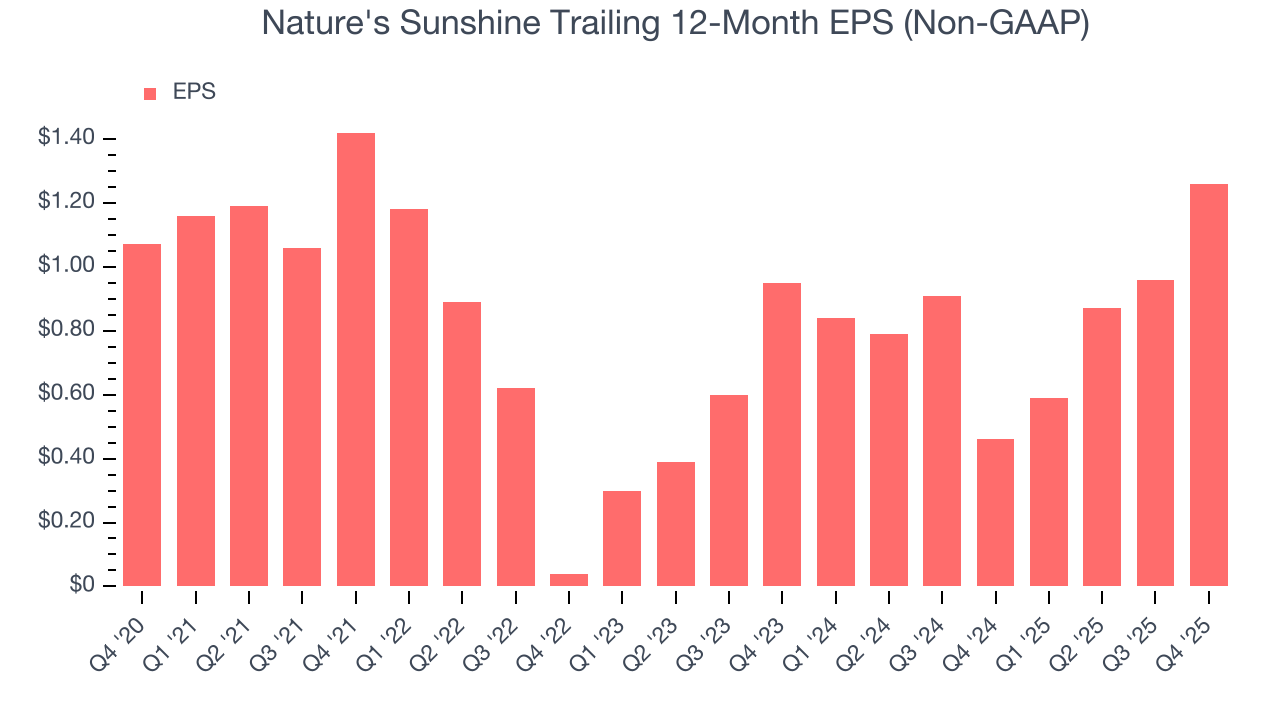

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Nature's Sunshine’s EPS grew at 216% compounded annual growth rate over the last three years, higher than its 4.4% annualized revenue growth. However, this alone doesn’t tell us much about its business quality because its operating margin didn’t improve.

In Q4, Nature's Sunshine reported adjusted EPS of $0.30, up from $0 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Nature's Sunshine’s full-year EPS of $1.26 to shrink by 23.8%.

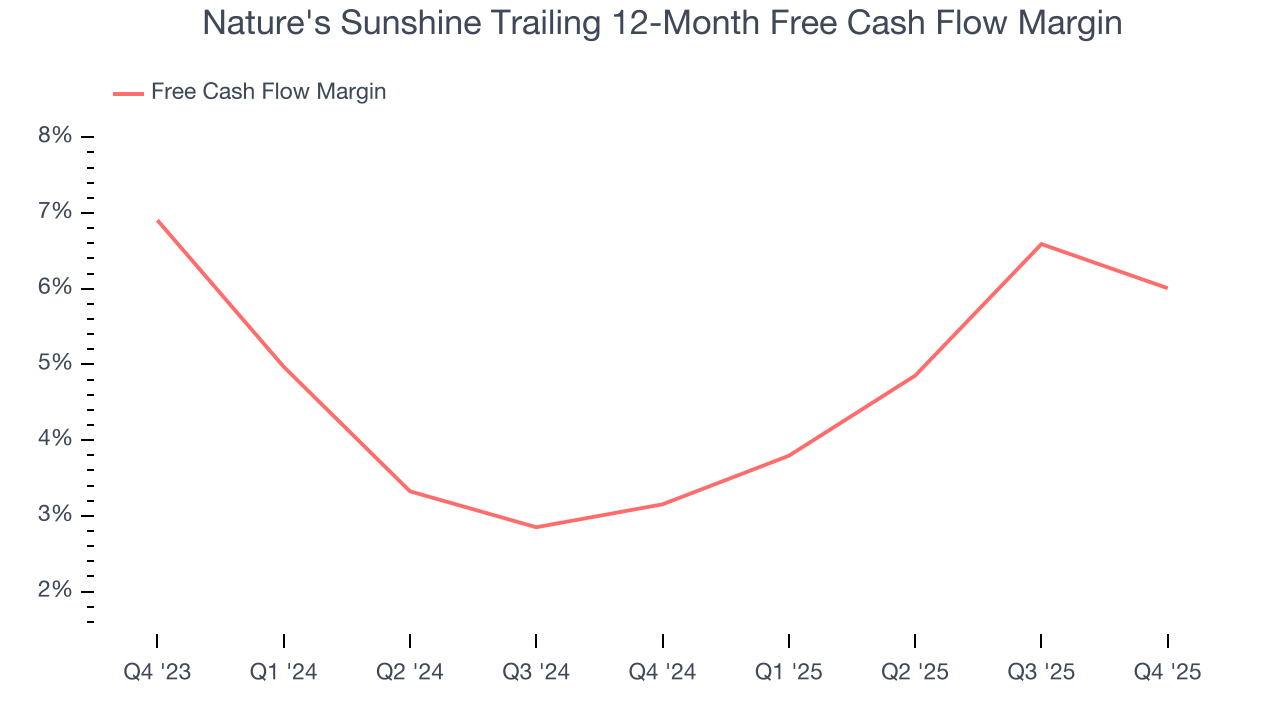

9. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Nature's Sunshine has shown mediocre cash profitability relative to peers over the last two years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 4.6%, below what we’d expect for a consumer staples business.

Taking a step back, an encouraging sign is that Nature's Sunshine’s margin expanded by 2.9 percentage points over the last year. The company’s improvement shows it’s heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose while its operating profitability was flat.

Nature's Sunshine’s free cash flow clocked in at $7.56 million in Q4, equivalent to a 6.1% margin. The company’s cash profitability regressed as it was 2.3 percentage points lower than in the same quarter last year, but it’s still above its two-year average. We wouldn’t read too much into this quarter’s decline because investment needs can be seasonal, causing short-term swings. Long-term trends carry greater meaning.

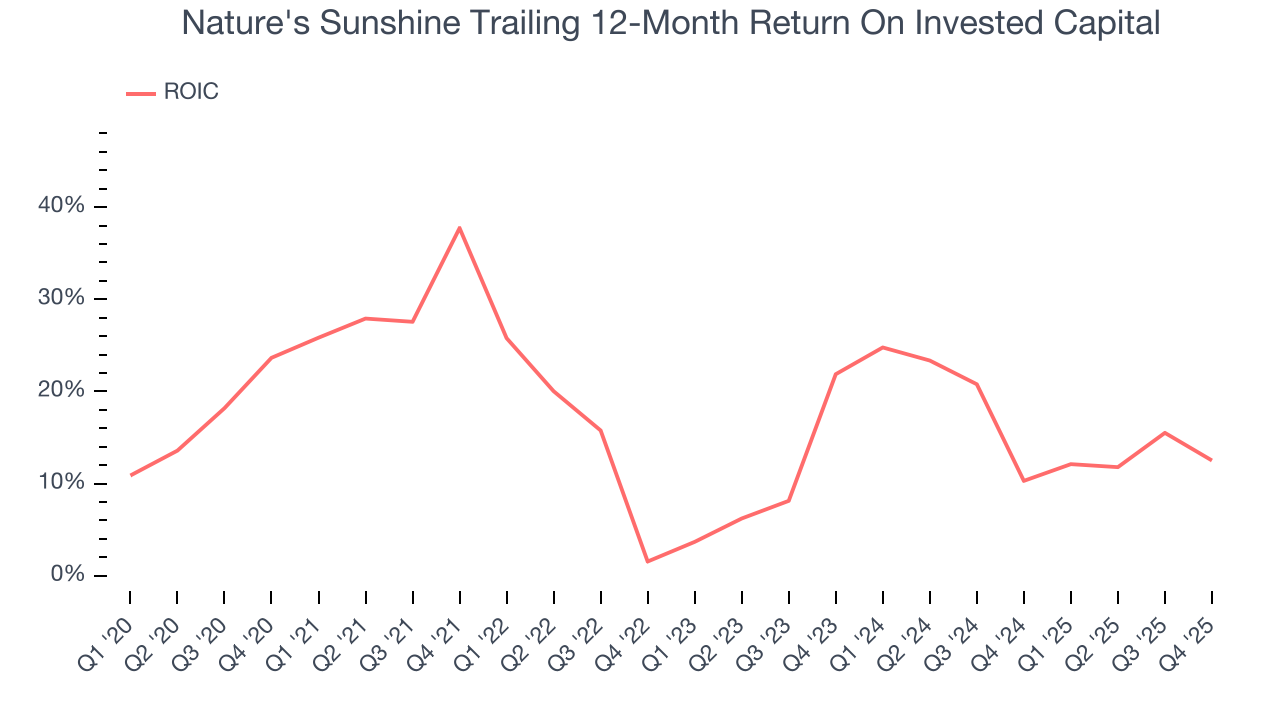

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Although Nature's Sunshine hasn’t been the highest-quality company lately, it historically found a few growth initiatives that worked. Its five-year average ROIC was 16.8%, higher than most consumer staples businesses.

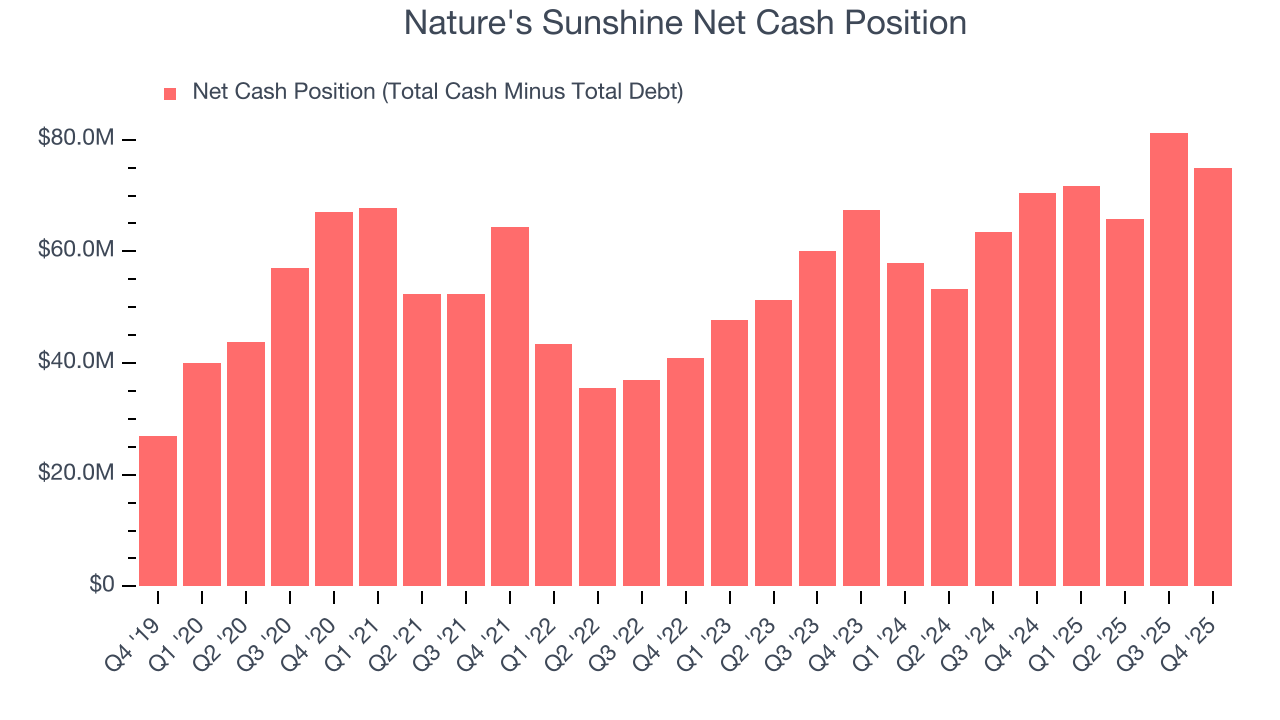

11. Balance Sheet Assessment

One of the best ways to mitigate bankruptcy risk is to hold more cash than debt.

Nature's Sunshine is a profitable, well-capitalized company with $93.89 million of cash and $18.9 million of debt on its balance sheet. This $74.99 million net cash position is 17.1% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

12. Key Takeaways from Nature's Sunshine’s Q4 Results

It was good to see Nature's Sunshine beat analysts’ EPS expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a solid print. The stock traded up 2.9% to $25.80 immediately following the results.

13. Is Now The Time To Buy Nature's Sunshine?

Updated: March 14, 2026 at 10:44 PM EDT

Before making an investment decision, investors should account for Nature's Sunshine’s business fundamentals and valuation in addition to what happened in the latest quarter.

Nature's Sunshine isn’t a terrible business, but it doesn’t pass our bar. To kick things off, its revenue growth was a little slower over the last three years. While its admirable gross margins are a wonderful starting point for the overall profitability of the business, the downside is its brand caters to a niche market. On top of that, its projected EPS for the next year is lacking.

Nature's Sunshine’s P/E ratio based on the next 12 months is 24.6x. Investors with a higher risk tolerance might like the company, but we think the potential downside is too great. We're fairly confident there are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $33 on the company (compared to the current share price of $24.48).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.