Novanta (NOVT)

We aren’t fans of Novanta. Its poor sales growth and falling returns on capital suggest its growth opportunities are shrinking.― StockStory Analyst Team

1. News

2. Summary

Why We Think Novanta Will Underperform

Originally a pioneer in the laser scanning industry during the late 1960s, Novanta (NASDAQ:NOVT) offers medicine and manufacturing technology to the medical, life sciences, and manufacturing industries.

- Anticipated sales growth of 6.5% for the next year implies demand will be shaky

- A positive is that its offerings are difficult to replicate at scale and result in a stellar gross margin of 44.2%

Novanta’s quality isn’t up to par. We believe there are better opportunities elsewhere.

Why There Are Better Opportunities Than Novanta

At $119.38 per share, Novanta trades at 34x forward P/E. This multiple is higher than that of industrials peers; it’s also rich for the business quality. Not a great combination.

We prefer to invest in similarly-priced but higher-quality companies with superior earnings growth.

3. Novanta (NOVT) Research Report: Q4 CY2025 Update

Medicine and manufacturing technology provider Novanta (NASDAQ:NOVT) missed Wall Street’s revenue expectations in Q4 CY2025, but sales rose 8.5% year on year to $258.3 million. Its non-GAAP profit of $0.91 per share was 3.4% above analysts’ consensus estimates.

Novanta (NOVT) Q4 CY2025 Highlights:

- Revenue: $258.3 million vs analyst estimates of $260.7 million (8.5% year-on-year growth, 0.9% miss)

- Adjusted EPS: $0.91 vs analyst estimates of $0.88 (3.4% beat)

- Adjusted EBITDA: $24.9 million vs analyst estimates of $63.12 million (9.6% margin, 60.6% miss)

- Operating Margin: 11.7%, down from 14.8% in the same quarter last year

- Free Cash Flow Margin: 2%, down from 24.9% in the same quarter last year

- Market Capitalization: $4.90 billion

Company Overview

Originally a pioneer in the laser scanning industry during the late 1960s, Novanta (NASDAQ:NOVT) offers medicine and manufacturing technology to the medical, life sciences, and manufacturing industries.

Novanta was founded in 1968 as General Scanning and originally focused on laser beam steering and scanning. In 2005, the company merged with Lumonics (forming GSI Group) which rebranded as Novanta in 2016 to better reflect its portfolio of medicine and manufacturing technologies. Today, the company provides for the medical, life sciences, and manufacturing industries.

Novanta’s product offerings include laser systems (make cuts/marks on materials and are used in surgery and diagnostics), precision motion control (move and position parts in machines), and vision technologies (cameras and software that help machines see and analyze what it is working on). Whether products are used for medical procedures or the manufacturing process, Novanta’s products enable customers to improve accuracy (removing human error) and efficiency. Its customers range from healthcare providers and medical device manufacturers to industrial automation firms and tech companies.

Novanta sells its products directly to original equipment manufacturers (OEMs) and through a network of distributors, engaging in long-term contracts that often include service and support agreements. This ensures a stable revenue stream and strong customer relationships. In addition, the company offers OEMs a volume discount to incentivize more frequent and larger volume orders.

4. Electronic Components

Like many equipment and component manufacturers, electronic components companies are buoyed by secular trends such as connectivity and industrial automation. More specific pockets of strong demand include data centers and telecommunications, which can benefit companies whose optical and transceiver offerings fit those markets. But like the broader industrials sector, these companies are also at the whim of economic cycles. Consumer spending, for example, can greatly impact these companies’ volumes.

Competitors offering similar products include Danaher (NYSE:DHR), MKS Instruments (NASDAQ:MKSI), and Coherent (NASDAQ:COHR).

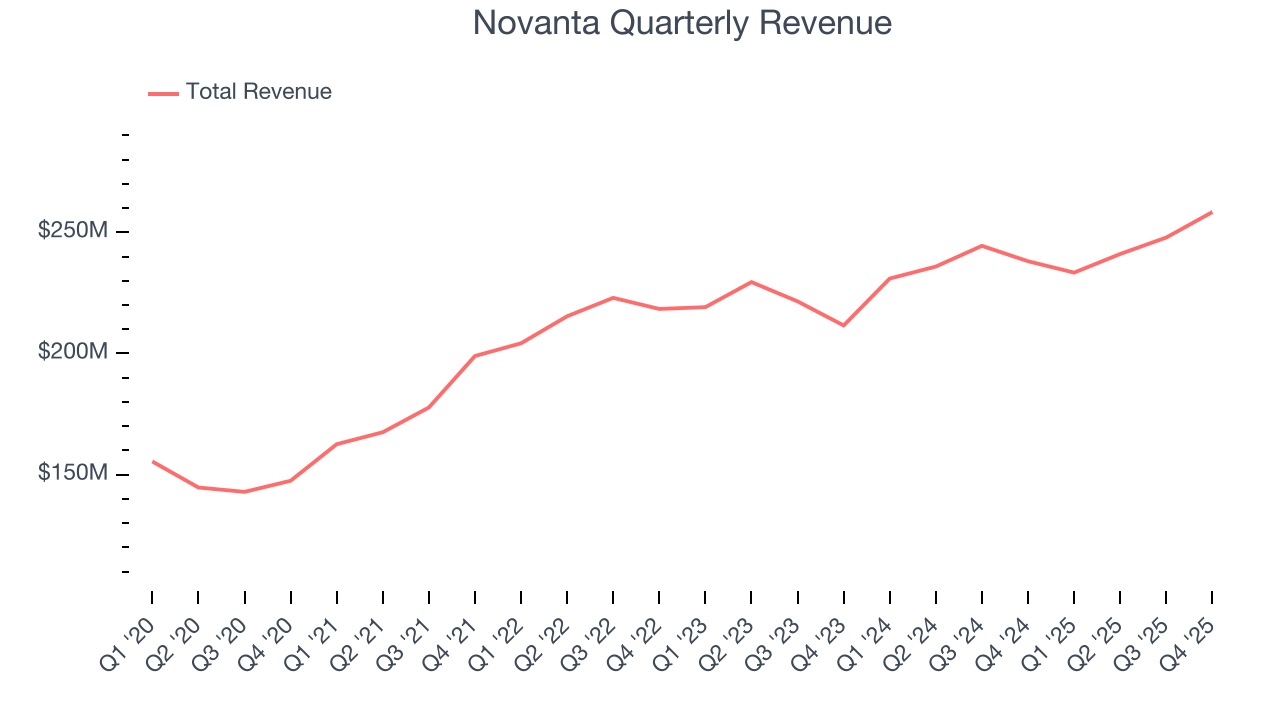

5. Revenue Growth

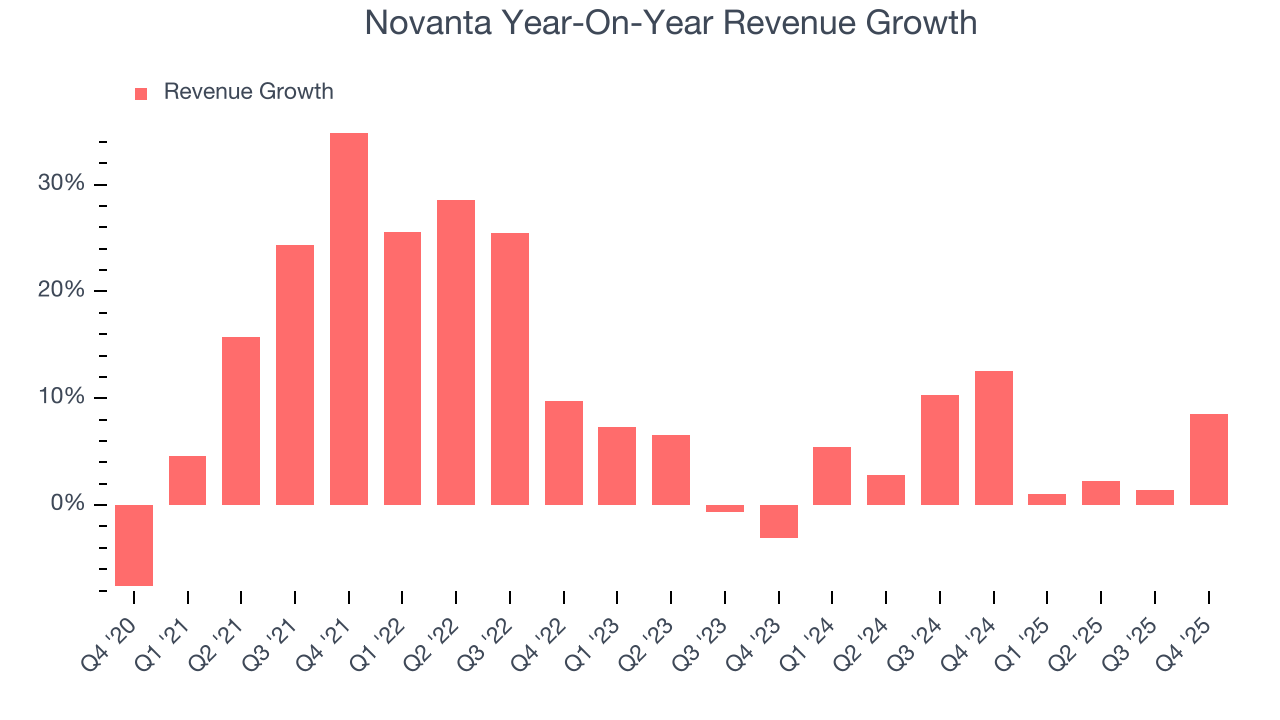

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Luckily, Novanta’s sales grew at an impressive 10.7% compounded annual growth rate over the last five years. Its growth beat the average industrials company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Novanta’s recent performance shows its demand has slowed significantly as its annualized revenue growth of 5.5% over the last two years was well below its five-year trend.

This quarter, Novanta’s revenue grew by 8.5% year on year to $258.3 million, missing Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 6.4% over the next 12 months, similar to its two-year rate. This projection is underwhelming and indicates its newer products and services will not accelerate its top-line performance yet.

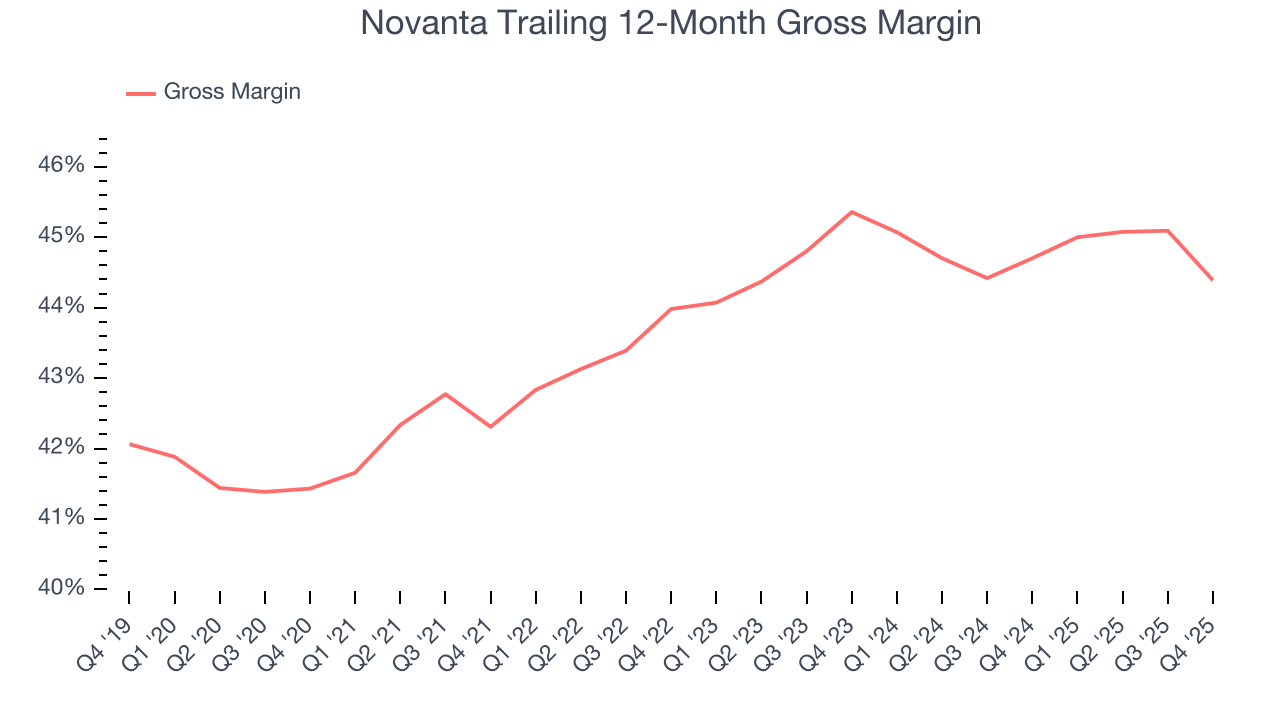

6. Gross Margin & Pricing Power

For industrials businesses, cost of sales is usually comprised of the direct labor, raw materials, and supplies needed to offer a product or service. These costs can be impacted by inflation and supply chain dynamics in the short term and a company’s purchasing power and scale over the long term.

Novanta has best-in-class unit economics for an industrials company, enabling it to invest in areas such as research and development. Its margin also signals it sells differentiated products, not commodities. As you can see below, it averaged an elite 44.2% gross margin over the last five years. Said differently, roughly $44.24 was left to spend on selling, marketing, R&D, and general administrative overhead for every $100 in revenue.

Novanta produced a 43.8% gross profit margin in Q4, down 2.8 percentage points year on year. On a wider time horizon, the company’s full-year margin has remained steady over the past four quarters, suggesting its input costs (such as raw materials and manufacturing expenses) have been stable and it isn’t under pressure to lower prices.

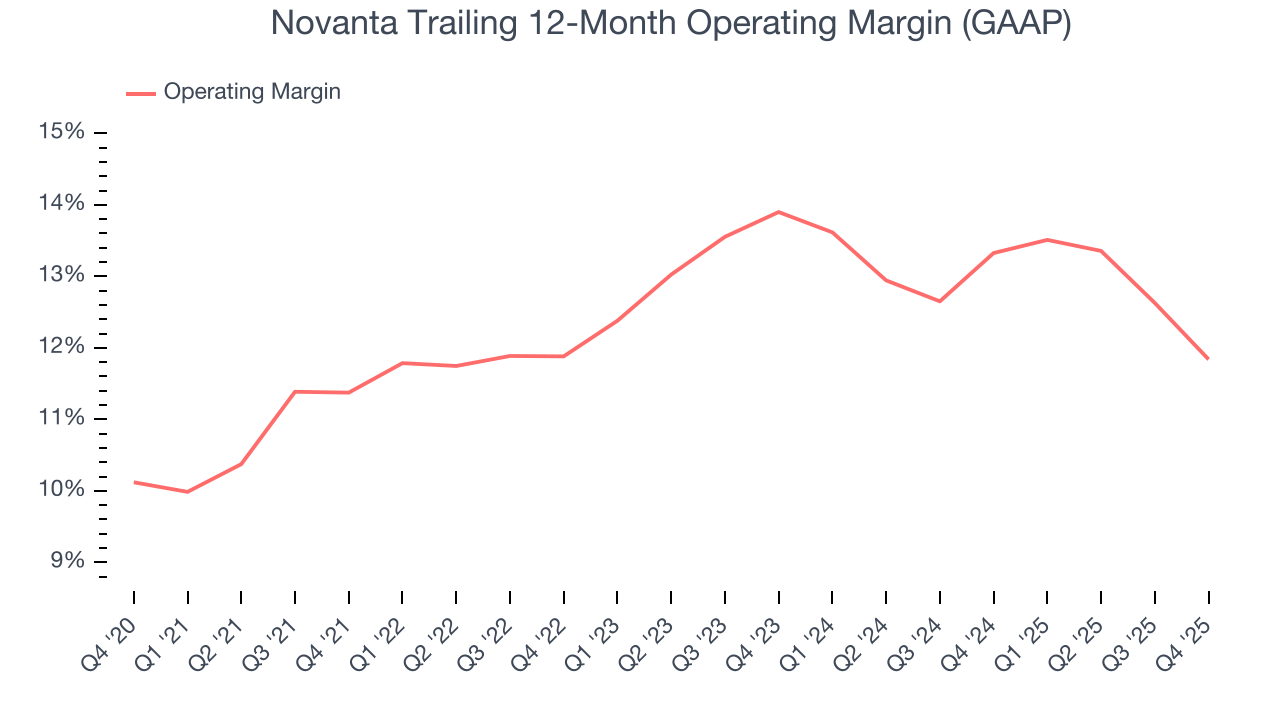

7. Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Novanta’s operating margin might fluctuated slightly over the last 12 months but has remained more or less the same, averaging 12.5% over the last five years. This profitability was top-notch for an industrials business, showing it’s an well-run company with an efficient cost structure. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Looking at the trend in its profitability, Novanta’s operating margin might fluctuated slightly but has generally stayed the same over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q4, Novanta generated an operating margin profit margin of 11.7%, down 3.2 percentage points year on year. Since Novanta’s operating margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, R&D, and administrative overhead increased.

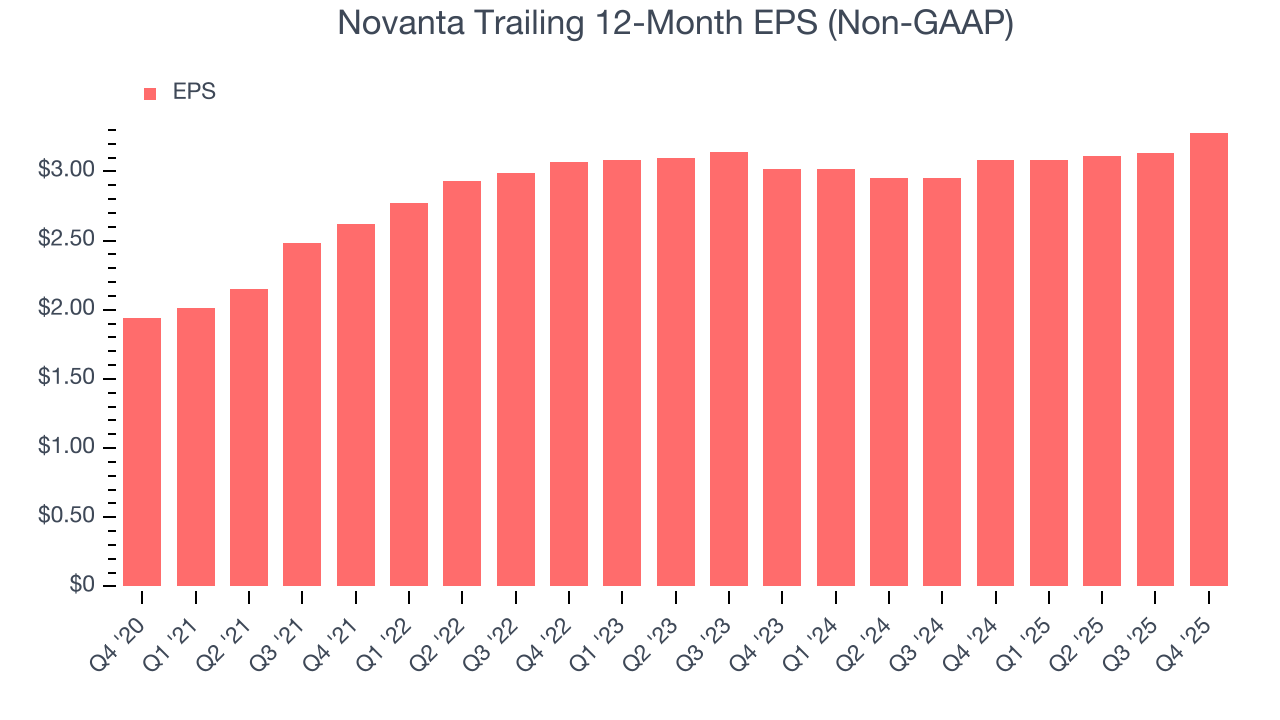

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Novanta’s solid 11.1% annual EPS growth over the last five years aligns with its revenue performance. This tells us its incremental sales were profitable.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Novanta, its two-year annual EPS growth of 4.2% was lower than its five-year trend. We hope its growth can accelerate in the future.

In Q4, Novanta reported adjusted EPS of $0.91, up from $0.76 in the same quarter last year. This print beat analysts’ estimates by 3.4%. Over the next 12 months, Wall Street expects Novanta’s full-year EPS of $3.28 to grow 11%.

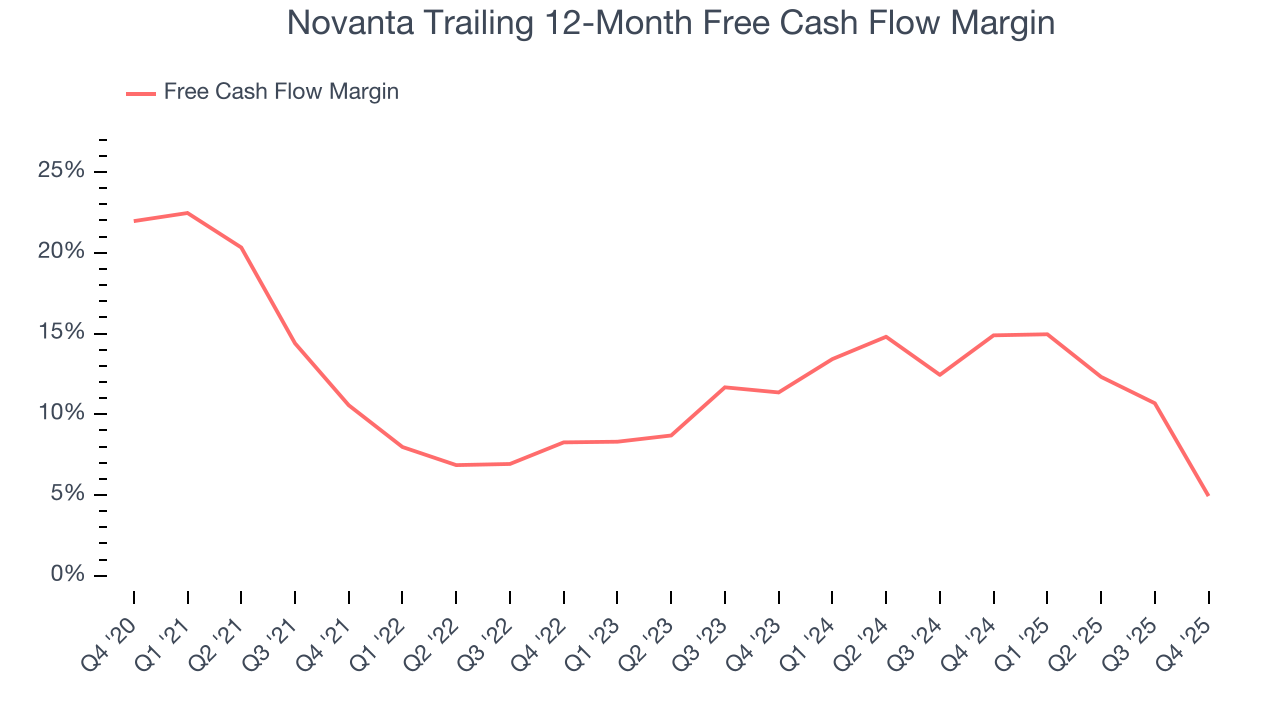

9. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Novanta has shown robust cash profitability, enabling it to comfortably ride out cyclical downturns while investing in plenty of new offerings and returning capital to investors. The company’s free cash flow margin averaged 9.9% over the last five years, quite impressive for an industrials business.

Taking a step back, we can see that Novanta’s margin dropped by 5.6 percentage points during that time. If its declines continue, it could signal increasing investment needs and capital intensity.

Novanta’s free cash flow clocked in at $5.13 million in Q4, equivalent to a 2% margin. The company’s cash profitability regressed as it was 22.9 percentage points lower than in the same quarter last year, suggesting its historical struggles have dragged on.

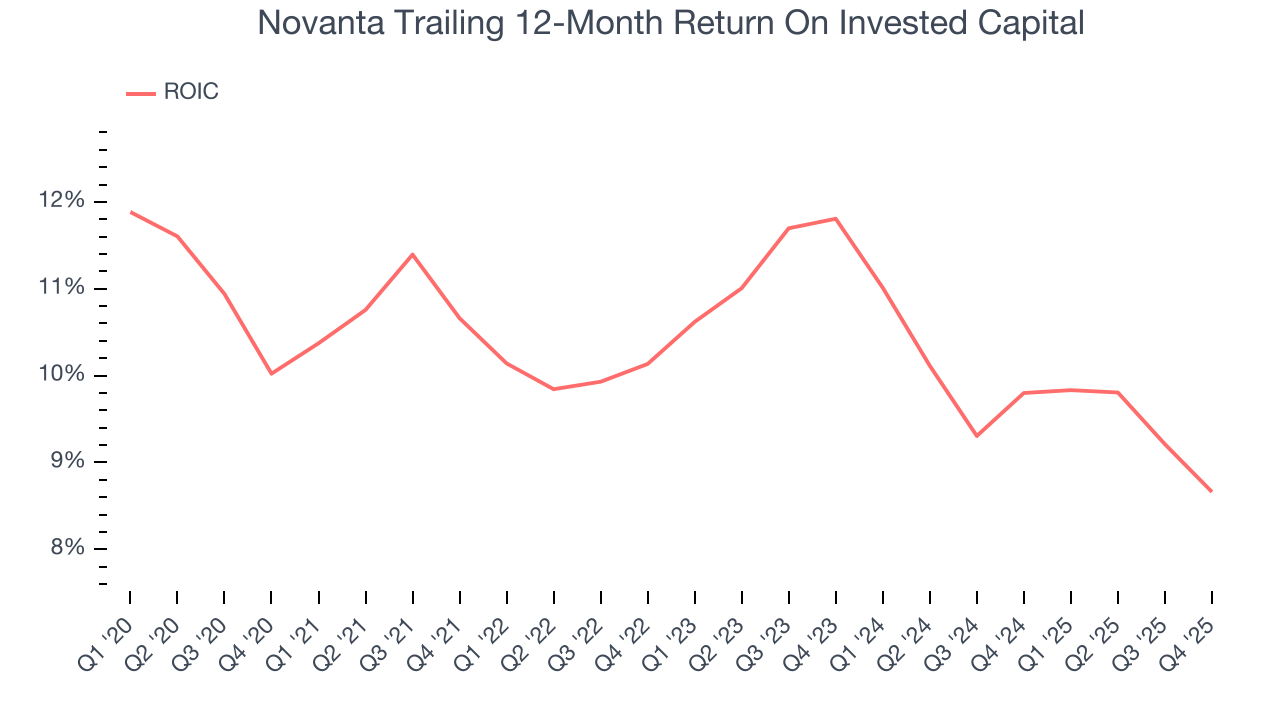

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Novanta’s management team makes decent investment decisions and generates value for shareholders. Its five-year average ROIC was 10.2%, slightly better than typical industrials business.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, Novanta’s ROIC averaged 1.2 percentage point decreases each year over the last few years. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

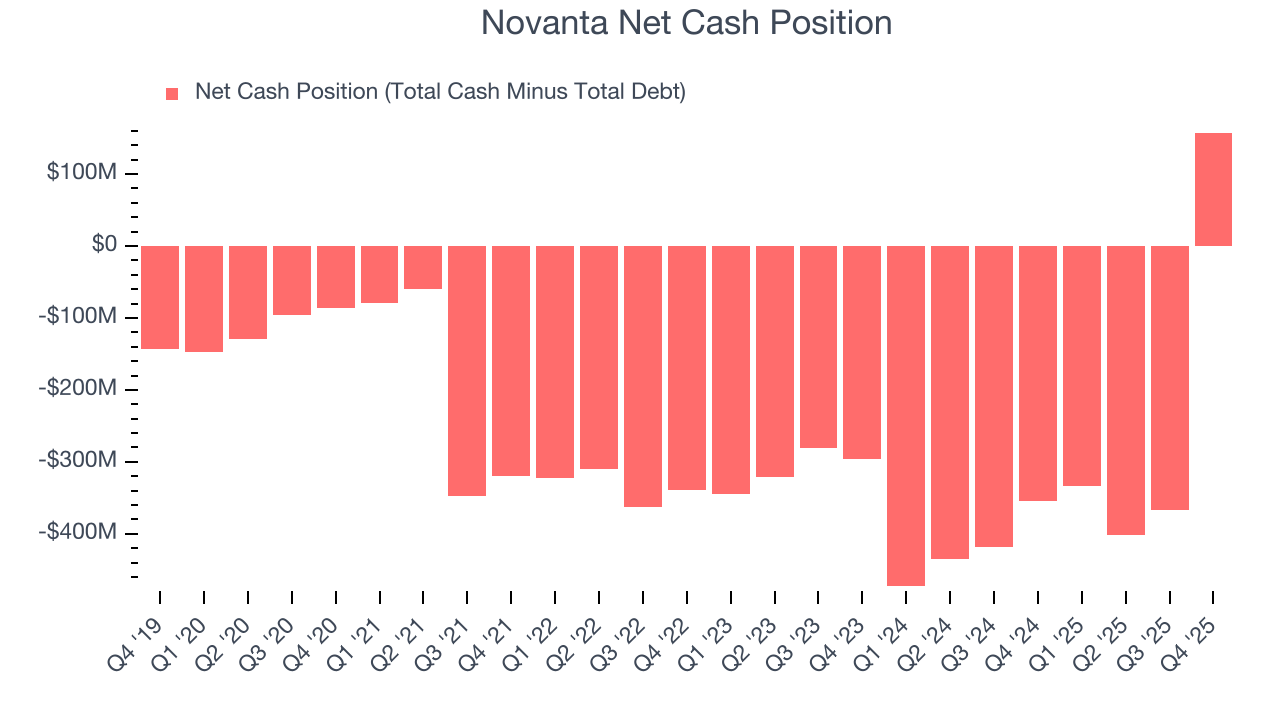

11. Balance Sheet Assessment

One of the best ways to mitigate bankruptcy risk is to hold more cash than debt.

Novanta is a profitable, well-capitalized company with $380.9 million of cash and $223.2 million of debt on its balance sheet. This $157.6 million net cash position is 3.2% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

12. Key Takeaways from Novanta’s Q4 Results

It was good to see Novanta beat analysts’ EPS expectations this quarter. On the other hand, its EBITDA missed and its revenue fell slightly short of Wall Street’s estimates. Overall, this quarter could have been better. The stock remained flat at $137.72 immediately after reporting.

13. Is Now The Time To Buy Novanta?

Updated: March 18, 2026 at 11:37 PM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Novanta.

Novanta isn’t a terrible business, but it isn’t one of our picks. Although its revenue growth was impressive over the last five years, it’s expected to deteriorate over the next 12 months and its cash profitability fell over the last five years.

Novanta’s P/E ratio based on the next 12 months is 34x. This multiple tells us a lot of good news is priced in - we think there are better opportunities elsewhere.

Wall Street analysts have a consensus one-year price target of $160 on the company (compared to the current share price of $119.38).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.