Shoals (SHLS)

We’re cautious of Shoals. Its poor sales growth and falling returns on capital suggest its growth opportunities are shrinking.― StockStory Analyst Team

1. News

2. Summary

Why We Think Shoals Will Underperform

Started in Huntsville, Alabama, Shoals (NASDAQ:SHLS) designs and manufactures products that make solar energy systems work more efficiently.

- A positive is that its annual revenue growth of 22% over the past five years was outstanding, reflecting market share gains this cycle

Shoals is skating on thin ice. There are more promising alternatives.

Why There Are Better Opportunities Than Shoals

Shoals is trading at $6.05 per share, or 14.8x forward P/E. Yes, this valuation multiple is lower than that of other industrials peers, but we’ll remind you that you often get what you pay for.

Cheap stocks can look like a great deal at first glance, but they can be value traps. They often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. Shoals (SHLS) Research Report: Q4 CY2025 Update

Solar energy systems company Shoals (NASDAQ:SHLS) reported revenue ahead of Wall Street’s expectations in Q4 CY2025, with sales up 38.6% year on year to $148.3 million. On top of that, next quarter’s revenue guidance ($130 million at the midpoint) was surprisingly good and 9.6% above what analysts were expecting. Its non-GAAP profit of $0.10 per share was 28.4% below analysts’ consensus estimates.

Shoals (SHLS) Q4 CY2025 Highlights:

- Revenue: $148.3 million vs analyst estimates of $144.9 million (38.6% year-on-year growth, 2.4% beat)

- Adjusted EPS: $0.10 vs analyst expectations of $0.14 (28.4% miss)

- Adjusted EBITDA: $30.28 million vs analyst estimates of $37.04 million (20.4% margin, 18.3% miss)

- Revenue Guidance for Q1 CY2026 is $130 million at the midpoint, above analyst estimates of $118.6 million

- EBITDA guidance for the upcoming financial year 2026 is $120 million at the midpoint, below analyst estimates of $134 million

- Operating Margin: 11.7%, down from 15.4% in the same quarter last year

- Free Cash Flow was -$11.25 million, down from $12.46 million in the same quarter last year

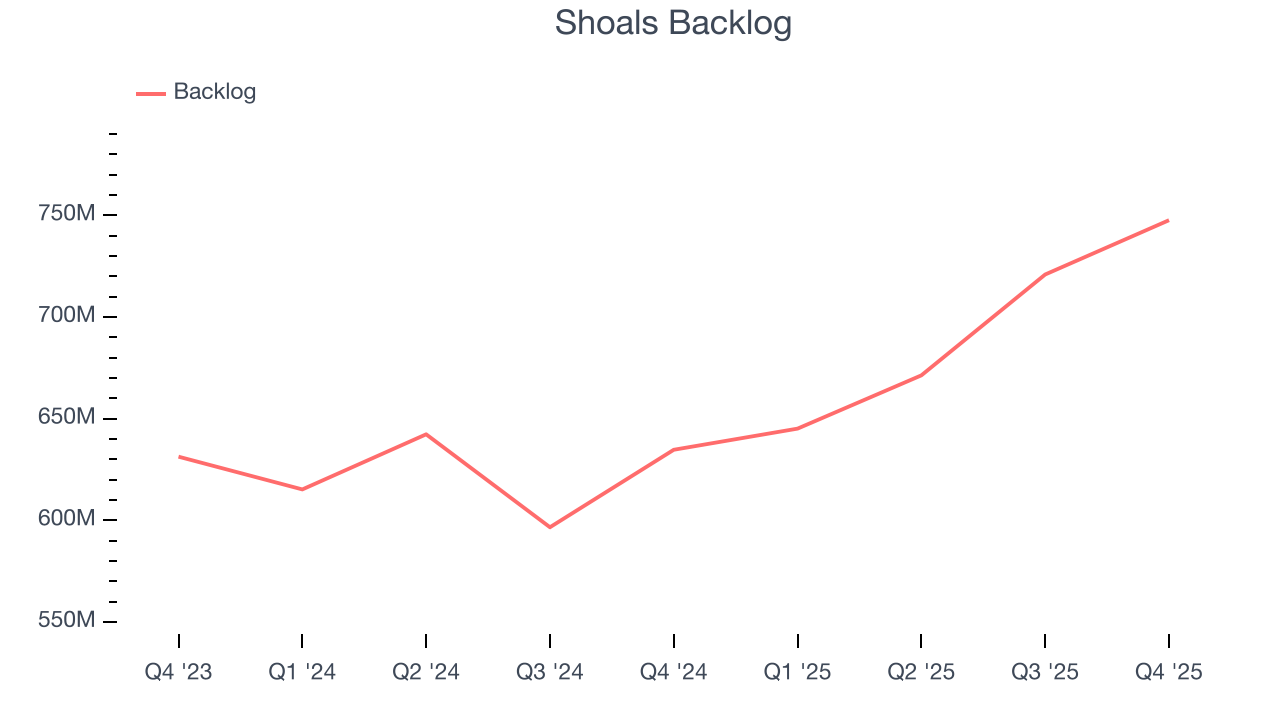

- Backlog: $747.6 million at quarter end, up 17.8% year on year

- Market Capitalization: $1.66 billion

Company Overview

Started in Huntsville, Alabama, Shoals (NASDAQ:SHLS) designs and manufactures products that make solar energy systems work more efficiently.

These products are called electrical balance of systems (BOS), which optimize the performance and reliability of companies or individuals using solar power. Shoals sells these BOS solutions to solar energy developers, installers, and operators, with companies like Tesla in its target market.

Specifically, Shoals's products include direct current disconnectors, combiner boxes, junction boxes, and other components that together make up a BOS. Along with its hardware, the company provides software to monitor and control its products, as well as installation and support services and engineering and design services for customized projects.

The company generates revenue through the sale of its hardware and software products, which are sold via direct sales to companies. Its accompanying services typically come in the form of service contracts or maintenance agreements.

4. Renewable Energy

Renewable energy companies are buoyed by the secular trend of green energy that is upending traditional power generation. Those who innovate and evolve with this dynamic market can win share while those who continue to rely on legacy technologies can see diminishing demand, which includes headwinds from increasing regulation against “dirty” energy. Additionally, these companies are at the whim of economic cycles, as interest rates can impact the willingness to invest in renewable energy projects.

Competitors of Shoals Technologies include ABB (NYSE:ABB), Amphenol (NYSE:APH), and private company TMEIC.

5. Revenue Growth

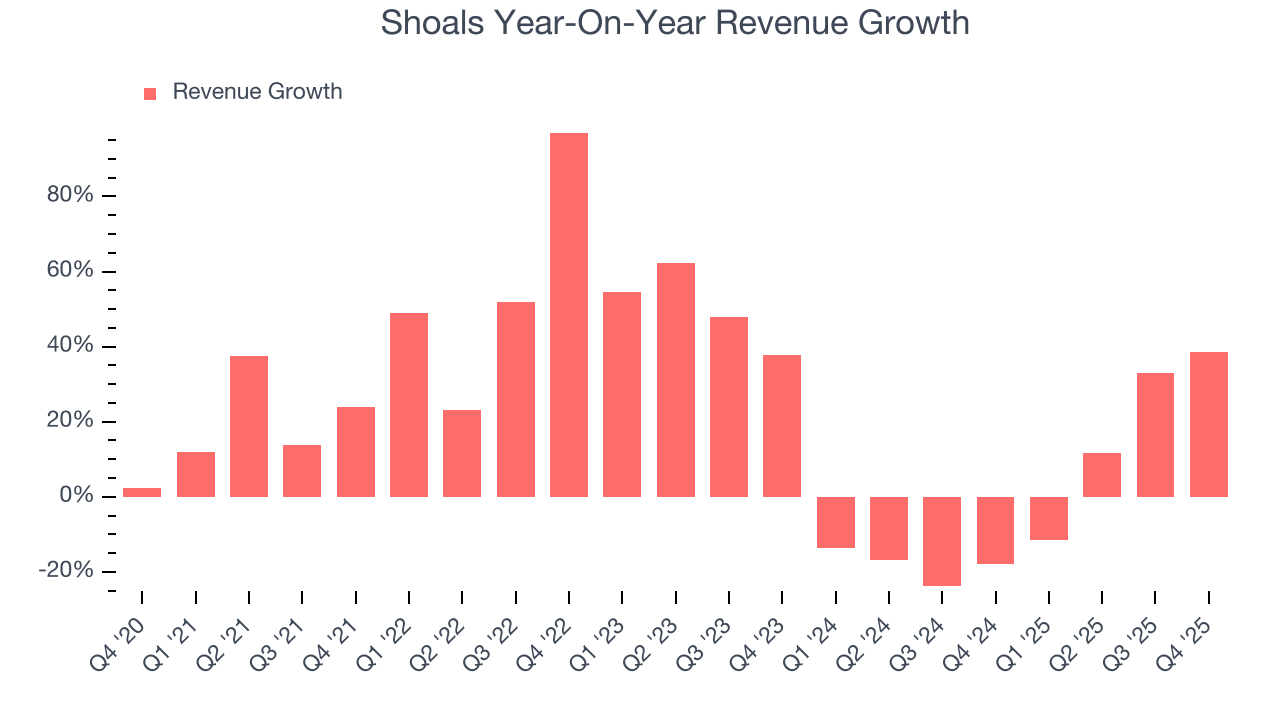

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, Shoals grew its sales at an incredible 22% compounded annual growth rate. Its growth beat the average industrials company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Shoals’s recent performance marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 1.4% over the last two years.

We can better understand the company’s revenue dynamics by analyzing its backlog, or the value of its outstanding orders that have not yet been executed or delivered. Shoals’s backlog reached $747.6 million in the latest quarter and averaged 9.7% year-on-year growth over the last two years. Because this number is better than its revenue growth, we can see the company accumulated more orders than it could fulfill and deferred revenue to the future. This could imply elevated demand for Shoals’s products and services but raises concerns about capacity constraints.

This quarter, Shoals reported wonderful year-on-year revenue growth of 38.6%, and its $148.3 million of revenue exceeded Wall Street’s estimates by 2.4%. Company management is currently guiding for a 61.8% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 18.3% over the next 12 months, an improvement versus the last two years. This projection is eye-popping and indicates its newer products and services will spur better top-line performance.

6. Gross Margin & Pricing Power

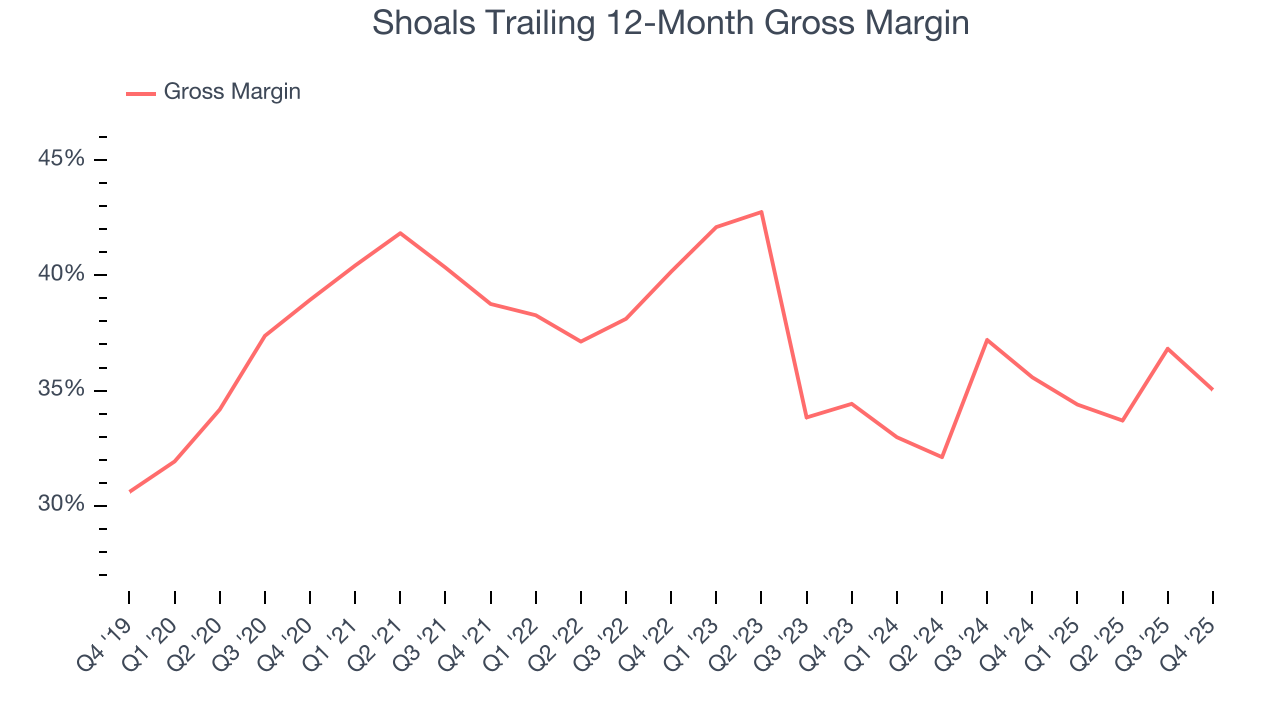

Shoals’s unit economics are great compared to the broader industrials sector and signal that it enjoys product differentiation through quality or brand. As you can see below, it averaged an excellent 36.3% gross margin over the last five years. That means Shoals only paid its suppliers $63.71 for every $100 in revenue.

This quarter, Shoals’s gross profit margin was 31.6%, down 5.9 percentage points year on year. Zooming out, the company’s full-year margin has remained steady over the past 12 months, suggesting its input costs (such as raw materials and manufacturing expenses) have been stable and it isn’t under pressure to lower prices.

7. Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

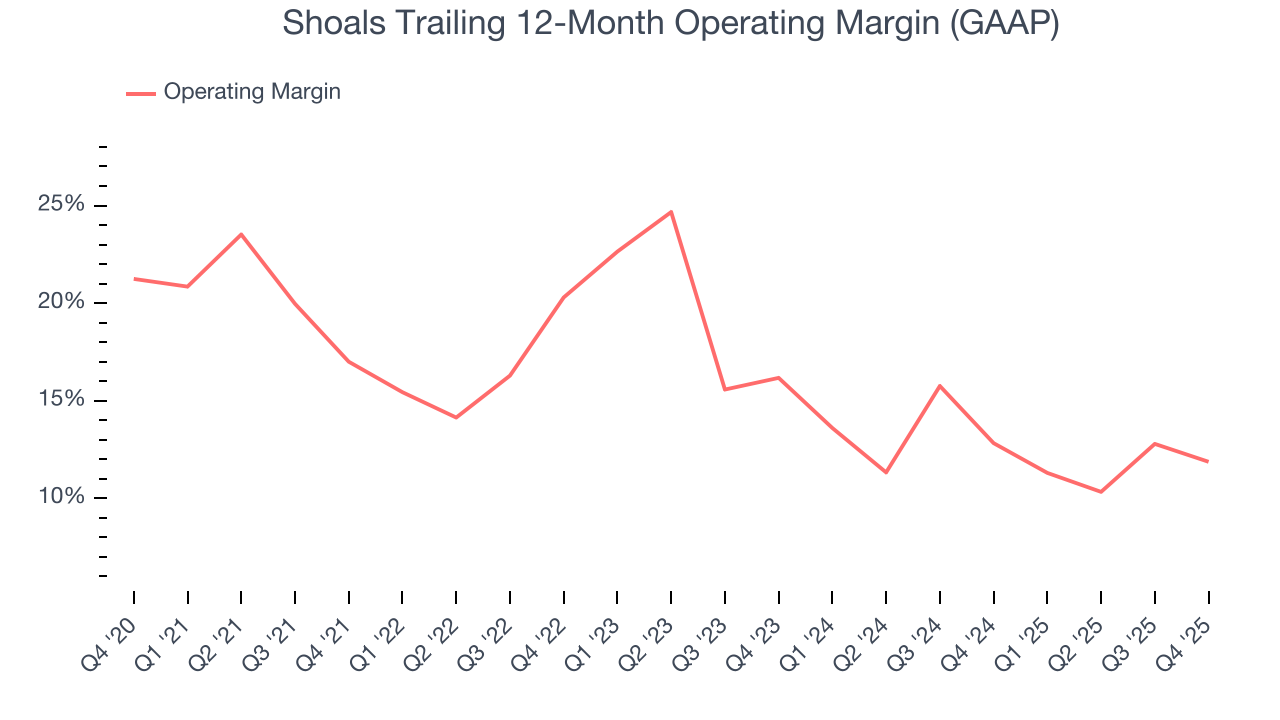

Shoals has been an efficient company over the last five years. It was one of the more profitable businesses in the industrials sector, boasting an average operating margin of 15.2%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, Shoals’s operating margin decreased by 5.1 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q4, Shoals generated an operating margin profit margin of 11.7%, down 3.7 percentage points year on year. Since Shoals’s gross margin decreased more than its operating margin, we can assume its recent inefficiencies were driven more by weaker leverage on its cost of sales rather than increased marketing, R&D, and administrative overhead expenses.

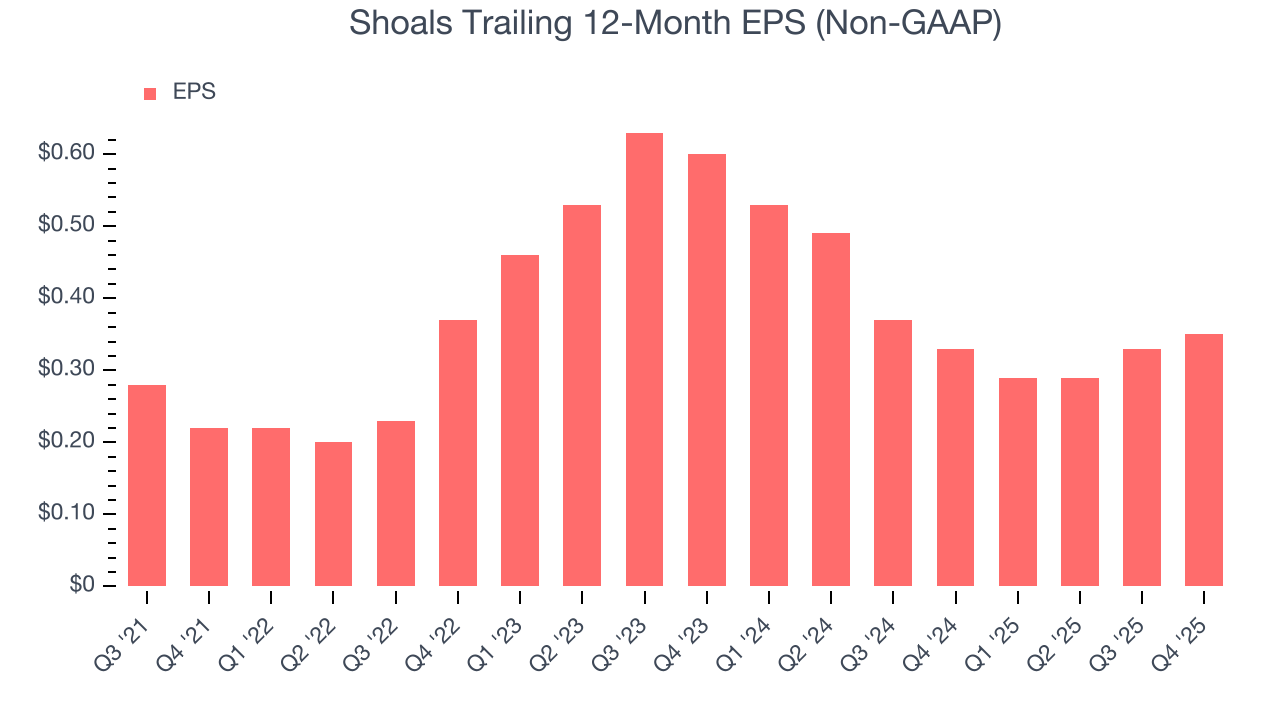

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Shoals’s full-year EPS grew at a remarkable 12.3% compounded annual growth rate over the last four years, better than the broader industrials sector.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

Sadly for Shoals, its EPS declined by more than its revenue over the last two years, dropping 23.6%. This tells us the company struggled to adjust to shrinking demand.

We can take a deeper look into Shoals’s earnings to better understand the drivers of its performance. Shoals’s operating margin has declined over the last two years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q4, Shoals reported adjusted EPS of $0.10, up from $0.08 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates, but we care more about long-term adjusted EPS growth than short-term movements. Over the next 12 months, Wall Street expects Shoals’s full-year EPS of $0.35 to grow 44.8%.

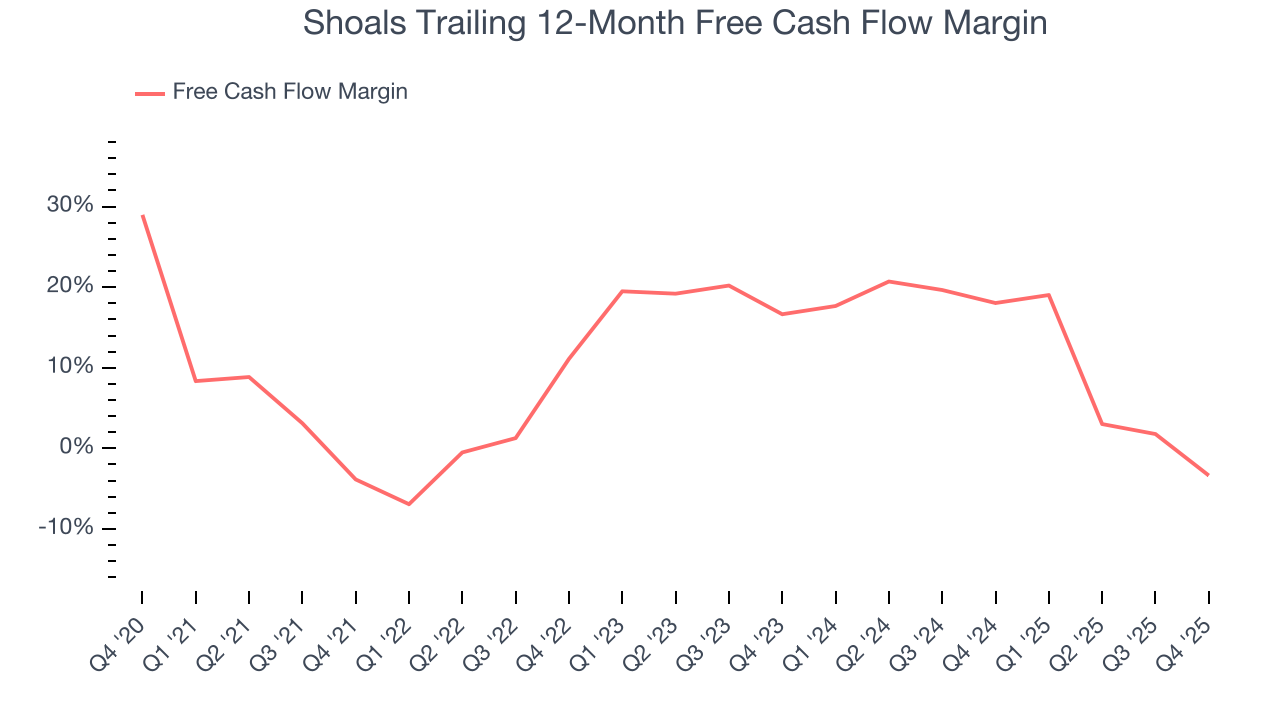

9. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Shoals has shown impressive cash profitability, enabling it to ride out cyclical downturns more easily while maintaining its investments in new and existing offerings. The company’s free cash flow margin averaged 8.7% over the last five years, better than the broader industrials sector.

Shoals burned through $11.25 million of cash in Q4, equivalent to a negative 7.6% margin. The company’s cash flow turned negative after being positive in the same quarter last year, prompting us to pay closer attention. Short-term fluctuations typically aren’t a big deal because investment needs can be seasonal, but we’ll be watching to see if the trend extrapolates into future quarters.

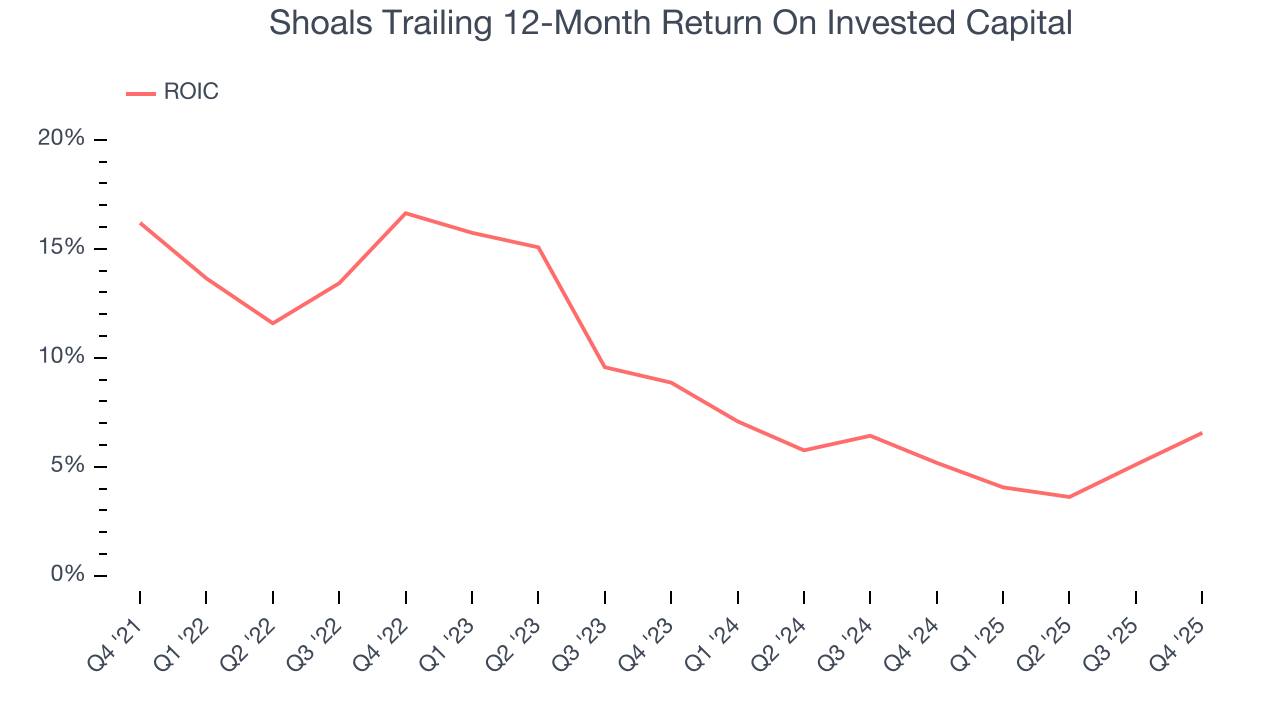

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Shoals’s management team makes decent investment decisions and generates value for shareholders. Its five-year average ROIC was 10.7%, slightly better than typical industrials business.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, Shoals’s ROIC has decreased significantly over the last few years. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

11. Balance Sheet Assessment

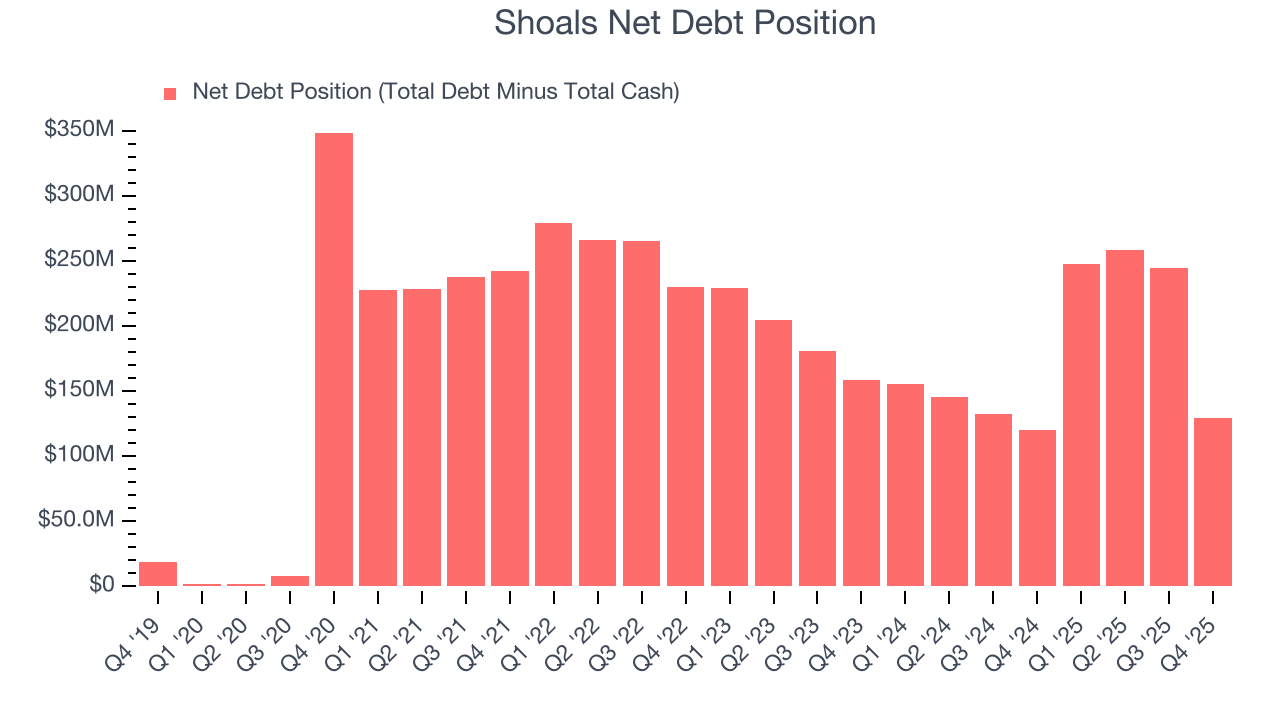

Shoals reported $7.32 million of cash and $136.8 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $99.52 million of EBITDA over the last 12 months, we view Shoals’s 1.3× net-debt-to-EBITDA ratio as safe. We also see its $4.81 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Shoals’s Q4 Results

We were impressed by Shoals’s optimistic revenue guidance for next quarter, which blew past analysts’ expectations. We were also glad its full-year revenue guidance trumped Wall Street’s estimates. On the other hand, its full-year EBITDA guidance missed and its EBITDA fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 10.8% to $8.83 immediately after reporting.

13. Is Now The Time To Buy Shoals?

Updated: March 15, 2026 at 11:20 PM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Shoals.

Shoals isn’t a terrible business, but it doesn’t pass our bar. Although its revenue growth was exceptional over the last five years and is expected to accelerate over the next 12 months, its diminishing returns show management's prior bets haven't worked out. And while the company’s projected EPS for the next year implies the company’s fundamentals will improve, the downside is its declining operating margin shows the business has become less efficient.

Shoals’s P/E ratio based on the next 12 months is 14.8x. This valuation multiple is fair, but we don’t have much faith in the company. We're fairly confident there are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $9.63 on the company (compared to the current share price of $6.05).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.