Zumiez (ZUMZ)

We wouldn’t recommend Zumiez. Not only are its sales cratering but also its low returns on capital suggest it struggles to generate profits.― StockStory Analyst Team

1. News

2. Summary

Why We Think Zumiez Will Underperform

With store associates called “Zumiez Stash Members”, Zumiez (NASDAQ:ZUMZ) is a specialty retailer of street and skate apparel, footwear, and accessories.

- Below-average returns on capital indicate management struggled to find compelling investment opportunities, and its shrinking returns suggest its past profit sources are losing steam

- Subscale operations are evident in its revenue base of $929.1 million, meaning it has fewer distribution channels than its larger rivals

- Store closures are a headwind for growth and suggest it’s rightsizing operations to optimize sales at existing locations

Zumiez doesn’t live up to our standards. We’re hunting for superior stocks elsewhere.

Why There Are Better Opportunities Than Zumiez

Zumiez’s stock price of $21.39 implies a valuation ratio of 25.8x forward P/E. This multiple is high given its weaker fundamentals.

It’s better to pay up for high-quality businesses with strong long-term earnings potential rather than to buy lower-quality companies with open questions and big downside risks.

3. Zumiez (ZUMZ) Research Report: Q4 CY2025 Update

Clothing and footwear retailer Zumiez (NASDAQ:ZUMZ) reported Q4 CY2025 results topping the market’s revenue expectations, with sales up 4.4% year on year to $291.3 million. Guidance for next quarter’s revenue was optimistic at $191 million at the midpoint, 2.5% above analysts’ estimates. Its GAAP profit of $1.16 per share was 8.9% above analysts’ consensus estimates.

Zumiez (ZUMZ) Q4 CY2025 Highlights:

- Revenue: $291.3 million vs analyst estimates of $289.1 million (4.4% year-on-year growth, 0.8% beat)

- EPS (GAAP): $1.16 vs analyst estimates of $1.07 (8.9% beat)

- Adjusted EBITDA: $37.43 million vs analyst estimates of $29.81 million (12.8% margin, 25.6% beat)

- Revenue Guidance for Q1 CY2026 is $191 million at the midpoint, above analyst estimates of $186.3 million

- EPS (GAAP) guidance for Q1 CY2026 is -$0.82 at the midpoint, missing analyst estimates by 9.3%

- Operating Margin: 8.6%, up from 7.2% in the same quarter last year

- Free Cash Flow Margin: 18.6%, similar to the same quarter last year

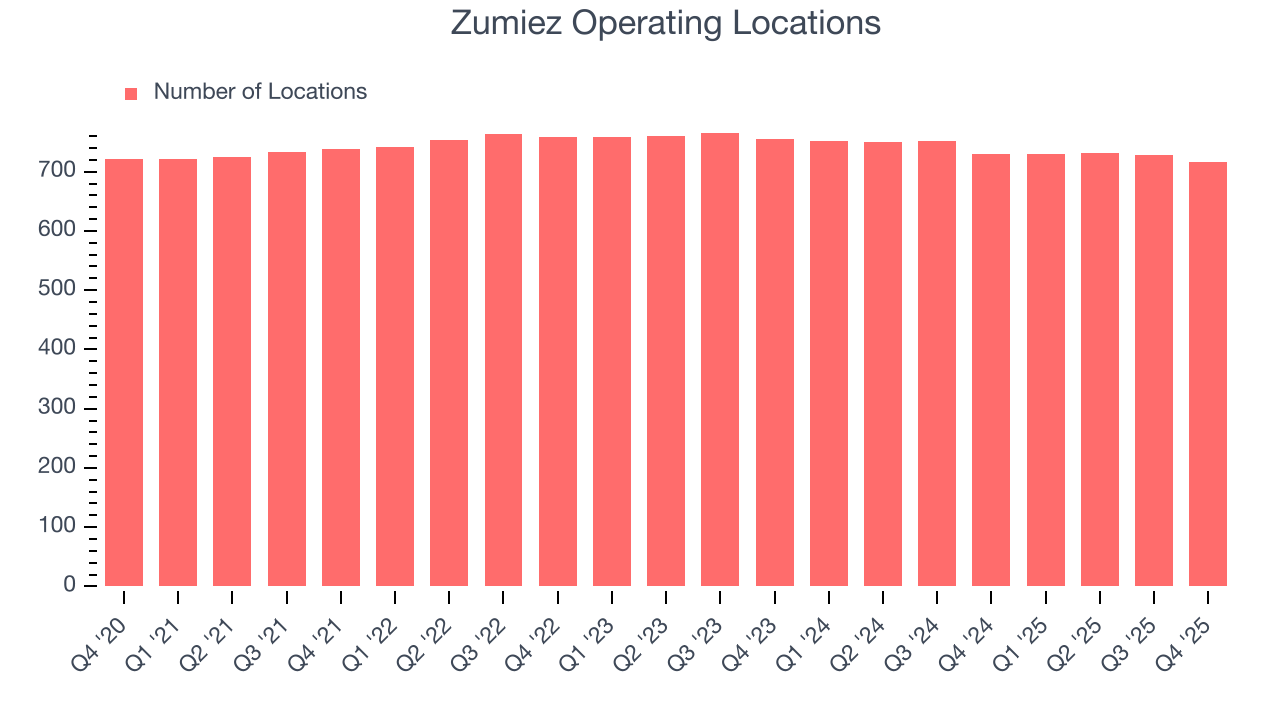

- Locations: 716 at quarter end, down from 730 in the same quarter last year

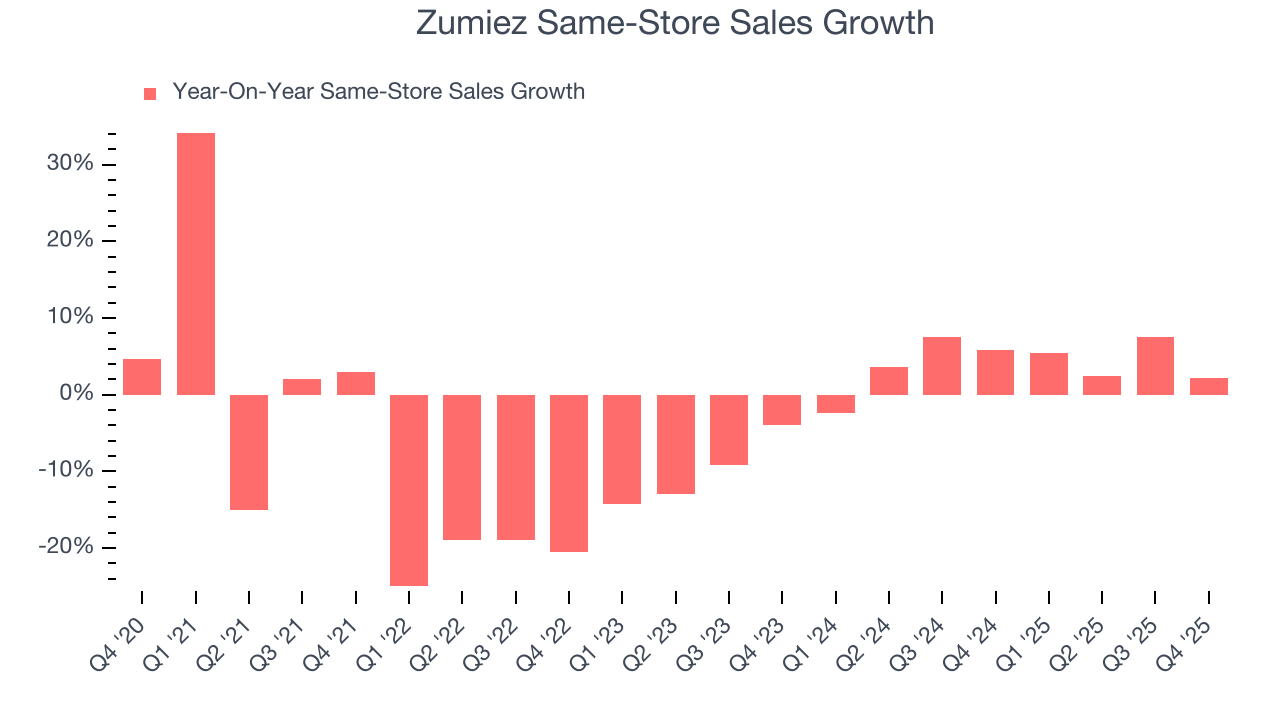

- Same-Store Sales rose 2.2% year on year (5.9% in the same quarter last year)

- Market Capitalization: $392.9 million

Company Overview

With store associates called “Zumiez Stash Members”, Zumiez (NASDAQ:ZUMZ) is a specialty retailer of street and skate apparel, footwear, and accessories.

Customers can also find skateboards, snowboards, and related equipment such as wheels and bindings. The core Zumiez customer is typically a teen or young adult who skates, snowboards, or surfs and wants to reflect these interests in their clothing and footwear choices. Unsurprisingly, brands focused on these subcultures such as Vans, Thrasher, Volcom, and Element are featured in Zumiez stores.

Zumiez stores tend to be small–roughly 3,000 square feet on average–and located in suburban malls and shopping centers. There are various merchandise zones dedicated to apparel, footwear, and hard goods such as skate decks. Two unique aspects of Zumiez stores are video screens or televisions featuring endless loops of action sports as well as interactive areas where customers can handle and lightly try out equipment.

In addition to its physical store footprint, Zumiez also has an e-commerce platform, which was launched in 2005. It allows the company to reach customers that may not have a physical store near them, and it allows customers with access to a store to buy online and pick up physically.

4. Apparel Retailer

Apparel sales are not driven so much by personal needs but by seasons, trends, and innovation, and over the last few decades, the category has shifted meaningfully online. Retailers that once only had brick-and-mortar stores are responding with omnichannel presences. The online shopping experience continues to improve and retail foot traffic in places like shopping malls continues to stall, so the evolution of clothing sellers marches on.

Competitors that offer street or skate apparel and footwear include Tilly’s (NYSE:TLYS), Genesco’s (NYSE:GCO) Journeys banner, Foot Locker (NYSE:FL), and private company PacSun.

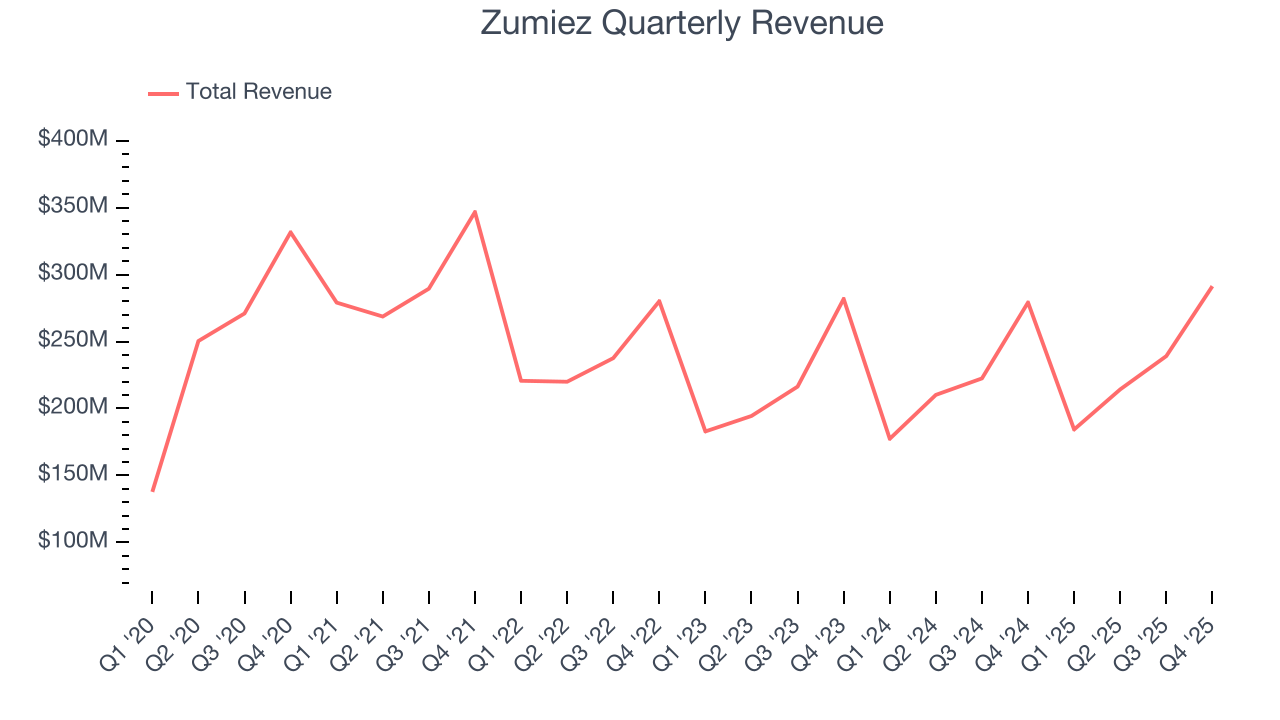

5. Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $929.1 million in revenue over the past 12 months, Zumiez is a small retailer, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with suppliers.

As you can see below, Zumiez’s demand was weak over the last three years. Its sales fell by 1% annually as it closed stores.

This quarter, Zumiez reported modest year-on-year revenue growth of 4.4% but beat Wall Street’s estimates by 0.8%. Company management is currently guiding for a 3.6% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 1.3% over the next 12 months. Although this projection implies its newer products will spur better top-line performance, it is still below the sector average.

6. Store Performance

Number of Stores

The number of stores a retailer operates is a critical driver of how quickly company-level sales can grow.

Zumiez operated 716 locations in the latest quarter. Over the last two years, the company has generally closed its stores, averaging 2.3% annual declines.

When a retailer shutters stores, it usually means that brick-and-mortar demand is less than supply, and it is responding by closing underperforming locations to improve profitability.

Same-Store Sales

The change in a company's store base only tells one side of the story. The other is the performance of its existing locations and e-commerce sales, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales is an industry measure of whether revenue is growing at those existing stores and is driven by customer visits (often called traffic) and the average spending per customer (ticket).

Zumiez’s demand has been spectacular for a retailer over the last two years. On average, the company has increased its same-store sales by an impressive 4% per year. Given its declining store base over the same period, this performance stems from a mixture of higher e-commerce sales and increased foot traffic at existing locations (closing stores can sometimes boost same-store sales).

In the latest quarter, Zumiez’s same-store sales rose 2.2% year on year. This growth was a deceleration from its historical levels, showing the business is still performing well but losing a bit of steam.

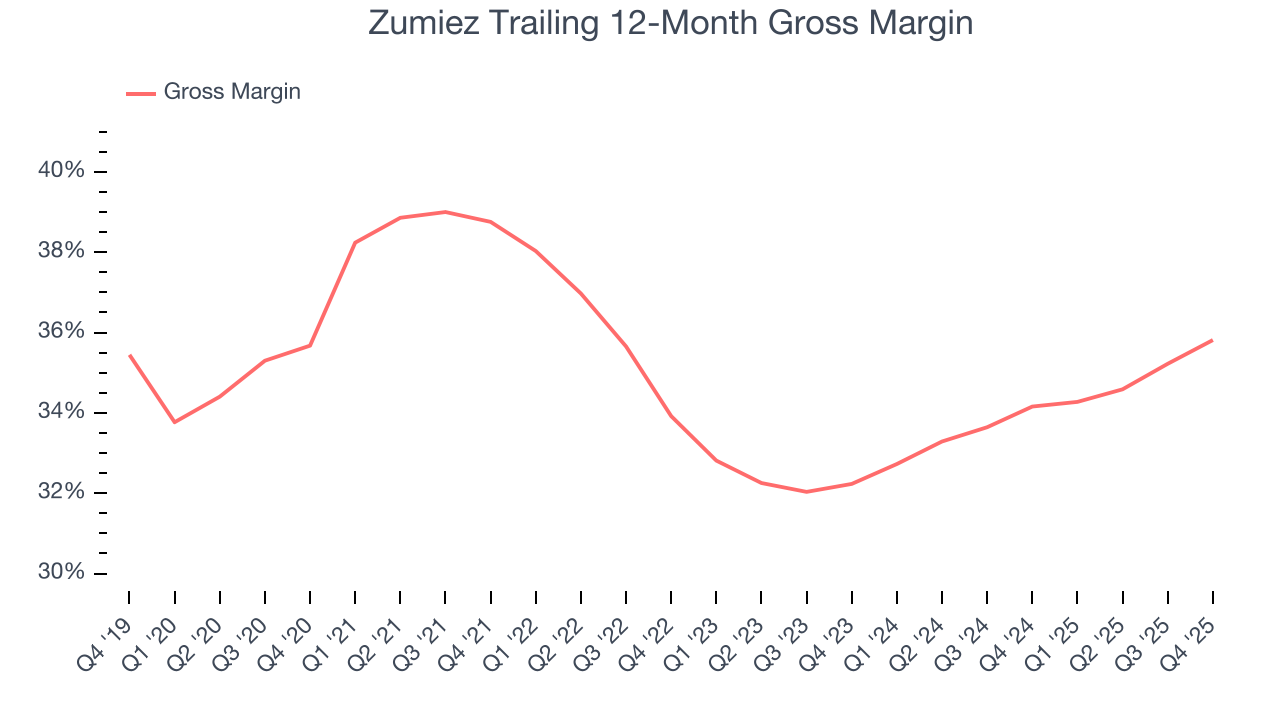

7. Gross Margin & Pricing Power

Zumiez has bad unit economics for a retailer, giving it less room to reinvest and grow its presence. As you can see below, it averaged a 35% gross margin over the last two years. That means Zumiez paid its suppliers a lot of money ($65.00 for every $100 in revenue) to run its business.

In Q4, Zumiez produced a 38.2% gross profit margin , marking a 1.8 percentage point increase from 36.4% in the same quarter last year. Zumiez’s full-year margin has also been trending up over the past 12 months, increasing by 1.7 percentage points. If this move continues, it could suggest better unit economics due to more leverage from its growing sales on the fixed portion of its cost of goods sold.

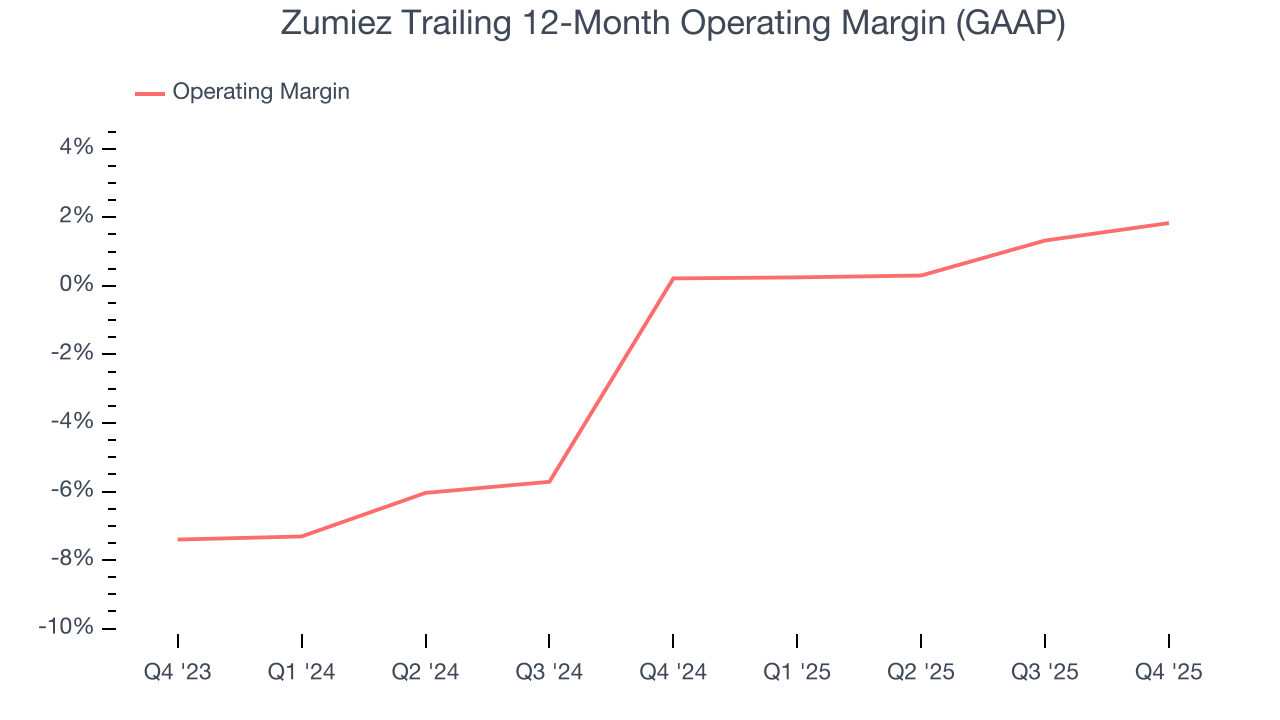

8. Operating Margin

Operating margin is an important measure of profitability for retailers as it accounts for all expenses necessary to run a store, including wages, inventory, rent, advertising, and other administrative costs.

Zumiez was profitable over the last two years but held back by its large cost base. Its average operating margin of 1% was weak for a consumer retail business. This result isn’t too surprising given its low gross margin as a starting point.

On the plus side, Zumiez’s operating margin rose by 1.6 percentage points over the last year.

In Q4, Zumiez generated an operating margin profit margin of 8.6%, up 1.4 percentage points year on year. Since its gross margin expanded more than its operating margin, we can infer that leverage on its cost of sales was the primary driver behind the recently higher efficiency.

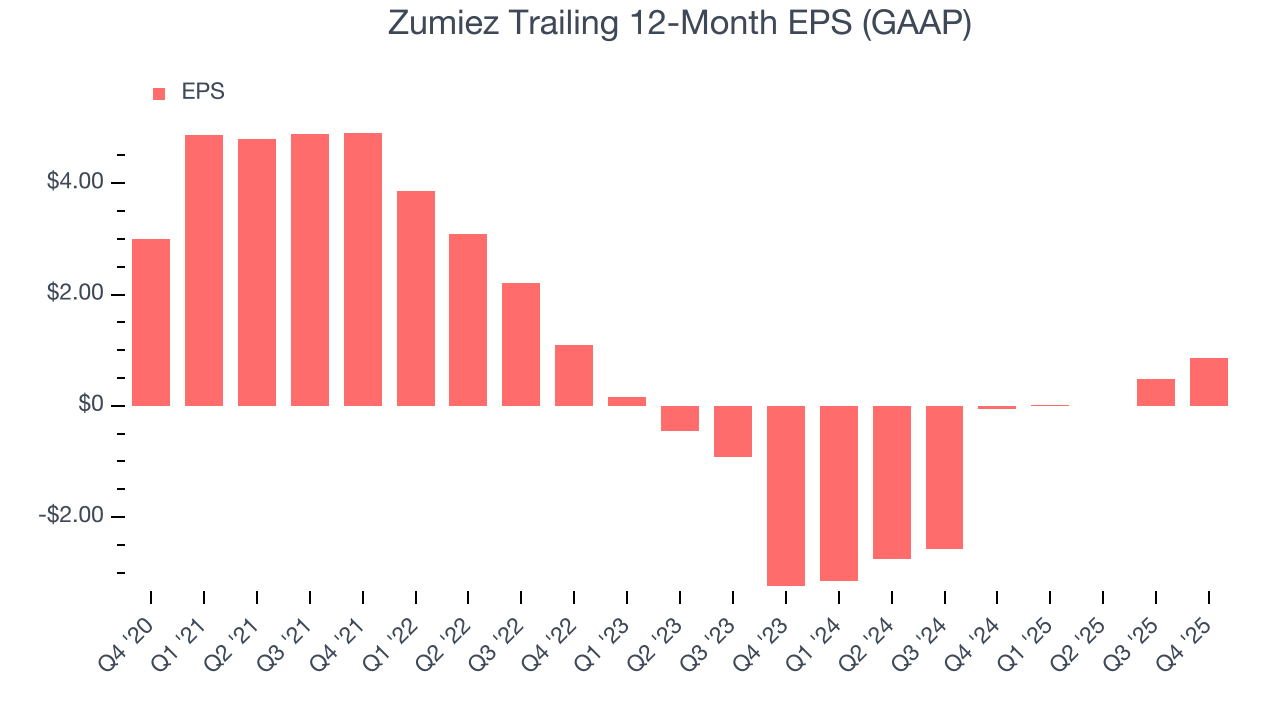

9. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Zumiez, its EPS declined by 7.7% annually over the last three years, more than its revenue. We can see the difference stemmed from higher interest expenses or taxes as the company actually improved its operating margin and repurchased its shares during this time.

In Q4, Zumiez reported EPS of $1.16, up from $0.78 in the same quarter last year. This print beat analysts’ estimates by 8.9%. Over the next 12 months, Wall Street expects Zumiez’s full-year EPS of $0.86 to grow 25.7%.

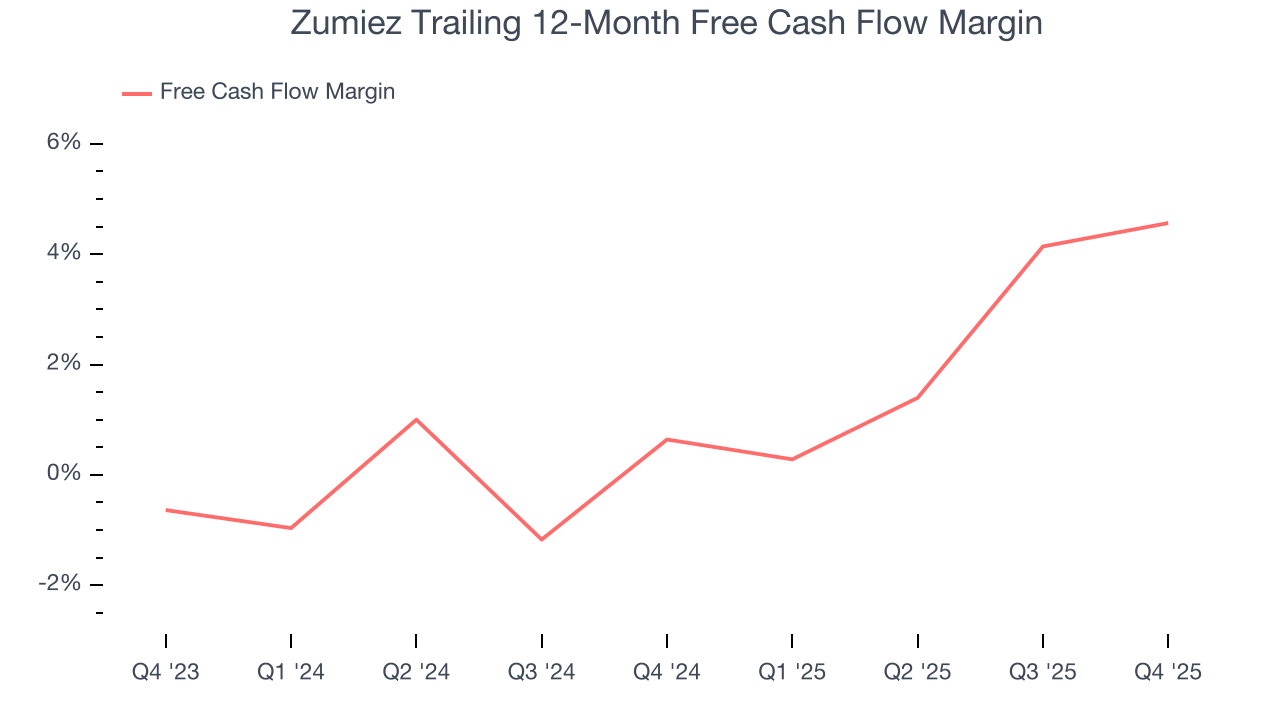

10. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Zumiez has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 2.6% over the last two years, slightly better than the broader consumer retail sector.

Taking a step back, we can see that Zumiez’s margin expanded by 3.9 percentage points over the last year. This shows the company is heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability.

Zumiez’s free cash flow clocked in at $54.14 million in Q4, equivalent to a 18.6% margin. This cash profitability was in line with the comparable period last year and above its two-year average.

11. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Zumiez historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 3.1%, lower than the typical cost of capital (how much it costs to raise money) for consumer retail companies.

12. Balance Sheet Assessment

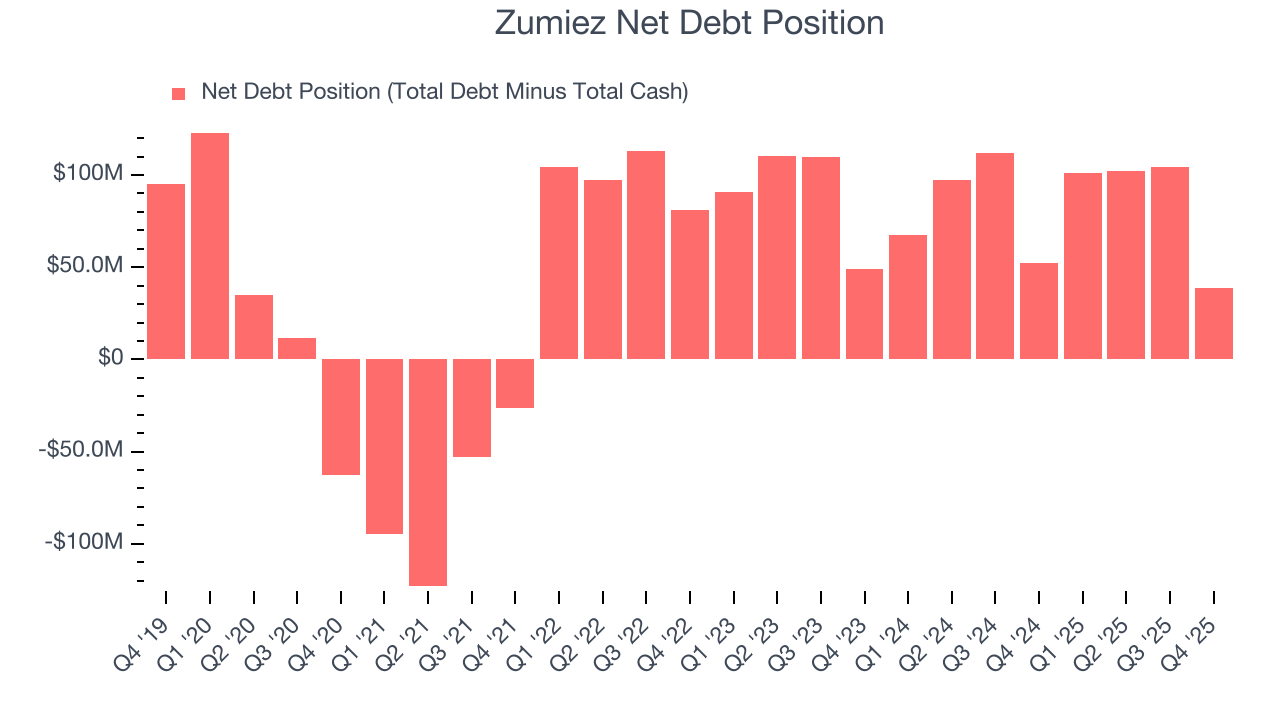

Zumiez reported $160.6 million of cash and $199.3 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $45.44 million of EBITDA over the last 12 months, we view Zumiez’s 0.9× net-debt-to-EBITDA ratio as safe. We also see its $3.11 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

13. Key Takeaways from Zumiez’s Q4 Results

We were impressed by how significantly Zumiez blew past analysts’ EBITDA expectations this quarter. We were also glad its revenue guidance for next quarter exceeded Wall Street’s estimates. On the other hand, its EPS guidance for next quarter missed and its gross margin fell short of Wall Street’s estimates. Overall, this print was mixed but still had some key positives. Investors were likely hoping for more, and shares traded down 6.8% to $21.86 immediately after reporting.

14. Is Now The Time To Buy Zumiez?

Updated: March 13, 2026 at 10:30 PM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Zumiez.

Zumiez falls short of our quality standards. To kick things off, its revenue has declined over the last three years. While its wonderful same-store sales growth is among the best in the consumer retail sector, the downside is its brand caters to a niche market. On top of that, its relatively low ROIC suggests management has struggled to find compelling investment opportunities.

Zumiez’s P/E ratio based on the next 12 months is 25.8x. This valuation tells us a lot of optimism is priced in - you can find more timely opportunities elsewhere.

Wall Street analysts have a consensus one-year price target of $24 on the company (compared to the current share price of $21.39).