Coupang (CPNG)

We’re cautious of Coupang. It not only barely produces cash but also has been less efficient lately, as seen by its falling margins.― StockStory Analyst Team

1. News

2. Summary

Why We Think Coupang Will Underperform

Founded in 2010 by Harvard Business School student Bom Kim, Coupang (NYSE:CPNG) is an e-commerce giant often referred to as the "Amazon of South Korea".

- Bad unit economics and steep infrastructure costs are reflected in its low gross margin of 29.1%

- Poor free cash flow generation means it has few chances to reinvest for growth, repurchase shares, or distribute capital

- A silver lining is that its incremental sales over the last three years have been highly profitable as its earnings per share increased by 62.5% annually, topping its revenue gains

Coupang’s quality is inadequate. We’re hunting for superior stocks elsewhere.

Why There Are Better Opportunities Than Coupang

Coupang’s stock price of $18.41 implies a valuation ratio of 17.6x forward EV/EBITDA. This multiple rich for the business quality. Not a great combination.

It’s better to pay up for high-quality businesses with strong long-term earnings potential rather than to buy lower-quality companies with open questions and big downside risks.

3. Coupang (CPNG) Research Report: Q4 CY2025 Update

Online platform company Coupang (NYSE:CPNG) missed Wall Street’s revenue expectations in Q4 CY2025, but sales rose 10.9% year on year to $8.84 billion. Its GAAP loss of $0.01 per share was significantly below analysts’ consensus estimates.

Coupang (CPNG) Q4 CY2025 Highlights:

- Revenue: $8.84 billion vs analyst estimates of $9.18 billion (10.9% year-on-year growth, 3.8% miss)

- EPS (GAAP): -$0.01 vs analyst estimates of $0.04 (significant miss)

- Adjusted EBITDA: $267 million vs analyst estimates of $271.8 million (3% margin, 1.8% miss)

- Operating Margin: 0.1%, down from 3.9% in the same quarter last year

- Free Cash Flow was -$278 million, down from $442 million in the previous quarter

- Active Customers: 24.6 million, up 1.8 million year on year

- Market Capitalization: $33.54 billion

Company Overview

Founded in 2010 by Harvard Business School student Bom Kim, Coupang (NYSE:CPNG) is an e-commerce giant often referred to as the "Amazon of South Korea".

Coupang revolutionized the online shopping experience in South Korea with its array of products, rapid delivery services, and customer-centric approach.

The company's extensive product range covers various categories including electronics, home goods, beauty products, fashion, groceries, and more. Coupang also operates its own private label brands to fill product assortment gaps with quality goods at competitive prices. In addition to physical goods, the company has expanded into services like video streaming and food delivery, further diversifying its offerings and increasing its appeal to a broad consumer base.

Coupang's rise can be attributed to its logistics and distribution network. The company has invested heavily in its infrastructure, establishing a vast network of warehouses and logistics centers throughout South Korea. This allows Coupang to offer "Rocket Delivery," which guarantees the delivery of millions of items within 24 hours. Unlike other countries, this is possible in South Korea because the country's high population density allows for efficient delivery routes - for example, Seoul only covers about 12% of the country's area but is home to nearly 50% of the population.

A key aspect of Coupang's strategy is its commitment to customer satisfaction. The company offers a no-questions-asked return policy, with most returns picked up directly from customers' homes. This focus on customer service has fostered strong loyalty among Korean consumers and is further amplified by its WOW membership offering, which is similar to Amazon Prime and gives customers additional perks.

4. Online Retail

Consumers ever rising demand for convenience, selection, and speed are secular engines underpinning ecommerce adoption. For years prior to Covid, ecommerce penetration as a percentage of overall retail would grow 1-2% annually, but in 2020 adoption accelerated by 5%, reaching 25%, as increased emphasis on convenience drove consumers to structurally buy more online. The surge in buying caused many online retailers to rapidly grow their logistics infrastructures, preparing them for further growth in the years ahead as consumer shopping habits continue to shift online.

Coupang's Korea-based competitors include Naver (KRX:035420), Lotte Shopping (KRX:023530), and Kakao (KRX:035720). Amazon (NASDAQ:AMZN), Pinduoduo’s Temu (NASDAQ:PDD), and Alibaba’s AliExpress (NYSE:BABA) are also big international players in the market.

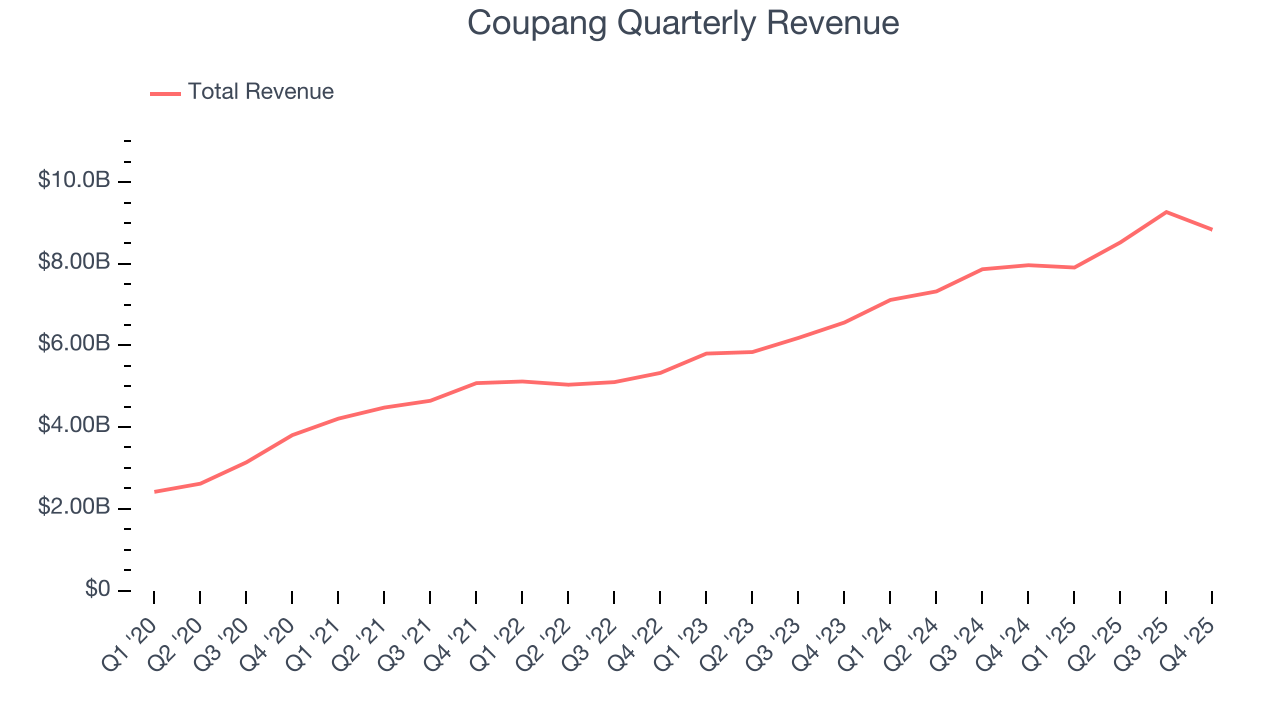

5. Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Luckily, Coupang’s sales grew at an impressive 18.8% compounded annual growth rate over the last three years. Its growth beat the average consumer internet company and shows its offerings resonate with customers.

This quarter, Coupang’s revenue grew by 10.9% year on year to $8.84 billion but fell short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 14.4% over the next 12 months, a deceleration versus the last three years. We still think its growth trajectory is attractive given its scale and suggests the market is forecasting success for its products and services.

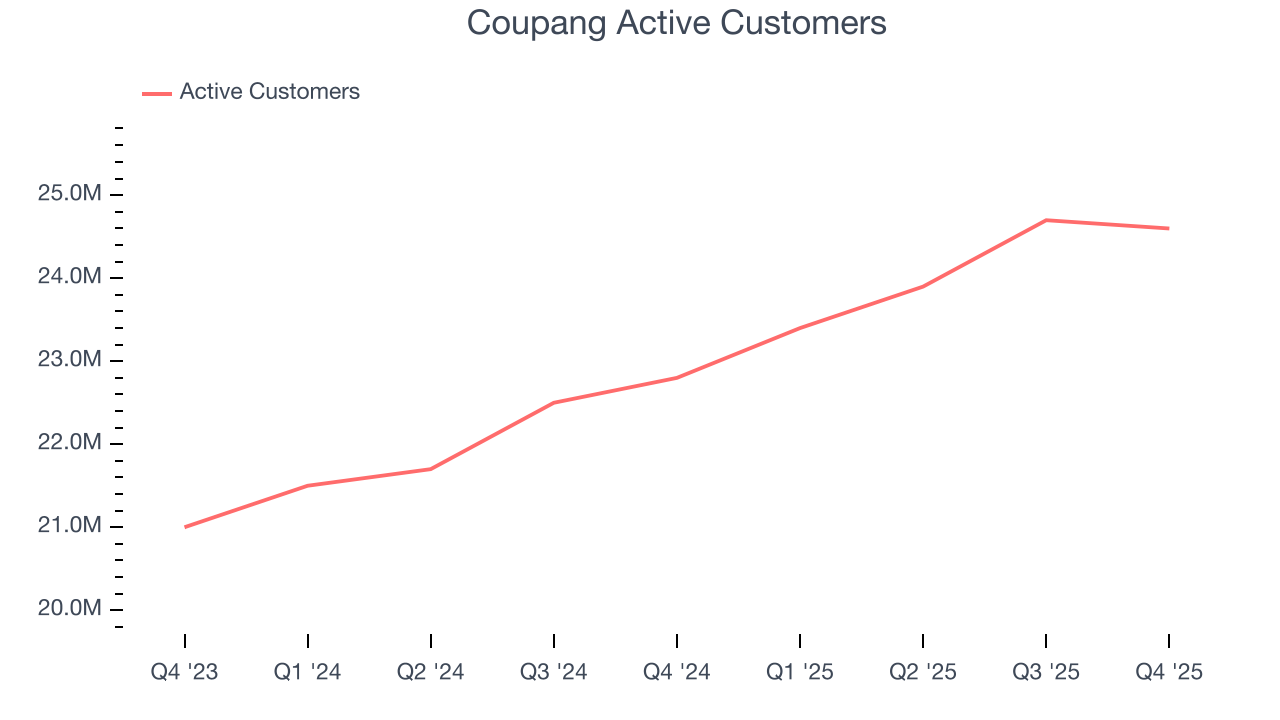

6. Active Customers

Buyer Growth

As an online retailer, Coupang generates revenue growth by expanding its number of users and the average order size in dollars.

Over the last two years, Coupang’s active customers, a key performance metric for the company, increased by 9% annually to 24.6 million in the latest quarter. This growth rate is solid for a consumer internet business and indicates people are excited about its offerings.

In Q4, Coupang added 1.8 million active customers, leading to 7.9% year-on-year growth. The quarterly print was lower than its two-year result, suggesting its new initiatives aren’t accelerating buyer growth just yet.

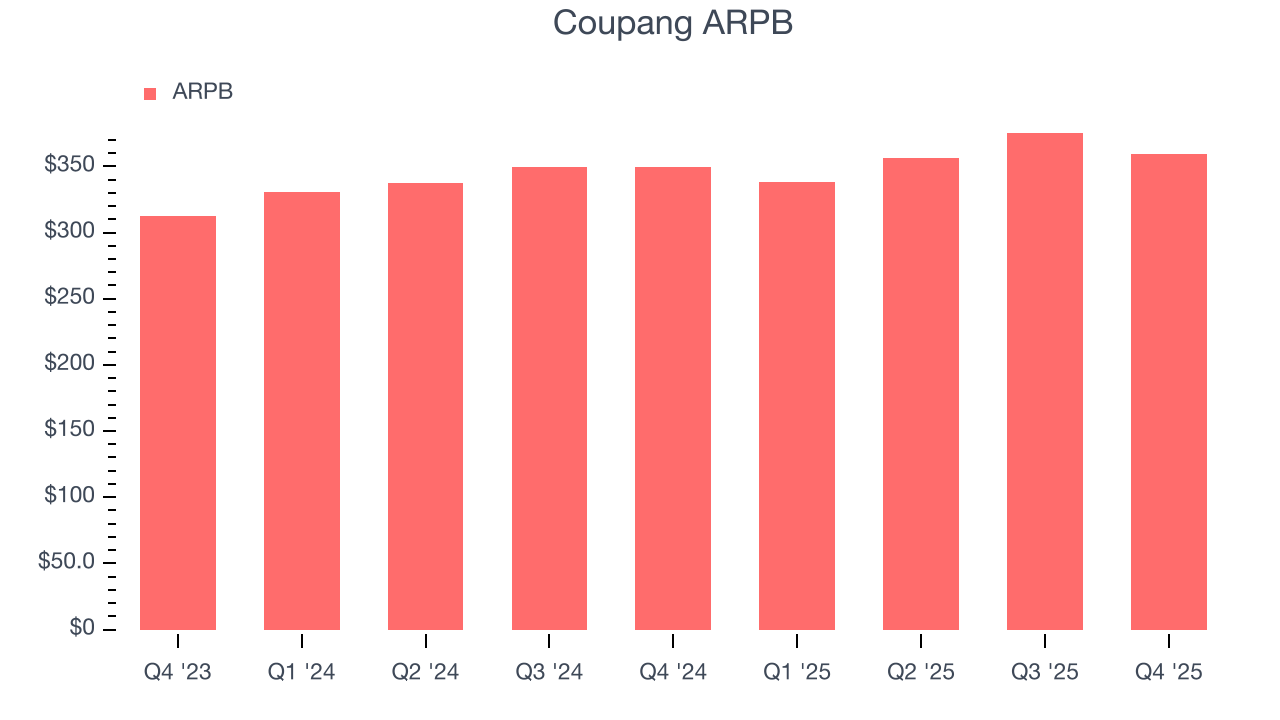

Revenue Per Buyer

Average revenue per buyer (ARPB) is a critical metric to track because it measures how much customers spend per order.

Coupang’s ARPB growth has been decent over the last two years, averaging 6%. Its ability to increase monetization while effectively growing its active customers demonstrates the value of its platform.

This quarter, Coupang’s ARPB clocked in at $359.15. It grew by 2.8% year on year, slower than its buyer growth.

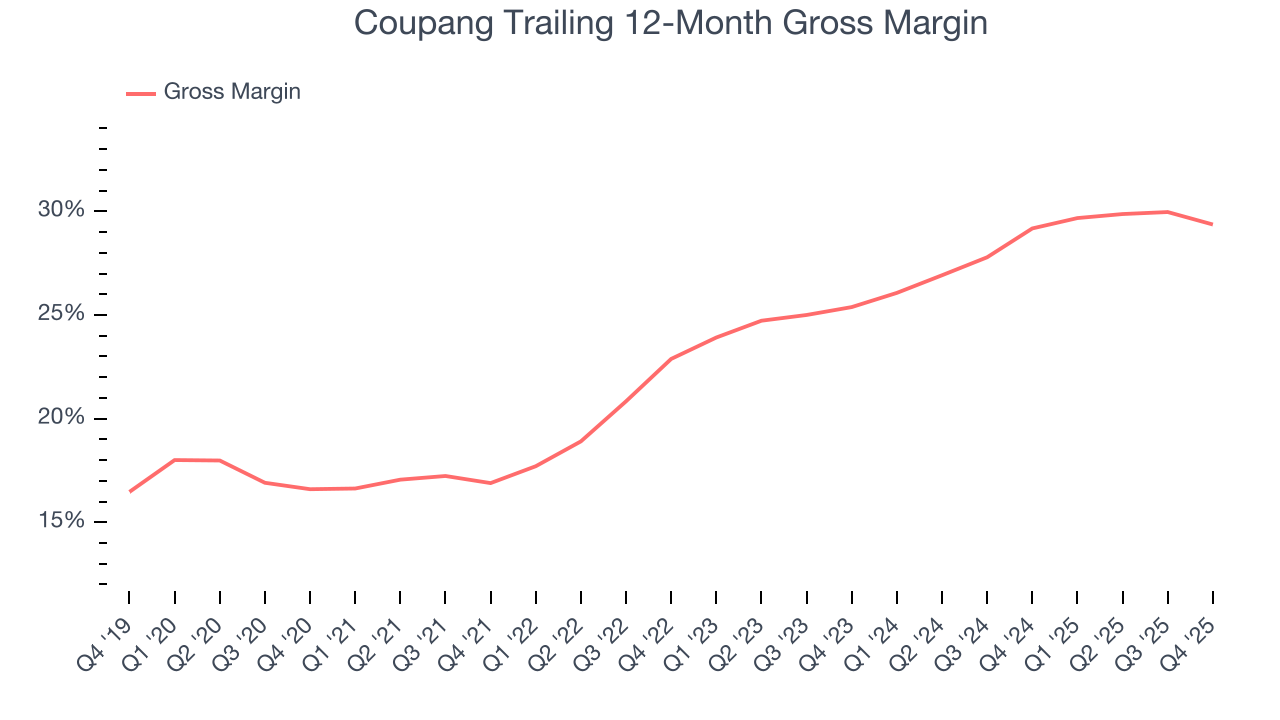

7. Gross Margin & Pricing Power

For online retail (separate from online marketplaces) businesses like Coupang, gross profit tells us how much money the company gets to keep after covering the base cost of its products and services, which typically include the cost of acquiring the products sold, shipping and fulfillment, customer service, and digital infrastructure.

Coupang’s unit economics are far below other consumer internet companies because it must carry inventories as an online retailer. This means it has relatively higher capital intensity than a pure software business like Meta or Airbnb and signals it operates in a competitive market. As you can see below, it averaged a 29.3% gross margin over the last two years. That means Coupang paid its providers a lot of money ($70.72 for every $100 in revenue) to run its business.

Coupang’s gross profit margin came in at 28.8% this quarter, down 2.5 percentage points year on year. Zooming out, the company’s full-year margin has remained steady over the past 12 months, suggesting its input costs have been stable and it isn’t under pressure to lower prices.

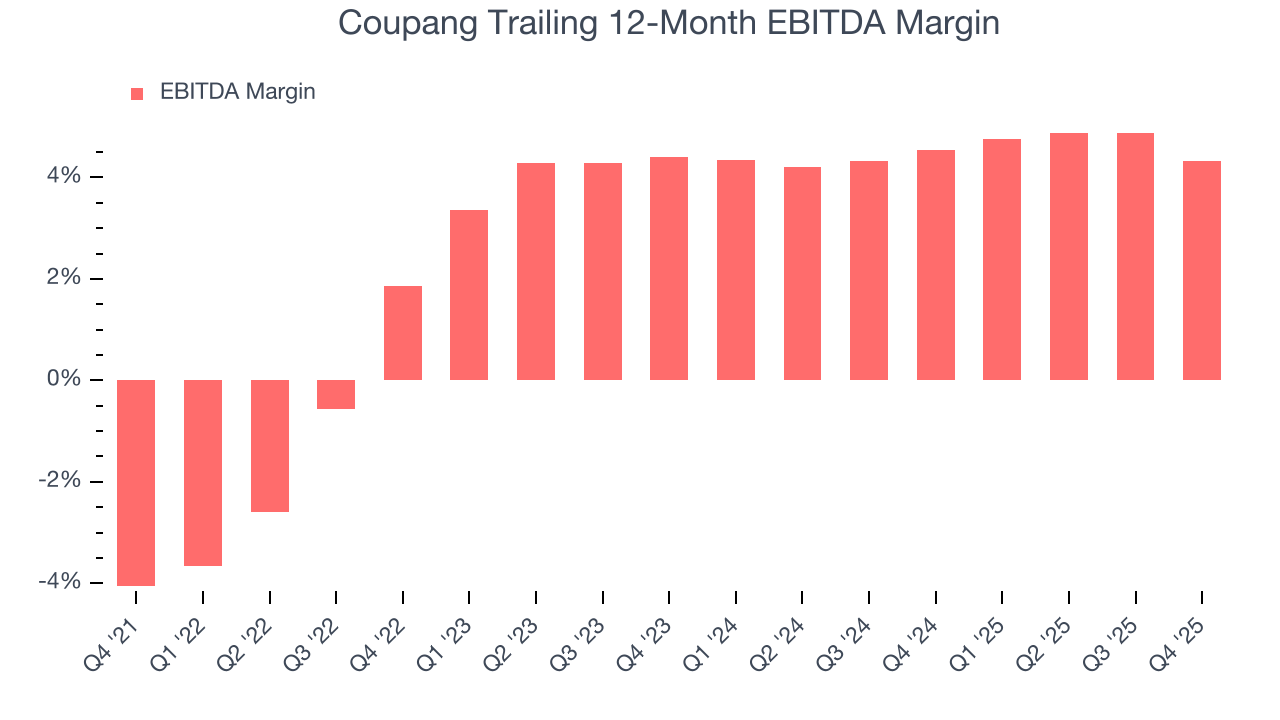

8. EBITDA

Investors frequently analyze operating income to understand a business’s core profitability. Similar to operating income, EBITDA is a common profitability metric for consumer internet companies because it removes various one-time or non-cash expenses, offering a more normalized view of profit potential.

Coupang has managed its cost base well over the last two years. It demonstrated solid profitability for a consumer internet business, producing an average EBITDA margin of 4.4%. This result was particularly impressive because of its low gross margin, which is mostly a factor of what it sells and takes huge shifts to move meaningfully. Companies have more control over their operating margins, and it’s a show of well-managed operations if they’re high when gross margins are low.

Analyzing the trend in its profitability, Coupang’s EBITDA margin rose by 2.5 percentage points over the last few years, as its sales growth gave it operating leverage.

In Q4, Coupang generated an EBITDA margin profit margin of 3%, down 2.3 percentage points year on year. Since Coupang’s gross margin decreased more than its EBITDA margin, we can assume its recent inefficiencies were driven more by weaker leverage on its cost of sales rather than increased marketing, R&D, and administrative overhead expenses.

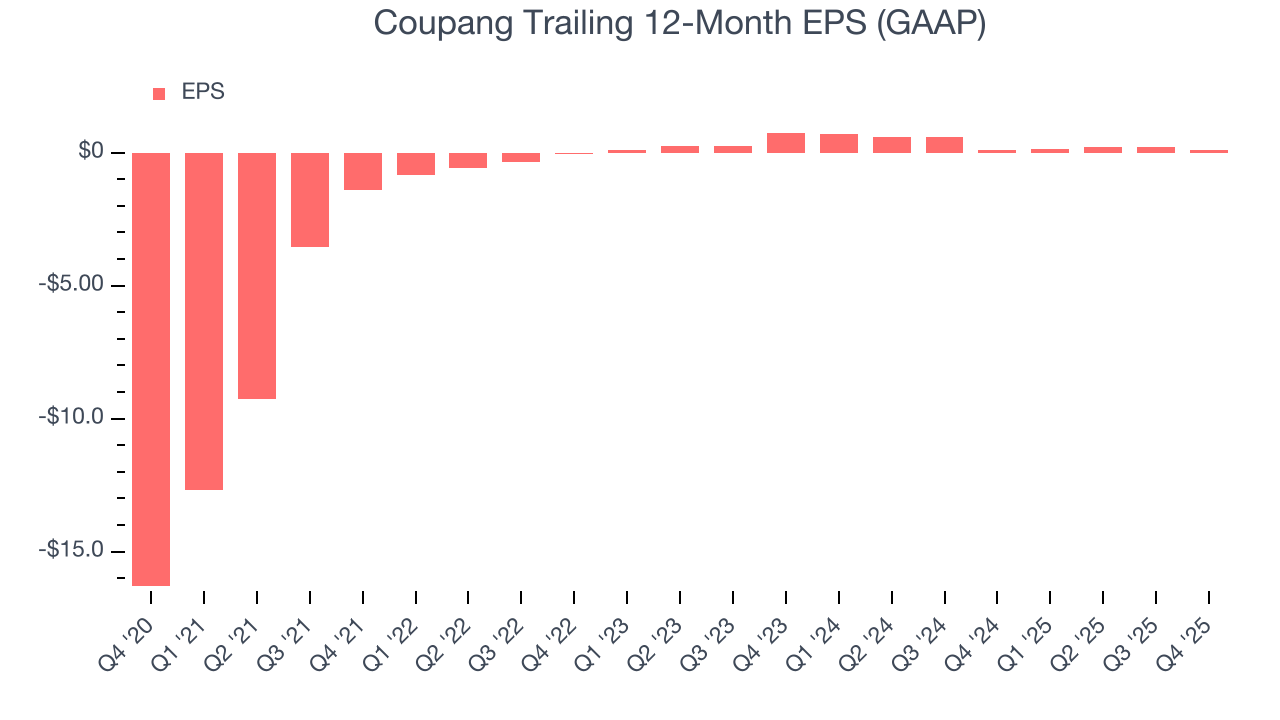

9. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Coupang’s full-year EPS flipped from negative to positive over the last three years. This is a good sign and shows it’s at an inflection point.

In Q4, Coupang reported EPS of negative $0.01, down from $0.08 in the same quarter last year. This print missed analysts’ estimates, but we care more about long-term EPS growth than short-term movements. Over the next 12 months, Wall Street expects Coupang’s full-year EPS of $0.12 to grow 337%.

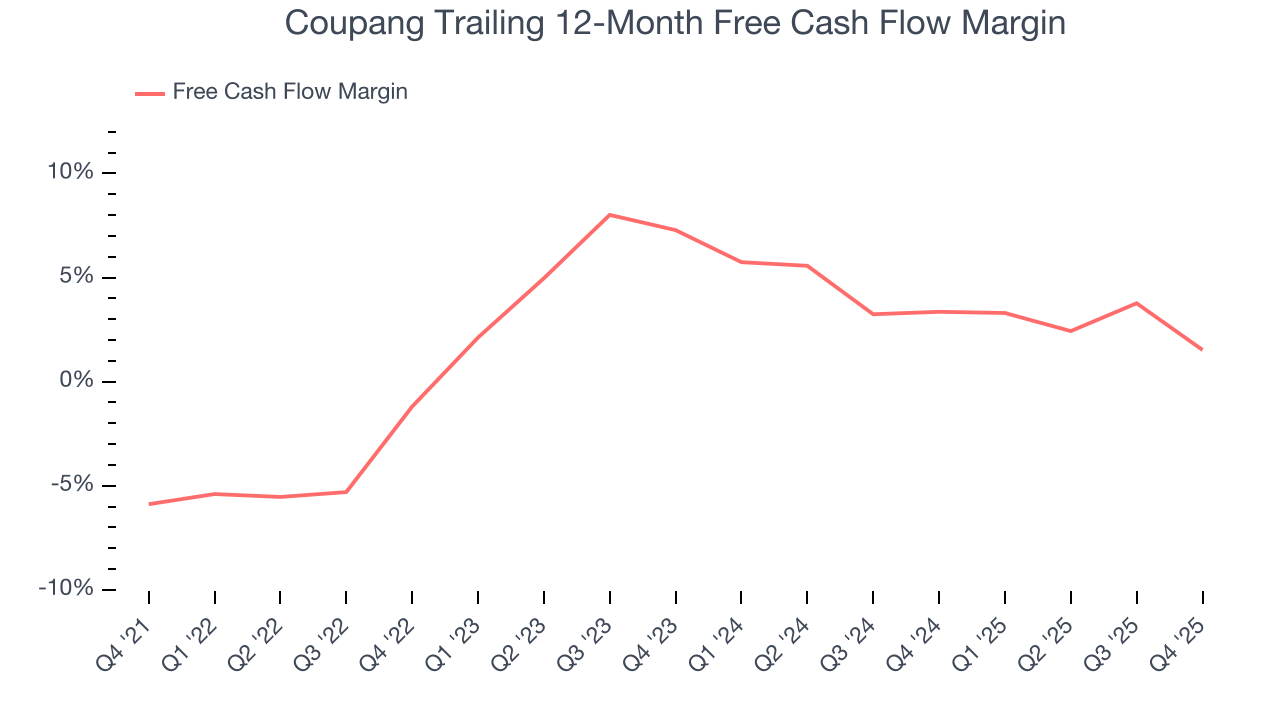

10. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Coupang has shown mediocre cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 2.4%, subpar for a consumer internet business.

Taking a step back, an encouraging sign is that Coupang’s margin expanded by 2.7 percentage points over the last few years. We have no doubt shareholders would like to continue seeing its cash conversion rise as it gives the company more optionality.

Coupang burned through $278 million of cash in Q4, equivalent to a negative 3.1% margin. The company’s cash flow turned negative after being positive in the same quarter last year, but we wouldn’t read too much into it because capital expenditures can be seasonal and companies often stockpile inventory in anticipation of higher demand, leading to quarter-to-quarter swings. Long-term trends are more important.

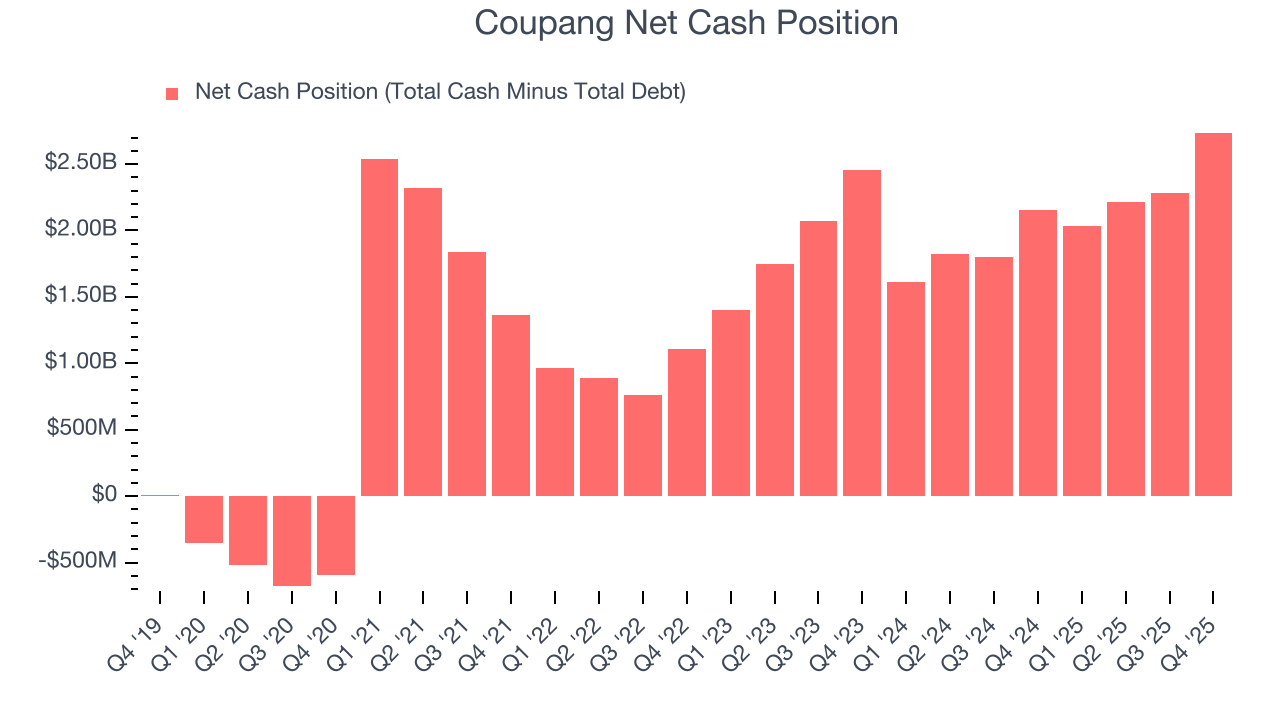

11. Balance Sheet Assessment

Companies with more cash than debt have lower bankruptcy risk.

Coupang is a profitable, well-capitalized company with $6.41 billion of cash and $3.68 billion of debt on its balance sheet. This $2.74 billion net cash position is 8.2% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

12. Key Takeaways from Coupang’s Q4 Results

We struggled to find many positives in these results. Its revenue missed and its EBITDA fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 2.7% to $18.18 immediately after reporting.

13. Is Now The Time To Buy Coupang?

Updated: March 15, 2026 at 10:06 PM EDT

Before deciding whether to buy Coupang or pass, we urge investors to consider business quality, valuation, and the latest quarterly results.

Coupang’s business quality ultimately falls short of our standards. Although its revenue growth was impressive over the last three years, it’s expected to deteriorate over the next 12 months and its projected EPS for the next year is lacking. And while the company’s EPS growth over the last three years has been fantastic, the downside is its gross margins make it extremely difficult to reach positive operating profits compared to other consumer internet businesses.

Coupang’s EV/EBITDA ratio based on the next 12 months is 17.6x. At this valuation, there’s a lot of good news priced in - we think there are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $27.27 on the company (compared to the current share price of $18.41).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.