Doximity (DOCS)

Doximity catches our eye. Its blend of high growth and outstanding profitability makes for a nice return algorithm.― StockStory Analyst Team

1. News

2. Summary

Why Doximity Is Interesting

With over 80% of U.S. physicians as members of its digital community, Doximity (NYSE:DOCS) operates a digital platform that enables physicians and other healthcare professionals to collaborate, stay current with medical news, manage their careers, and conduct virtual patient visits.

- Software is difficult to replicate at scale and results in a best-in-class gross margin of 89.7%

- Healthy operating margin shows it’s a well-run company with efficient processes

- On the other hand, its costs have risen faster than its revenue over the last year, causing its operating margin to decline by 2.7 percentage points

Doximity shows some signs of a high-quality business. If you like the stock, the price seems fair.

Why Is Now The Time To Buy Doximity?

Doximity is trading at $24.31 per share, or 7.2x forward price-to-sales. Scanning the software landscape, we think the price is reasonable for the revenue growth you get.

If you think the market is not giving the company enough credit for its fundamentals, now could be a good time to invest.

3. Doximity (DOCS) Research Report: Q4 CY2025 Update

Medical professional network Doximity (NYSE:DOCS) beat Wall Street’s revenue expectations in Q4 CY2025, with sales up 9.8% year on year to $185.1 million. On the other hand, next quarter’s revenue guidance of $143.5 million was less impressive, coming in 5.2% below analysts’ estimates. Its non-GAAP profit of $0.46 per share was 2.9% above analysts’ consensus estimates.

Doximity (DOCS) Q4 CY2025 Highlights:

- Revenue: $185.1 million vs analyst estimates of $181.5 million (9.8% year-on-year growth, 2% beat)

- Adjusted EPS: $0.46 vs analyst estimates of $0.45 (2.9% beat)

- Adjusted Operating Income: $109.3 million vs analyst estimates of $102.1 million (59.1% margin, 7.1% beat)

- Revenue Guidance for Q1 CY2026 is $143.5 million at the midpoint, below analyst estimates of $151.3 million

- EBITDA guidance for the full year is $356 million at the midpoint, in line with analyst expectations

- Operating Margin: 38.9%, down from 47.4% in the same quarter last year

- Free Cash Flow Margin: 31.6%, down from 54.3% in the previous quarter

- Market Capitalization: $6.64 billion

Company Overview

With over 80% of U.S. physicians as members of its digital community, Doximity (NYSE:DOCS) operates a digital platform that enables physicians and other healthcare professionals to collaborate, stay current with medical news, manage their careers, and conduct virtual patient visits.

The platform functions as a specialized professional network tailored specifically for the medical community, offering features like digital CVs, secure messaging, clinical discussions, and peer connections. While free for healthcare professionals, Doximity generates revenue through subscription-based solutions marketed to pharmaceutical companies and health systems.

These revenue streams include Marketing Solutions, which allow pharmaceutical manufacturers and health systems to deliver targeted content to relevant medical specialists; Hiring Solutions, which help healthcare employers identify and recruit medical talent; and Productivity Solutions, which provide enterprise-level tools to streamline clinical workflows.

For example, a pharmaceutical company might use Doximity to share clinical trial results for a new diabetes medication specifically with endocrinologists in certain regions, while a hospital network might leverage the platform to recruit cardiologists for its expanding heart center. The platform's telehealth tools also allow physicians to conduct patient video calls without revealing their personal phone numbers, while its AI writing assistant helps draft patient documentation and correspondence.

With a network that includes most U.S. physicians, nurse practitioners, physician assistants, and medical students, Doximity benefits from strong network effects—as more professionals join and engage with the platform, its value increases for both members and customers. The company continues to expand its offerings beyond physicians to other healthcare professionals, while developing new productivity tools and enterprise solutions.

4. Healthcare And Life Sciences Software

The coronavirus pandemic has underscored the importance of high-quality health infrastructure in times of crisis. Coupled with intense competition between drugmakers and the growing volume of data in the health care sector, demand for data management solutions in the healthcare space is expected to remain strong in the years ahead.

Doximity's competitors include broad professional networks like LinkedIn (owned by Microsoft, NASDAQ:MSFT) and Facebook (Meta Platforms, NASDAQ:META), as well as healthcare-specific platforms like Sermo and Figure 1. In the telehealth space, they compete with Teladoc Health (NYSE:TDOC) and Amwell (NYSE:AMWL), while their scheduling tools face competition from QGenda.

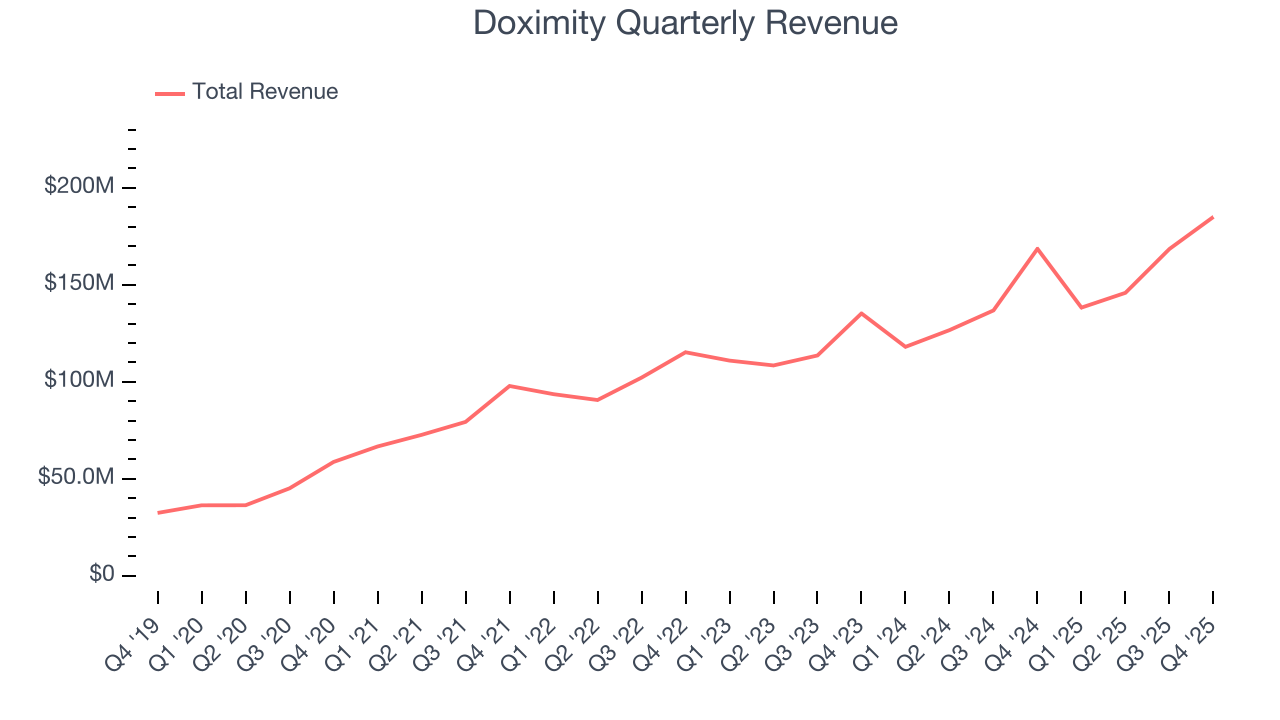

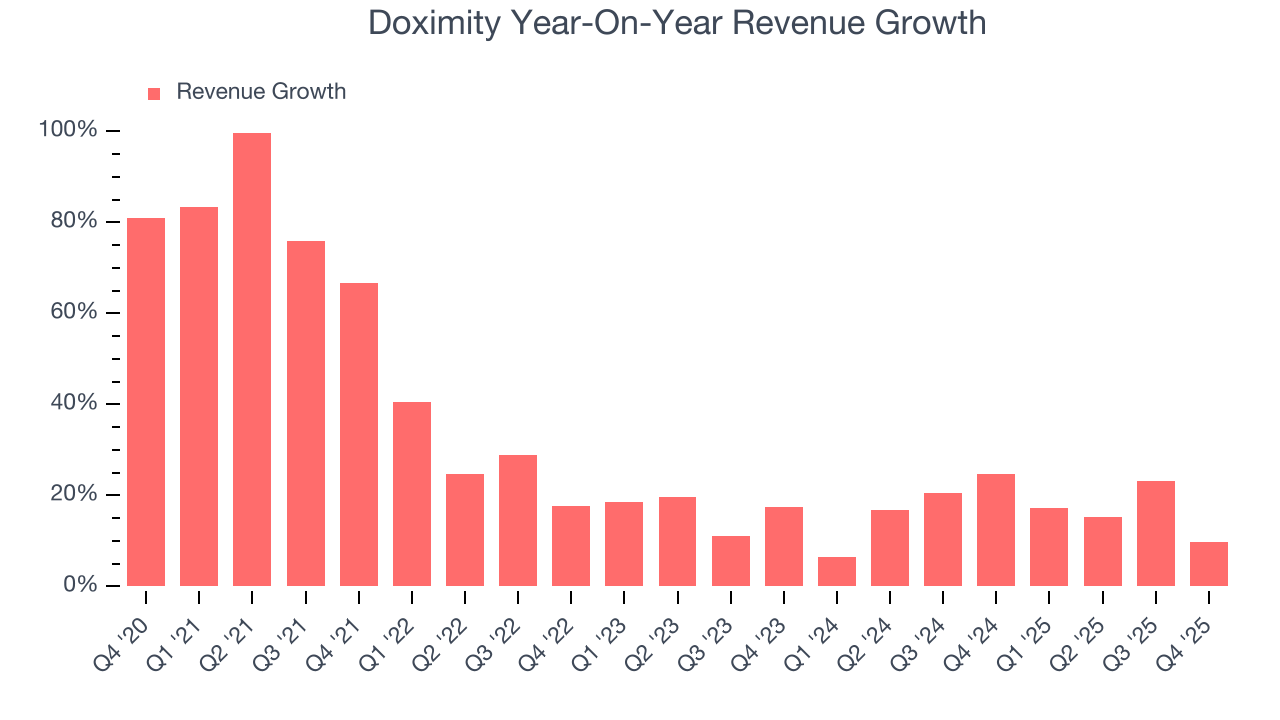

5. Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Luckily, Doximity’s sales grew at an impressive 29.3% compounded annual growth rate over the last five years. Its growth surpassed the average software company and shows its offerings resonate with customers, a great starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within software, a half-decade historical view may miss recent innovations or disruptive industry trends. Doximity’s annualized revenue growth of 16.7% over the last two years is below its five-year trend, but we still think the results were respectable.

This quarter, Doximity reported year-on-year revenue growth of 9.8%, and its $185.1 million of revenue exceeded Wall Street’s estimates by 2%. Company management is currently guiding for a 3.8% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 9% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and indicates its products and services will see some demand headwinds. At least the company is tracking well in other measures of financial health.

6. Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

Doximity is extremely efficient at acquiring new customers, and its CAC payback period checked in at 6.4 months this quarter. The company’s rapid recovery of its customer acquisition costs indicates it has a highly differentiated product offering and a strong brand reputation. These dynamics give Doximity more resources to pursue new product initiatives while maintaining the flexibility to increase its sales and marketing investments.

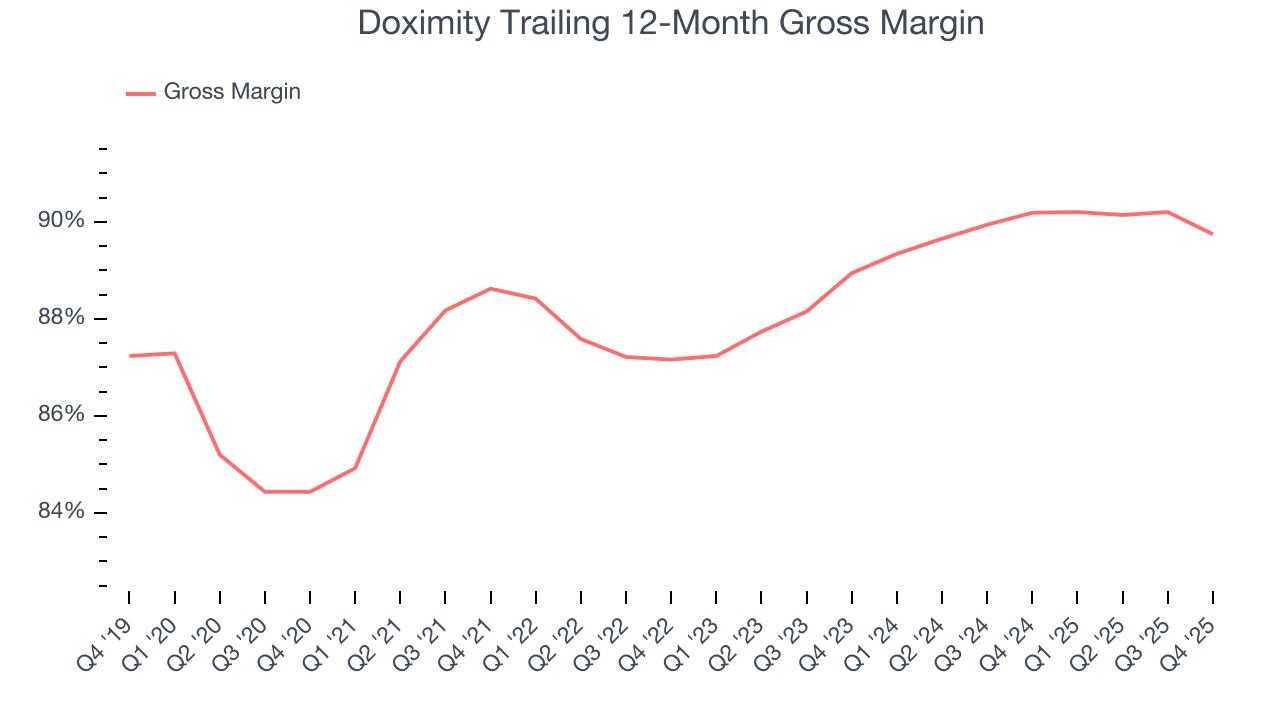

7. Gross Margin & Pricing Power

Software is eating the world. It’s one of our favorite business models because once you develop the product, it usually doesn’t cost much to provide it as an ongoing service. These minimal costs can include servers, licenses, and certain personnel.

Doximity’s gross margin is one of the best in the software sector, an output of its asset-lite business model and strong pricing power. It also enables the company to fund large investments in new products and sales during periods of rapid growth to achieve higher profits in the future. As you can see below, it averaged an elite 89.7% gross margin over the last year. Said differently, roughly $89.75 was left to spend on selling, marketing, and R&D for every $100 in revenue.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. Doximity has seen gross margins improve by 0.8 percentage points over the last 2 year, which is slightly better than average for software.

Doximity produced a 89.9% gross profit margin in Q4, marking a 1.7 percentage point decrease from 91.6% in the same quarter last year. On a wider time horizon, the company’s full-year margin has remained steady over the past four quarters, suggesting its input costs have been stable and it isn’t under pressure to lower prices.

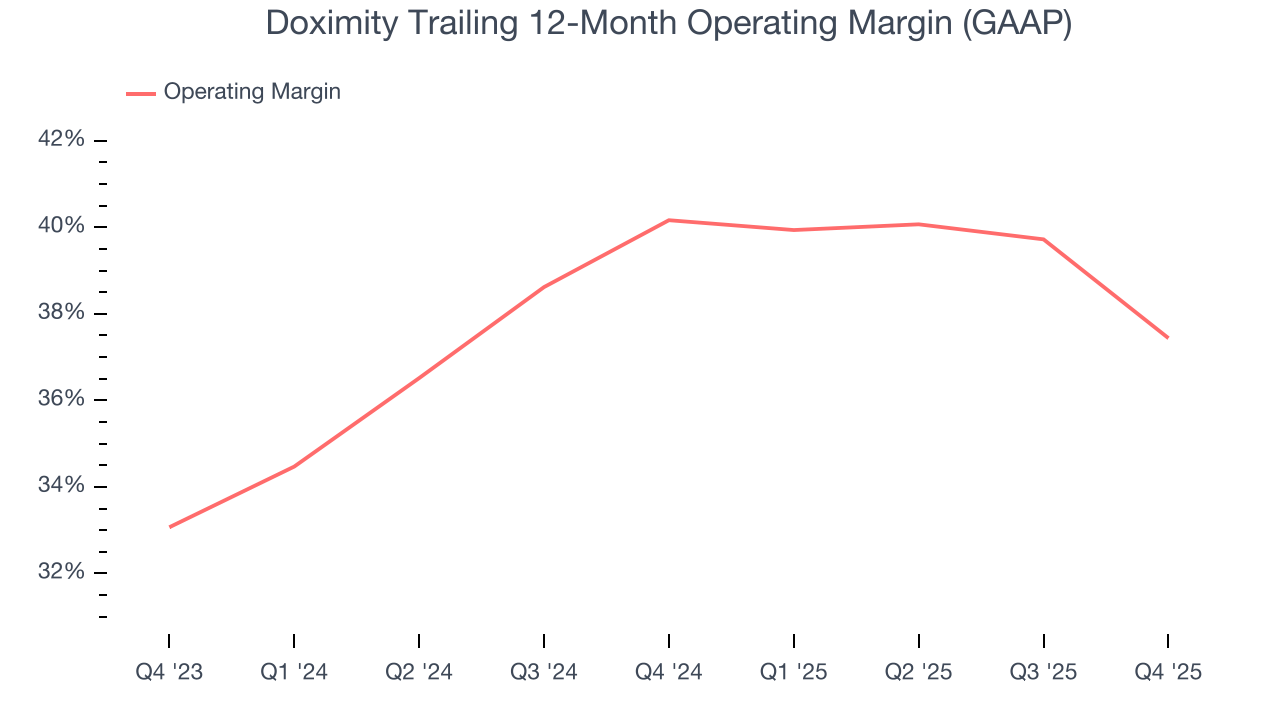

8. Operating Margin

Doximity has been a well-oiled machine over the last year. It demonstrated elite profitability for a software business, boasting an average operating margin of 37.4%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Looking at the trend in its profitability, Doximity’s operating margin decreased by 2.7 percentage points over the last two years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q4, Doximity generated an operating margin profit margin of 38.9%, down 8.6 percentage points year on year. Since Doximity’s operating margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, R&D, and administrative overhead increased.

9. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

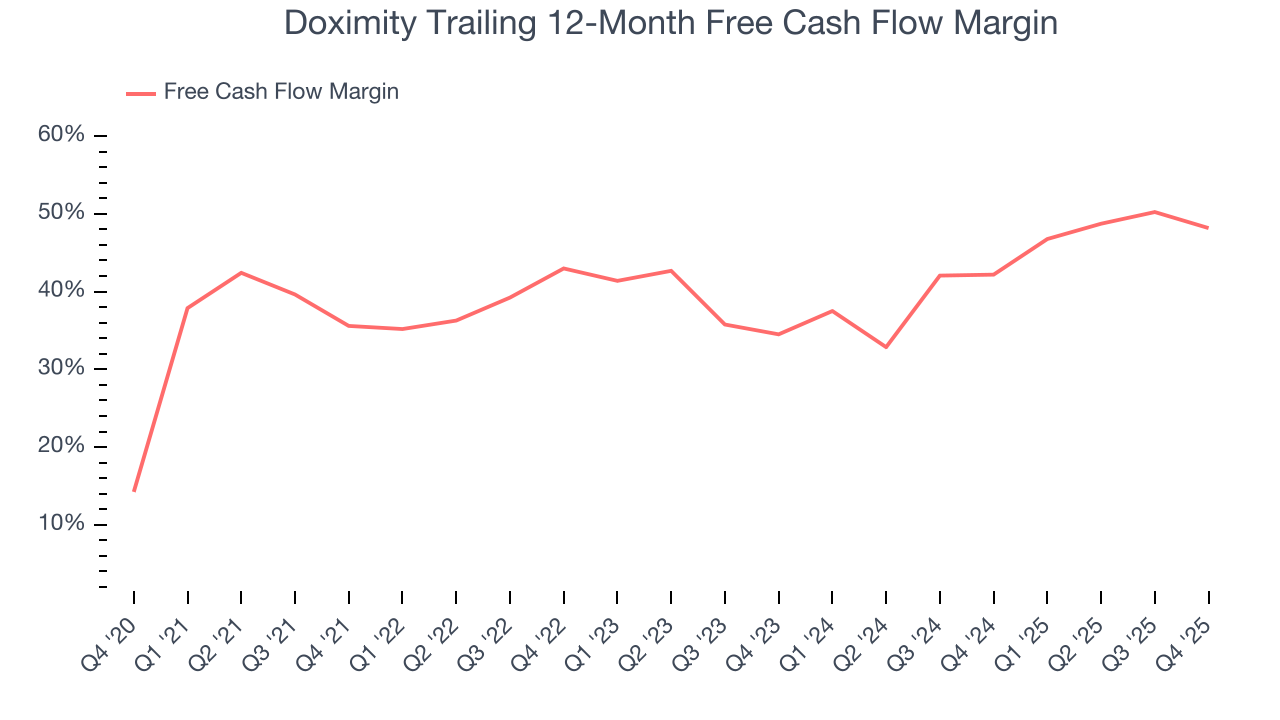

Doximity has shown terrific cash profitability, driven by its lucrative business model and cost-effective customer acquisition strategy that enable it to stay ahead of the competition through investments in new products rather than sales and marketing. The company’s free cash flow margin was among the best in the software sector, averaging an eye-popping 48.2% over the last year.

Doximity’s free cash flow clocked in at $58.52 million in Q4, equivalent to a 31.6% margin. The company’s cash profitability regressed as it was 6 percentage points lower than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, leading to temporary swings. Long-term trends carry greater meaning.

Over the next year, analysts’ consensus estimates show they’re expecting Doximity’s free cash flow margin of 48.2% for the last 12 months to remain the same.

10. Balance Sheet Assessment

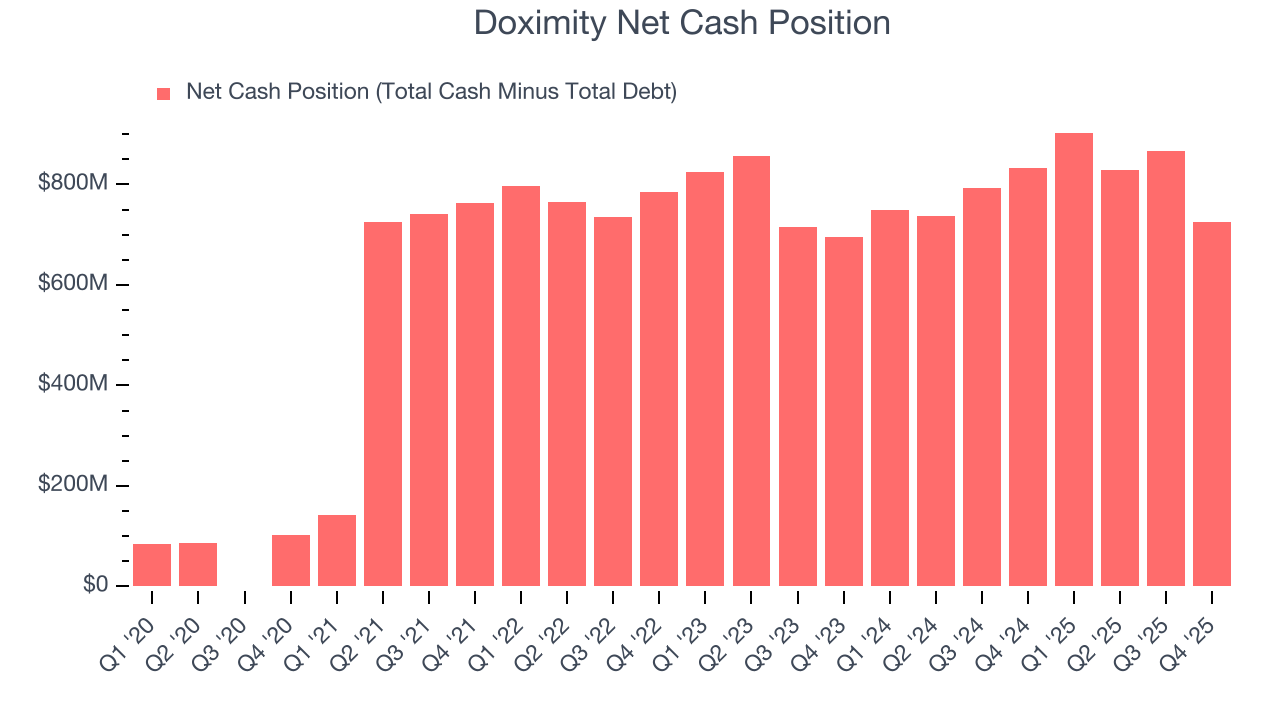

One of the best ways to mitigate bankruptcy risk is to hold more cash than debt.

Doximity is a profitable, well-capitalized company with $735.1 million of cash and $10.69 million of debt on its balance sheet. This $724.4 million net cash position is 10.9% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

11. Key Takeaways from Doximity’s Q4 Results

We enjoyed seeing Doximity beat analysts’ EBITDA expectations this quarter. We were also happy its revenue outperformed Wall Street’s estimates. On the other hand, its revenue guidance for next quarter missed and its EBITDA guidance for next quarter fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 32.5% to $22.50 immediately after reporting.

12. Is Now The Time To Buy Doximity?

Updated: March 13, 2026 at 10:33 PM EDT

Are you wondering whether to buy Doximity or pass? We urge investors to not only consider the latest earnings results but also longer-term business quality and valuation as well.

There’s plenty to admire about Doximity. To kick things off, its revenue growth was strong over the last five years. And while its declining operating margin shows it’s becoming less efficient at building and selling its software, its bountiful generation of free cash flow empowers it to invest in growth initiatives. On top of that, its admirable gross margin indicates excellent unit economics.

Doximity’s price-to-sales ratio based on the next 12 months is 7.2x. Looking at the software space right now, Doximity trades at a compelling valuation. If you’re a fan of the business and management team, now is a good time to scoop up some shares.

Wall Street analysts have a consensus one-year price target of $39.95 on the company (compared to the current share price of $24.31), implying they see 64.3% upside in buying Doximity in the short term.