Korn Ferry (KFY)

Korn Ferry doesn’t impress us. Its weak sales growth and declining returns on capital show its demand and profits are shrinking.― StockStory Analyst Team

1. News

2. Summary

Why Korn Ferry Is Not Exciting

With clients including 97% of the S&P 100 and operations in 103 offices across 51 countries, Korn Ferry (NYSE:KFY) is a global consulting firm that helps organizations design optimal structures, recruit talent, develop leaders, and create effective compensation strategies.

- Anticipated sales growth of 3.7% for the next year implies demand will be shaky

- The good news is that its earnings per share have outperformed its peers over the last five years, increasing by 41.6% annually

Korn Ferry is in the penalty box. We’re hunting for superior stocks elsewhere.

Why There Are Better Opportunities Than Korn Ferry

Korn Ferry is trading at $60.49 per share, or 10.8x forward P/E. This multiple is cheaper than most business services peers, but we think this is justified.

We’d rather pay up for companies with elite fundamentals than get a bargain on weak ones. Cheap stocks can be value traps, and as their performance deteriorates, they will stay cheap or get even cheaper.

3. Korn Ferry (KFY) Research Report: Q4 CY2025 Update

Organizational consulting firm Korn Ferry (NYSE:KFY) reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 7.2% year on year to $725 million. On the other hand, next quarter’s revenue guidance of $740 million was less impressive, coming in 1% below analysts’ estimates. Its GAAP profit of $1.23 per share was in line with analysts’ consensus estimates.

Korn Ferry (KFY) Q4 CY2025 Highlights:

- Revenue: $725 million vs analyst estimates of $708.8 million (7.2% year-on-year growth, 2.3% beat)

- EPS (GAAP): $1.23 vs analyst estimates of $1.23 (in line)

- Adjusted EBITDA: $123.1 million vs analyst estimates of $120.3 million (17% margin, 2.4% beat)

- Revenue Guidance for Q1 CY2026 is $740 million at the midpoint, below analyst estimates of $747.6 million

- EPS (GAAP) guidance for Q1 CY2026 is $1.37 at the midpoint, missing analyst estimates by 1.1%

- Operating Margin: 12.6%, in line with the same quarter last year

- Market Capitalization: $3.32 billion

Company Overview

With clients including 97% of the S&P 100 and operations in 103 offices across 51 countries, Korn Ferry (NYSE:KFY) is a global consulting firm that helps organizations design optimal structures, recruit talent, develop leaders, and create effective compensation strategies.

Korn Ferry's business spans five core capabilities: organizational strategy, assessment and succession, talent acquisition, leadership development, and total rewards. The company serves as a strategic partner throughout the entire talent lifecycle, from helping clients design their organizational structures to recruiting executives and developing their leadership teams.

For organizational strategy, Korn Ferry maps talent strategy to business strategy, designing operating models that help companies execute their plans. Its assessment solutions identify growth opportunities for leaders and employees, while its talent acquisition services include executive search, professional search, interim staffing, and recruitment process outsourcing.

A typical client might engage Korn Ferry to restructure their organization following a merger, with the firm designing the new organizational chart, assessing existing leadership for key roles, recruiting new executives where needed, and developing comprehensive compensation packages to retain top talent.

The company monetizes its expertise through consulting services and subscription-based digital products. Its technology platform includes tools like Profile Manager (defining role requirements), Architect (organization structure planning), Assess (evaluating individual capabilities), Engage (employee feedback), Pay (compensation benchmarking), and Sell (sales methodology).

Korn Ferry also offers specialized solutions for workforce transformation, cost optimization, M&A integration, culture change, career transition, inclusion initiatives, and sales effectiveness. The company maintains a research arm, the Korn Ferry Institute, which develops proprietary intellectual property and analytics that inform its consulting work and digital products.

4. Professional Staffing & HR Solutions

The Professional Staffing & HR Solutions subsector within Business Services is set to benefit from evolving workforce trends, including the rise of remote work and the gig economy. With companies casting a wider net to find talent due to remote work, the expertise of staffing and recruiting companies is even more valuable. For those who invest wisely, the use of predictive AI in recruitment and screening as well as automation in HR workflows can enhance efficiency and scalability. On the other hand, digitization means that talent discovery is less of a manual process, opening the door for tech-first platforms. Additionally, regulatory scrutiny around data privacy in HR is evolving and may require companies in this sector to change their go-to-market strategies over time.

Korn Ferry competes with global consulting firms like Aon, Mercer, Willis Towers Watson, McKinsey, and Deloitte in the organizational consulting space. In executive search, its competitors include Egon Zehnder, Heidrick & Struggles, Russell Reynolds Associates, and Spencer Stuart.

5. Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

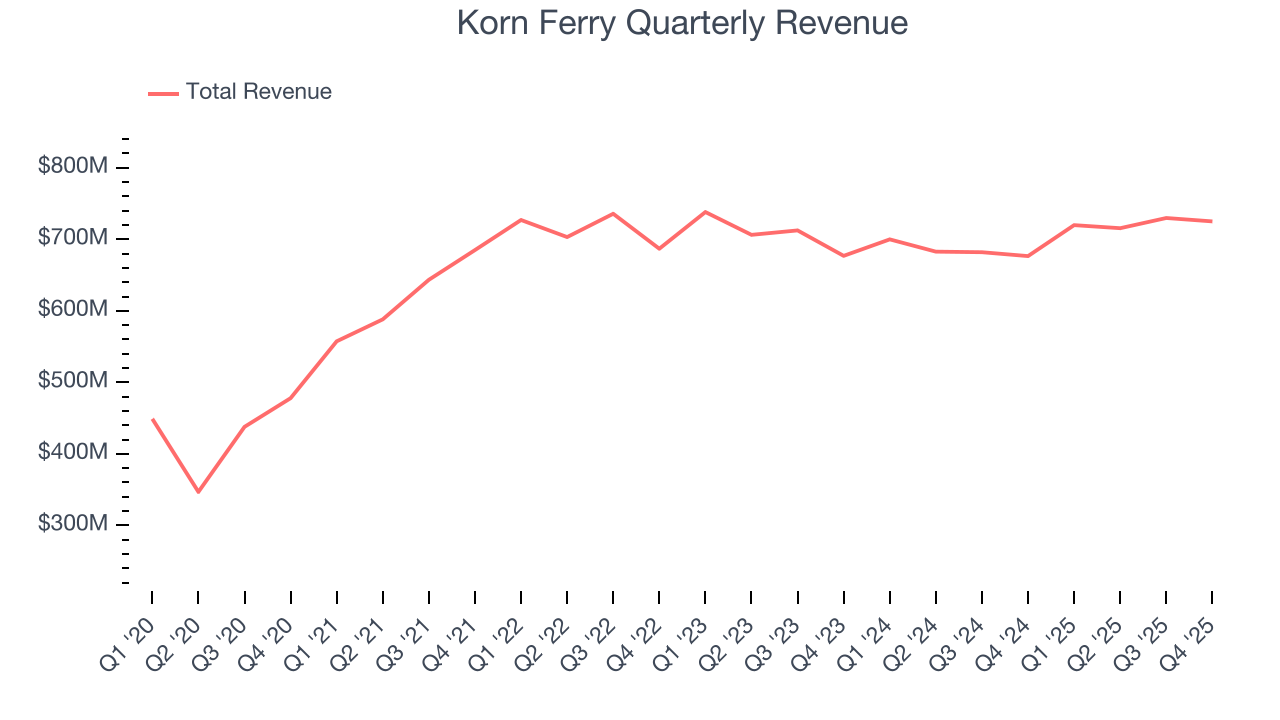

With $2.89 billion in revenue over the past 12 months, Korn Ferry is a mid-sized business services company, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale. On the bright side, it can still flex high growth rates because it’s working from a smaller revenue base.

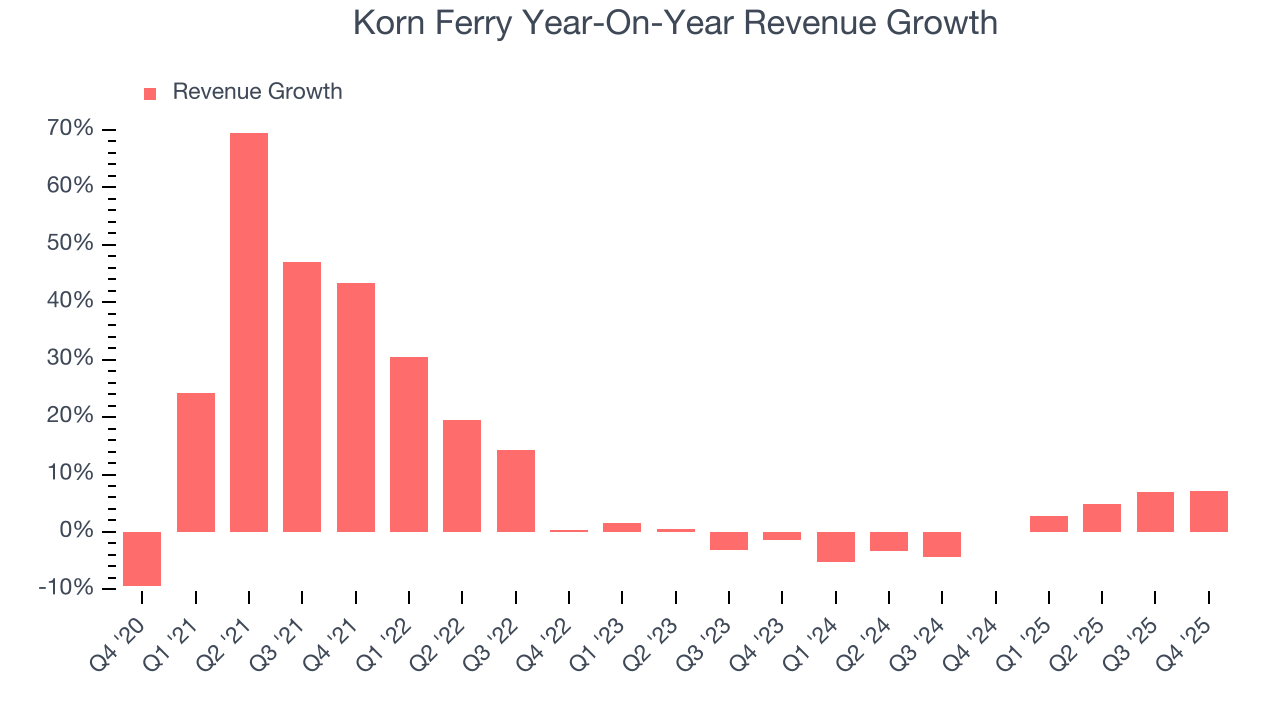

As you can see below, Korn Ferry grew its sales at an excellent 11% compounded annual growth rate over the last five years. This shows it had high demand, a useful starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within business services, a half-decade historical view may miss recent innovations or disruptive industry trends. Korn Ferry’s recent performance shows its demand has slowed significantly as its revenue was flat over the last two years.

This quarter, Korn Ferry reported year-on-year revenue growth of 7.2%, and its $725 million of revenue exceeded Wall Street’s estimates by 2.3%. Company management is currently guiding for a 2.8% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 3.2% over the next 12 months. Although this projection indicates its newer products and services will fuel better top-line performance, it is still below the sector average.

6. Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

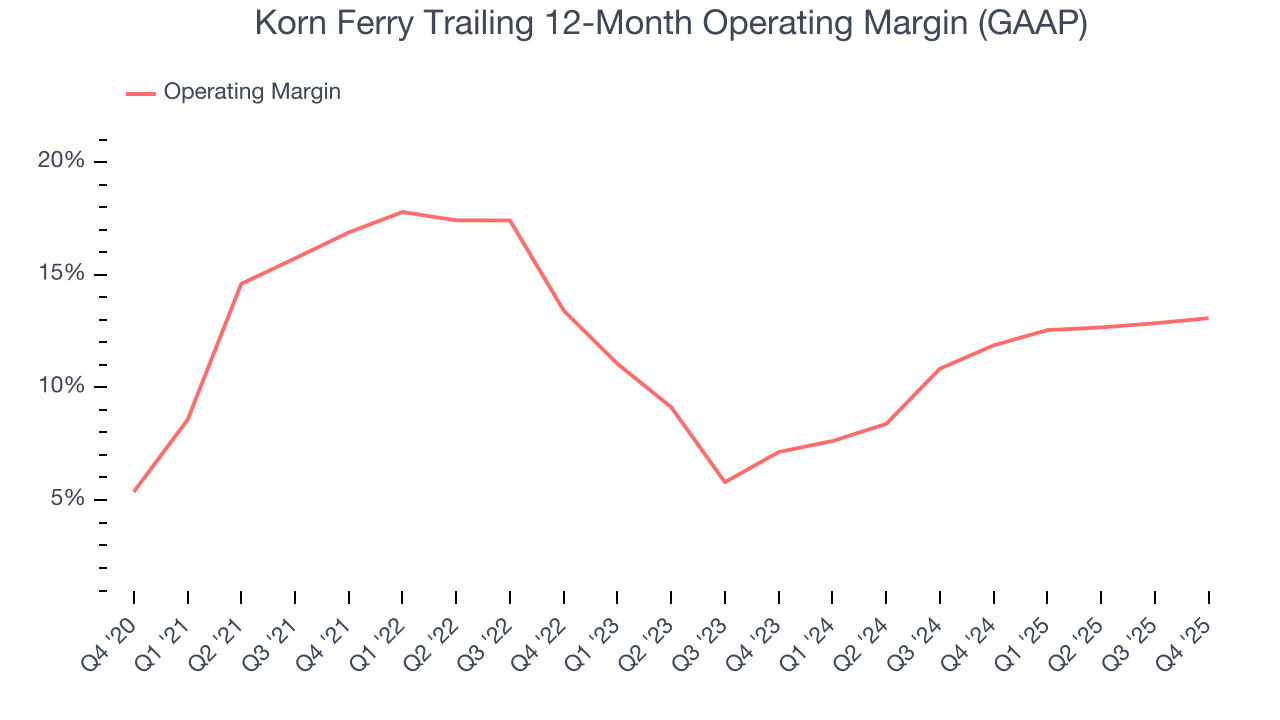

Korn Ferry has managed its cost base well over the last five years. It demonstrated solid profitability for a business services business, producing an average operating margin of 12.4%.

Looking at the trend in its profitability, Korn Ferry’s operating margin decreased by 3.8 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, Korn Ferry generated an operating margin profit margin of 12.6%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

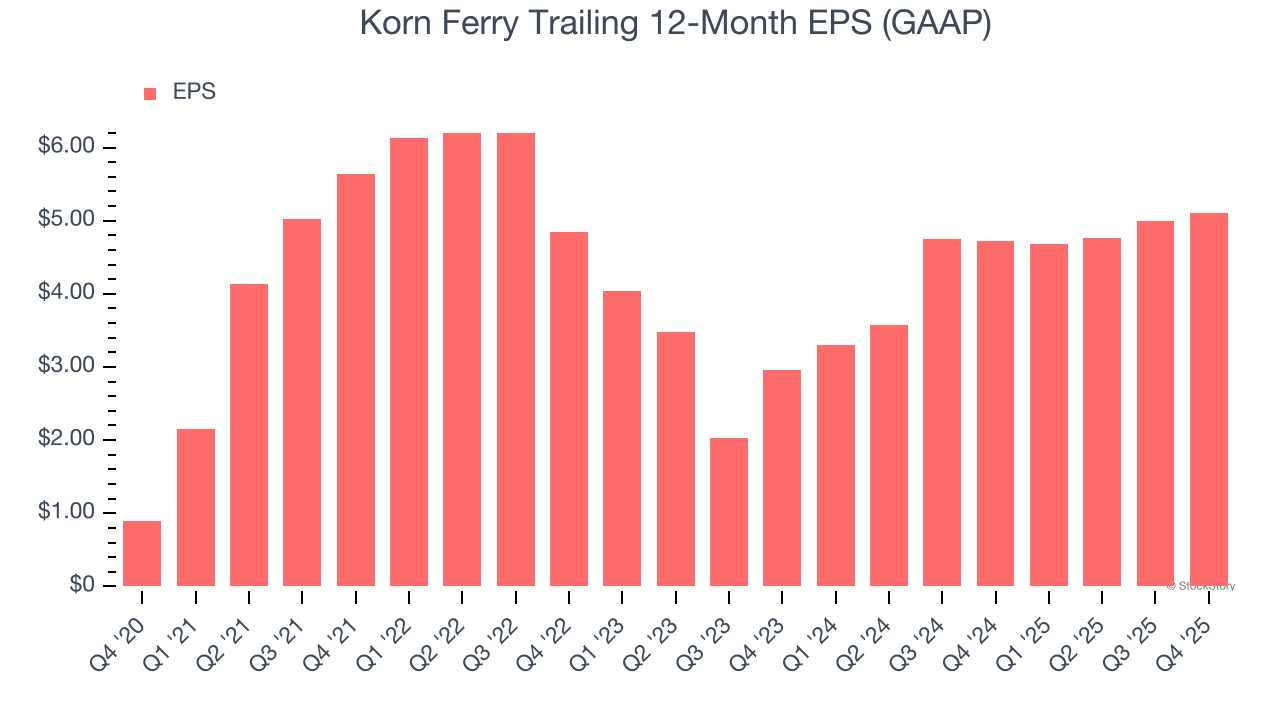

Korn Ferry’s EPS grew at 41.6% compounded annual growth rate over the last five years, higher than its 11% annualized revenue growth. However, this alone doesn’t tell us much about its business quality because its operating margin didn’t improve.

Diving into the nuances of Korn Ferry’s earnings can give us a better understanding of its performance. A five-year view shows that Korn Ferry has repurchased its stock, shrinking its share count by 1.1%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Korn Ferry, its two-year annual EPS growth of 31.4% was lower than its five-year trend. We still think its growth was good and hope it can accelerate in the future.

In Q4, Korn Ferry reported EPS of $1.23, up from $1.12 in the same quarter last year. This print was close to analysts’ estimates. Over the next 12 months, Wall Street expects Korn Ferry’s full-year EPS of $5.10 to grow 8%.

8. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

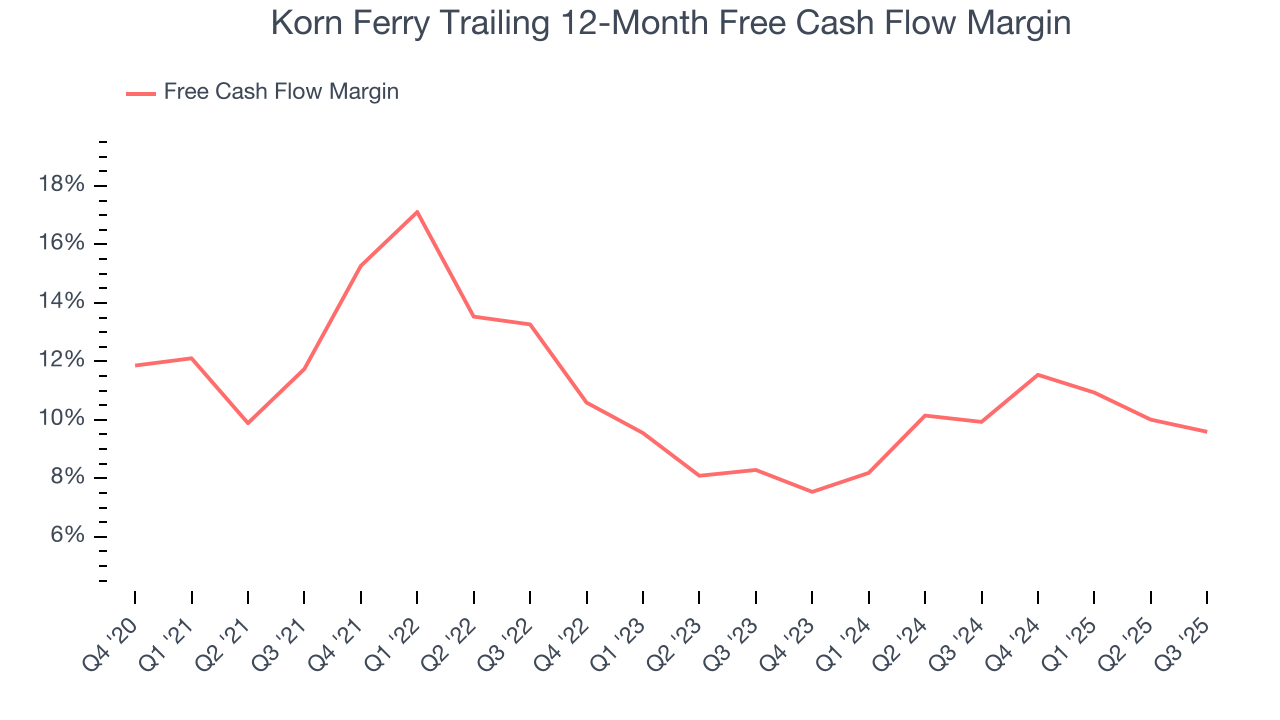

Korn Ferry has shown robust cash profitability, giving it an edge over its competitors and the ability to reinvest or return capital to investors. The company’s free cash flow margin averaged 9.8% over the last five years, quite impressive for a business services business.

Taking a step back, we can see that Korn Ferry’s margin dropped by 3.6 percentage points during that time. Continued declines could signal it is in the middle of an investment cycle.

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

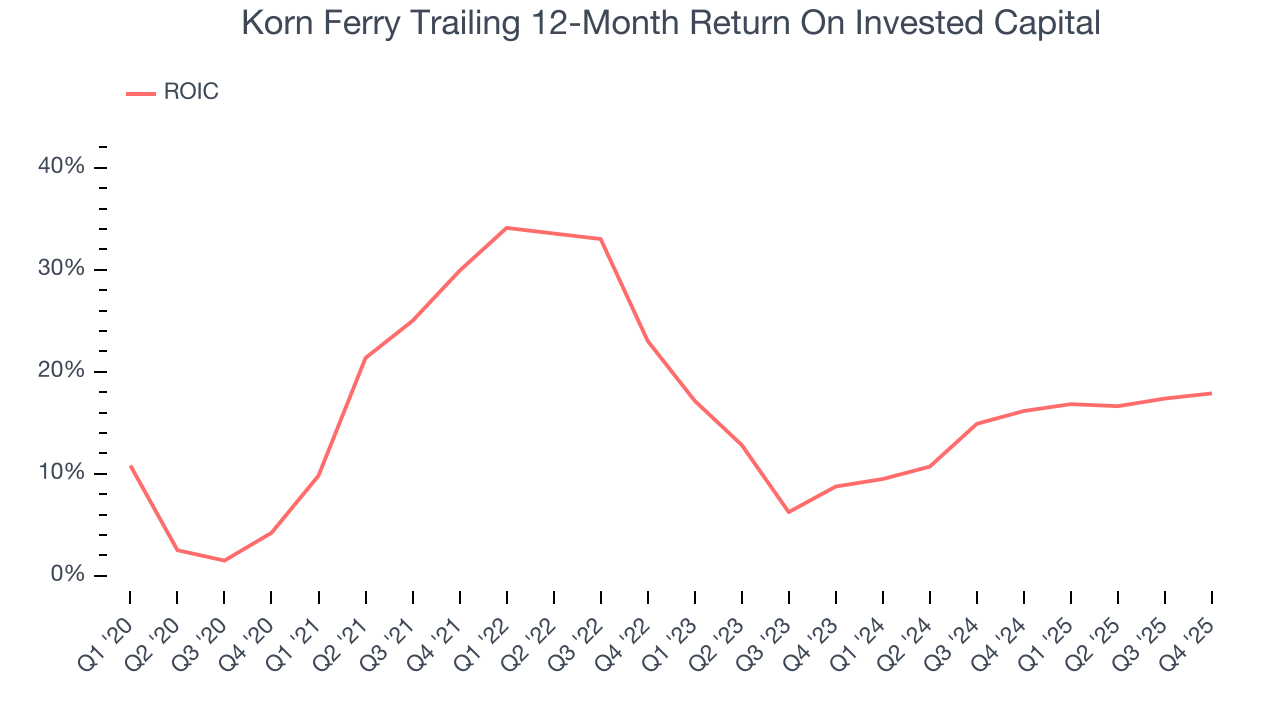

Although Korn Ferry hasn’t been the highest-quality company lately, it historically found a few growth initiatives that worked out well. Its five-year average ROIC was 19.2%, impressive for a business services business.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, Korn Ferry’s ROIC has decreased over the last few years. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

10. Balance Sheet Assessment

Companies with more cash than debt have lower bankruptcy risk.

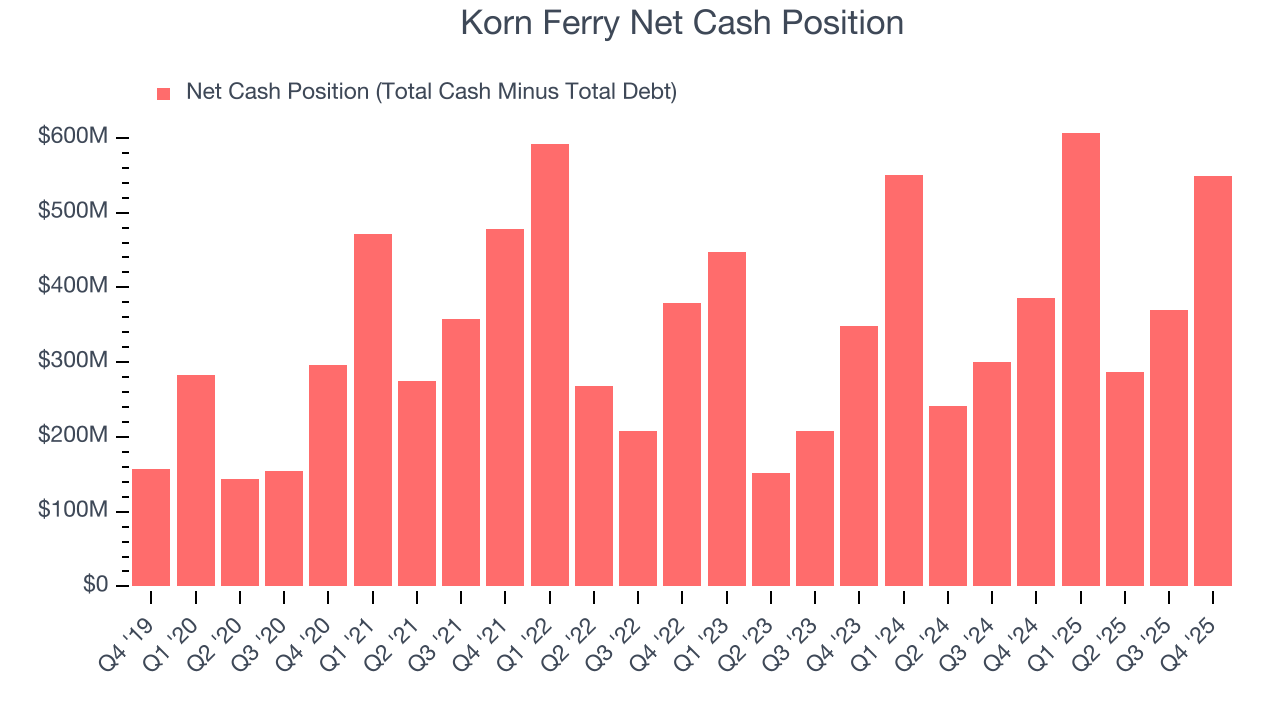

Korn Ferry is a profitable, well-capitalized company with $976.7 million of cash and $427.8 million of debt on its balance sheet. This $549 million net cash position is 17% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

11. Key Takeaways from Korn Ferry’s Q4 Results

It was encouraging to see Korn Ferry beat analysts’ revenue expectations this quarter. On the other hand, its revenue guidance for next quarter slightly missed and its EPS guidance for next quarter fell slightly short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 3.6% to $61.31 immediately after reporting.

12. Is Now The Time To Buy Korn Ferry?

Updated: March 17, 2026 at 12:21 AM EDT

Before making an investment decision, investors should account for Korn Ferry’s business fundamentals and valuation in addition to what happened in the latest quarter.

Korn Ferry isn’t a bad business, but we’re not clamoring to buy it here and now. First off, its revenue growth was impressive over the last five years. And while Korn Ferry’s diminishing returns show management's prior bets haven't worked out, its astounding EPS growth over the last five years shows its profits are trickling down to shareholders.

Korn Ferry’s P/E ratio based on the next 12 months is 10.8x. This valuation multiple is fair, but we don’t have much faith in the company. We're fairly confident there are better investments elsewhere.

Wall Street analysts have a consensus one-year price target of $74.25 on the company (compared to the current share price of $60.49).