MasTec (MTZ)

MasTec doesn’t impress us. Its low returns on capital raise concerns about its ability to deliver profits, a must for quality companies.― StockStory Analyst Team

1. News

2. Summary

Why MasTec Is Not Exciting

Involved in the 1996 Olympic Games MasTec (NYSE:MTZ) is an infrastructure construction company that specializes in the telecommunications, energy, and utility industries.

- Gross margin of 12.7% is below its competitors, leaving less money to invest in areas like marketing and R&D

- Poor expense management has led to an operating margin that is below the industry average

- One positive is that its impressive 17.7% annual revenue growth over the last five years indicates it’s winning market share this cycle

MasTec doesn’t pass our quality test. There are superior stocks for sale in the market.

Why There Are Better Opportunities Than MasTec

MasTec’s stock price of $303.00 implies a valuation ratio of 35.9x forward P/E. This multiple is higher than that of industrials peers; it’s also rich for the business quality. Not a great combination.

There are stocks out there similarly priced with better business quality. We prefer owning these.

3. MasTec (MTZ) Research Report: Q4 CY2025 Update

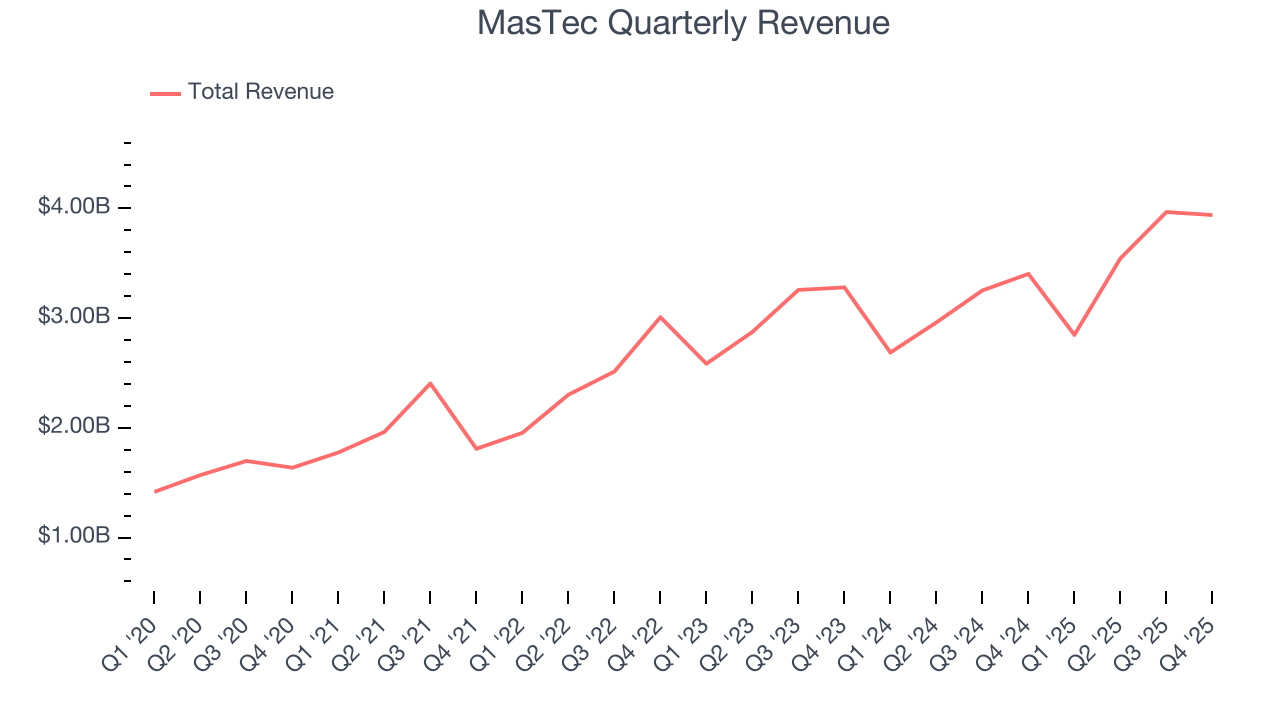

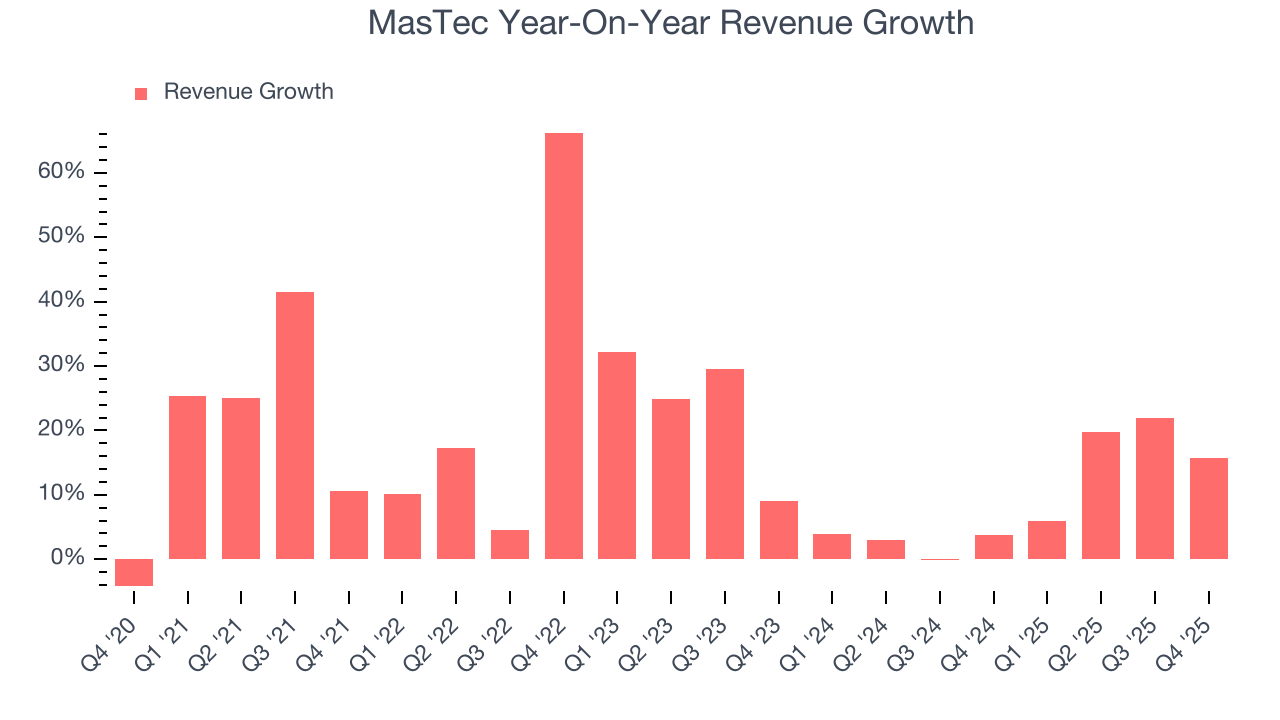

Infrastructure construction company MasTec (NYSE:MTZ) reported Q4 CY2025 results exceeding the market’s revenue expectations, with sales up 15.8% year on year to $3.94 billion. On top of that, next quarter’s revenue guidance ($3.48 billion at the midpoint) was surprisingly good and 8.7% above what analysts were expecting. Its non-GAAP profit of $2.07 per share was 6.4% above analysts’ consensus estimates.

MasTec (MTZ) Q4 CY2025 Highlights:

- Revenue: $3.94 billion vs analyst estimates of $3.72 billion (15.8% year-on-year growth, 5.9% beat)

- Adjusted EPS: $2.07 vs analyst estimates of $1.95 (6.4% beat)

- Adjusted EBITDA: $338.2 million vs analyst estimates of $325.5 million (8.6% margin, 3.9% beat)

- Revenue Guidance for Q1 CY2026 is $3.48 billion at the midpoint, above analyst estimates of $3.2 billion

- Adjusted EPS guidance for the upcoming financial year 2026 is $8.40 at the midpoint, beating analyst estimates by 3%

- EBITDA guidance for the upcoming financial year 2026 is $1.45 billion at the midpoint, above analyst estimates of $1.39 billion

- Operating Margin: 4.4%, in line with the same quarter last year

- Free Cash Flow Margin: 9.5%, down from 12.4% in the same quarter last year

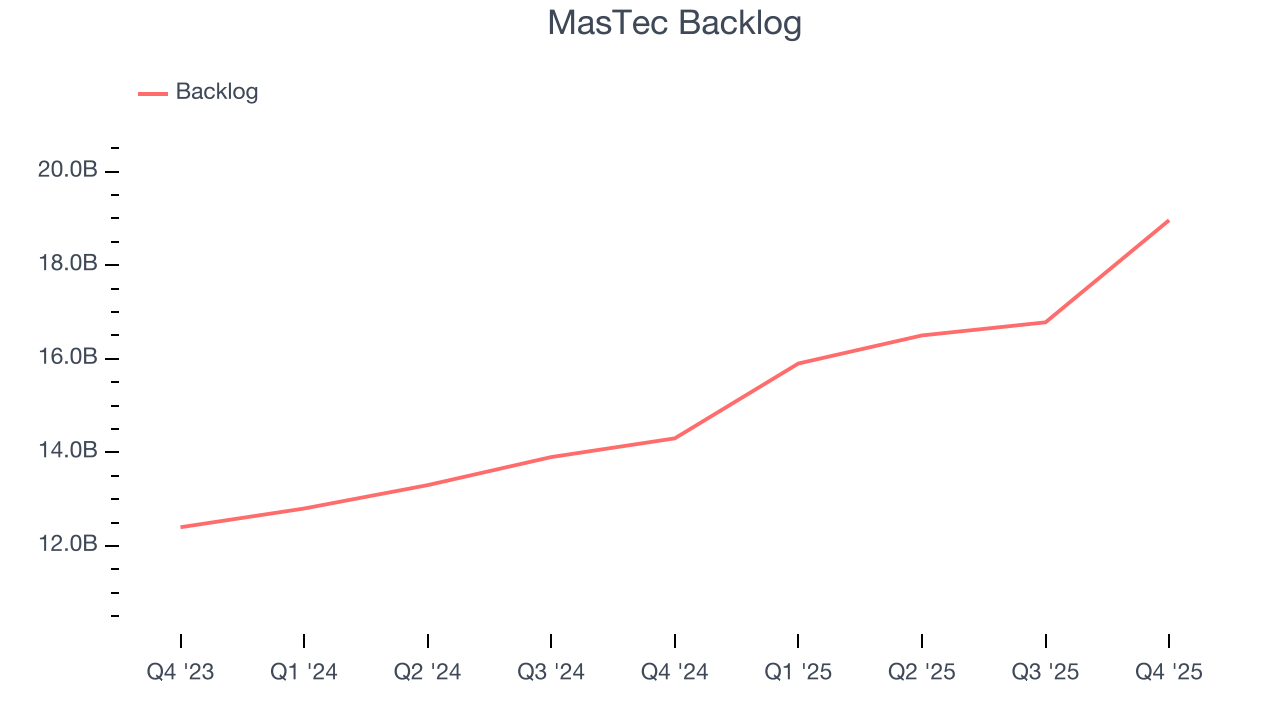

- Backlog: $18.96 billion at quarter end, up 32.6% year on year

- Market Capitalization: $22.15 billion

Company Overview

Involved in the 1996 Olympic Games MasTec (NYSE:MTZ) is an infrastructure construction company that specializes in the telecommunications, energy, and utility industries.

MasTec played a pivotal role in the development of the telecommunications infrastructure for the 1996 Atlanta Olympic Games, which showcased its ability to provide infrastructure to large-scale construction projects. The company’s services give society the telecommunications, energy, and utility it needs to live our modern life.

Its services, starting with its telecommunications segment, include the installation of wireline and wireless communication equipment like fiber optic cables and cell sites. Its many other service offerings include oil and gas pipeline construction, installation, and maintenance, and the construction and maintenance of electrical transmission lines, wind-energy farms, and solar farms. The company also installs and upgrades water and sewer systems, as well as the installation and servicing of smart home technologies like security systems for residential and business applications.

The company generates most of its revenue through contracts, made via direct sales, for its aforementioned services. It also produces some recurring revenue due to the repeating nature of its maintenance services, and it does business with both public and private sector clients.

4. Engineering and Design Services

Companies providing engineering and design services boast ever-evolving technical expertise. Compared to their counterparts who manufacture and sell physical products, these companies can also pivot faster to more trending areas due to their smaller physical asset bases. Green energy and water conservation, for example, are current themes driving incremental demand in this space. On the other hand, those providing engineering and design services are at the whim of construction and infrastructure project volumes, which tend to be cyclical and can be impacted heavily by economic factors such as interest rates.

Other companies in the infrastructure construction and services industry include Quanta Services (NYSE:PWR), Dycom Industries (NYSE:DY), and Primoris Services (NASDAQ:PRIM).

5. Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Thankfully, MasTec’s 17.7% annualized revenue growth over the last five years was incredible. Its growth beat the average industrials company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. MasTec’s annualized revenue growth of 9.2% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

MasTec also reports its backlog, or the value of its outstanding orders that have not yet been executed or delivered. MasTec’s backlog reached $18.96 billion in the latest quarter and averaged 23.4% year-on-year growth over the last two years. Because this number is better than its revenue growth, we can see the company accumulated more orders than it could fulfill and deferred revenue to the future. This could imply elevated demand for MasTec’s products and services but raises concerns about capacity constraints.

This quarter, MasTec reported year-on-year revenue growth of 15.8%, and its $3.94 billion of revenue exceeded Wall Street’s estimates by 5.9%. Company management is currently guiding for a 22% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 8.8% over the next 12 months, similar to its two-year rate. This projection is above the sector average and implies its newer products and services will help maintain its recent top-line performance.

6. Gross Margin & Pricing Power

All else equal, we prefer higher gross margins because they make it easier to generate more operating profits and indicate that a company commands pricing power by offering more differentiated products.

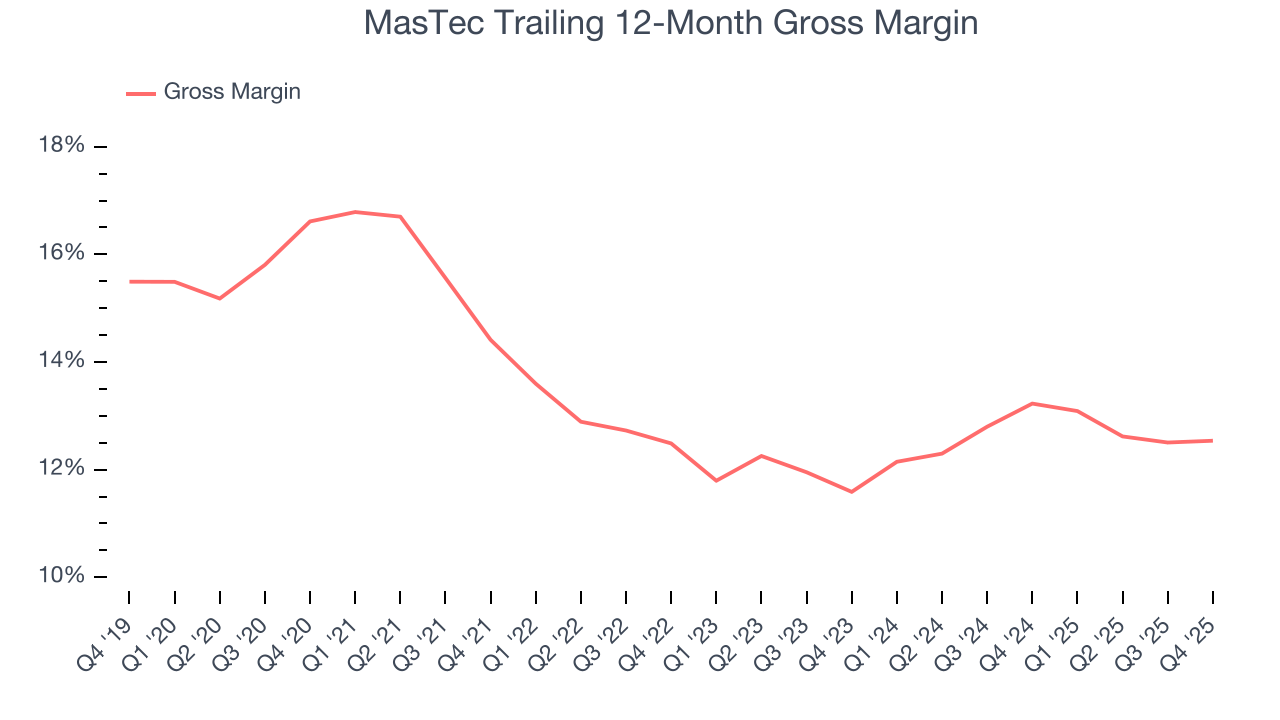

MasTec has bad unit economics for an industrials business, signaling it operates in a competitive market. As you can see below, it averaged a 12.7% gross margin over the last five years. Said differently, MasTec had to pay a chunky $87.26 to its suppliers for every $100 in revenue.

MasTec produced a 12.9% gross profit margin in Q4, in line with the same quarter last year. Zooming out, the company’s full-year margin has remained steady over the past 12 months, suggesting its input costs (such as raw materials and manufacturing expenses) have been stable and it isn’t under pressure to lower prices.

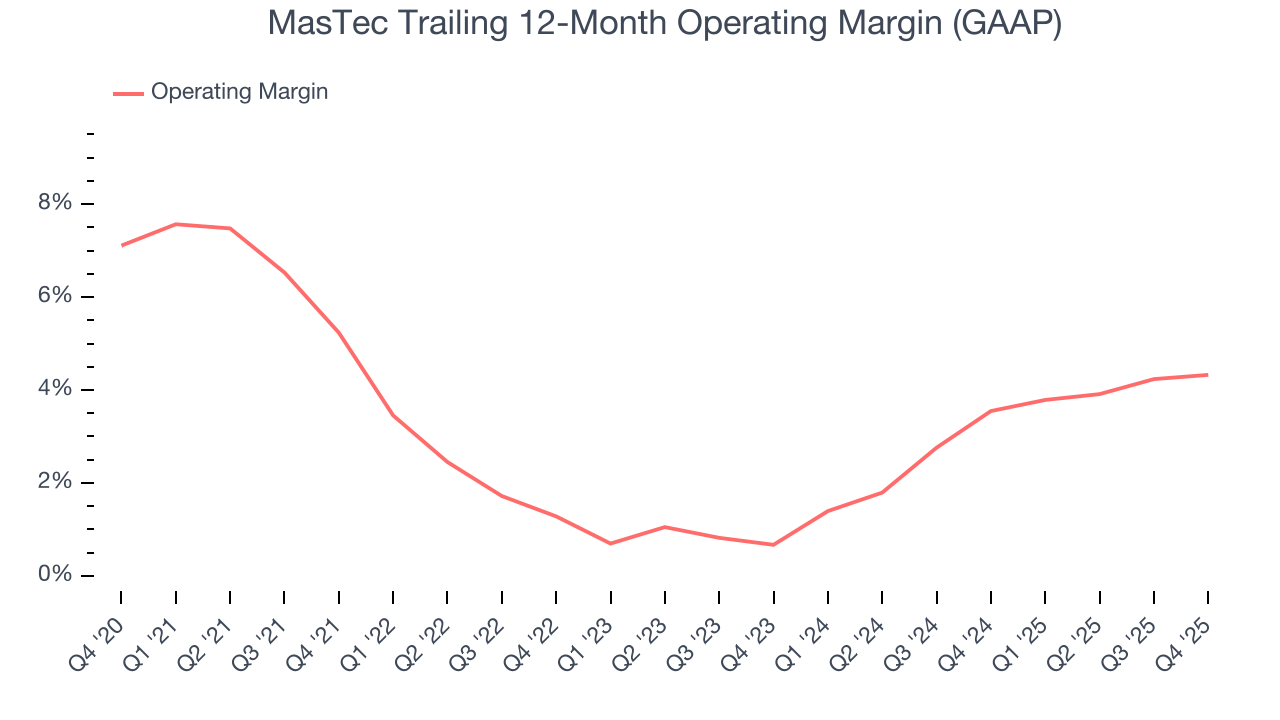

7. Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

MasTec’s operating margin might fluctuated slightly over the last 12 months but has remained more or less the same, averaging 3% over the last five years. This profitability was lousy for an industrials business and caused by its suboptimal cost structureand low gross margin.

Looking at the trend in its profitability, MasTec’s operating margin might fluctuated slightly but has generally stayed the same over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q4, MasTec generated an operating margin profit margin of 4.4%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

8. Earnings Per Share

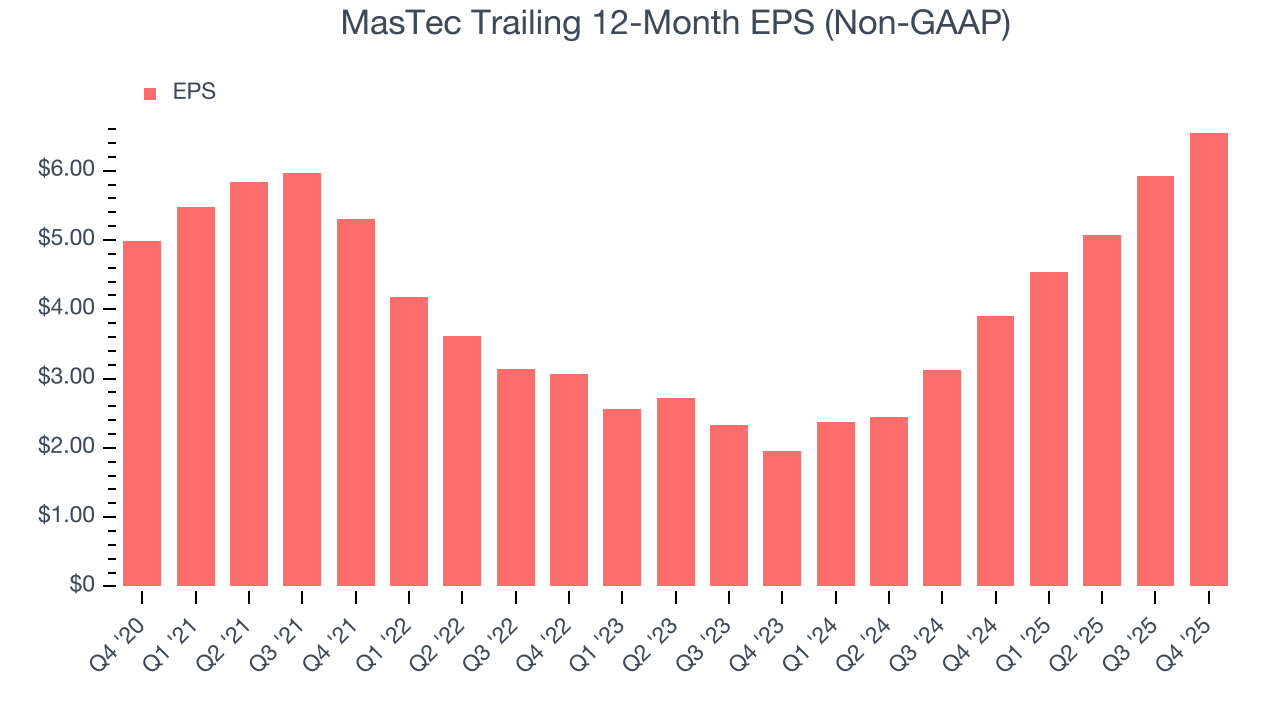

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

MasTec’s EPS grew at an unimpressive 5.6% compounded annual growth rate over the last five years, lower than its 17.7% annualized revenue growth. However, its operating margin didn’t change during this time, telling us that non-fundamental factors such as interest and taxes affected its ultimate earnings.

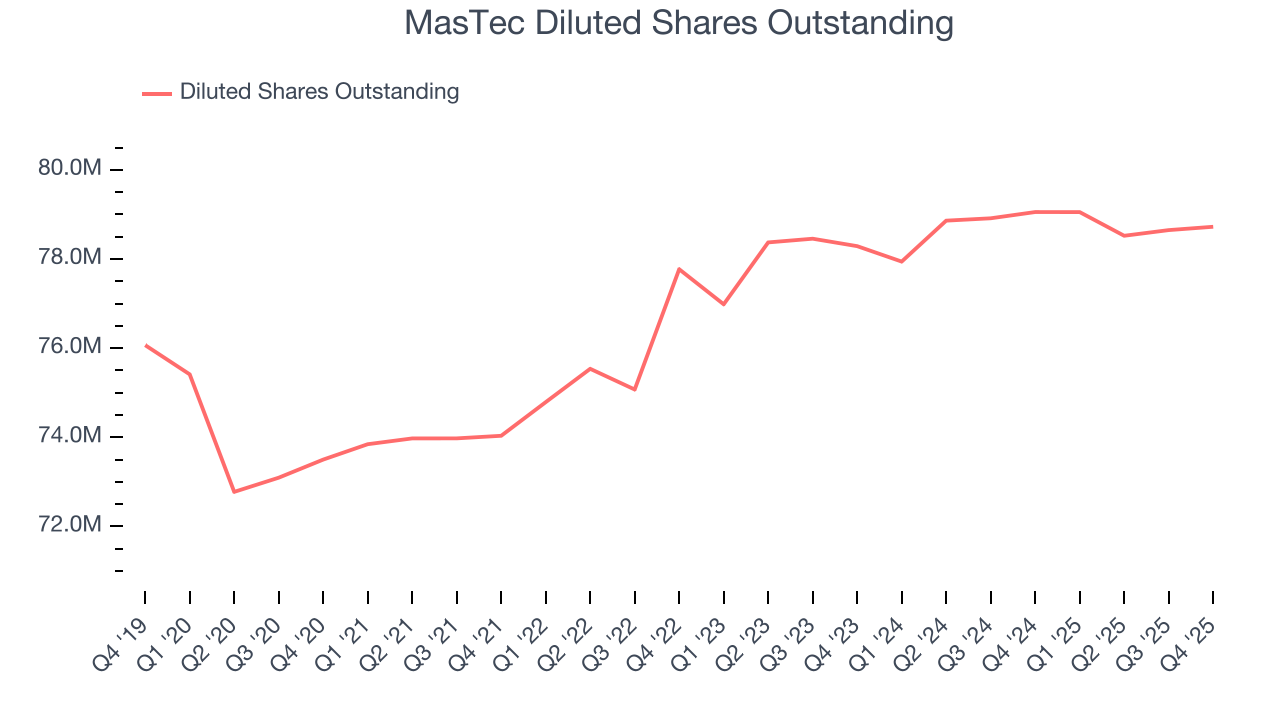

We can take a deeper look into MasTec’s earnings to better understand the drivers of its performance. A five-year view shows MasTec has diluted its shareholders, growing its share count by 7.1%. This has led to lower per share earnings. Taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For MasTec, its two-year annual EPS growth of 82.8% was higher than its five-year trend. This acceleration made it one of the faster-growing industrials companies in recent history.

In Q4, MasTec reported adjusted EPS of $2.07, up from $1.44 in the same quarter last year. This print beat analysts’ estimates by 6.4%. Over the next 12 months, Wall Street expects MasTec’s full-year EPS of $6.55 to grow 25.4%.

9. Cash Is King

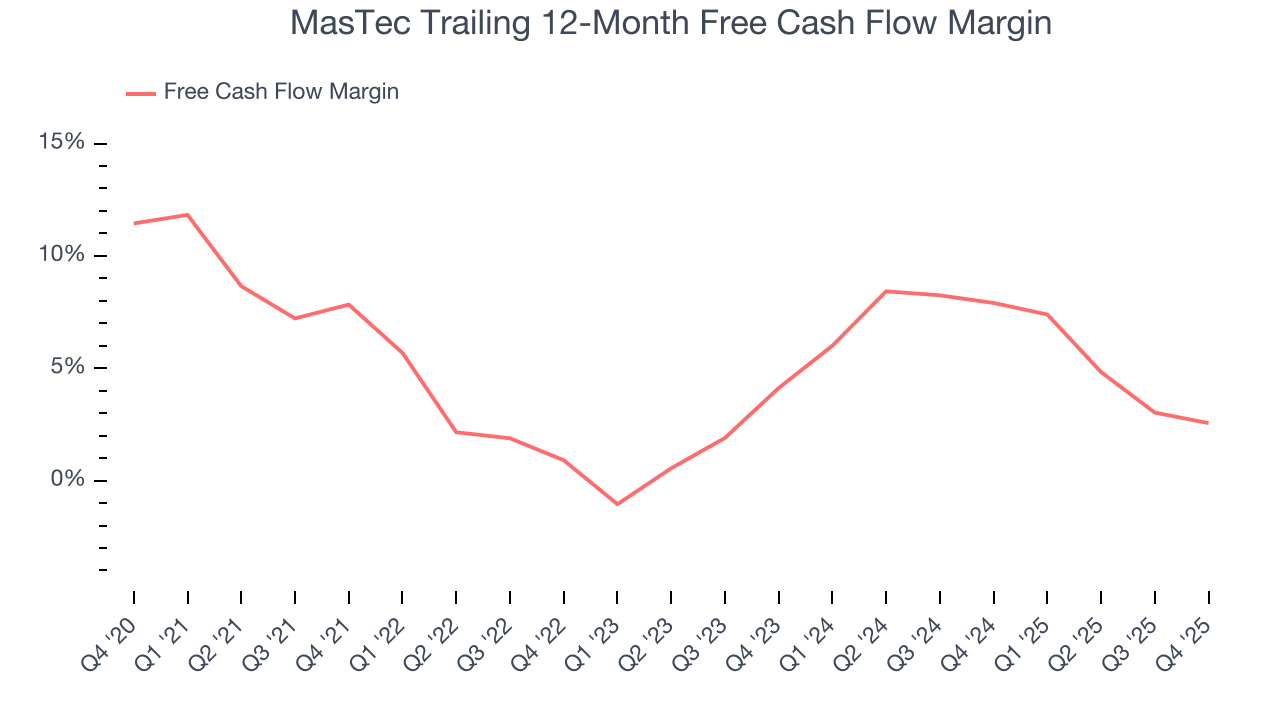

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

MasTec has shown weak cash profitability over the last five years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 4.5%, subpar for an industrials business.

Taking a step back, we can see that MasTec’s margin dropped by 5.3 percentage points during that time. This along with its unexciting margin put the company in a tough spot, and shareholders are likely hoping it can reverse course. If the trend continues, it could signal it’s becoming a more capital-intensive business.

MasTec’s free cash flow clocked in at $372.7 million in Q4, equivalent to a 9.5% margin. The company’s cash profitability regressed as it was 3 percentage points lower than in the same quarter last year, but it’s still above its five-year average. We wouldn’t read too much into this quarter’s decline because capital expenditures can be seasonal and companies often stockpile inventory in anticipation of higher demand, causing short-term swings. Long-term trends carry greater meaning.

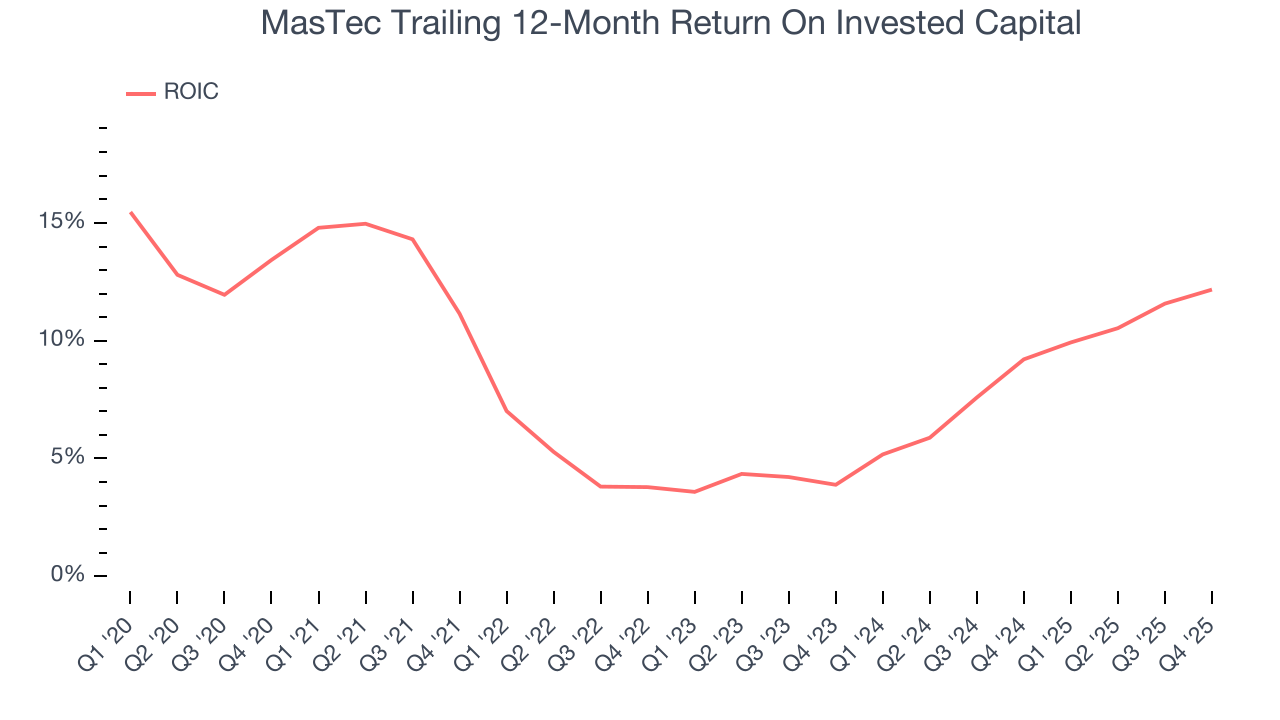

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

MasTec historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 8%, somewhat low compared to the best industrials companies that consistently pump out 20%+.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Fortunately, MasTec’s ROIC averaged 3.2 percentage point increases each year over the last few years. This is a good sign, and if its returns keep rising, there’s a chance it could evolve into an investable business.

11. Balance Sheet Assessment

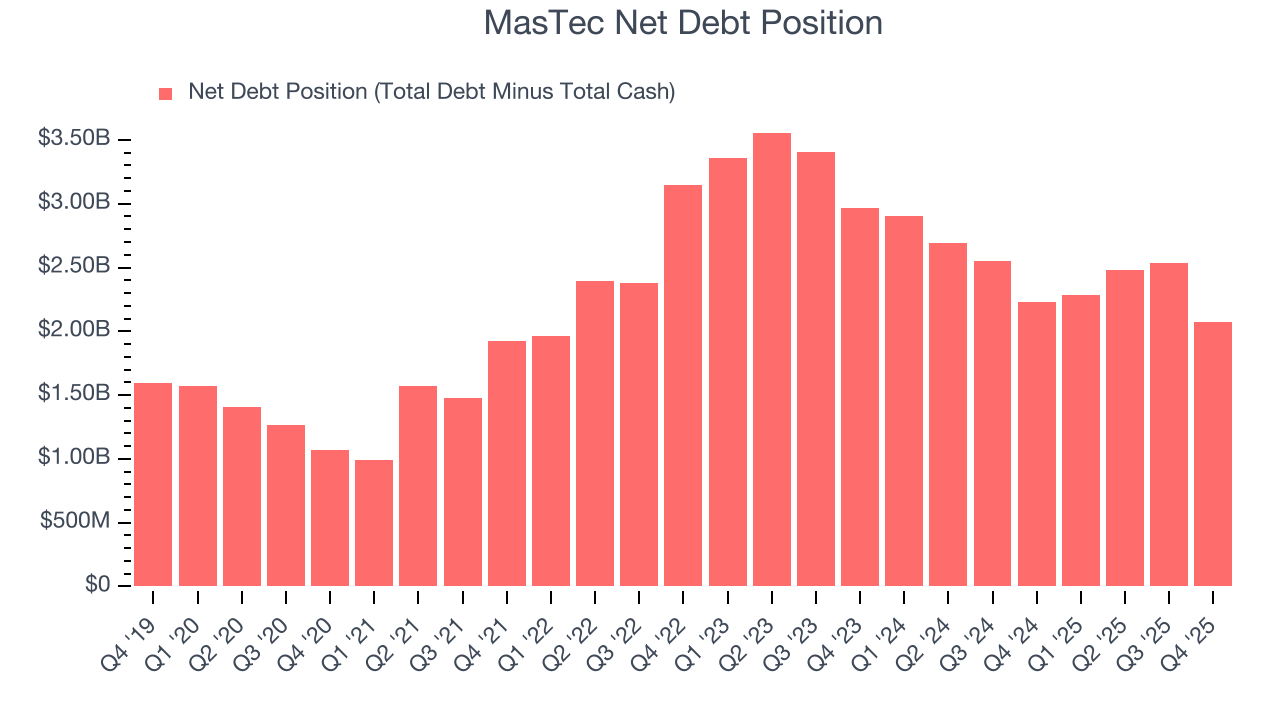

MasTec reported $396 million of cash and $2.47 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $1.15 billion of EBITDA over the last 12 months, we view MasTec’s 1.8× net-debt-to-EBITDA ratio as safe. We also see its $83.69 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from MasTec’s Q4 Results

We were impressed by MasTec’s optimistic full-year revenue guidance, which blew past analysts’ expectations. We were also glad its full-year EBITDA guidance trumped Wall Street’s estimates. Zooming out, we think this was a solid print. The stock traded up 3% to $298.58 immediately following the results.

13. Is Now The Time To Buy MasTec?

Updated: March 18, 2026 at 11:57 PM EDT

Before deciding whether to buy MasTec or pass, we urge investors to consider business quality, valuation, and the latest quarterly results.

MasTec has some positive attributes, but it isn’t one of our picks. First off, its revenue growth was exceptional over the last five years and is expected to accelerate over the next 12 months. And while MasTec’s cash profitability fell over the last five years, its backlog growth has been marvelous.

MasTec’s P/E ratio based on the next 12 months is 35.9x. Investors with a higher risk tolerance might like the company, but we don’t really see a big opportunity at the moment. We're pretty confident there are more exciting stocks to buy at the moment.

Wall Street analysts have a consensus one-year price target of $336.32 on the company (compared to the current share price of $303.00).