NVR (NVR)

We’re skeptical of NVR. Its poor sales growth and falling returns on capital suggest its growth opportunities are shrinking.― StockStory Analyst Team

1. News

2. Summary

Why We Think NVR Will Underperform

Known for its unique land acquisition strategy, NVR (NYSE:NVR) is a respected homebuilder and mortgage company in the United States.

- Estimated sales decline of 10.2% for the next 12 months implies a challenging demand environment

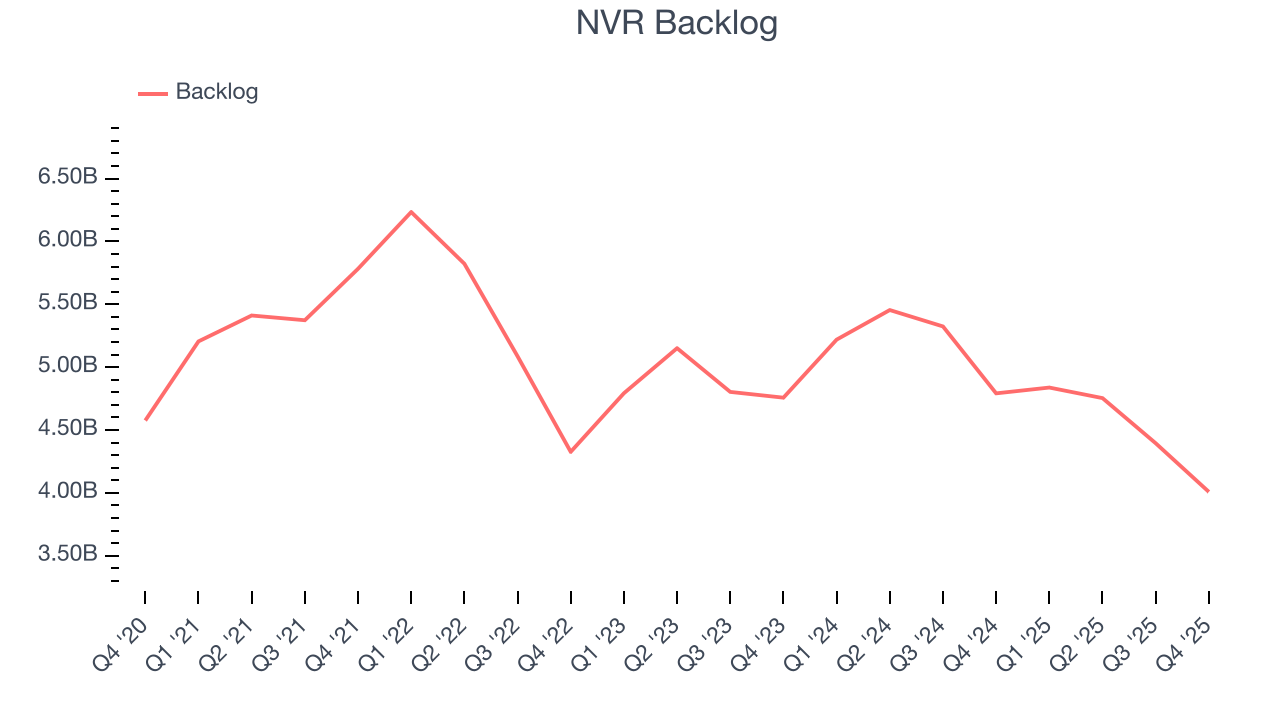

- New orders were hard to come by as its backlog was flat over the past two years

- One positive is that its disciplined cost controls and effective management have materialized in a strong operating margin

NVR doesn’t meet our quality standards. Better businesses are for sale in the market.

Why There Are Better Opportunities Than NVR

NVR is trading at $7,542 per share, or 19.1x forward P/E. This multiple is lower than most industrials companies, but for good reason.

Cheap stocks can look like great bargains at first glance, but you often get what you pay for. These mediocre businesses often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. NVR (NVR) Research Report: Q4 CY2025 Update

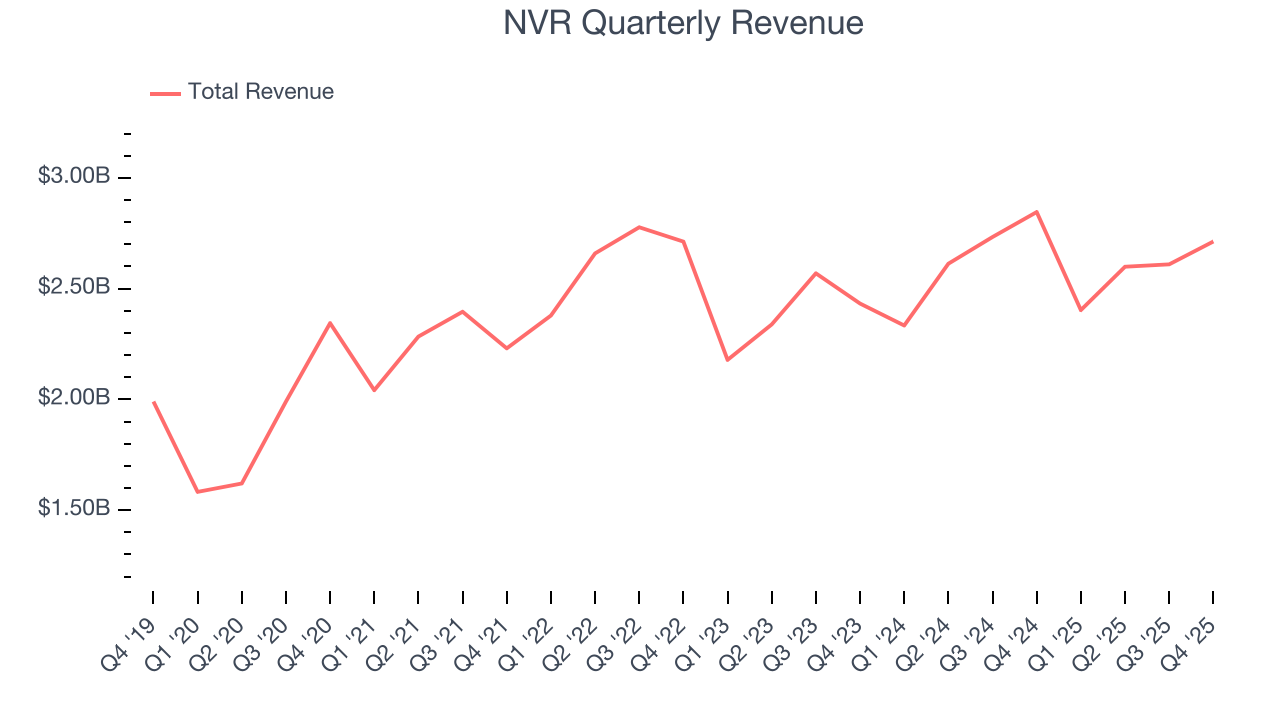

Homebuilder NVR (NYSE:NVR) reported revenue ahead of Wall Streets expectations in Q4 CY2025, but sales fell by 4.7% year on year to $2.71 billion. Its non-GAAP profit of $121.54 per share was 14.8% above analysts’ consensus estimates.

NVR (NVR) Q4 CY2025 Highlights:

- Revenue: $2.71 billion vs analyst estimates of $2.48 billion (4.7% year-on-year decline, 9.4% beat)

- Adjusted EPS: $121.54 vs analyst estimates of $105.90 (14.8% beat)

- Adjusted EBITDA: $459.5 million vs analyst estimates of $441.2 million (16.9% margin, 4.1% beat)

- Operating Margin: 16.5%, down from 19% in the same quarter last year

- Free Cash Flow Margin: 15.5%, down from 22.2% in the same quarter last year

- Backlog: $4.01 billion at quarter end, down 16.4% year on year

- Market Capitalization: $21.3 billion

Company Overview

Known for its unique land acquisition strategy, NVR (NYSE:NVR) is a respected homebuilder and mortgage company in the United States.

NVR, Inc., a Virginia corporation formed in 1980, primarily focuses on the construction and sale of single-family detached homes, townhomes, and condominium buildings, which are primarily built on a pre-sold basis.

The company operates its homebuilding activities directly and its mortgage banking operations primarily through a wholly owned subsidiary, NVR Mortgage Finance (NVRM).

As one of the largest homebuilders in the United States, NVR operates in 30+ metropolitan areas across 15+states and Washington, D.C. The company's homebuilding operations include the construction and sale of homes under three trade names: Ryan Homes, NVHomes, and Heartland Homes. These brands cater to different segments of the market, with Ryan Homes targeting first-time and first-time move-up buyers (current homeowners looking to upgrade their homes), while NVHomes and Heartland Homes focus on move-up and luxury buyers.

NVR typically acquires finished building lots from third-party land developers through fixed-price finished lot purchase agreements (LPAs) rather than engaging in direct land development. This strategy helps the company avoid the financial requirements and risks associated with direct land ownership and development. NVR seeks to maintain control over a supply of lots suitable for its five-year business plan.

The company generates revenue primarily through the sale of its homes. It also brings in revenue through NVRM, where it originates mortgages, , records gains and losses from the sale of loans, and provides title services. NVRM sells almost all of the mortgage loans it closes into the secondary markets.

4. Home Builders

Traditionally, homebuilders have built competitive advantages with economies of scale that lead to advantaged purchasing and brand recognition among consumers. Aesthetic trends have always been important in the space, but more recently, energy efficiency and conservation are driving innovation. However, these companies are still at the whim of the macro, specifically interest rates that heavily impact new and existing home sales. In fact, homebuilders are one of the most cyclical subsectors within industrials.

Other homebuilders operating in NVR’s market include Lennary (NYSE:LEN), PulteGroup (NYSE:PHM), and DR Horton (NYSE:NVR).

5. Revenue Growth

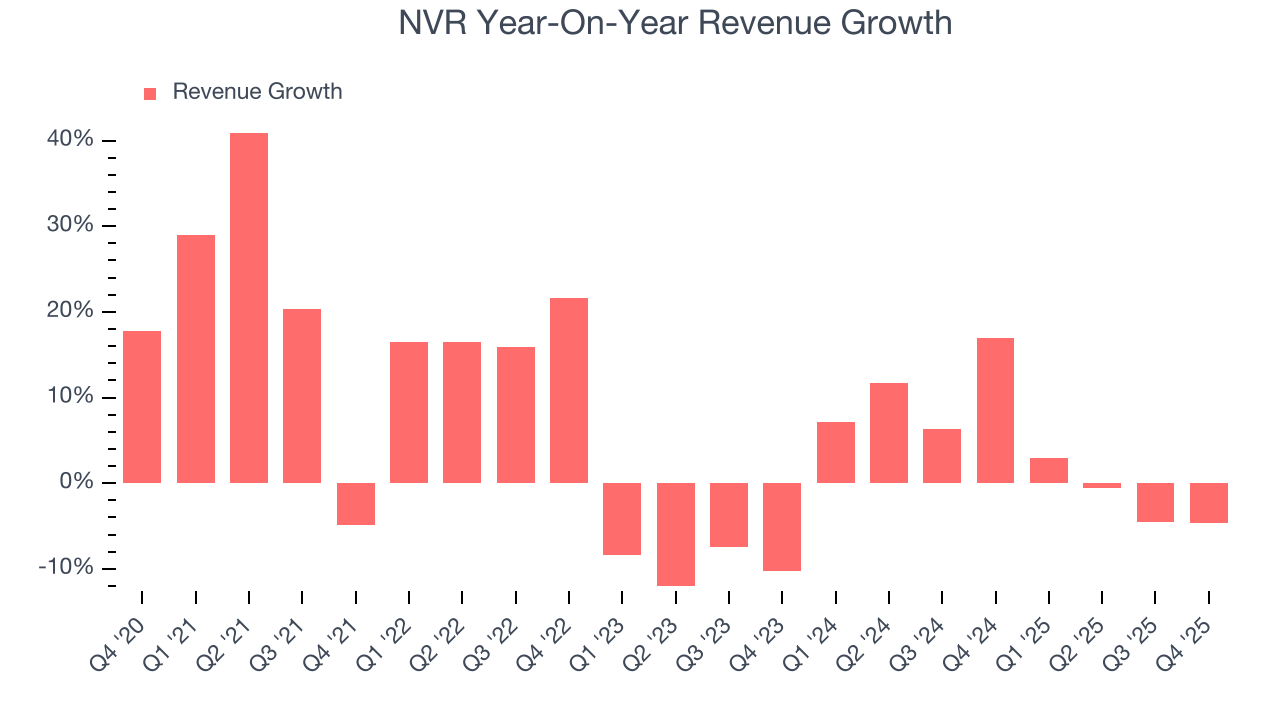

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Unfortunately, NVR’s 6.5% annualized revenue growth over the last five years was mediocre. This fell short of our benchmark for the industrials sector and is a rough starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. NVR’s recent performance shows its demand has slowed as its annualized revenue growth of 4.1% over the last two years was below its five-year trend.

NVR also reports its backlog, or the value of its outstanding orders that have not yet been executed or delivered. NVR’s backlog reached $4.01 billion in the latest quarter and averaged 3.4% year-on-year declines over the last two years. Because this number is lower than its revenue growth, we can see the company hasn’t secured enough new orders to maintain its growth rate in the future.

This quarter, NVR’s revenue fell by 4.7% year on year to $2.71 billion but beat Wall Street’s estimates by 9.4%.

Looking ahead, sell-side analysts expect revenue to decline by 2.1% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and indicates its products and services will see some demand headwinds.

6. Gross Margin & Pricing Power

All else equal, we prefer higher gross margins because they make it easier to generate more operating profits and indicate that a company commands pricing power by offering more differentiated products.

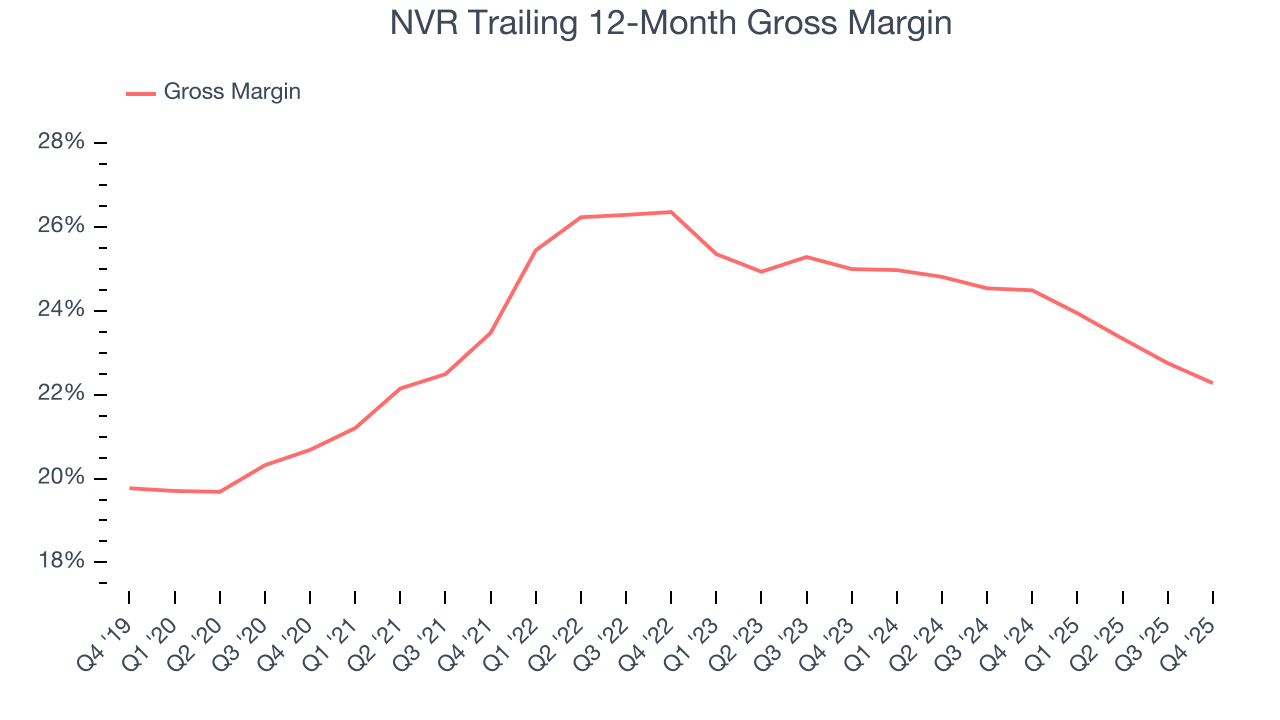

NVR has bad unit economics for an industrials company, giving it less room to reinvest and develop new offerings. As you can see below, it averaged a 24.3% gross margin over the last five years. That means NVR paid its suppliers a lot of money ($75.66 for every $100 in revenue) to run its business.

NVR’s gross profit margin came in at 22.7% this quarter, marking a 1.7 percentage point decrease from 24.4% in the same quarter last year. NVR’s full-year margin has also been trending down over the past 12 months, decreasing by 2.2 percentage points. If this move continues, it could suggest a more competitive environment with some pressure to lower prices and higher input costs (such as raw materials and manufacturing expenses).

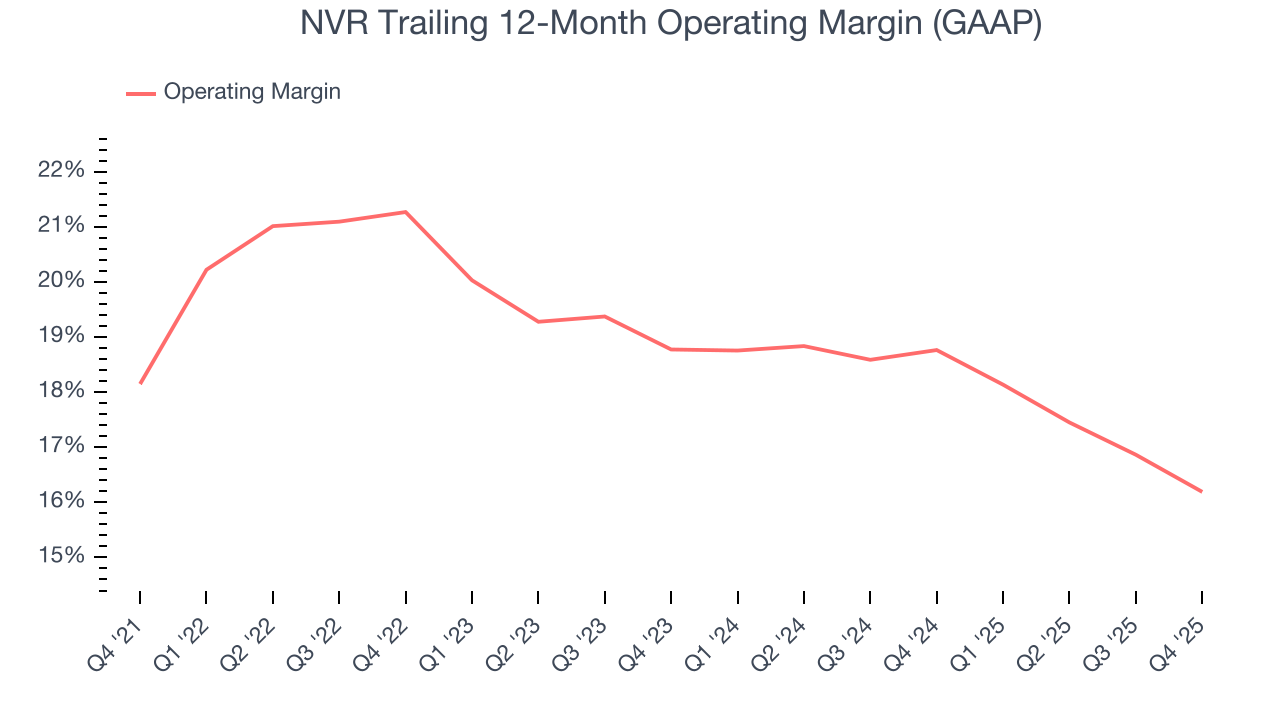

7. Operating Margin

NVR has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 18.7%. This result was particularly impressive because of its low gross margin, which is mostly a factor of what it sells and takes huge shifts to move meaningfully. Companies have more control over their operating margins, and it’s a show of well-managed operations if they’re high when gross margins are low.

Analyzing the trend in its profitability, NVR’s operating margin decreased by 2 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, NVR generated an operating margin profit margin of 16.5%, down 2.5 percentage points year on year. Since NVR’s operating margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, R&D, and administrative overhead increased.

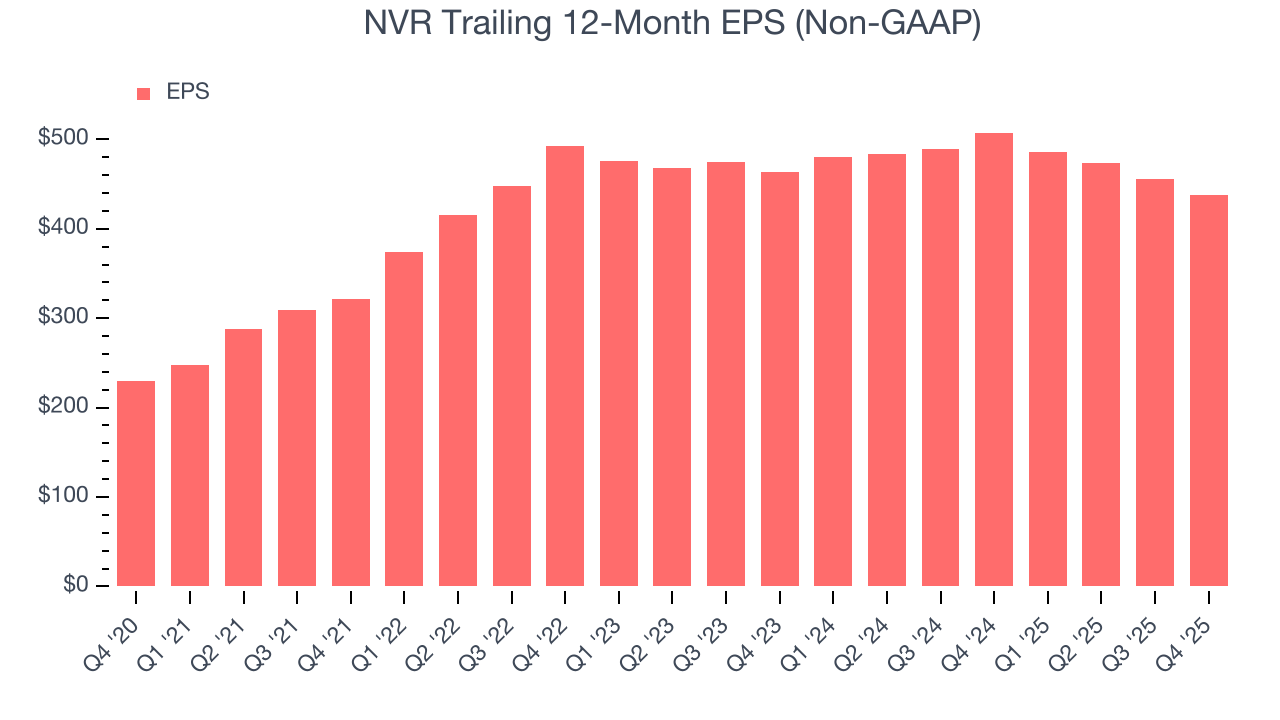

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

NVR’s EPS grew at a remarkable 13.8% compounded annual growth rate over the last five years, higher than its 6.5% annualized revenue growth. However, this alone doesn’t tell us much about its business quality because its operating margin didn’t improve.

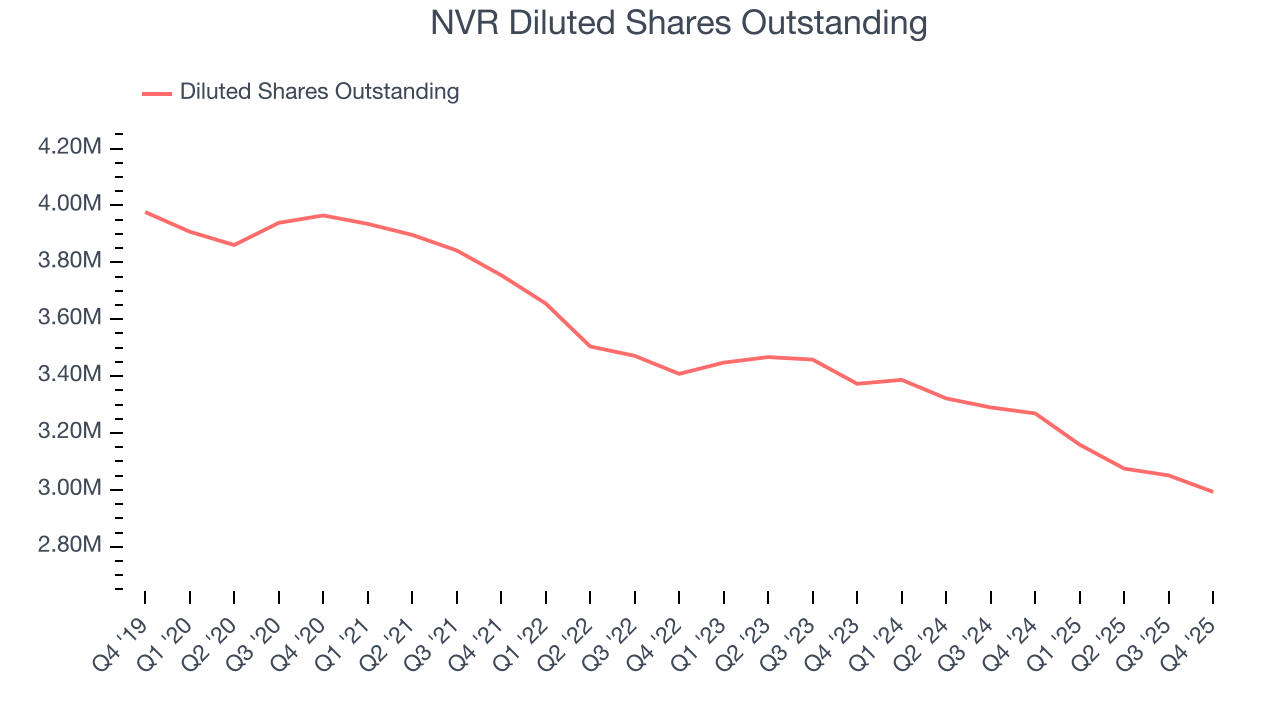

Diving into NVR’s quality of earnings can give us a better understanding of its performance. A five-year view shows that NVR has repurchased its stock, shrinking its share count by 24.5%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For NVR, its two-year annual EPS declines of 2.8% mark a reversal from its (seemingly) healthy five-year trend. We hope NVR can return to earnings growth in the future.

In Q4, NVR reported adjusted EPS of $121.54, down from $139.93 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects NVR’s full-year EPS of $437.24 to shrink by 6.5%.

9. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

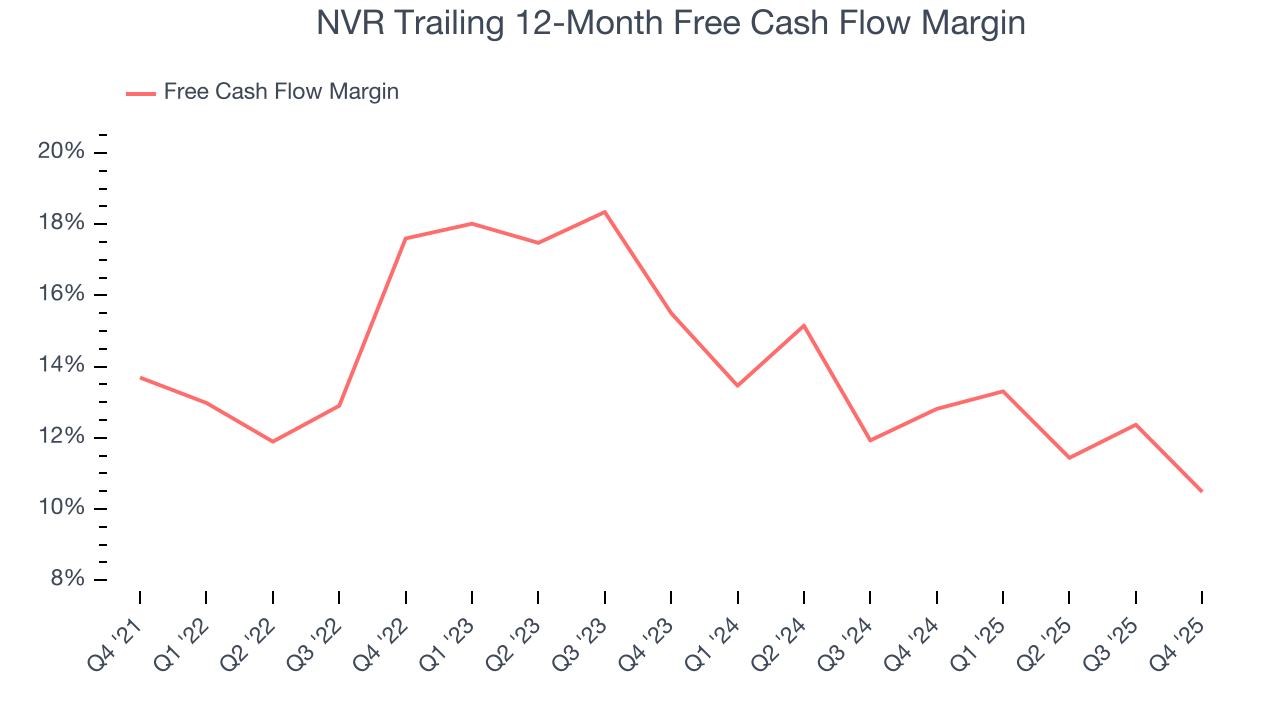

NVR has shown terrific cash profitability, putting it in an advantageous position to invest in new products, return capital to investors, and consolidate the market during industry downturns. The company’s free cash flow margin was among the best in the industrials sector, averaging 14% over the last five years.

Taking a step back, we can see that NVR’s margin dropped by 3.2 percentage points during that time. If its declines continue, it could signal increasing investment needs and capital intensity.

NVR’s free cash flow clocked in at $420.7 million in Q4, equivalent to a 15.5% margin. The company’s cash profitability regressed as it was 6.7 percentage points lower than in the same quarter last year, but it’s still above its five-year average. We wouldn’t read too much into this quarter’s decline because investment needs can be seasonal, causing short-term swings. Long-term trends are more important.

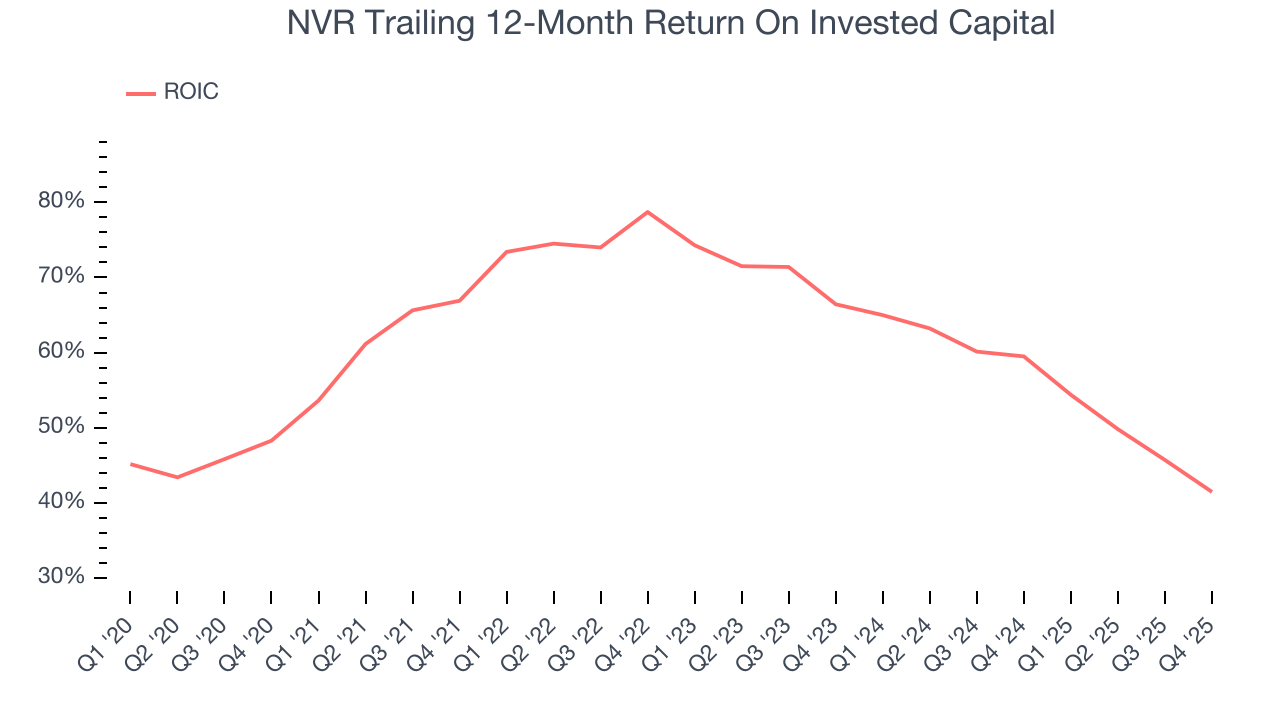

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Although NVR hasn’t been the highest-quality company lately, it found a few growth initiatives in the past that worked out wonderfully. Its five-year average ROIC was 62.6%, splendid for an industrials business.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, NVR’s ROIC has decreased significantly over the last few years. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

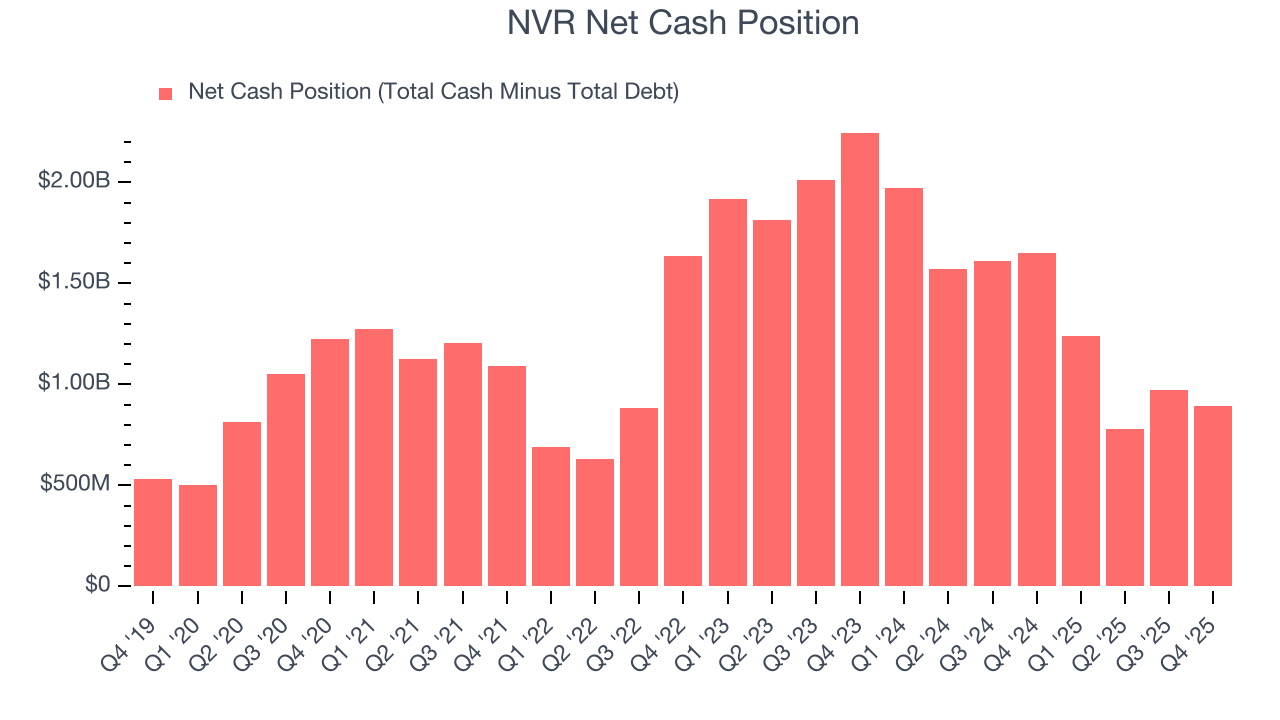

11. Balance Sheet Assessment

Companies with more cash than debt have lower bankruptcy risk.

NVR is a profitable, well-capitalized company with $1.92 billion of cash and $1.03 billion of debt on its balance sheet. This $891.4 million net cash position is 4.2% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

12. Key Takeaways from NVR’s Q4 Results

We were impressed by how significantly NVR blew past analysts’ adjusted operating income expectations this quarter. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this quarter featured some important positives. The stock remained flat at $7,640 immediately after reporting.

13. Is Now The Time To Buy NVR?

Updated: January 28, 2026 at 11:01 PM EST

Before deciding whether to buy NVR or pass, we urge investors to consider business quality, valuation, and the latest quarterly results.

NVR falls short of our quality standards. To kick things off, its revenue growth was mediocre over the last five years, and analysts expect its demand to deteriorate over the next 12 months. And while its impressive operating margins show it has a highly efficient business model, the downside is its diminishing returns show management's prior bets haven't worked out. On top of that, its projected EPS for the next year is lacking.

NVR’s P/E ratio based on the next 12 months is 18x. This valuation is reasonable, but the company’s shaky fundamentals present too much downside risk. There are superior stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $8,168 on the company (compared to the current share price of $7,640).