Primoris (PRIM)

We’d invest in Primoris. Its revenue is growing quickly while its profitability is rising, giving it multiple ways to win.― StockStory Analyst Team

1. News

2. Summary

Why We Like Primoris

Listed on the NASDAQ in 2008, Primoris (NYSE:PRIM) builds, maintains, and upgrades infrastructure in the utility, energy, and civil construction industries.

- Annual revenue growth of 16.8% over the last five years was superb and indicates its market share increased during this cycle

- Earnings per share grew by 20.6% annually over the last five years and trumped its peers

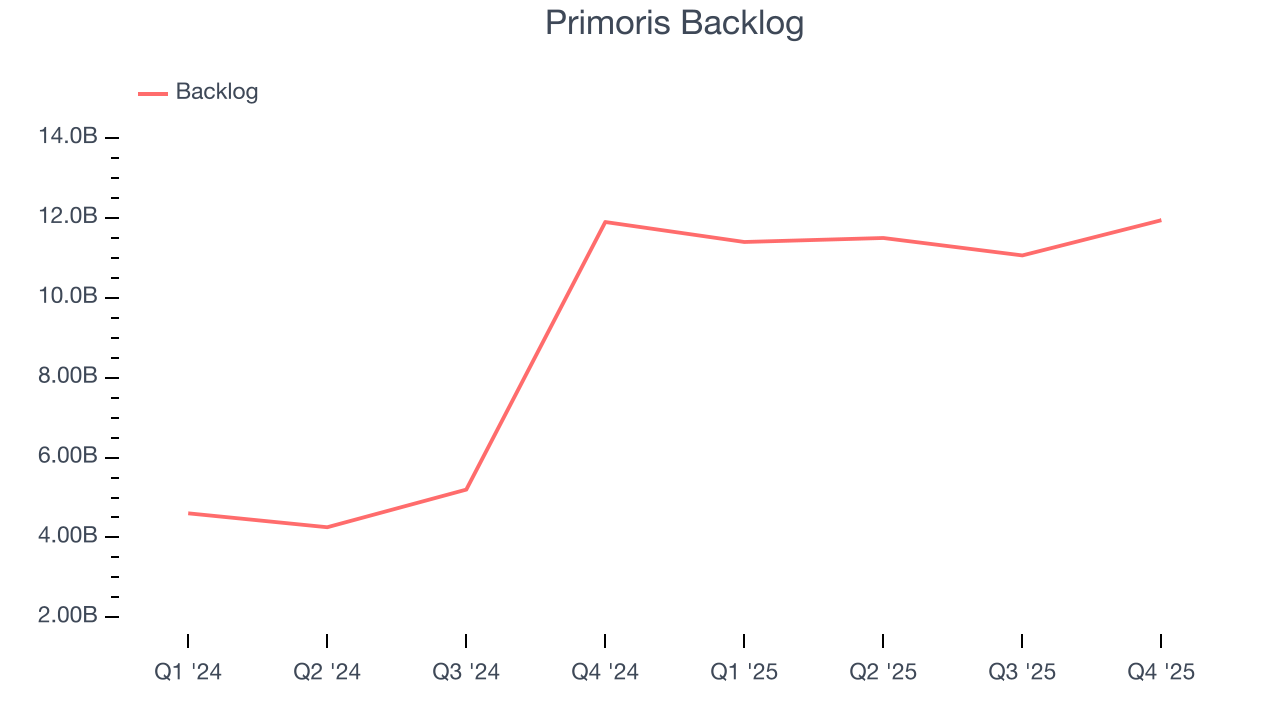

- Backlog has averaged 108% growth over the past two years, showing it has a pipeline of unfulfilled orders that will support revenue in the future

Primoris is a top-tier company. The valuation looks fair when considering its quality, so this could be a good time to buy some shares.

Why Is Now The Time To Buy Primoris?

Primoris is trading at $133.48 per share, or 22.3x forward P/E. This valuation is fair - even cheap depending on how much you like the story - for the quality you get.

Entry price matters far less than business fundamentals if you’re investing for a multi-year period. But if you can get a bargain price it’s certainly icing on the cake.

3. Primoris (PRIM) Research Report: Q4 CY2025 Update

Infrastructure construction company Primoris (NYSE:PRIM) reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 6.7% year on year to $1.86 billion. Its non-GAAP profit of $1.08 per share was 8.9% above analysts’ consensus estimates.

Primoris (PRIM) Q4 CY2025 Highlights:

- Revenue: $1.86 billion vs analyst estimates of $1.80 billion (6.7% year-on-year growth, 3.3% beat)

- Adjusted EPS: $1.08 vs analyst estimates of $0.99 (8.9% beat)

- Adjusted EBITDA: $108.2 million vs analyst estimates of $104.7 million (5.8% margin, 3.4% beat)

- Adjusted EPS guidance for the upcoming financial year 2026 is $5.90 at the midpoint, beating analyst estimates by 1%

- EBITDA guidance for the upcoming financial year 2026 is $570 million at the midpoint, above analyst estimates of $565.3 million

- Operating Margin: 4.2%, in line with the same quarter last year

- Free Cash Flow Margin: 6.5%, down from 15.5% in the same quarter last year

- Backlog: $11.95 billion at quarter end, in line with the same quarter last year

- Market Capitalization: $9.15 billion

Company Overview

Listed on the NASDAQ in 2008, Primoris (NYSE:PRIM) builds, maintains, and upgrades infrastructure in the utility, energy, and civil construction industries.

Examples of infrastructure projects it has worked on include pipelines, power plants, renewable energy facilities, water and wastewater systems, highways, bridges, airport runaways, and tunnels.

The company engages in the design, construction, and maintenance of these projects. A significant portion of its revenue comes from fixed-price and cost-plus contracts for its construction business while it earns consulting fees from its engineering and design services. The recurring portion of its revenue comes from its maintenance and service agreements for existing infrastructure, and these three prongs help Primoris support its clients from the conceptual stage to project completion and upkeep.

Both private and public sector clients contribute to the company’s revenue, and it sells through a direct sales force and strategic bidding on projects.

4. Construction and Maintenance Services

Construction and maintenance services companies not only boast technical know-how in specialized areas but also may hold special licenses and permits. Those who work in more regulated areas can enjoy more predictable revenue streams - for example, fire escapes need to be inspected every five years. More recently, services to address energy efficiency and labor availability are also creating incremental demand. But like the broader industrials sector, construction and maintenance services companies are at the whim of economic cycles as external factors like interest rates can greatly impact the new construction that drives incremental demand for these companies’ offerings.

Competitors of Primoris include Flour (NYSE:FLR), AECOM (NYSE:ACM), and private company Kiewit.

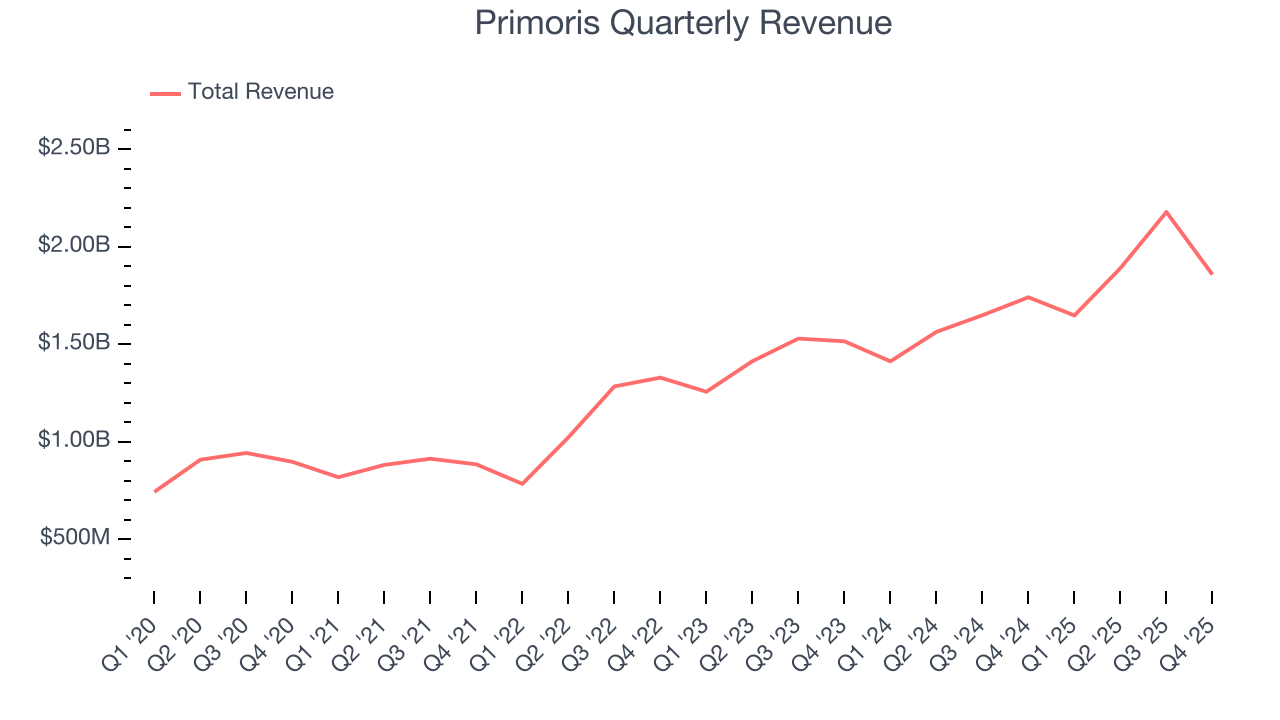

5. Revenue Growth

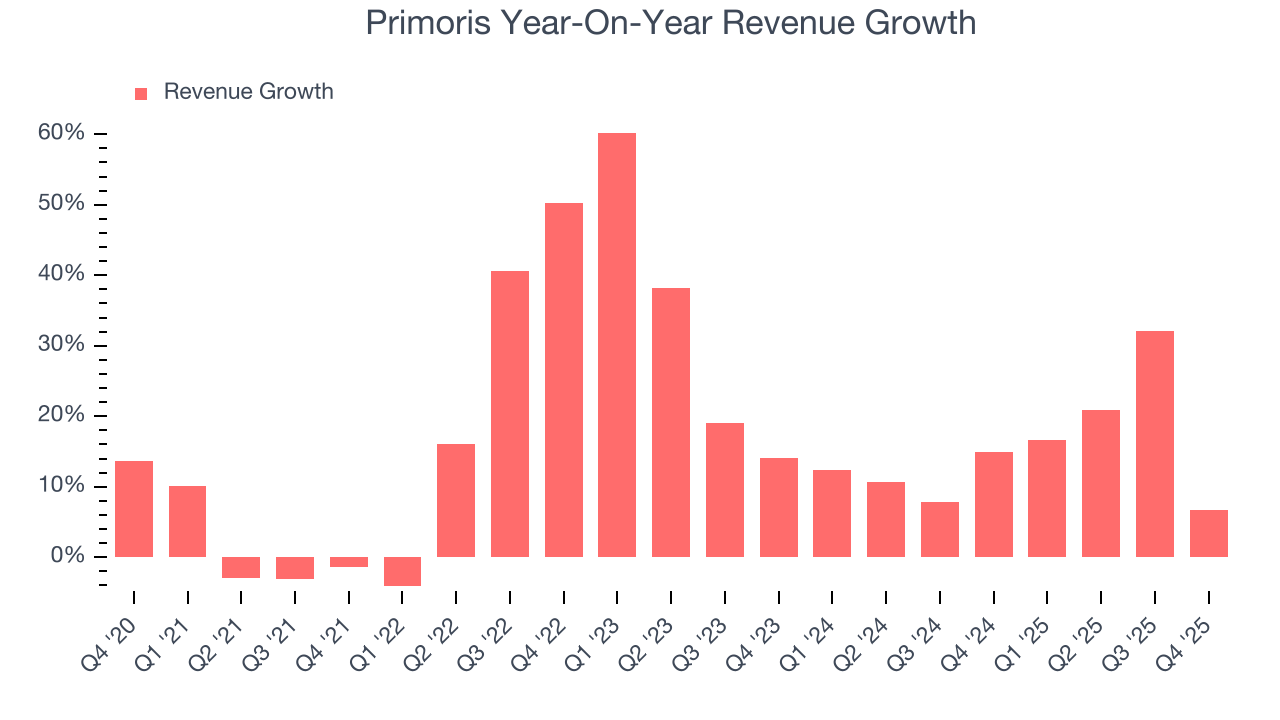

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Thankfully, Primoris’s 16.8% annualized revenue growth over the last five years was incredible. Its growth surpassed the average industrials company and shows its offerings resonate with customers, a great starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Primoris’s annualized revenue growth of 15.1% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

We can better understand the company’s revenue dynamics by analyzing its backlog, or the value of its outstanding orders that have not yet been executed or delivered. Primoris’s backlog reached $11.95 billion in the latest quarter and averaged 108% year-on-year growth over the last two years. Because this number is better than its revenue growth, we can see the company accumulated more orders than it could fulfill and deferred revenue to the future. This could imply elevated demand for Primoris’s products and services but raises concerns about capacity constraints.

This quarter, Primoris reported year-on-year revenue growth of 6.7%, and its $1.86 billion of revenue exceeded Wall Street’s estimates by 3.3%.

Looking ahead, sell-side analysts expect revenue to grow 5.9% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and suggests its products and services will see some demand headwinds. At least the company is tracking well in other measures of financial health.

6. Gross Margin & Pricing Power

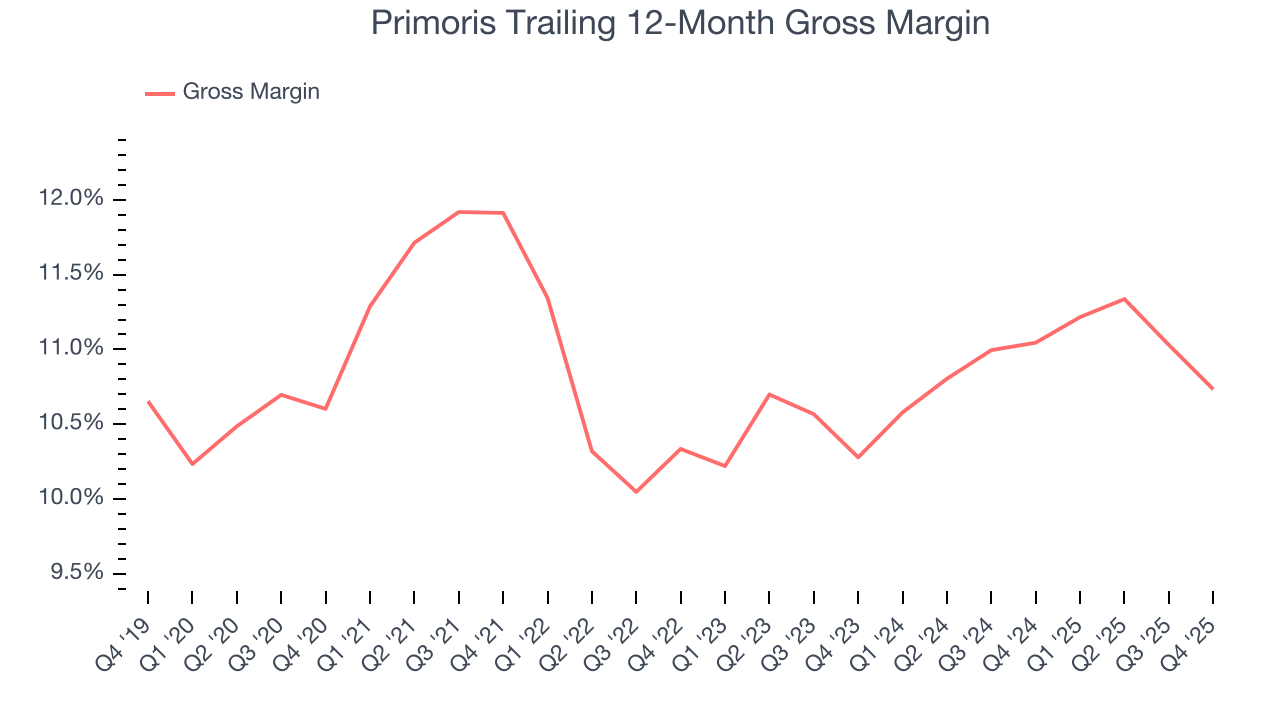

Primoris has bad unit economics for an industrials business, signaling it operates in a competitive market. As you can see below, it averaged a 10.8% gross margin over the last five years. That means Primoris paid its suppliers a lot of money ($89.20 for every $100 in revenue) to run its business.

Primoris’s gross profit margin came in at 9.4% this quarter , marking a 1.2 percentage point decrease from 10.6% in the same quarter last year. On a wider time horizon, the company’s full-year margin has remained steady over the past four quarters, suggesting its input costs (such as raw materials and manufacturing expenses) have been stable and it isn’t under pressure to lower prices.

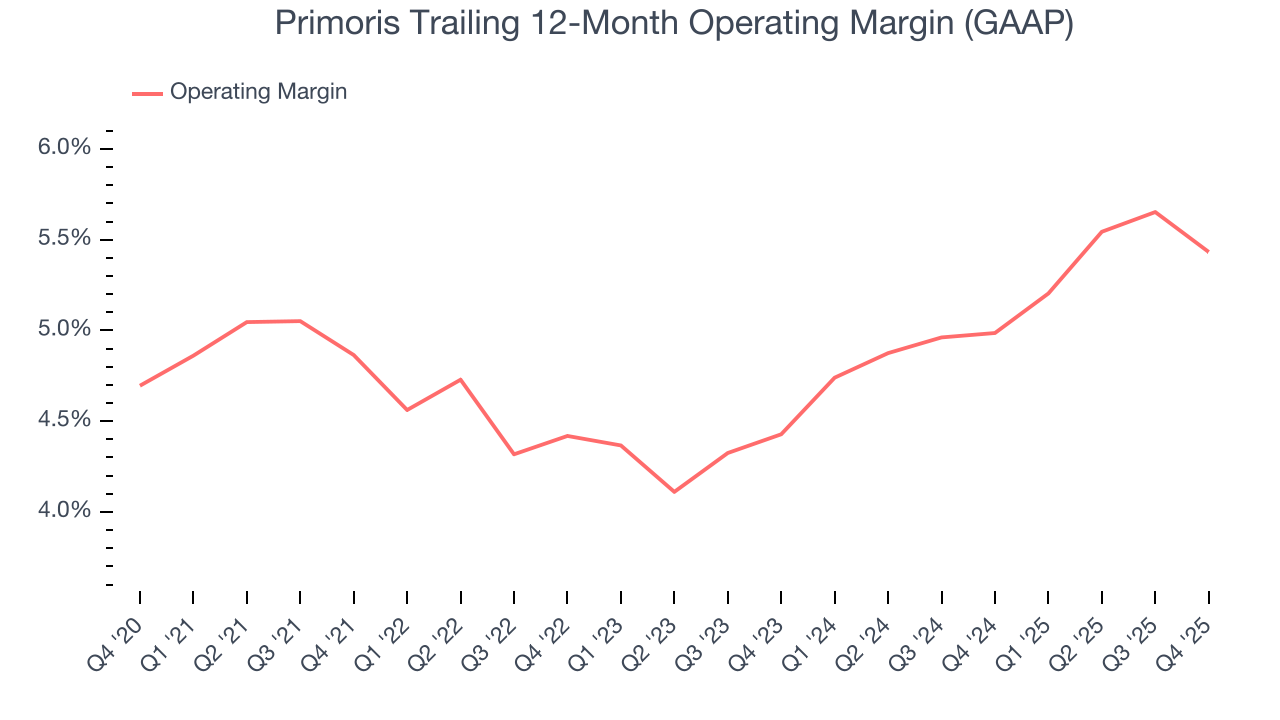

7. Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

Primoris’s operating margin might fluctuated slightly over the last 12 months but has remained more or less the same, averaging 4.9% over the last five years. This profitability was paltry for an industrials business and caused by its suboptimal cost structureand low gross margin.

Analyzing the trend in its profitability, Primoris’s operating margin might fluctuated slightly but has generally stayed the same over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, Primoris generated an operating margin profit margin of 4.2%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

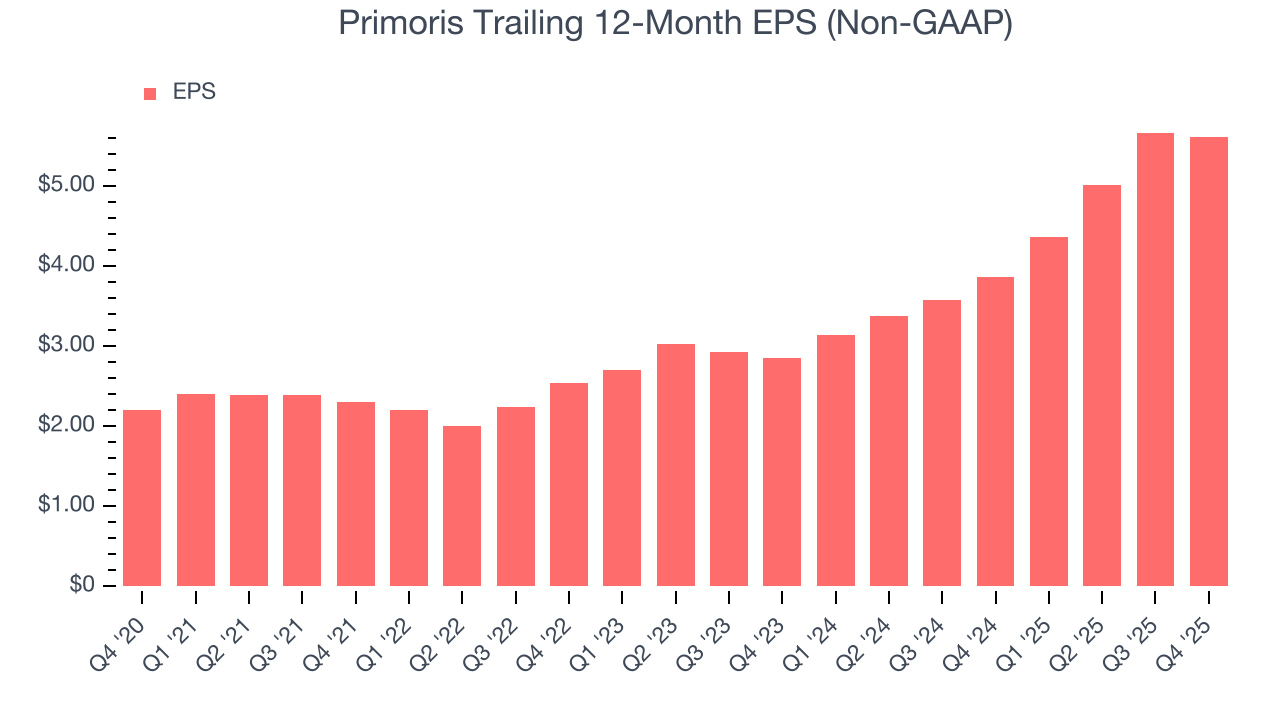

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Primoris’s EPS grew at an astounding 20.6% compounded annual growth rate over the last five years, higher than its 16.8% annualized revenue growth. However, we take this with a grain of salt because its operating margin didn’t improve and it didn’t repurchase its shares, meaning the delta came from reduced interest expenses or taxes.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Primoris, its two-year annual EPS growth of 40.4% was higher than its five-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.

In Q4, Primoris reported adjusted EPS of $1.08, down from $1.13 in the same quarter last year. Despite falling year on year, this print beat analysts’ estimates by 8.9%. Over the next 12 months, Wall Street expects Primoris’s full-year EPS of $5.62 to grow 5.3%.

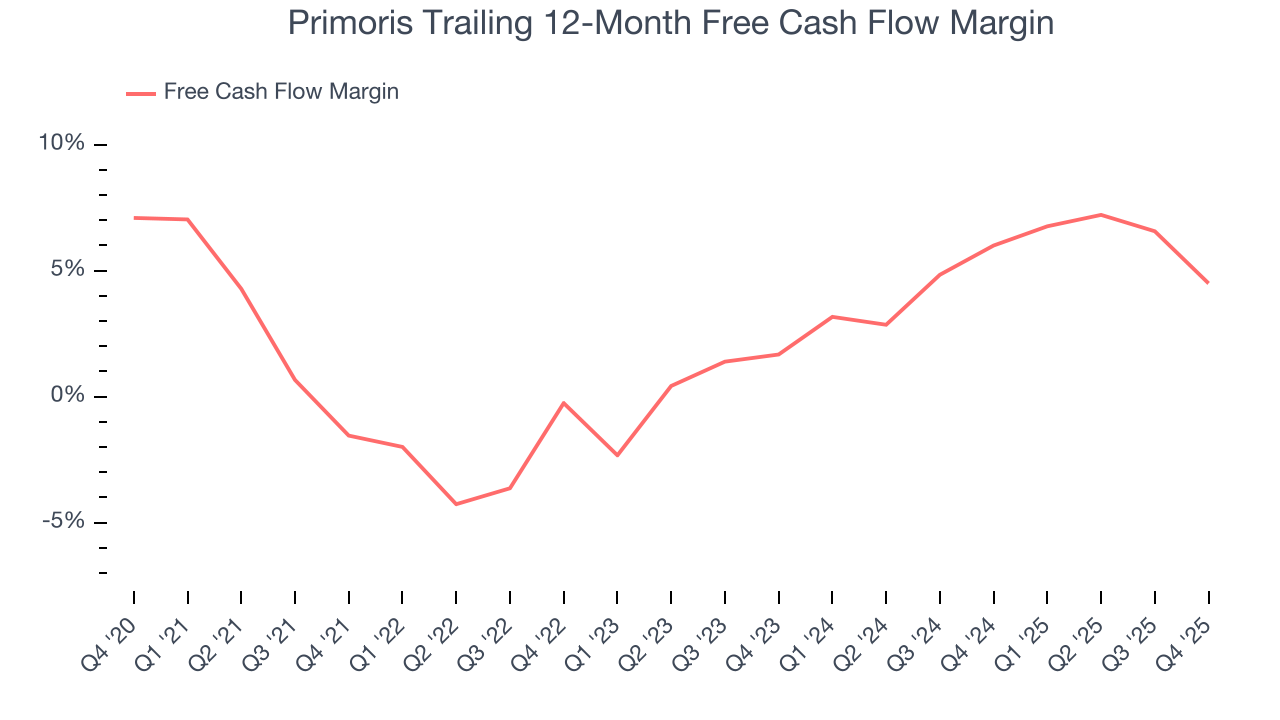

9. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Primoris has shown poor cash profitability over the last five years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 2.7%, lousy for an industrials business.

Taking a step back, an encouraging sign is that Primoris’s margin expanded by 6 percentage points during that time. The company’s improvement shows it’s heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose while its operating profitability was flat.

Primoris’s free cash flow clocked in at $121.1 million in Q4, equivalent to a 6.5% margin. The company’s cash profitability regressed as it was 9 percentage points lower than in the same quarter last year, but it’s still above its five-year average. We wouldn’t read too much into this quarter’s decline because investment needs can be seasonal, causing short-term swings. Long-term trends carry greater meaning.

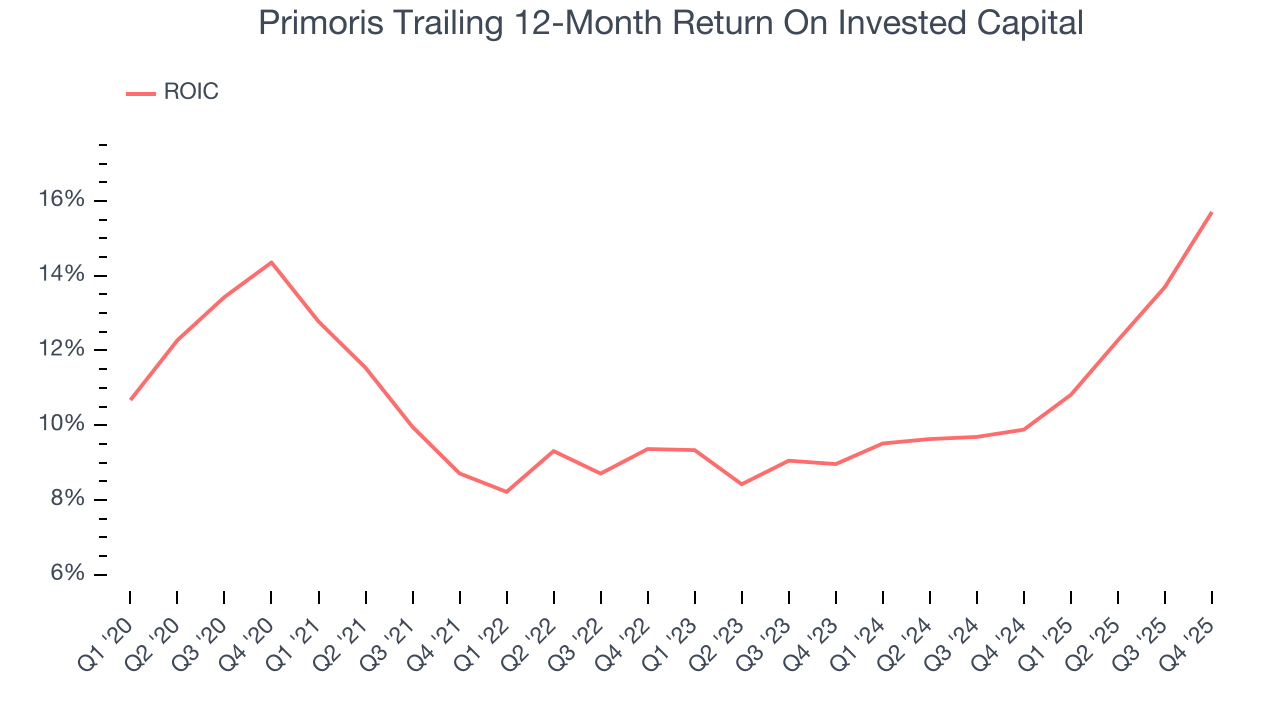

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Primoris’s management team makes decent investment decisions and generates value for shareholders. Its five-year average ROIC was 10.5%, slightly better than typical industrials business.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. On average, Primoris’s ROIC increased by 3.8 percentage points annually each year over the last few years. This is a great sign when paired with its already strong returns. It could suggest its competitive advantage or profitable growth opportunities are expanding.

11. Balance Sheet Assessment

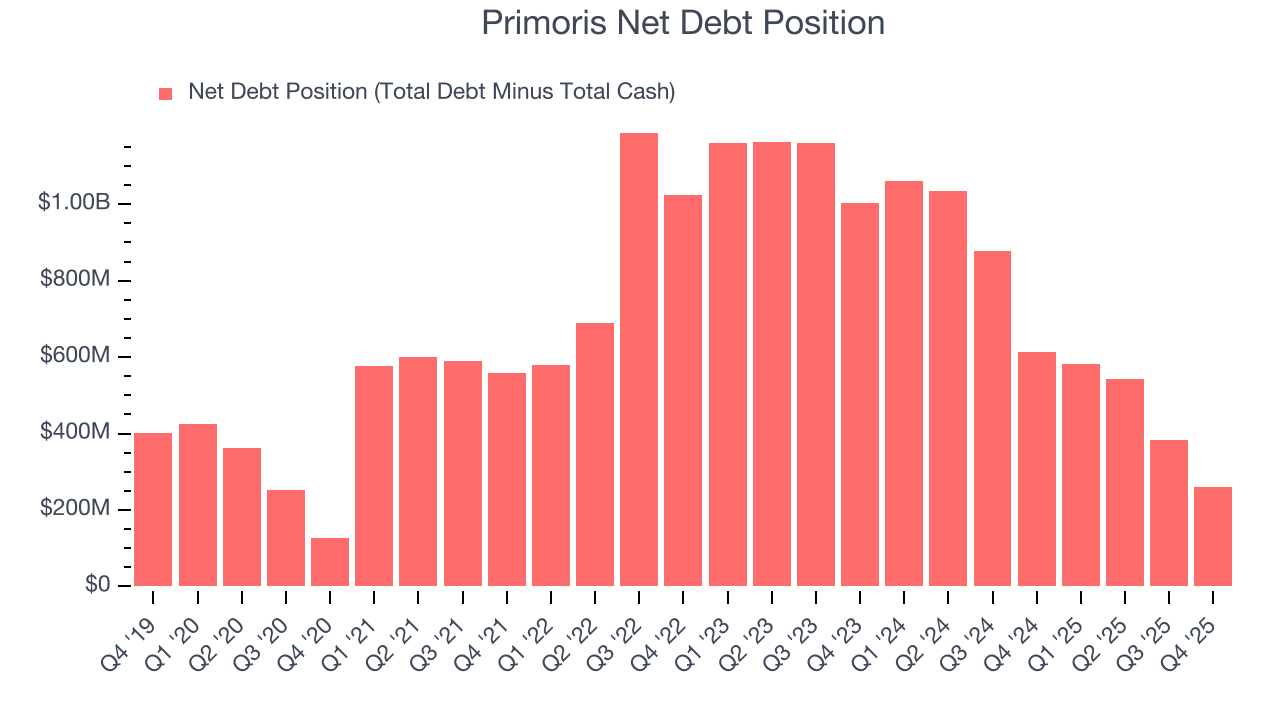

Primoris reported $535.5 million of cash and $795.5 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $531.1 million of EBITDA over the last 12 months, we view Primoris’s 0.5× net-debt-to-EBITDA ratio as safe. We also see its $25 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Primoris’s Q4 Results

We enjoyed seeing Primoris beat analysts’ revenue expectations this quarter. We were also happy its EBITDA outperformed Wall Street’s estimates. Zooming out, we think this was a good print with some key areas of upside. The market seemed to be hoping for more, and the stock traded down 7.7% to $152.83 immediately following the results.

13. Is Now The Time To Buy Primoris?

Updated: March 15, 2026 at 11:29 PM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Primoris.

There are multiple reasons why we think Primoris is an amazing business. For starters, its revenue growth was exceptional over the last five years. And while its low gross margins indicate some combination of competitive pressures and high production costs, its backlog growth has been marvelous. Additionally, Primoris’s rising cash profitability gives it more optionality.

Primoris’s P/E ratio based on the next 12 months is 22.3x. Scanning the industrials space today, Primoris’s fundamentals really stand out, and we like it at this price.

Wall Street analysts have a consensus one-year price target of $169.57 on the company (compared to the current share price of $133.48), implying they see 27% upside in buying Primoris in the short term.