Ruger (RGR)

Ruger keeps us up at night. Not only are its sales cratering but also its low returns on capital suggest it struggles to generate profits.― StockStory Analyst Team

1. News

2. Summary

Why We Think Ruger Will Underperform

Founded in 1949, Ruger (NYSE:RGR) is an American manufacturer of firearms for the commercial sporting market.

- Flat sales over the last five years suggest it must innovate and find new ways to grow

- Earnings per share fell by 24.6% annually over the last five years while its revenue was flat, showing each sale was less profitable

- Operating margin falls short of the industry average, and the smaller profit dollars make it harder to react to unexpected market developments

Ruger doesn’t meet our quality standards. We’re looking for better stocks elsewhere.

Why There Are Better Opportunities Than Ruger

At $39.19 per share, Ruger trades at 20.2x forward P/E. This multiple is higher than that of consumer discretionary peers; it’s also rich for the top-line growth of the company. Not a great combination.

We prefer to invest in similarly-priced but higher-quality companies with superior earnings growth.

3. Ruger (RGR) Research Report: Q4 CY2025 Update

American firearm manufacturing company Ruger (NYSE:RGR) announced better-than-expected revenue in Q4 CY2025, with sales up 3.7% year on year to $151.1 million. Its non-GAAP profit of $0.26 per share was 17.5% below analysts’ consensus estimates.

Ruger (RGR) Q4 CY2025 Highlights:

- Revenue: $151.1 million vs analyst estimates of $139.2 million (3.7% year-on-year growth, 8.5% beat)

- Adjusted EPS: $0.26 vs analyst expectations of $0.32 (17.5% miss)

- Adjusted EBITDA: $29.55 million vs analyst estimates of $11.22 million (19.6% margin, significant beat)

- Operating Margin: 2.3%, down from 8.9% in the same quarter last year

- Free Cash Flow Margin: 8.2%, down from 11.2% in the same quarter last year

- Market Capitalization: $597 million

Company Overview

Founded in 1949, Ruger (NYSE:RGR) is an American manufacturer of firearms for the commercial sporting market.

Ruger was founded by William B. Ruger and Alexander McCormick Sturm in a small rented machine shop, with their first product, the Ruger Standard .22 caliber pistol, setting a high standard for reliable, well-made guns. The founders' vision was to offer shooters quality firearms that were both functional and affordable, filling a gap in the market for well-crafted weapons that could be enjoyed by shooting enthusiasts of all levels.

Today, Ruger provides an array of firearms, including rifles, pistols, and revolvers, catering to the needs of hunters, competitive shooters, and those seeking personal defense options. Specifically, the company's customers include law enforcement and military organizations as well as recreational shooters.

4. Consumer Discretionary - Leisure Products

The Consumer Discretionary sector, by definition, is made up of companies selling non-essential goods and services. When economic conditions deteriorate or tastes shift, consumers can easily cut back or eliminate these purchases. For long-term investors with five-year holding periods, this creates a structural challenge: the sector is inherently hit-driven, with low switching costs and fickle customers. As a result, only a handful of companies can reliably grow demand and compound earnings over long periods, which is why our bar is high and High Quality ratings are rare.

Leisure products companies manufacture recreational goods such as bicycles, marine vessels, fitness equipment, camping gear, and musical instruments. Tailwinds include heightened outdoor-activity participation, health-and-wellness awareness, and periodic innovation cycles that drive trade-up purchases. Headwinds are pronounced: demand is highly discretionary and sensitive to economic cycles—consumers readily defer big-ticket leisure purchases during downturns. Post-pandemic normalization has created excess channel inventory after demand surged then retreated. Raw-material and shipping cost inflation squeezes margins, while competition from low-cost imports and a fragmented market make pricing power elusive for most players.

Competitors in the firearm sector include Smith & Wesson Brands (NASDAQ:SWBI), Vista Outdoor (NYSE:VSTO), and American Outdoor Brands (NASDAQ:AOUT).

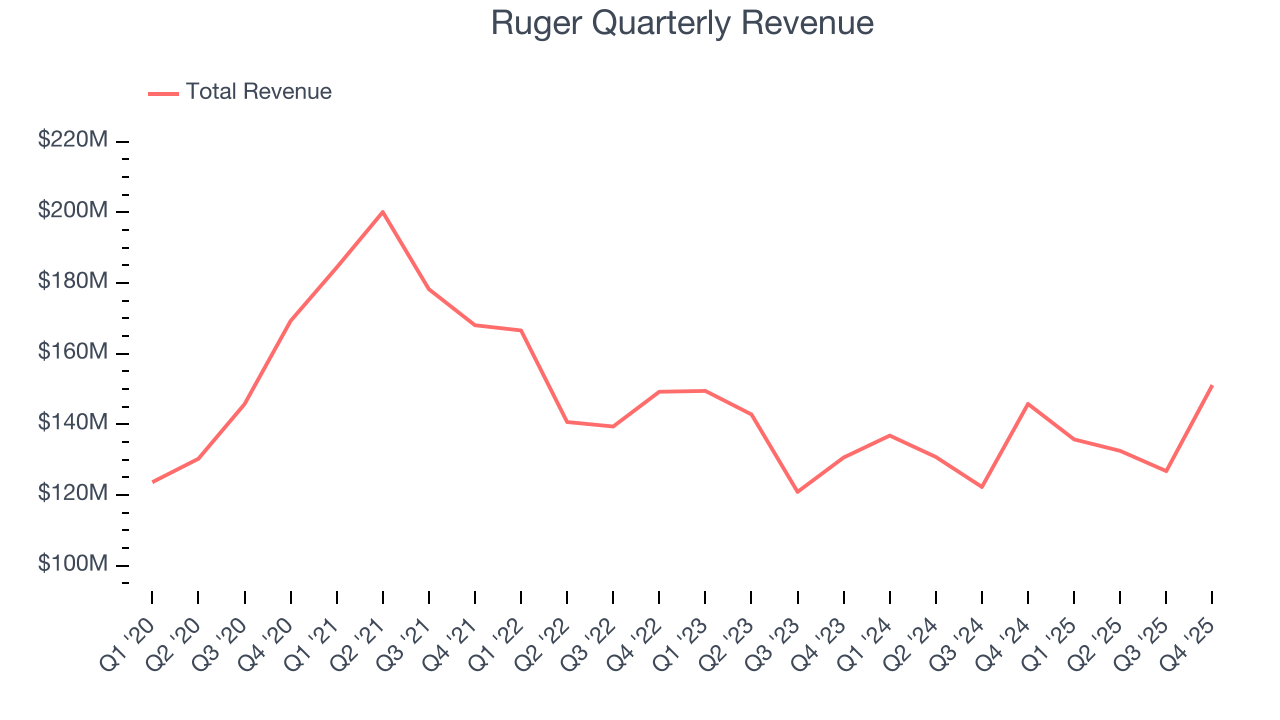

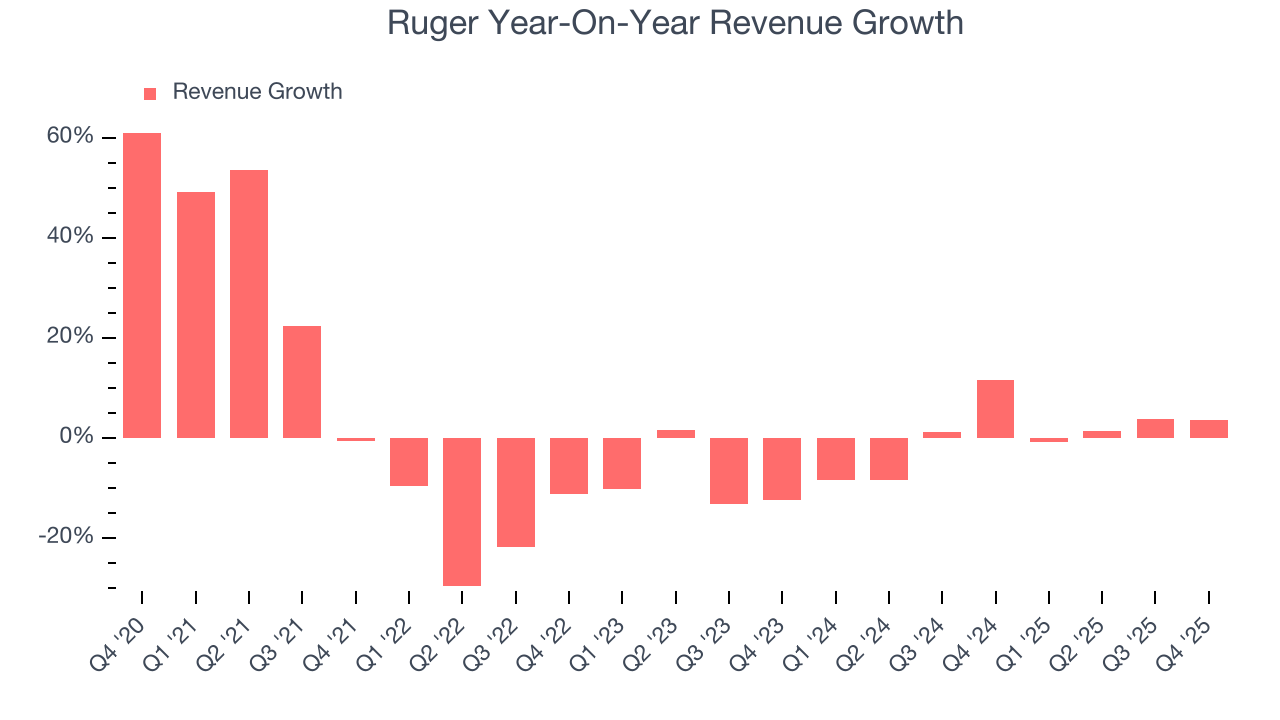

5. Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Unfortunately, Ruger struggled to consistently increase demand as its $546.1 million of sales for the trailing 12 months was close to its revenue five years ago. This was below our standards and is a sign of poor business quality.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. Just like its five-year trend, Ruger’s revenue over the last two years was flat, suggesting it is in a slump.

This quarter, Ruger reported modest year-on-year revenue growth of 3.7% but beat Wall Street’s estimates by 8.5%.

Looking ahead, sell-side analysts expect revenue to decline by 2.7% over the next 12 months, a slight deceleration versus the last two years. This projection is underwhelming and implies its products and services will see some demand headwinds.

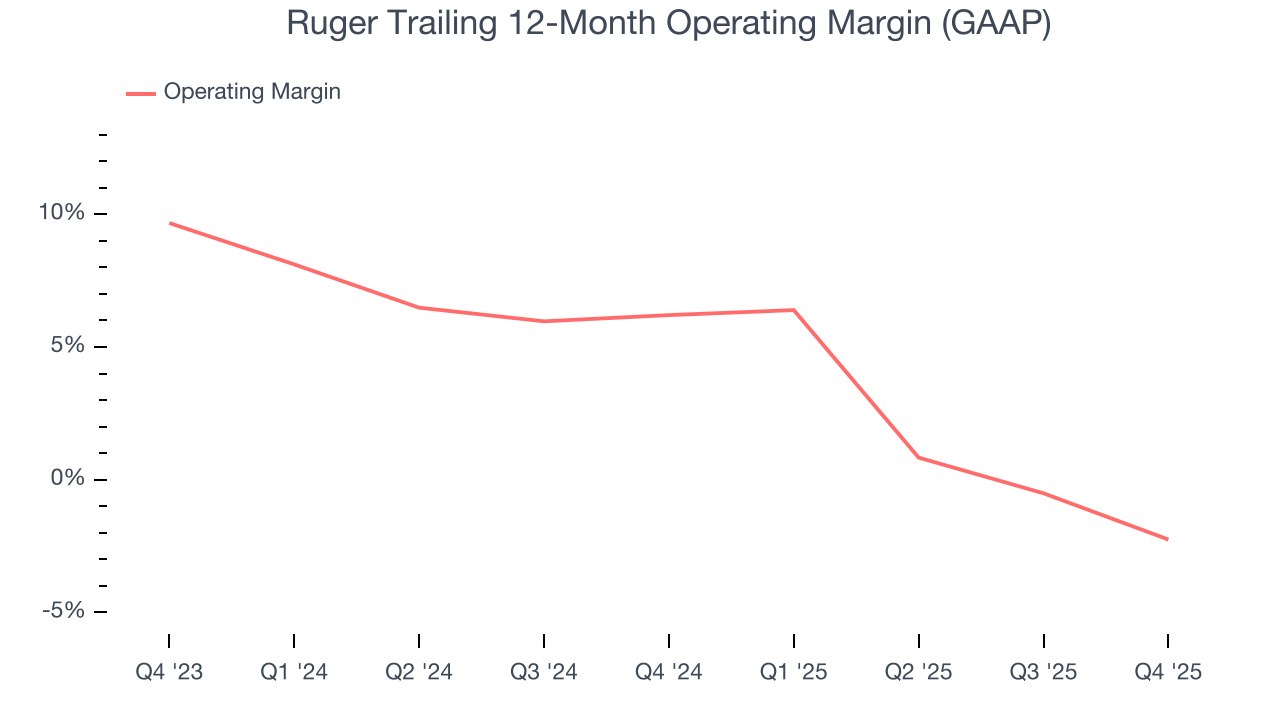

6. Operating Margin

Ruger’s operating margin has shrunk over the last 12 months and averaged 1.9% over the last two years. The company’s profitability was mediocre for a consumer discretionary business and shows it couldn’t pass its higher operating expenses onto its customers.

This quarter, Ruger generated an operating margin profit margin of 2.3%, down 6.6 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

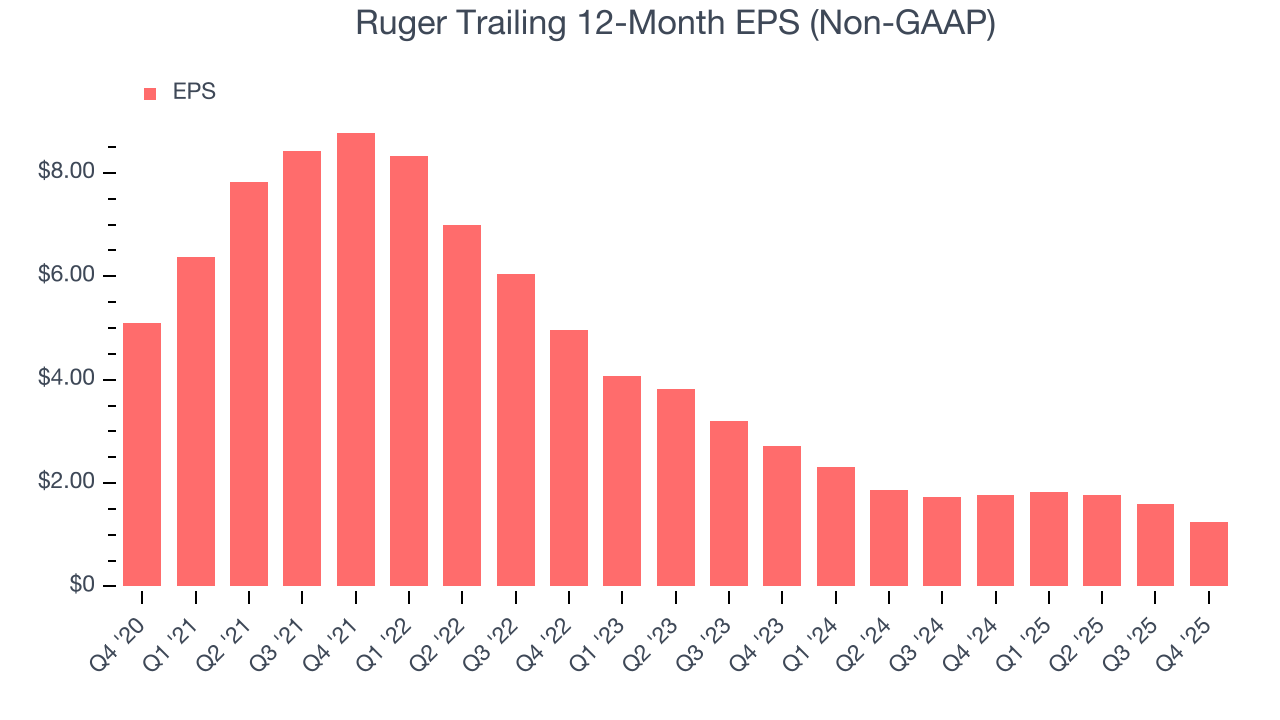

7. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Ruger, its EPS declined by 24.6% annually over the last five years while its revenue was flat. This tells us the company struggled because its fixed cost base made it difficult to adjust to choppy demand.

In Q4, Ruger reported adjusted EPS of $0.26, down from $0.62 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects Ruger’s full-year EPS of $1.24 to grow 42.7%.

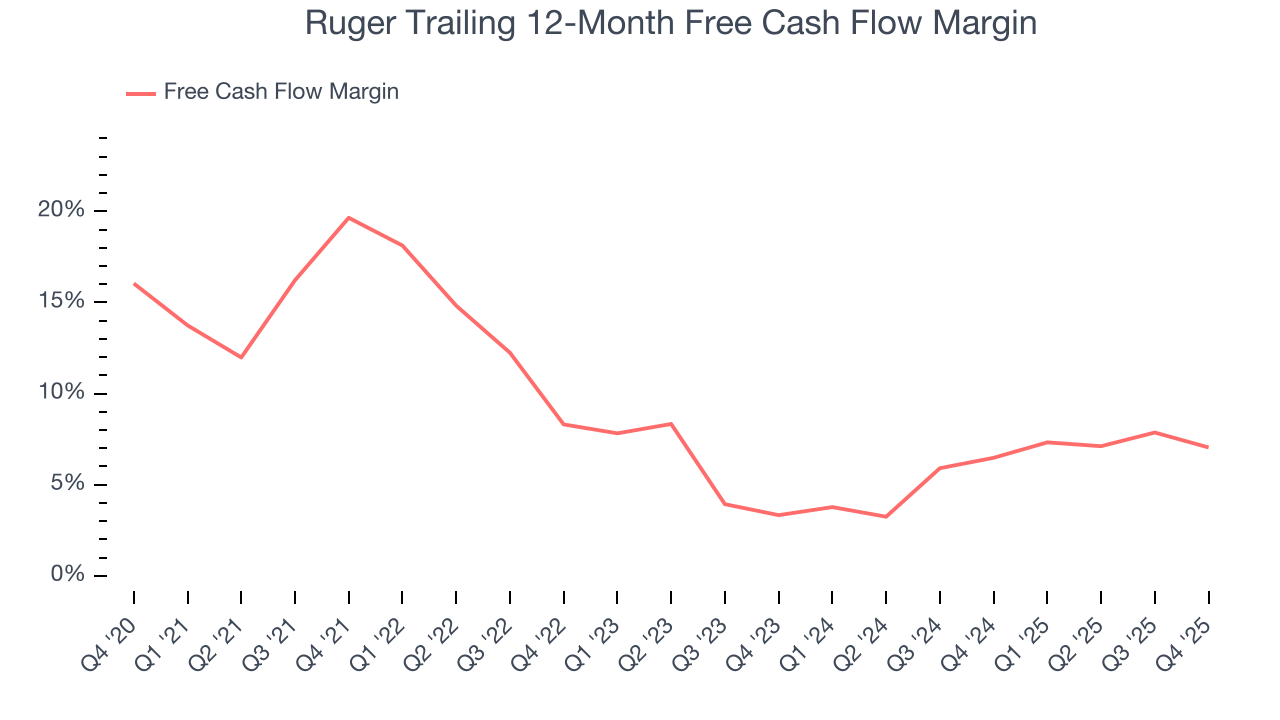

8. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Ruger has shown poor cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 6.8%, lousy for a consumer discretionary business.

Ruger’s free cash flow clocked in at $12.33 million in Q4, equivalent to a 8.2% margin. The company’s cash profitability regressed as it was 3.1 percentage points lower than in the same quarter last year, but it’s still above its two-year average. We wouldn’t read too much into this quarter’s decline because investment needs can be seasonal, causing short-term swings. Long-term trends are more important.

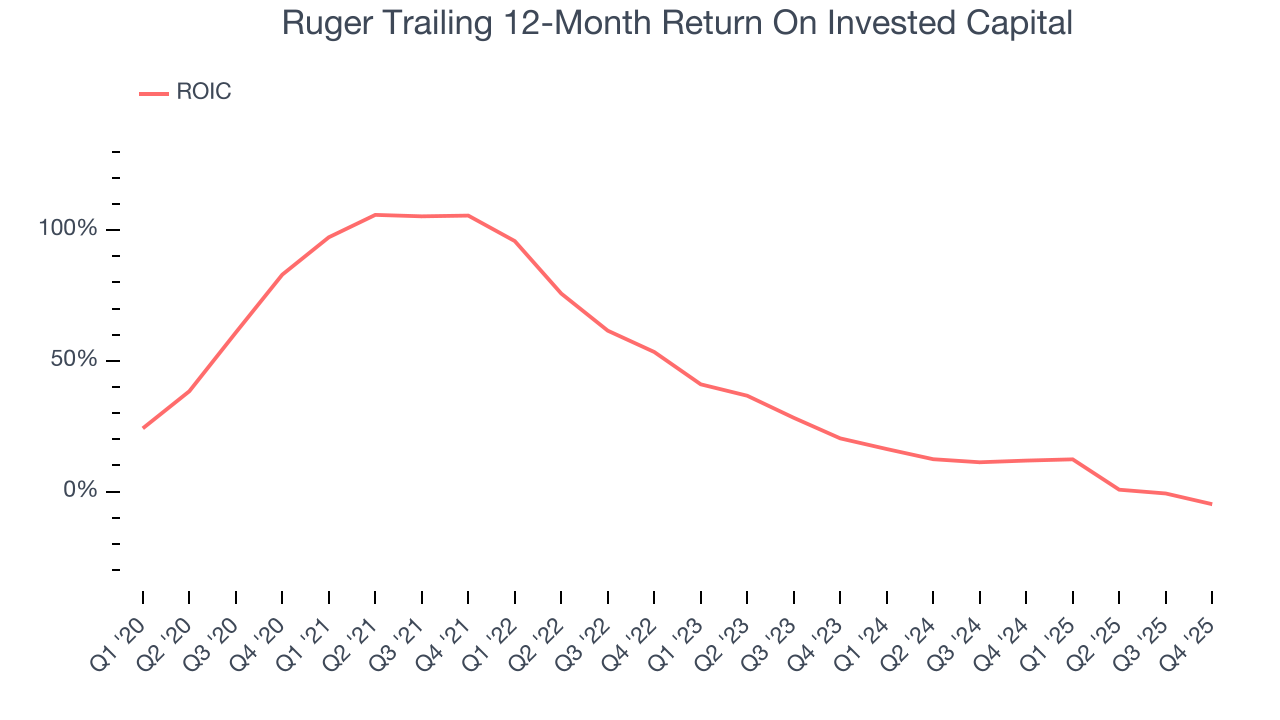

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Ruger historically did a mediocre job investing in profitable growth initiatives. Its four-year average ROIC was 20.2%, somewhat low compared to the best consumer discretionary companies that consistently pump out 25%+.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Ruger’s ROIC has unfortunately decreased significantly. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

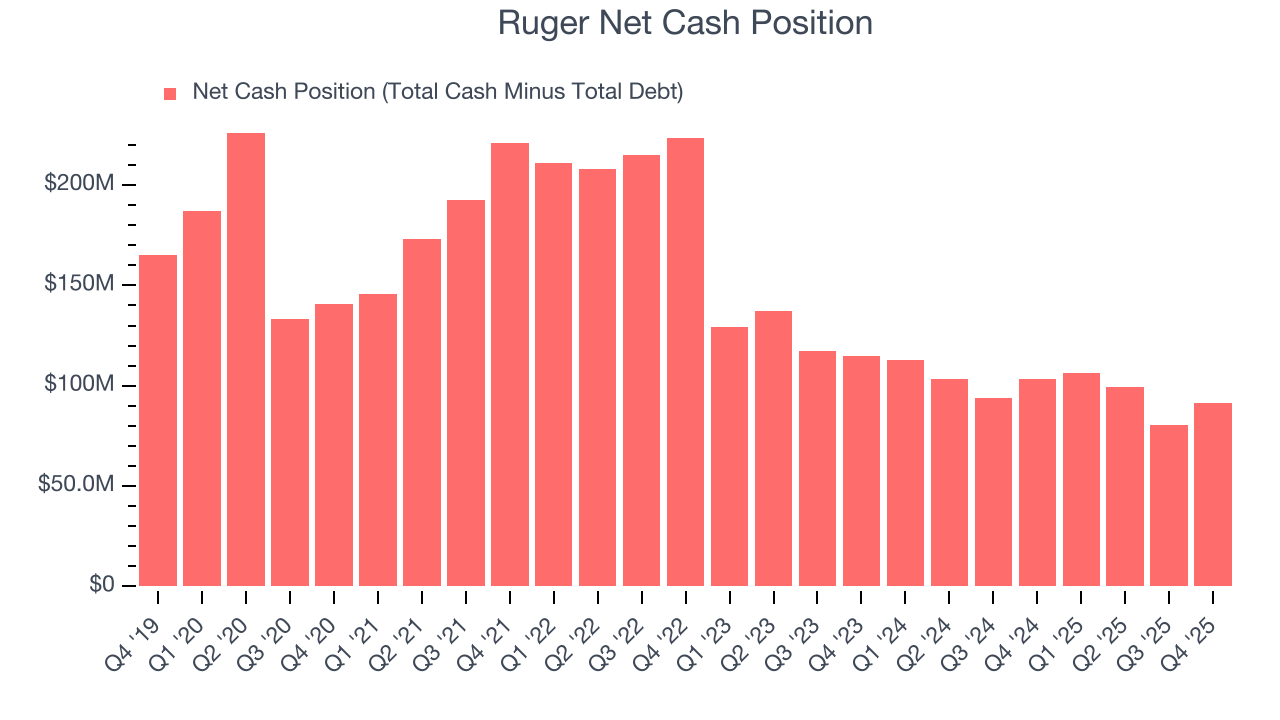

10. Balance Sheet Assessment

Businesses that maintain a cash surplus face reduced bankruptcy risk.

Ruger is a well-capitalized company with $92.53 million of cash and $1.16 million of debt on its balance sheet. This $91.38 million net cash position is 15.3% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

11. Key Takeaways from Ruger’s Q4 Results

We were impressed by how significantly Ruger blew past analysts’ EBITDA expectations this quarter. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. On the other hand, its EPS missed. Overall, we think this was a solid quarter with some key areas of upside. The market seemed to be hoping for more, and the stock traded down 1.1% to $37.54 immediately following the results.

12. Is Now The Time To Buy Ruger?

Updated: March 16, 2026 at 11:00 PM EDT

Are you wondering whether to buy Ruger or pass? We urge investors to not only consider the latest earnings results but also longer-term business quality and valuation as well.

Ruger falls short of our quality standards. While its projected EPS for the next year implies the company’s fundamentals will improve, the downside is its declining EPS over the last five years makes it a less attractive asset to the public markets. On top of that, its low free cash flow margins give it little breathing room.

Ruger’s P/E ratio based on the next 12 months is 20.2x. This valuation tells us a lot of optimism is priced in - we think other companies feature superior fundamentals at the moment.

Wall Street analysts have a consensus one-year price target of $45.50 on the company (compared to the current share price of $39.19).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.