Revolve (RVLV)

Revolve is in for a bumpy ride. Its underwhelming revenue growth and failure to generate meaningful free cash flow is a concerning trend.― StockStory Analyst Team

1. News

2. Summary

Why We Think Revolve Will Underperform

Launched in 2003 by software engineers Michael Mente and Mike Karanikolas, Revolve (NASDAQ:RVLV) is a fashion retailer leveraging social media and a community of fashion influencers to drive its merchandising strategy.

- Earnings per share were flat over the last three years and fell short of the peer group average

- Lackluster 3.6% annual revenue growth over the last three years indicates the company is losing ground to competitors

- Excessive marketing spend signals little organic demand and traction for its platform

Revolve doesn’t check our boxes. We’d rather invest in businesses with stronger moats.

Why There Are Better Opportunities Than Revolve

Revolve is trading at $22.92 per share, or 14.3x forward EV/EBITDA. This multiple expensive for its subpar fundamentals.

Paying up for elite businesses with strong earnings potential is better than investing in lower-quality companies with shaky fundamentals. That’s how you avoid big downside over the long term.

3. Revolve (RVLV) Research Report: Q4 CY2025 Update

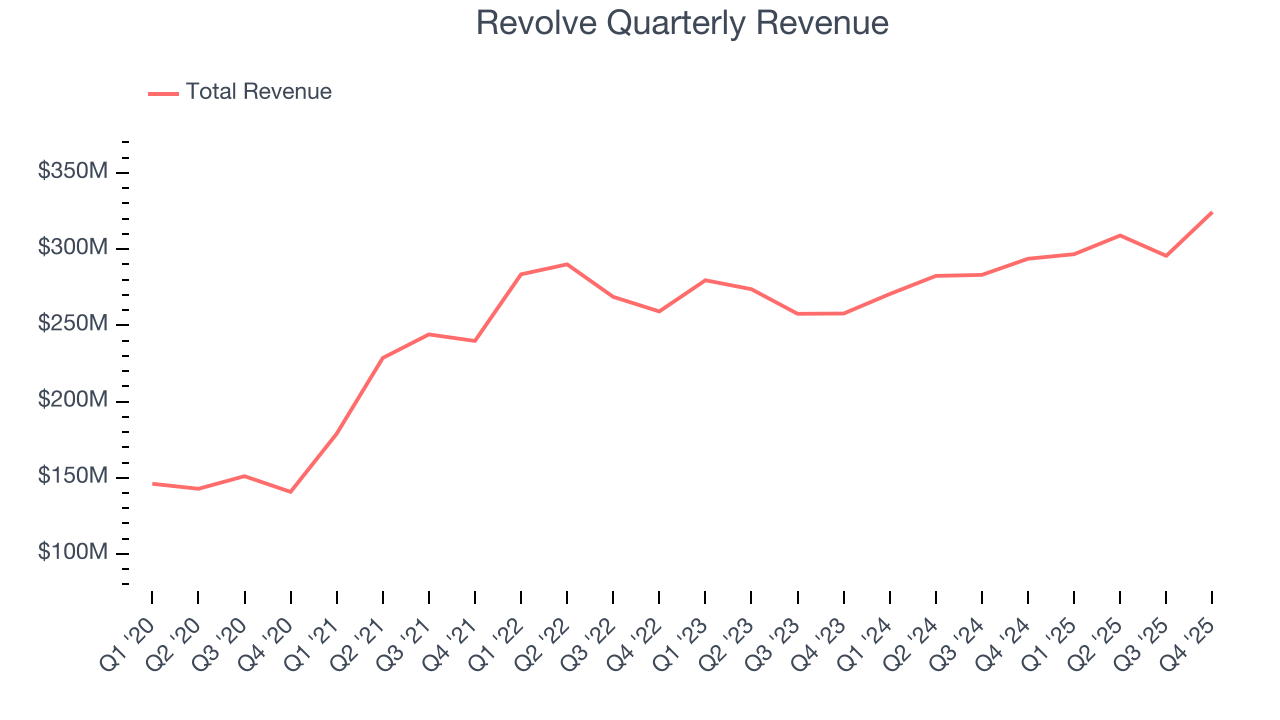

Online fashion retailer Revolve (NASDAQ:RVLV) reported Q4 CY2025 results exceeding the market’s revenue expectations, with sales up 10.4% year on year to $324.4 million. Its GAAP profit of $0.26 per share was 57.8% above analysts’ consensus estimates.

Revolve (RVLV) Q4 CY2025 Highlights:

- Revenue: $324.4 million vs analyst estimates of $305.5 million (10.4% year-on-year growth, 6.2% beat)

- EPS (GAAP): $0.26 vs analyst estimates of $0.16 (57.8% beat)

- Adjusted EBITDA: $26.26 million vs analyst estimates of $19.61 million (8.1% margin, 33.9% beat)

- Operating Margin: 6.3%, up from 3.9% in the same quarter last year

- Free Cash Flow was -$12.85 million, down from $7.50 million in the previous quarter

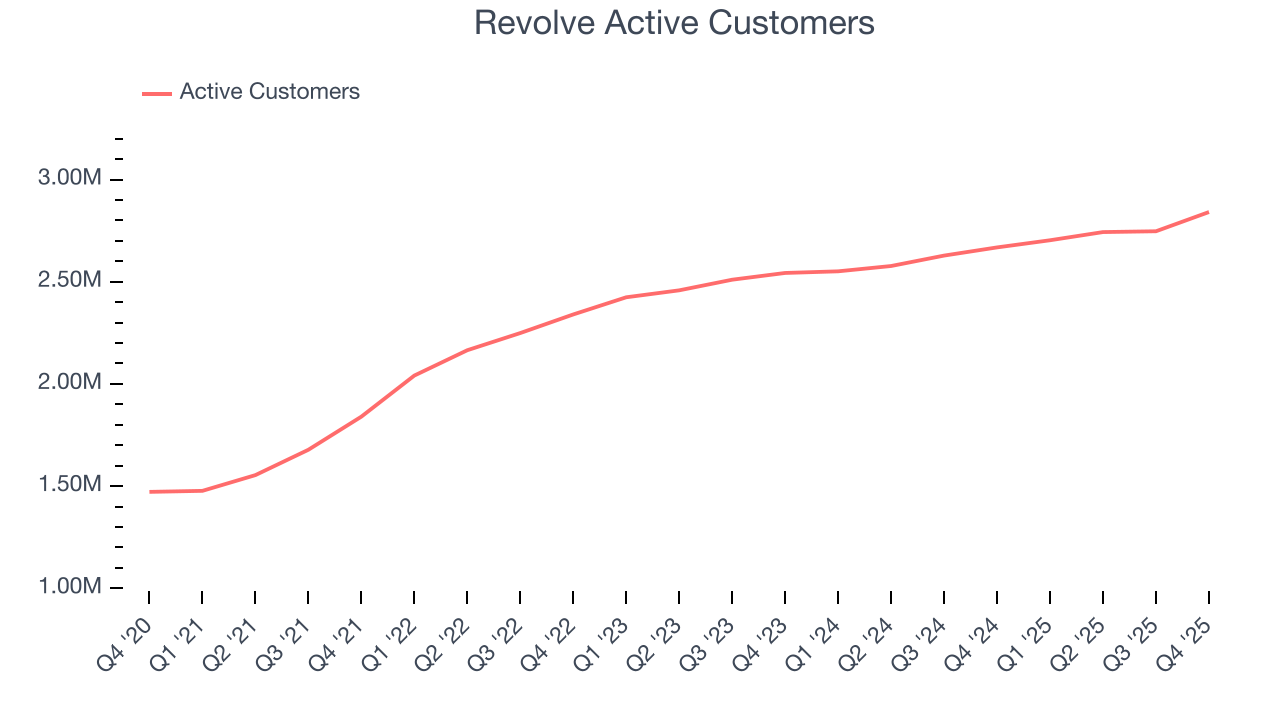

- Active Customers : 2.84 million, up 173,000 year on year

- Market Capitalization: $1.73 billion

Company Overview

Launched in 2003 by software engineers Michael Mente and Mike Karanikolas, Revolve (NASDAQ:RVLV) is a fashion retailer leveraging social media and a community of fashion influencers to drive its merchandising strategy.

Revolve is focused on Millennials and Generation Z customers, who spend significant amounts of time on social media and often look for digital content from influencers as their inspiration for purchasing decisions. It leverages a data-driven buying and merchandising model, which spends and monitors its marketing dollars across a network of over 3,500 social media influencers’ fashion choices on TikTok, Instagram, and YouTube.

Specifically, the company’s "read and react" merchandising approach identifies and invests behind new trends in small initial order quantities. It also employs a “test and reorder” model, which minimizes fashion risk like its fast-fashion peers by quickly pivoting from one style to another.

Revolve operates through two main brands: Revolve and Forward. Revolve focuses on a broad yet curated assortment of premium apparel, footwear, accessories, and beauty products while Forward is an aspiring luxury brand.

4. Online Retail

Consumers ever rising demand for convenience, selection, and speed are secular engines underpinning ecommerce adoption. For years prior to Covid, ecommerce penetration as a percentage of overall retail would grow 1-2% annually, but in 2020 adoption accelerated by 5%, reaching 25%, as increased emphasis on convenience drove consumers to structurally buy more online. The surge in buying caused many online retailers to rapidly grow their logistics infrastructures, preparing them for further growth in the years ahead as consumer shopping habits continue to shift online.

Revolve (NYSE:RVLV) competes with Stitchfix (NASDAQ: SFIX), The RealReal (NASDAQ:REAL), Poshmark (NASDAQ: POSH), Asos (AIM:ASC), and boohoo group (AIM:BOO).

5. Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Regrettably, Revolve’s sales grew at a sluggish 3.6% compounded annual growth rate over the last three years. This was below our standard for the consumer internet sector and is a tough starting point for our analysis.

This quarter, Revolve reported year-on-year revenue growth of 10.4%, and its $324.4 million of revenue exceeded Wall Street’s estimates by 6.2%.

Looking ahead, sell-side analysts expect revenue to grow 4.8% over the next 12 months, similar to its three-year rate. Although this projection implies its newer products and services will catalyze better top-line performance, it is still below the sector average.

6. Active Customers

Buyer Growth

As an online retailer, Revolve generates revenue growth by expanding its number of users and the average order size in dollars.

Over the last two years, Revolve’s active customers , a key performance metric for the company, increased by 5.4% annually to 2.84 million in the latest quarter. This growth rate lags behind the hottest consumer internet applications. If Revolve wants to accelerate growth, it likely needs to engage users more effectively with its existing offerings or innovate with new products.

In Q4, Revolve added 173,000 active customers , leading to 6.5% year-on-year growth. The quarterly print was higher than its two-year result, suggesting its new initiatives are accelerating buyer growth.

Revenue Per Buyer

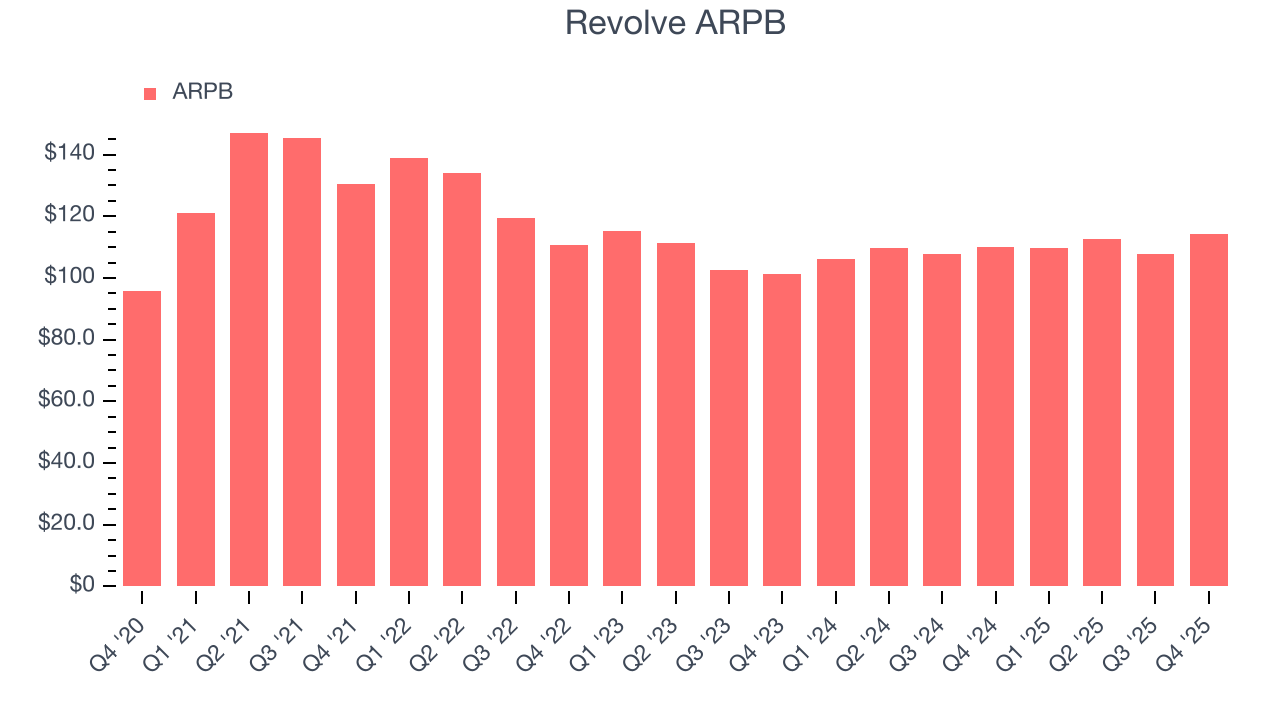

Average revenue per buyer (ARPB) is a critical metric to track because it measures how much customers spend per order.

Revolve’s ARPB growth has been subpar over the last two years, averaging 1.7%. This isn’t great when combined with its weaker active customers performance. If Revolve tries boosting ARPB by taking a more aggressive approach to monetization, it’s unclear whether buyer growth would be sustainable.

This quarter, Revolve’s ARPB clocked in at $114.17. It grew by 3.7% year on year, slower than its buyer growth.

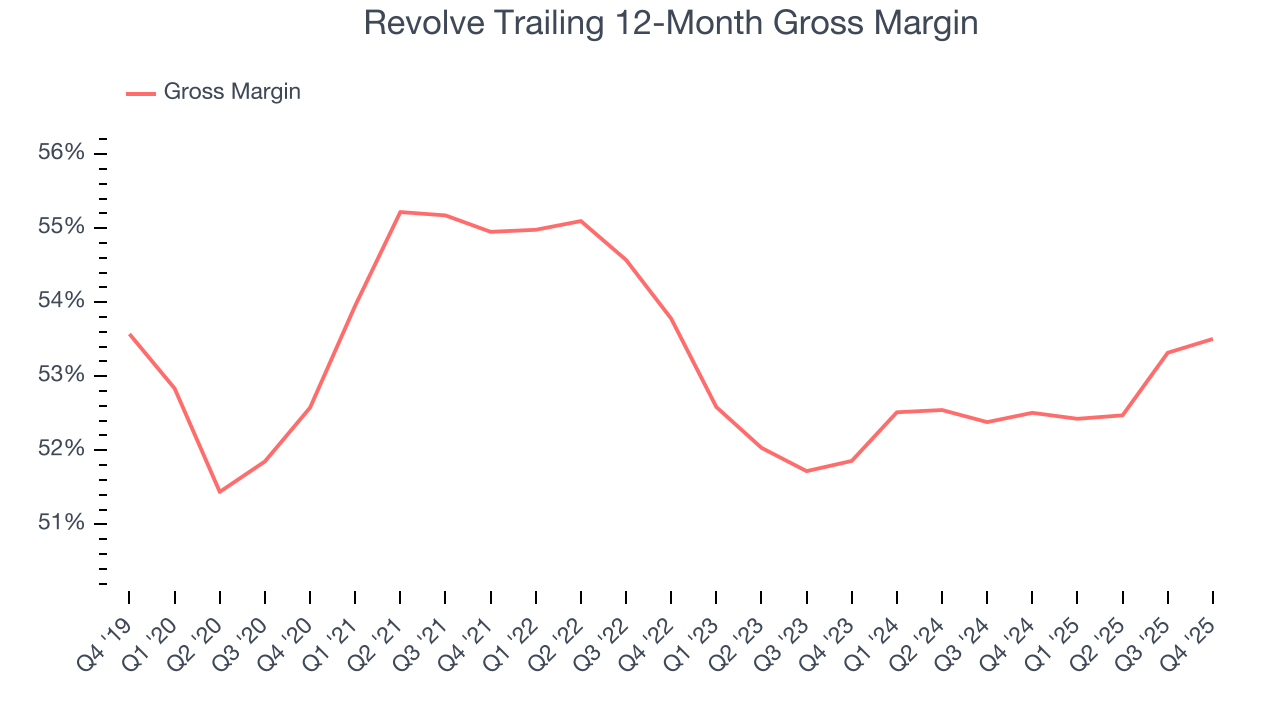

7. Gross Margin & Pricing Power

For online retail (separate from online marketplaces) businesses like Revolve, gross profit tells us how much money the company gets to keep after covering the base cost of its products and services, which typically include the cost of acquiring the products sold, shipping and fulfillment, customer service, and digital infrastructure.

Revolve’s gross margin is slightly below the average consumer internet company, giving it less room to invest in areas such as product and marketing to grow its presence. As you can see below, it averaged a 53% gross margin over the last two years. That means Revolve paid its providers a lot of money ($46.97 for every $100 in revenue) to run its business.

This quarter, Revolve’s gross profit margin was 53.3%, in line with the same quarter last year. Zooming out, the company’s full-year margin has remained steady over the past 12 months, suggesting its input costs have been stable and it isn’t under pressure to lower prices.

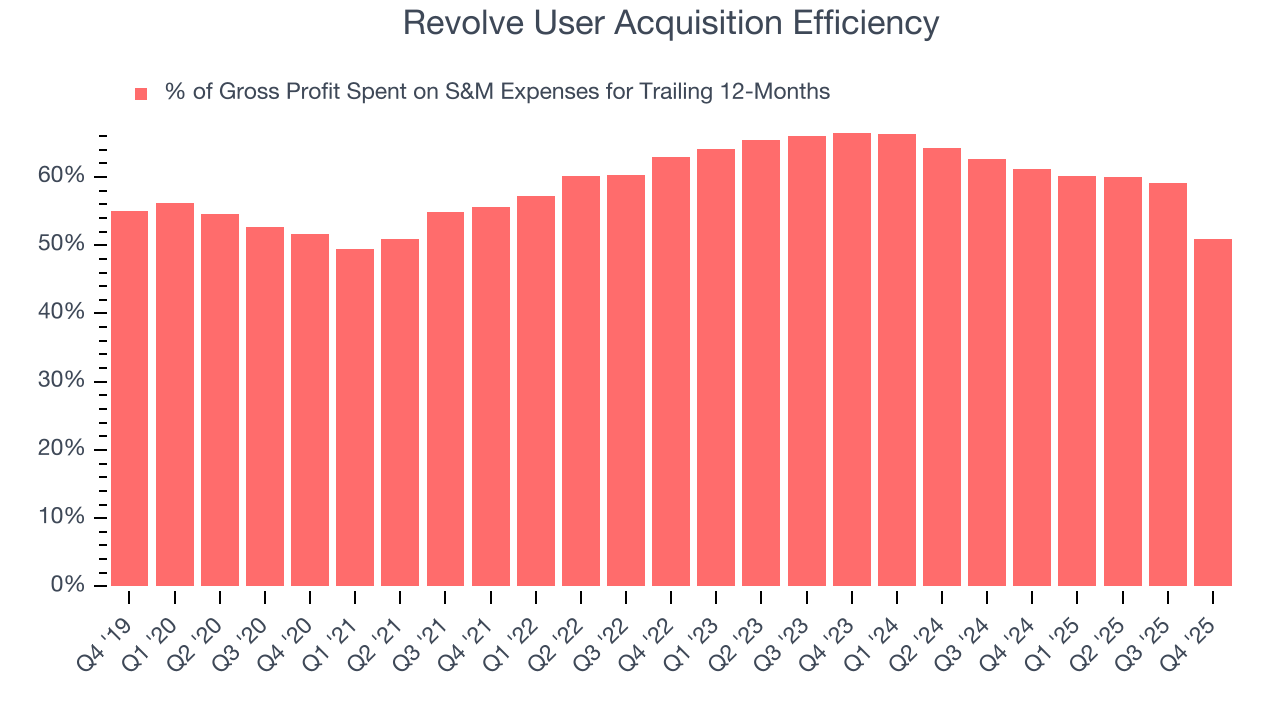

8. User Acquisition Efficiency

Consumer internet businesses like Revolve grow from a combination of product virality, paid advertisement, and incentives (unlike enterprise software products, which are often sold by dedicated sales teams).

It’s relatively expensive for Revolve to acquire new users as the company has spent 50.9% of its gross profit on sales and marketing expenses over the last year. This inefficiency indicates that Revolve operates in a competitive market and must continue investing to maintain an acceptable growth trajectory.

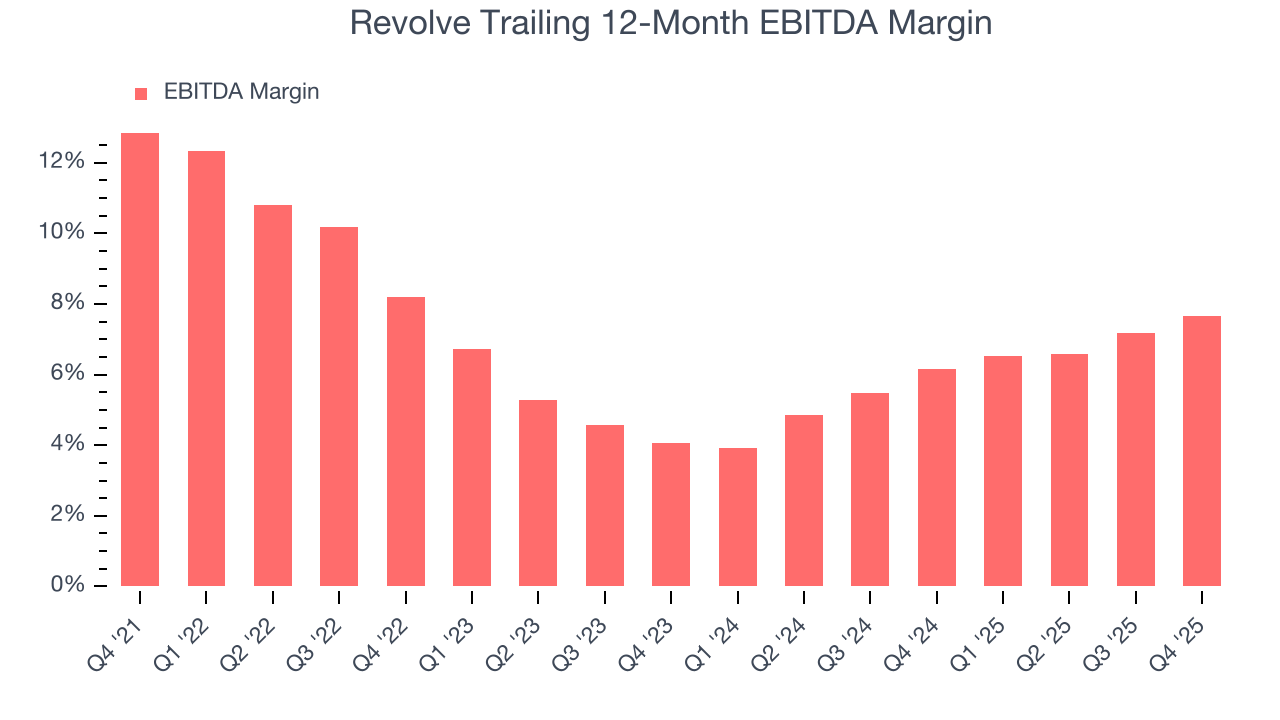

9. EBITDA

Investors regularly analyze operating income to understand a company’s profitability. Similarly, EBITDA is a common profitability metric for consumer internet companies because it excludes various one-time or non-cash expenses, offering a better perspective of the business’s profit potential.

Revolve’s EBITDA margin has risen over the last 12 months and averaged 6.9% over the last two years. Its solid profitability for a consumer internet business shows it’s an efficient company that manages its expenses effectively. This result was particularly impressive because of its low gross margin, which is mostly a factor of what it sells and takes huge shifts to move meaningfully. Companies have more control over their operating margins, and it’s a show of well-managed operations if they’re high when gross margins are low.

Looking at the trend in its profitability, Revolve’s EBITDA margin might fluctuated slightly but has generally stayed the same over the last few years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, Revolve generated an EBITDA margin profit margin of 8.1%, up 1.9 percentage points year on year. The increase was encouraging, and because its EBITDA margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

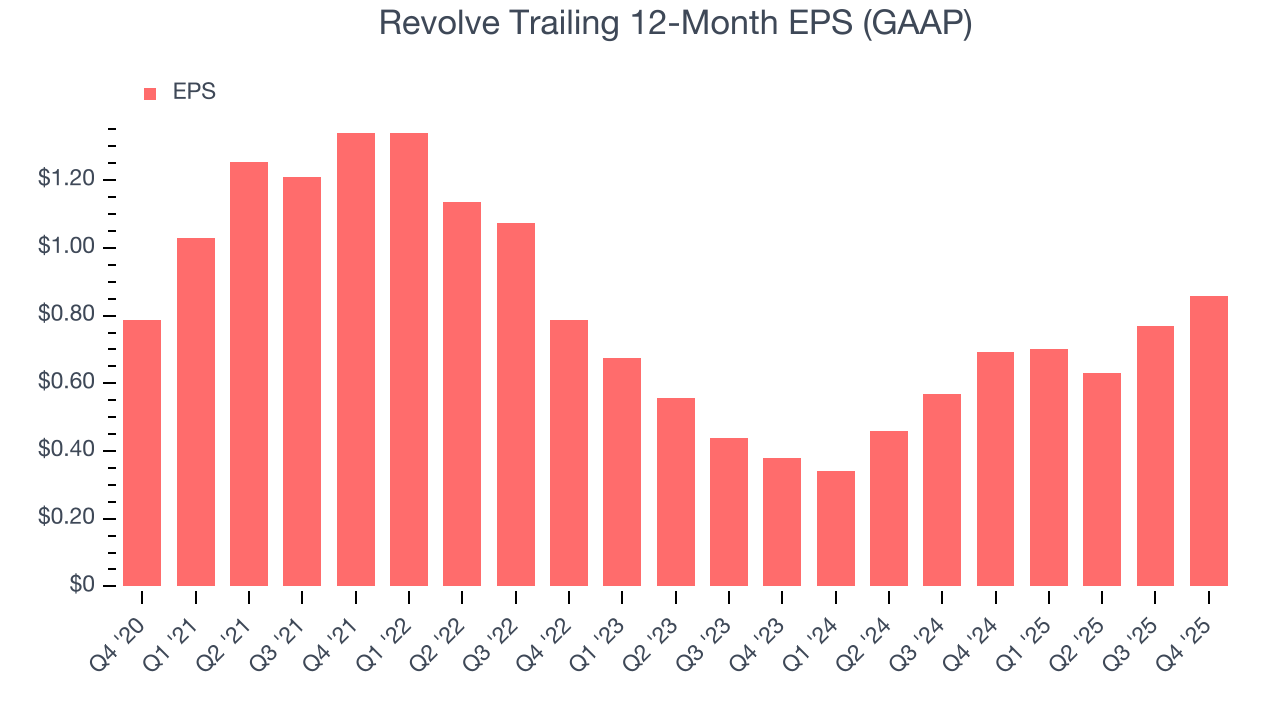

10. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Revolve’s weak 3% annual EPS growth over the last three years aligns with its revenue performance. On the bright side, this tells us its incremental sales were profitable.

In Q4, Revolve reported EPS of $0.26, up from $0.17 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Revolve’s full-year EPS of $0.86 to shrink by 1.4%.

11. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

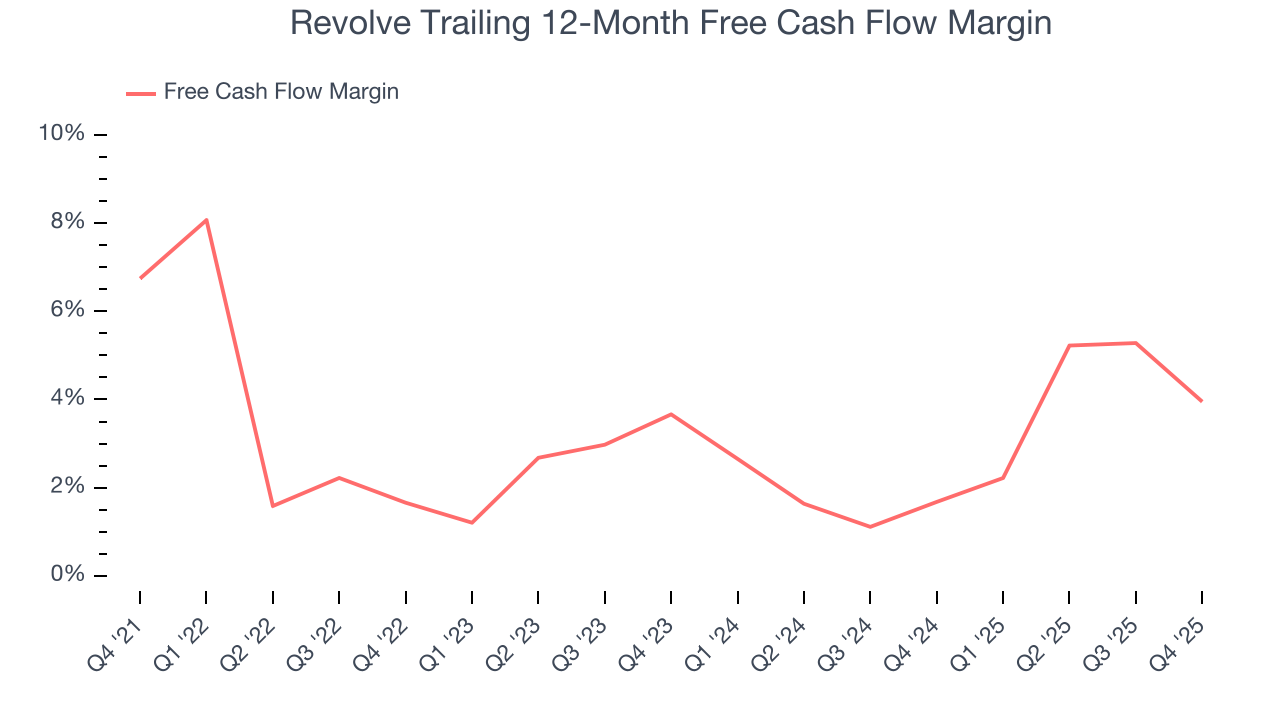

Revolve has shown mediocre cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 2.9%, subpar for a consumer internet business.

Taking a step back, an encouraging sign is that Revolve’s margin expanded by 2.3 percentage points over the last few years. The company’s improvement shows it’s heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose while its operating profitability was flat.

Revolve burned through $12.85 million of cash in Q4, equivalent to a negative 4% margin. The company’s cash burn increased meaningfully year on year and is a deviation from its longer-term margin, indicating it is a seasonal business that must build up inventory during certain quarters.

12. Balance Sheet Assessment

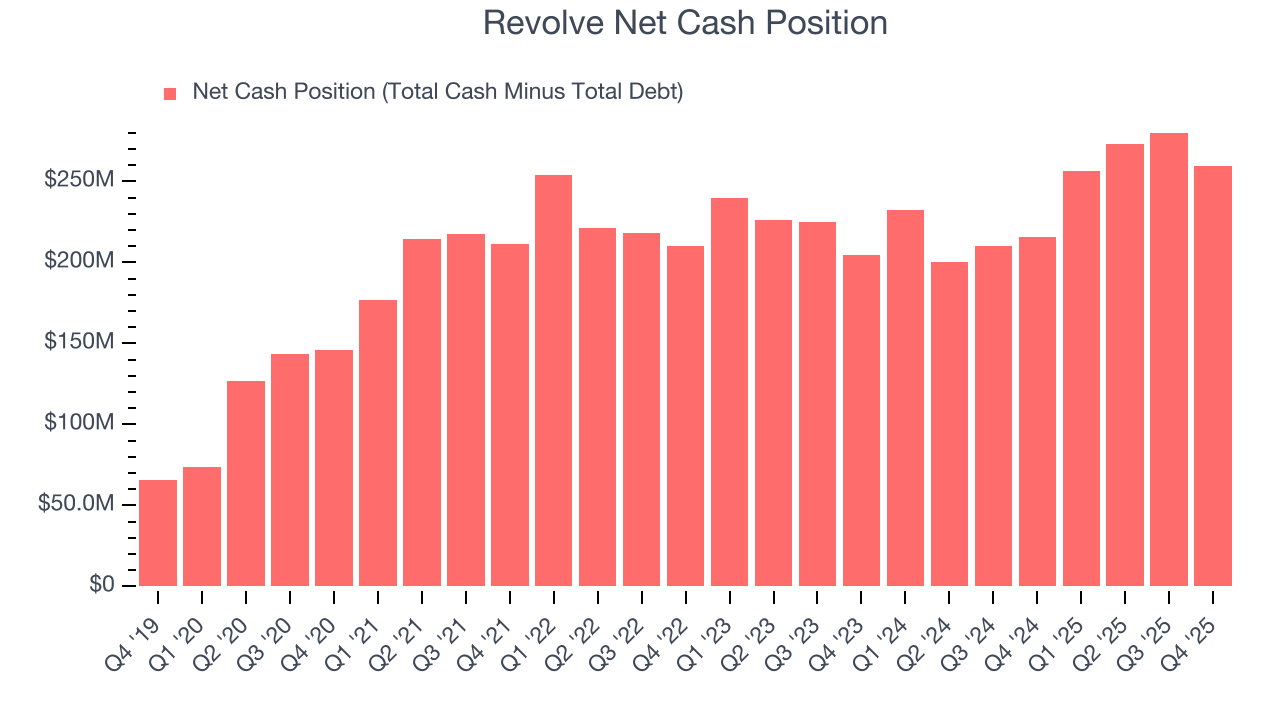

One of the best ways to mitigate bankruptcy risk is to hold more cash than debt.

Revolve is a profitable, well-capitalized company with $292.3 million of cash and $32.46 million of debt on its balance sheet. This $259.8 million net cash position is 15% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

13. Key Takeaways from Revolve’s Q4 Results

We were impressed by how significantly Revolve blew past analysts’ EBITDA expectations this quarter. We were also glad its revenue outperformed Wall Street’s estimates. Zooming out, we think this quarter featured some important positives. The stock traded up 1.5% to $26.29 immediately after reporting.

14. Is Now The Time To Buy Revolve?

Updated: March 13, 2026 at 10:26 PM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Revolve.

We cheer for all companies serving everyday consumers, but in the case of Revolve, we’ll be cheering from the sidelines. For starters, its revenue growth was weak over the last three years. While its sturdy EBITDA margins show it has disciplined cost controls, the downside is its disappointing EPS growth over the last three years shows it’s failed to produce meaningful profits for shareholders. On top of that, its sales and marketing efficiency is subpar.

Revolve’s EV/EBITDA ratio based on the next 12 months is 14.3x. At this valuation, there’s a lot of good news priced in - we think other companies feature superior fundamentals at the moment.

Wall Street analysts have a consensus one-year price target of $31.21 on the company (compared to the current share price of $22.92).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.