Tutor Perini (TPC)

We’re not sold on Tutor Perini. Its low returns on capital and plummeting sales suggest it struggles to generate demand and profits, a red flag.― StockStory Analyst Team

1. News

2. Summary

Why Tutor Perini Is Not Exciting

Known for constructing the Philadelphia Eagles’ Stadium, Tutor Perini (NYSE:TPC) is a civil and building construction company offering diversified general contracting and design-build services.

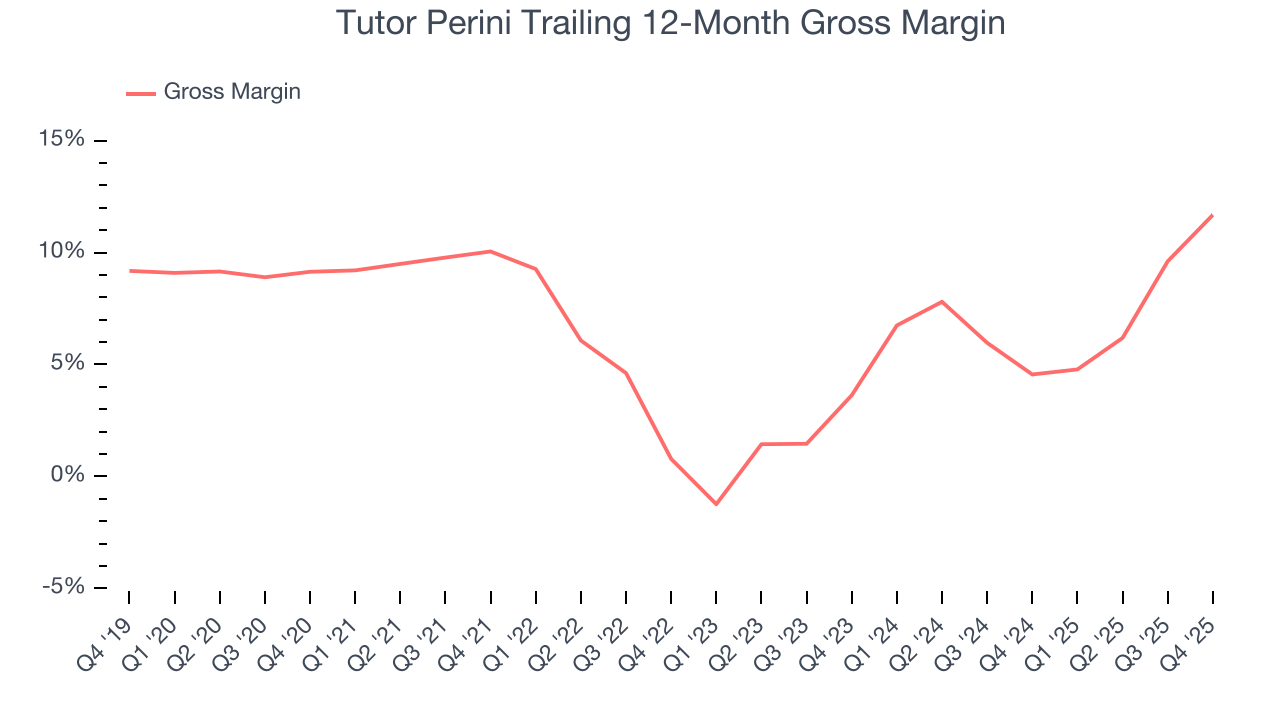

- Competitive supply chain dynamics and steep production costs are reflected in its low gross margin of 6.7%

- Low returns on capital reflect management’s struggle to allocate funds effectively

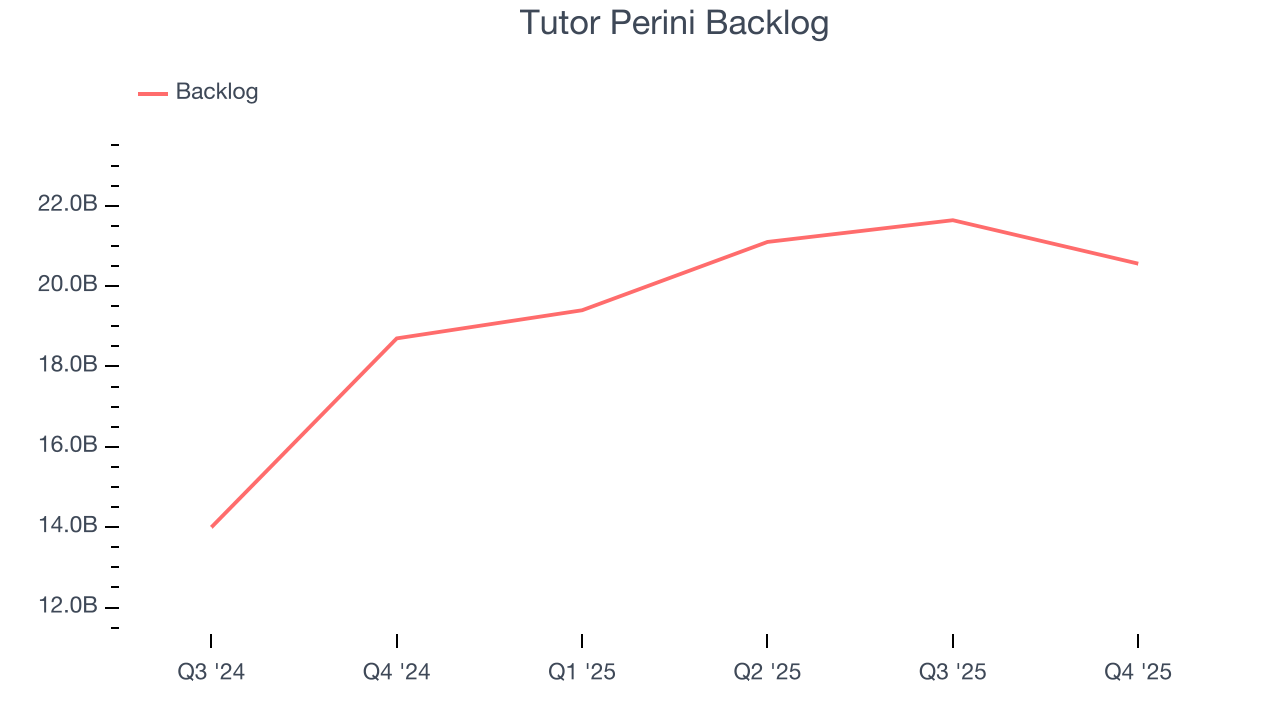

- On the plus side, its backlog has averaged 32.3% growth over the past two years, showing it has a pipeline of unfulfilled orders that will support revenue in the future

Tutor Perini is in the penalty box. We see more favorable opportunities in the market.

Why There Are Better Opportunities Than Tutor Perini

Tutor Perini is trading at $68.57 per share, or 14x forward P/E. Tutor Perini’s multiple may seem like a great deal among industrials peers, but we think there are valid reasons why it’s this cheap.

We’d rather pay up for companies with elite fundamentals than get a bargain on weak ones. Cheap stocks can be value traps, and as their performance deteriorates, they will stay cheap or get even cheaper.

3. Tutor Perini (TPC) Research Report: Q4 CY2025 Update

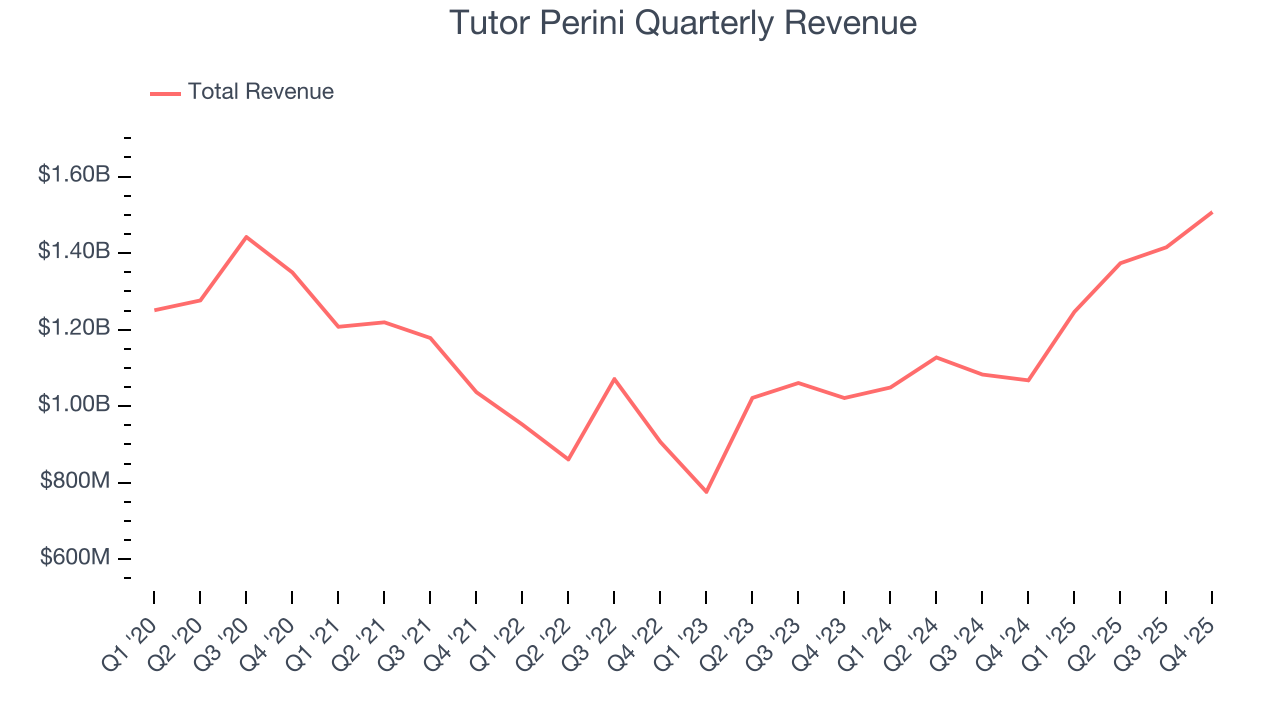

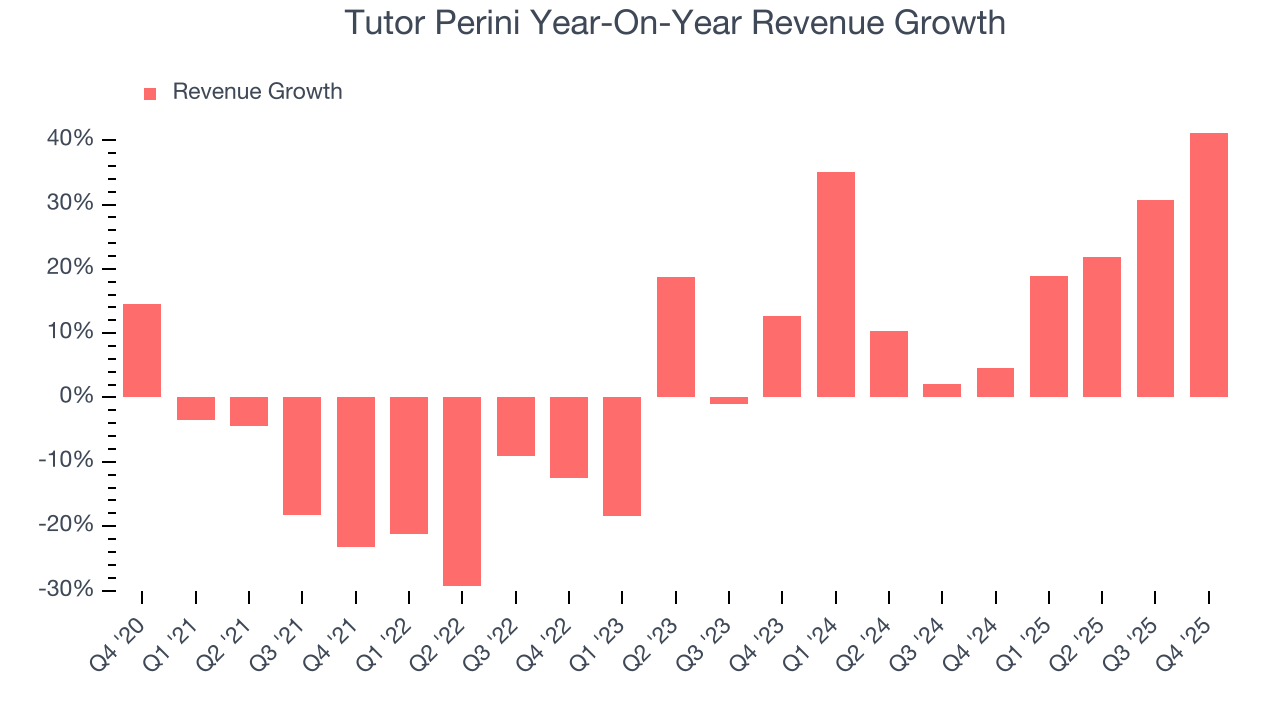

General contracting company Tutor Perini (NYSE:TPC) announced better-than-expected revenue in Q4 CY2025, with sales up 41.2% year on year to $1.51 billion. Its non-GAAP profit of $1.07 per share was 16.3% above analysts’ consensus estimates.

Tutor Perini (TPC) Q4 CY2025 Highlights:

- Revenue: $1.51 billion vs analyst estimates of $1.35 billion (41.2% year-on-year growth, 11.4% beat)

- Adjusted EPS: $1.07 vs analyst estimates of $0.92 (16.3% beat)

- Adjusted EPS guidance for the upcoming financial year 2026 is $5.10 at the midpoint, beating analyst estimates by 5.8%

- Operating Margin: 3.3%, up from -8% in the same quarter last year

- Free Cash Flow Margin: 5%, down from 30% in the same quarter last year

- Backlog: $20.56 billion at quarter end, up 9.9% year on year

- Market Capitalization: $4.54 billion

Company Overview

Known for constructing the Philadelphia Eagles’ Stadium, Tutor Perini (NYSE:TPC) is a civil and building construction company offering diversified general contracting and design-build services.

Tutor Perini was founded in 1894 by Bonfiglio Perini under the name Perini Corporation, initially focusing on stonework and excavation. The company has since evolved into a general construction firm, handling large-scale civil, building, and specialty construction projects across various sectors, including healthcare, education, transportation, and defense.

Today, Tutor Perini offers a range of construction services, including complex civil engineering projects like highway and bridge construction, railway and transit systems, and airport infrastructures. It also handles large building contracts for high-rises, hospitals, universities, and casinos.

The company’s revenue comes primarily from contracts won through bidding and negotiated procurements, fostering long-term relationships with public and private sector clients. Revenue is primarily project-based, with some recurring aspects through maintenance and management contracts within the civil and specialty sectors. The company’s ability to secure large-scale projects regularly contributes to a large project pipeline, which supports sustained financial performance.

4. Construction and Maintenance Services

Construction and maintenance services companies not only boast technical know-how in specialized areas but also may hold special licenses and permits. Those who work in more regulated areas can enjoy more predictable revenue streams - for example, fire escapes need to be inspected every five years. More recently, services to address energy efficiency and labor availability are also creating incremental demand. But like the broader industrials sector, construction and maintenance services companies are at the whim of economic cycles as external factors like interest rates can greatly impact the new construction that drives incremental demand for these companies’ offerings.

Competitors in the construction services industry include Fluor Corporation (NYSE:FLR), AECOM (NYSE:ACM), and Jacobs Engineering (NYSE:J)

5. Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Unfortunately, Tutor Perini struggled to consistently increase demand as its $5.54 billion of sales for the trailing 12 months was close to its revenue five years ago. This wasn’t a great result, but there are still things to like about Tutor Perini.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Tutor Perini’s annualized revenue growth of 19.5% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

Tutor Perini also reports its backlog, or the value of its outstanding orders that have not yet been executed or delivered. Tutor Perini’s backlog reached $20.56 billion in the latest quarter and averaged 32.3% year-on-year growth over the last two years. Because this number is better than its revenue growth, we can see the company accumulated more orders than it could fulfill and deferred revenue to the future. This could imply elevated demand for Tutor Perini’s products and services but raises concerns about capacity constraints.

This quarter, Tutor Perini reported magnificent year-on-year revenue growth of 41.2%, and its $1.51 billion of revenue beat Wall Street’s estimates by 11.4%.

Looking ahead, sell-side analysts expect revenue to grow 11.3% over the next 12 months, a deceleration versus the last two years. Still, this projection is healthy and suggests the market is baking in success for its products and services.

6. Gross Margin & Pricing Power

Tutor Perini has bad unit economics for an industrials business, signaling it operates in a competitive market. As you can see below, it averaged a 6.7% gross margin over the last five years. That means Tutor Perini paid its suppliers a lot of money ($93.32 for every $100 in revenue) to run its business.

In Q4, Tutor Perini produced a 9.8% gross profit margin , marking a 10.7 percentage point increase from -0.9% in the same quarter last year. Tutor Perini’s full-year margin has also been trending up over the past 12 months, increasing by 7.1 percentage points. If this move continues, it could suggest a less competitive environment where the company has better pricing power and leverage from its growing sales on the fixed portion of its cost of goods sold (such as manufacturing expenses).

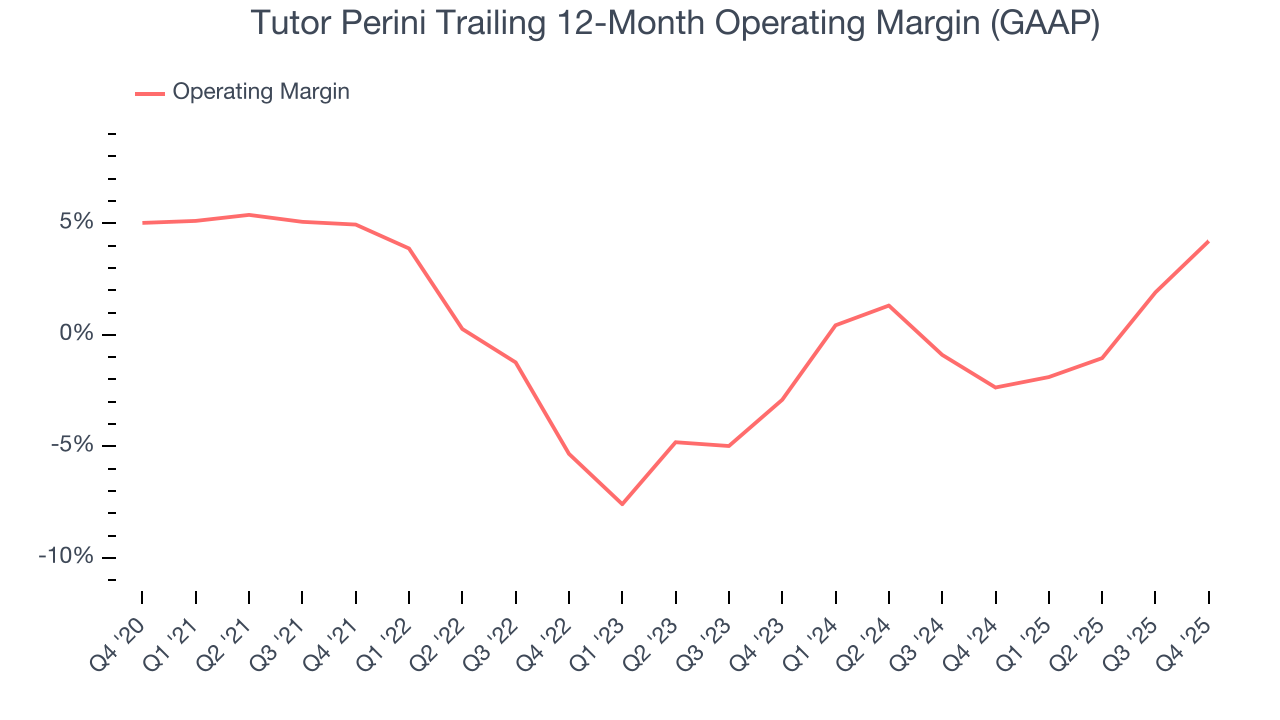

7. Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Tutor Perini’s operating margin has been trending up over the last 12 months, leading to break even profits over the last five years. However, its large expense base and inefficient cost structure mean it still sports inadequate profitability for an industrials business. This result isn’t too surprising given its low gross margin as a starting point.

Looking at the trend in its profitability, Tutor Perini’s operating margin might fluctuated slightly but has generally stayed the same over the last five years, meaning it will take a fundamental shift in the business model to change.

This quarter, Tutor Perini generated an operating margin profit margin of 3.3%, up 11.4 percentage points year on year. The increase was solid, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

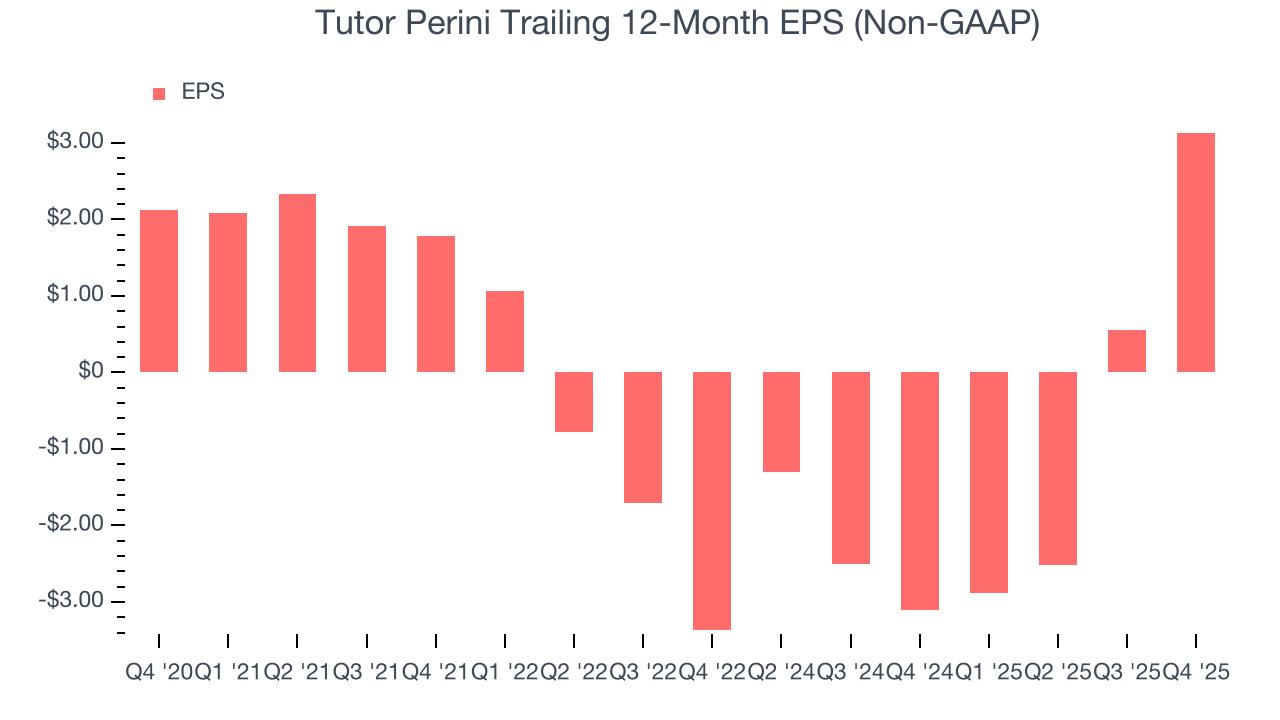

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Tutor Perini’s EPS grew at a decent 8.1% compounded annual growth rate over the last five years, higher than its flat revenue. However, we take this with a grain of salt because its operating margin didn’t improve and it didn’t repurchase its shares, meaning the delta came from reduced interest expenses or taxes.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Tutor Perini, its two-year annual EPS growth of 83.6% was higher than its five-year trend. This acceleration made it one of the faster-growing industrials companies in recent history.

In Q4, Tutor Perini reported adjusted EPS of $1.07, up from negative $1.51 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Tutor Perini’s full-year EPS of $3.13 to grow 53.4%.

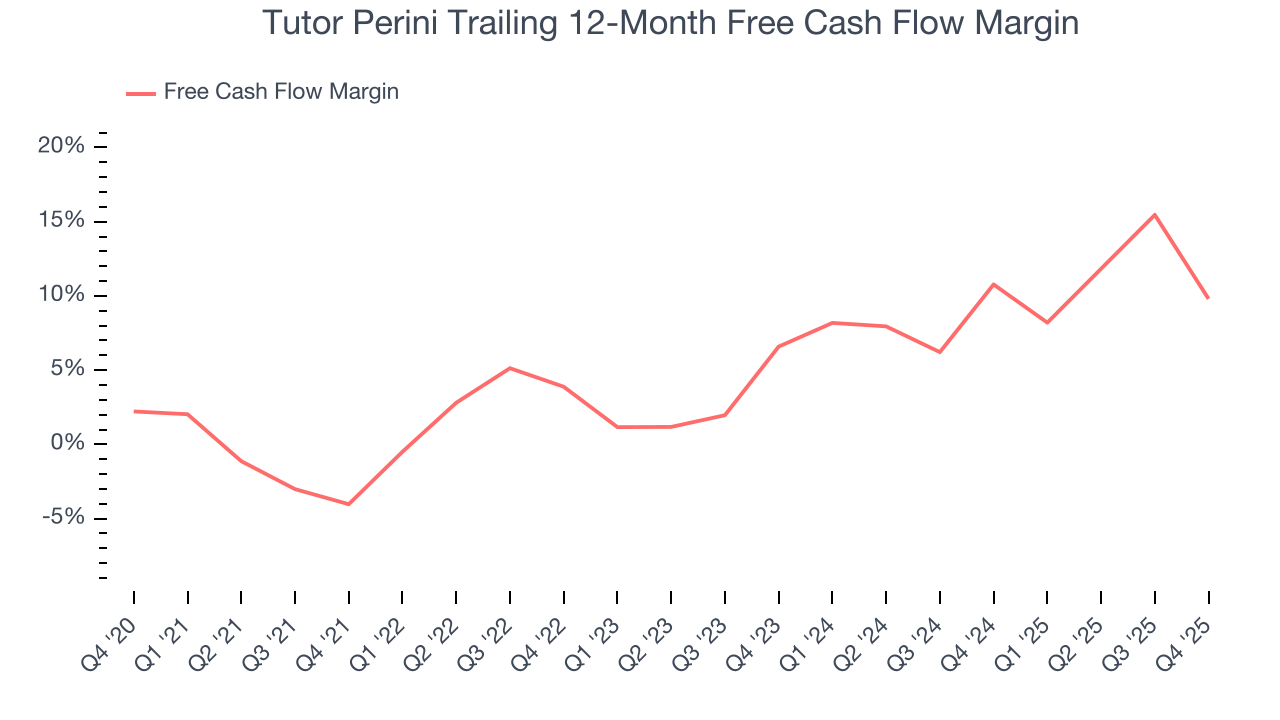

9. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Tutor Perini has shown mediocre cash profitability over the last five years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 5.5%, subpar for an industrials business.

Taking a step back, an encouraging sign is that Tutor Perini’s margin expanded by 13.8 percentage points during that time. The company’s improvement shows it’s heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose while its operating profitability was flat.

Tutor Perini’s free cash flow clocked in at $74.96 million in Q4, equivalent to a 5% margin. The company’s cash profitability regressed as it was 25 percentage points lower than in the same quarter last year, but we wouldn’t read too much into it because capital expenditures can be seasonal and companies often stockpile inventory in anticipation of higher demand, causing quarter-to-quarter swings. Long-term trends trump fluctuations.

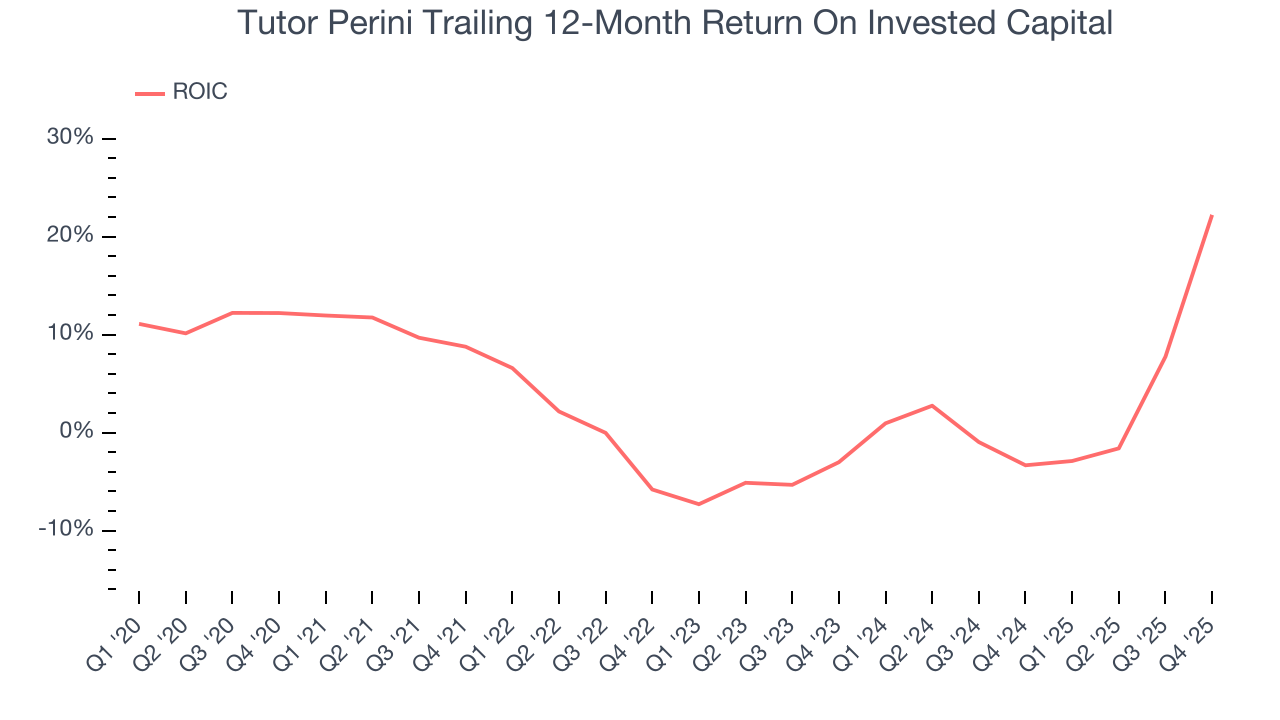

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Tutor Perini historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 3.8%, lower than the typical cost of capital (how much it costs to raise money) for industrials companies.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Fortunately, Tutor Perini’s has increased over the last few years. This is a good sign, and if its returns keep rising, there’s a chance it could evolve into an investable business.

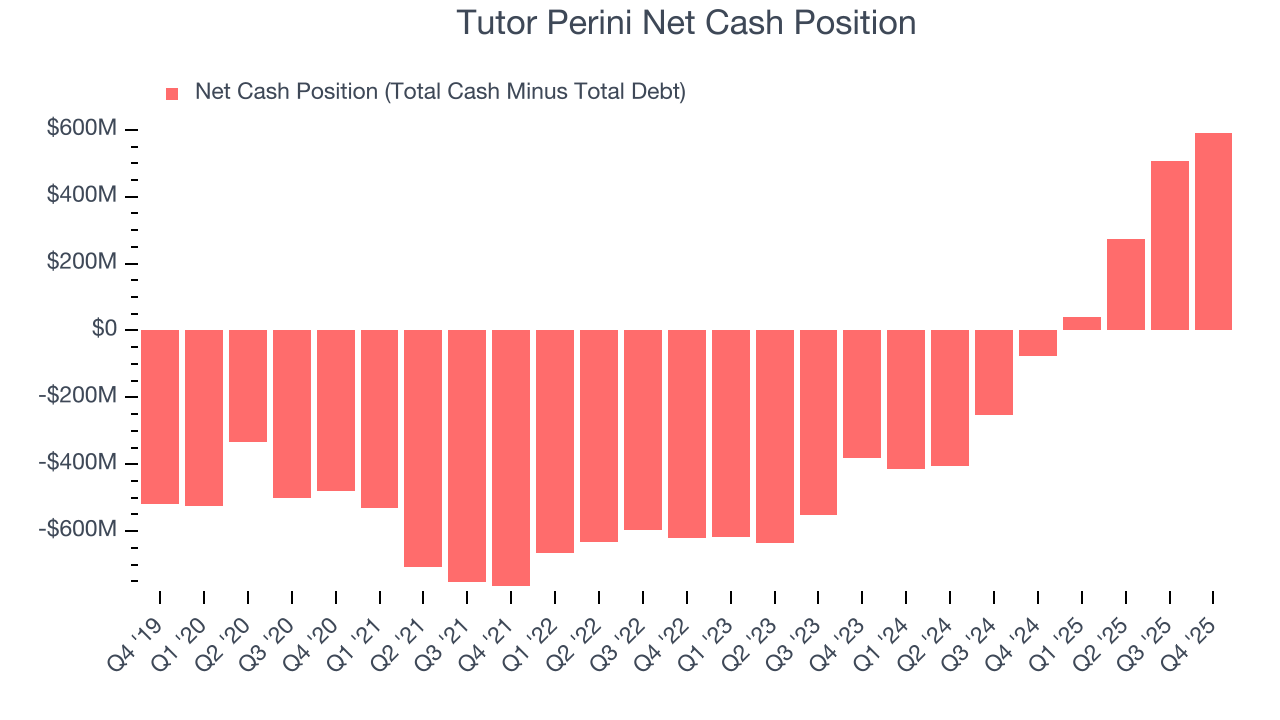

11. Balance Sheet Assessment

Companies with more cash than debt have lower bankruptcy risk.

Tutor Perini is a profitable, well-capitalized company with $999.2 million of cash and $407.4 million of debt on its balance sheet. This $591.8 million net cash position is 14.9% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

12. Key Takeaways from Tutor Perini’s Q4 Results

We were impressed by how significantly Tutor Perini blew past analysts’ revenue expectations this quarter. We were also glad its full-year EPS guidance trumped Wall Street’s estimates. Zooming out, we think this quarter featured some important positives. The stock remained flat at $89.96 immediately after reporting.

13. Is Now The Time To Buy Tutor Perini?

Updated: March 15, 2026 at 11:55 PM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Tutor Perini.

When it comes to Tutor Perini’s business quality, there are some positives, but it ultimately falls short. Although its revenue growth was weak over the last five years, its growth over the next 12 months is expected to be higher. And while Tutor Perini’s relatively low ROIC suggests management has struggled to find compelling investment opportunities, its backlog growth has been marvelous.

Tutor Perini’s P/E ratio based on the next 12 months is 14x. This valuation is reasonable, but the company’s shakier fundamentals present too much downside risk. We're fairly confident there are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $109.50 on the company (compared to the current share price of $68.57).