Acadia Healthcare (ACHC)

We wouldn’t buy Acadia Healthcare. Its weak sales growth and low returns on capital show it struggled to generate demand and profits.― StockStory Analyst Team

1. News

2. Summary

Why We Think Acadia Healthcare Will Underperform

With a network of over 250 facilities serving patients in 38 states and Puerto Rico, Acadia Healthcare (NASDAQ:ACHC) operates facilities providing mental health and substance use disorder treatment services across the United States.

- Incremental sales over the last five years were much less profitable as its earnings per share fell by 6.1% annually while its revenue grew

- Low returns on capital reflect management’s struggle to allocate funds effectively, and its falling returns suggest its earlier profit pools are drying up

- Long-term business health is up for debate as its cash burn has increased over the last five years

Acadia Healthcare falls short of our quality standards. More profitable opportunities exist elsewhere.

Why There Are Better Opportunities Than Acadia Healthcare

Acadia Healthcare’s stock price of $24.02 implies a valuation ratio of 15.3x forward P/E. Acadia Healthcare’s valuation may seem like a bargain, especially when stacked up against other healthcare companies. We remind you that you often get what you pay for, though.

Cheap stocks can look like great bargains at first glance, but you often get what you pay for. These mediocre businesses often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. Acadia Healthcare (ACHC) Research Report: Q4 CY2025 Update

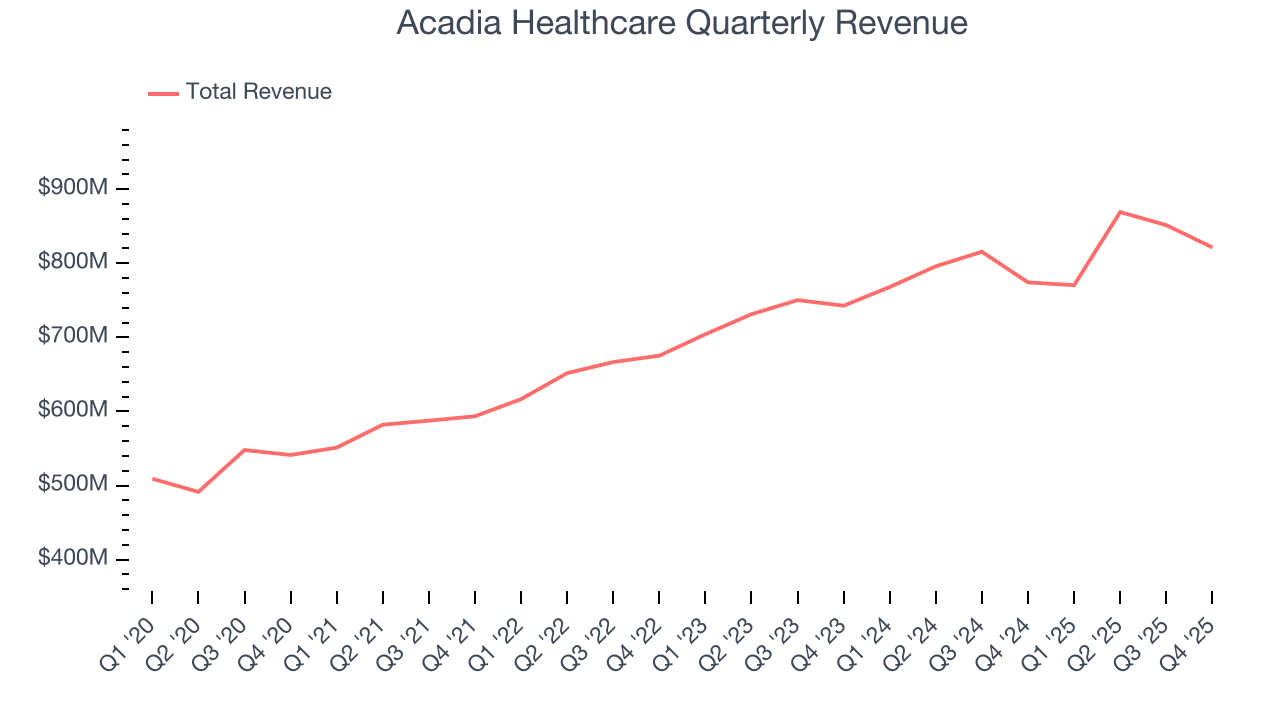

Behavioral health company Acadia Healthcare (NASDAQ:ACHC) announced better-than-expected revenue in Q4 CY2025, with sales up 6.1% year on year to $821.5 million. Guidance for next quarter’s revenue was optimistic at $825 million at the midpoint, 2.6% above analysts’ estimates. Its non-GAAP profit of $0.07 per share was significantly above analysts’ consensus estimates.

Acadia Healthcare (ACHC) Q4 CY2025 Highlights:

- Revenue: $821.5 million vs analyst estimates of $799.1 million (6.1% year-on-year growth, 2.8% beat)

- Adjusted EPS: $0.07 vs analyst estimates of $0.01 (significant beat)

- Adjusted EBITDA: $152 million vs analyst estimates of $94.7 million (18.5% margin, 60.5% beat)

- Revenue Guidance for Q1 CY2026 is $825 million at the midpoint, above analyst estimates of $803.8 million

- Adjusted EPS guidance for the upcoming financial year 2026 is $1.43 at the midpoint, missing analyst estimates by 16.6%

- EBITDA guidance for the upcoming financial year 2026 is $592.5 million at the midpoint, below analyst estimates of $598.6 million

- Operating Margin: -142%, down from 8.8% in the same quarter last year

- Free Cash Flow was -$179.5 million compared to -$86.79 million in the same quarter last year

- Sales Volumes rose 9% year on year (3% in the same quarter last year)

- Market Capitalization: $1.58 billion

Company Overview

With a network of over 250 facilities serving patients in 38 states and Puerto Rico, Acadia Healthcare (NASDAQ:ACHC) operates facilities providing mental health and substance use disorder treatment services across the United States.

Acadia's treatment facilities are organized into four main categories, each addressing different levels of patient needs. Acute inpatient psychiatric facilities provide 24-hour crisis stabilization for patients who may be a danger to themselves or others, with psychiatrists, nurses, and therapists delivering intensive medical and behavioral interventions. Specialty treatment facilities focus on addiction recovery and eating disorders, offering various levels of care from detoxification to outpatient services.

The company's Comprehensive Treatment Centers (CTCs) specialize in medication-assisted treatment for opioid addiction in outpatient settings, combining behavioral therapy with medications that normalize brain chemistry. Residential treatment centers provide longer-term care for children and adolescents with severe psychiatric disorders and trauma histories, often in secure environments with educational programs.

A patient experiencing severe depression might enter Acadia's acute care for immediate stabilization, then transition to a specialty facility for ongoing therapy. Similarly, someone struggling with opioid addiction might receive medication and counseling at a CTC, with treatment potentially lasting a year or longer.

Acadia generates revenue through multiple payment sources, including state Medicaid programs, commercial insurance, Medicare, and direct patient payments. The company pursues growth through five main pathways: expanding existing facilities, forming joint venture partnerships (often with healthcare systems), building new facilities, acquiring other behavioral healthcare providers, and extending its continuum of care offerings.

The behavioral healthcare industry faces significant regulatory oversight, with facilities maintaining accreditations from organizations like The Joint Commission and complying with various healthcare laws including HIPAA privacy regulations and physician self-referral restrictions.

4. Hospital Chains

Hospital chains operate scale-driven businesses that rely on patient volumes, efficient operations, and favorable payer contracts to drive revenue and profitability. These organizations benefit from the essential nature of their services, which ensures consistent demand, particularly as populations age and chronic diseases become more prevalent. However, profitability can be pressured by rising labor costs, regulatory requirements, and the challenges of balancing care quality with cost efficiency. Dependence on government and private insurance reimbursements also introduces financial uncertainty. Looking ahead, hospital chains stand to benefit from tailwinds such as increasing healthcare utilization driven by an aging population that generally has higher incidents of disease. AI can also be a tailwind in areas such as predictive analytics for more personalized treatment and efficiency (intake, staffing, resourcing allocation). However, the sector faces potential headwinds such as labor shortages that could push up wages as well as substantial investments needs for digital infrastructure to support telehealth and electronic health records. Regulatory scrutiny, and reimbursement cuts are also looming topics that could further strain margins.

Acadia Healthcare's primary competitor is Universal Health Services (NYSE:UHS), which operates behavioral health facilities alongside its acute care hospitals. Other competitors include private behavioral health providers and hospital systems with psychiatric units.

5. Economies of Scale

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With $3.31 billion in revenue over the past 12 months, Acadia Healthcare has decent scale. This is important as it gives the company more leverage in a heavily regulated, competitive environment that is complex and resource-intensive.

6. Revenue Growth

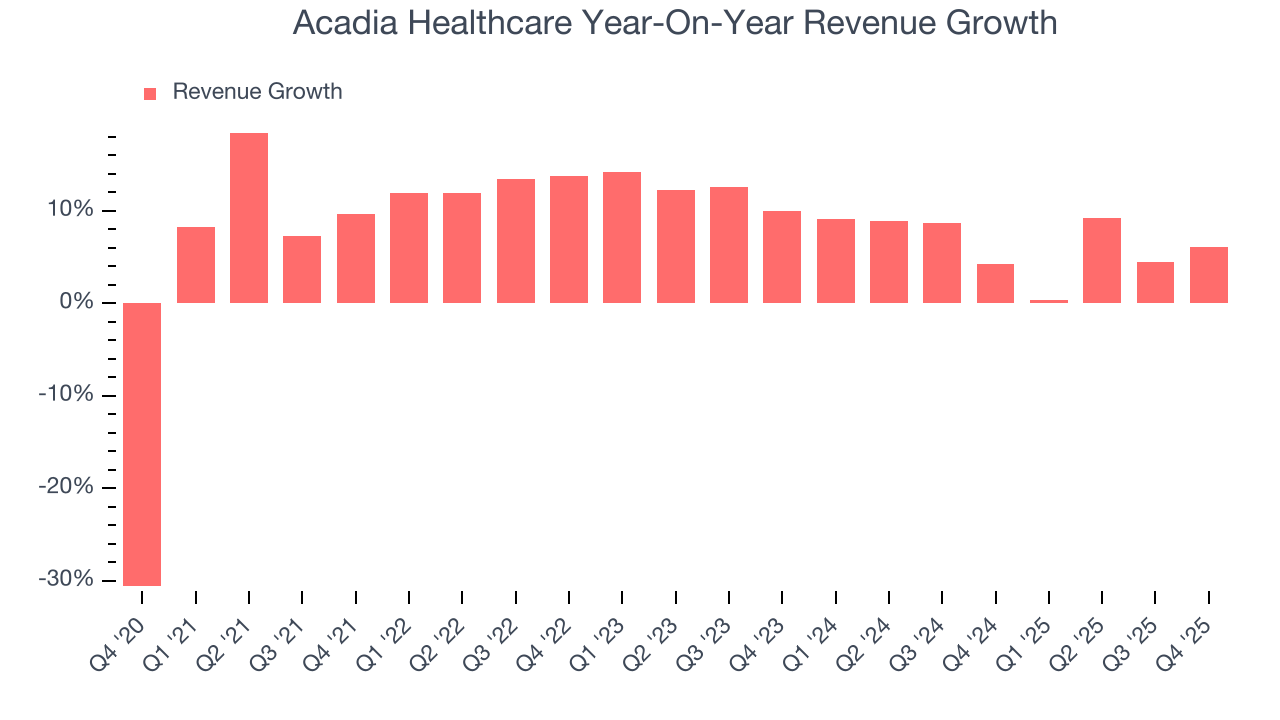

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Luckily, Acadia Healthcare’s sales grew at a decent 9.7% compounded annual growth rate over the last five years. Its growth was slightly above the average healthcare company and shows its offerings resonate with customers.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Acadia Healthcare’s recent performance shows its demand has slowed as its annualized revenue growth of 6.4% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

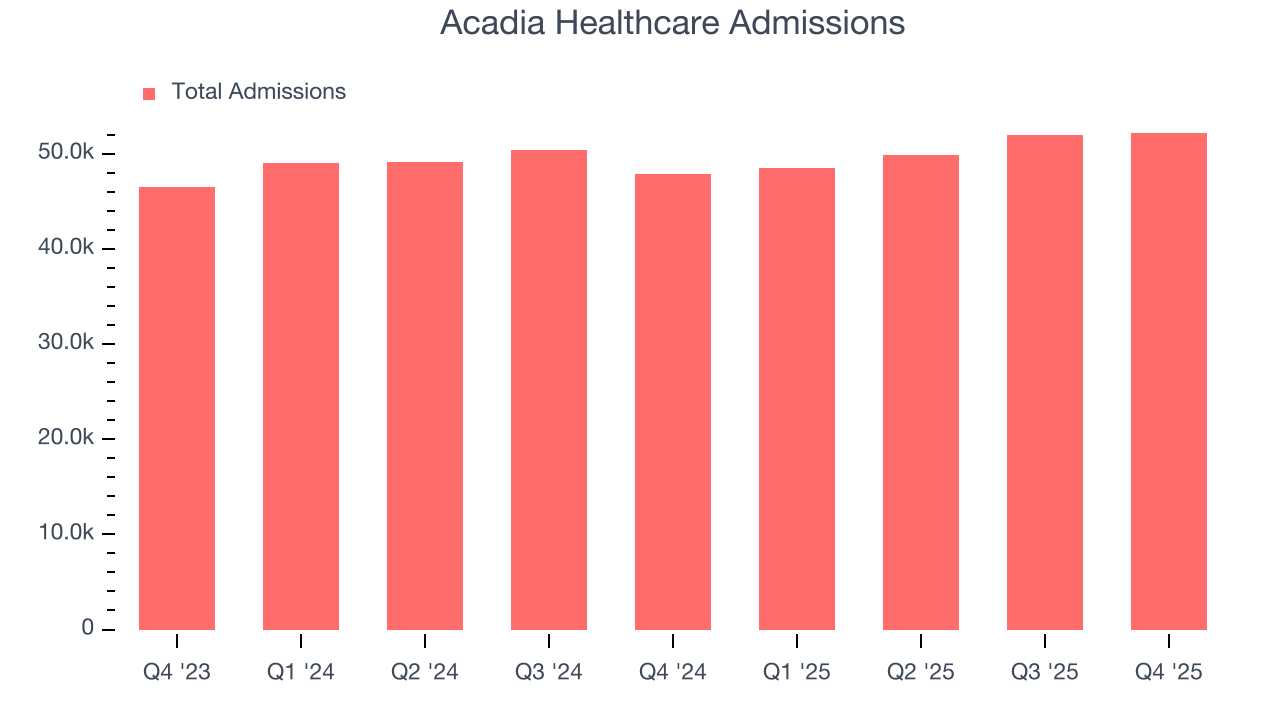

We can dig further into the company’s revenue dynamics by analyzing its number of admissions, which reached 52,170 in the latest quarter. Over the last two years, Acadia Healthcare’s admissions averaged 3.1% year-on-year growth. Because this number is lower than its revenue growth, we can see the company benefited from price increases.

This quarter, Acadia Healthcare reported year-on-year revenue growth of 6.1%, and its $821.5 million of revenue exceeded Wall Street’s estimates by 2.8%. Company management is currently guiding for a 7.1% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 2.5% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and suggests its products and services will see some demand headwinds.

7. Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D.

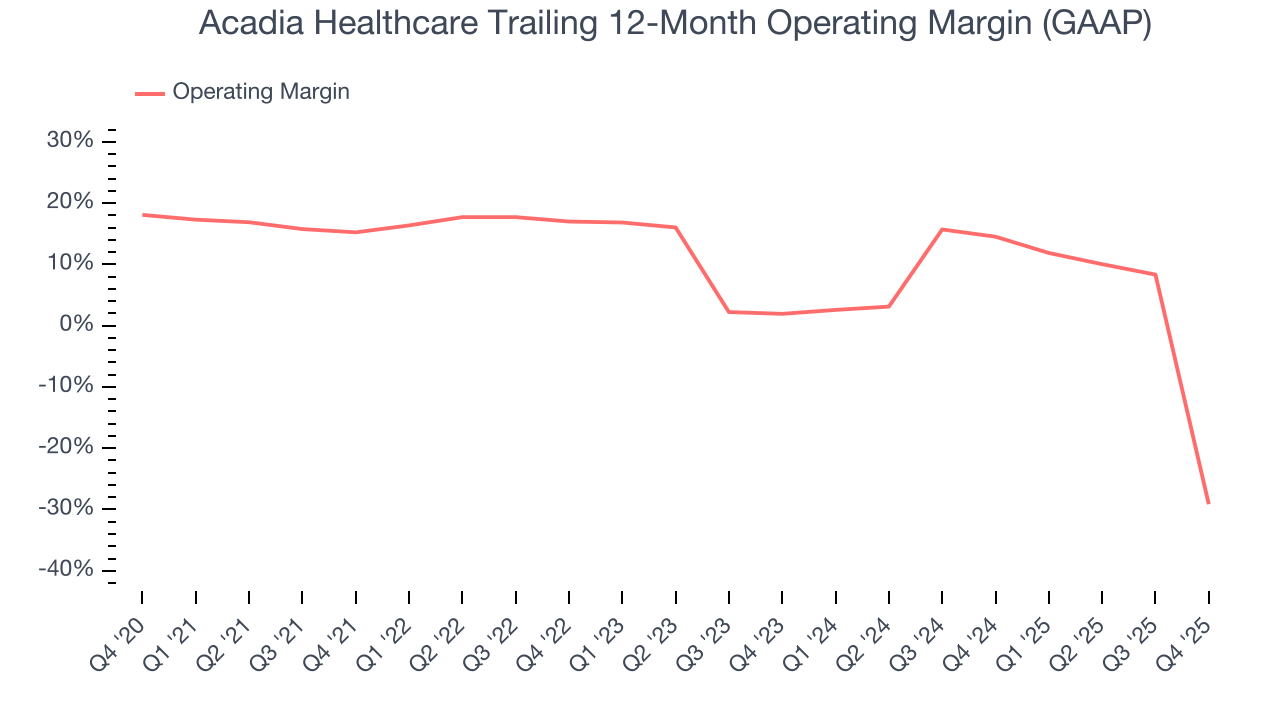

Acadia Healthcare was profitable over the last five years but held back by its large cost base. Its average operating margin of 2.4% was weak for a healthcare business.

Analyzing the trend in its profitability, Acadia Healthcare’s operating margin decreased by 44.4 percentage points over the last five years. The company’s two-year trajectory also shows it failed to get its profitability back to the peak as its margin fell by 31.1 percentage points. This performance was poor no matter how you look at it - it shows its expenses were rising and it couldn’t pass those costs onto its customers.

In Q4, Acadia Healthcare generated an operating margin profit margin of negative 142%, down 151.1 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

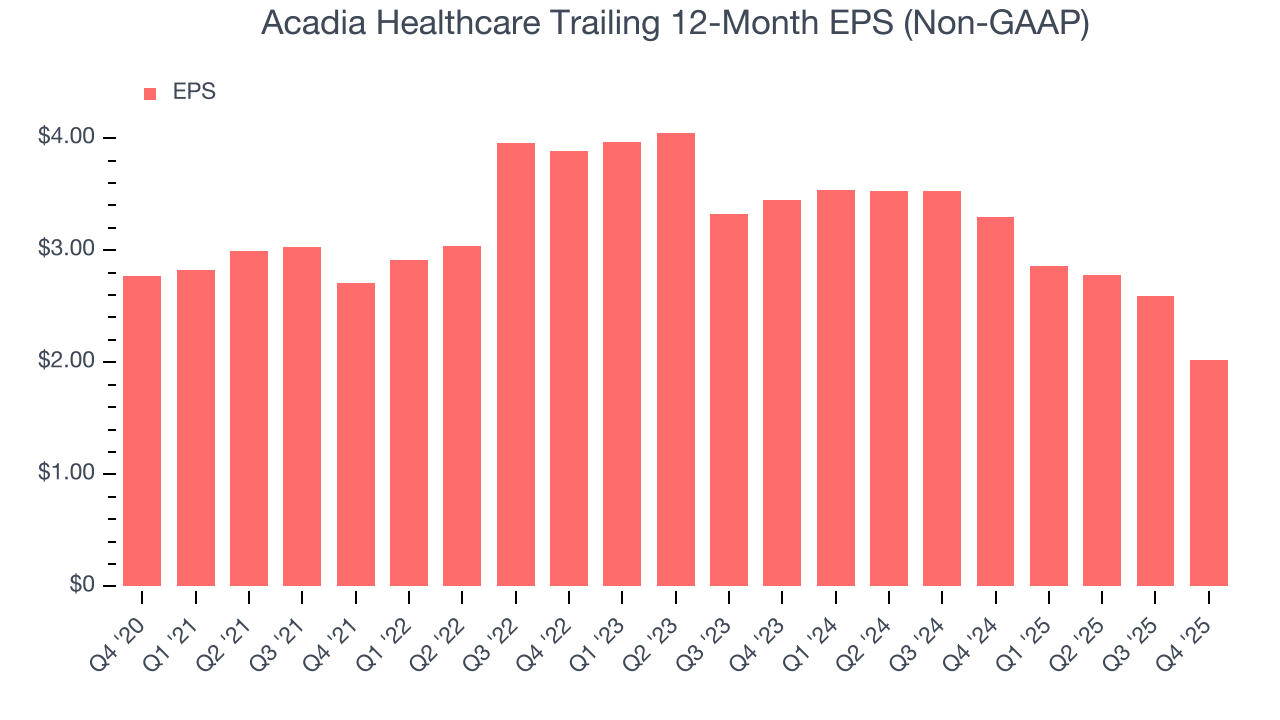

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Acadia Healthcare, its EPS declined by 6.1% annually over the last five years while its revenue grew by 9.7%. This tells us the company became less profitable on a per-share basis as it expanded.

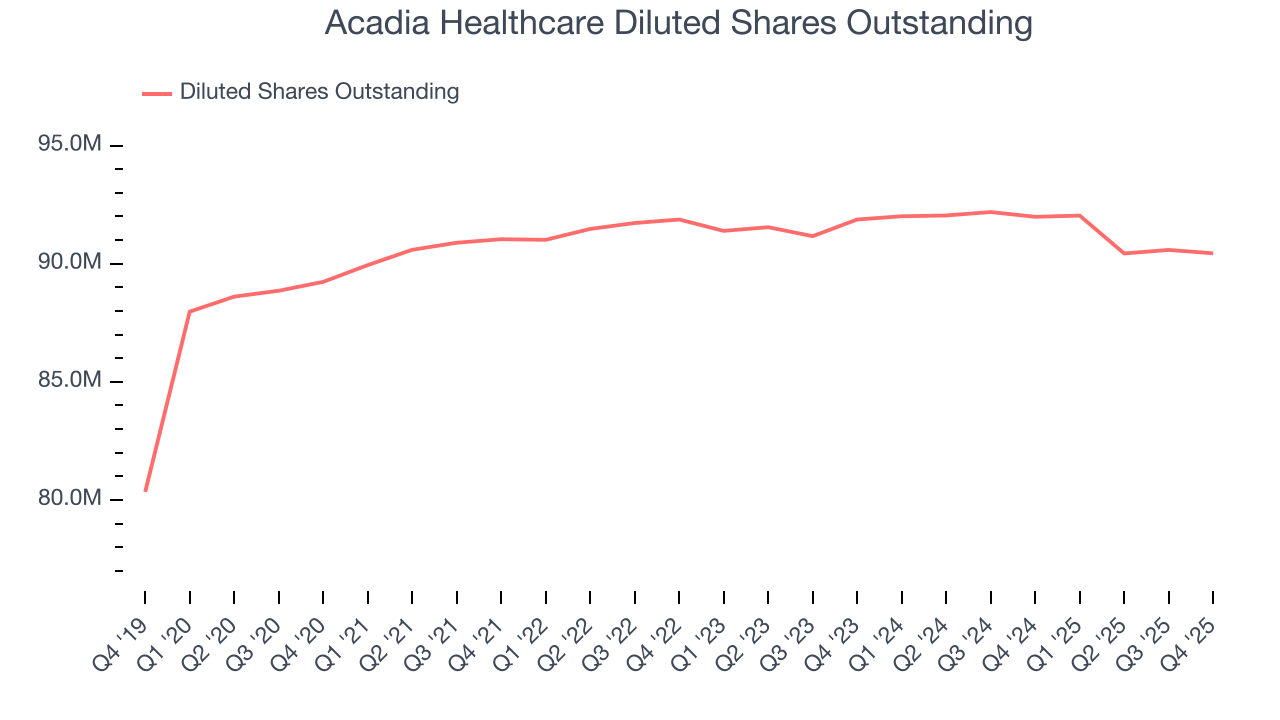

We can take a deeper look into Acadia Healthcare’s earnings to better understand the drivers of its performance. As we mentioned earlier, Acadia Healthcare’s operating margin declined by 44.4 percentage points over the last five years. Its share count also grew by 1.4%, meaning the company not only became less efficient with its operating expenses but also diluted its shareholders.

In Q4, Acadia Healthcare reported adjusted EPS of $0.07, down from $0.64 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Acadia Healthcare’s full-year EPS of $2.02 to shrink by 14.6%.

9. Cash Is King

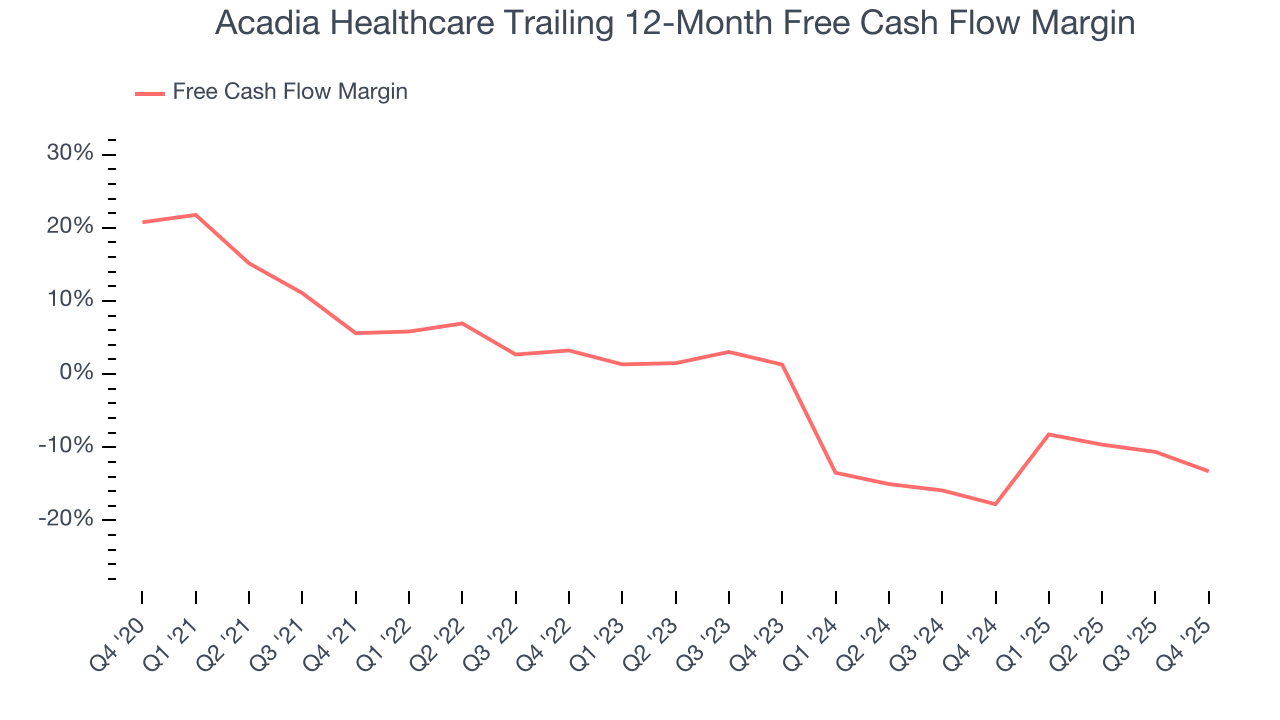

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Acadia Healthcare’s demanding reinvestments have consumed many resources over the last five years, contributing to an average free cash flow margin of negative 5.2%. This means it lit $5.23 of cash on fire for every $100 in revenue.

Taking a step back, we can see that Acadia Healthcare’s margin dropped by 18.9 percentage points during that time. It may have ticked higher more recently, but shareholders are likely hoping for its margin to at least revert to its historical level. Almost any movement in the wrong direction is undesirable because it’s already burning cash. If the longer-term trend returns, it could signal it’s in the middle of a big investment cycle.

Acadia Healthcare burned through $179.5 million of cash in Q4, equivalent to a negative 21.8% margin. The company’s cash burn increased from $86.79 million of lost cash in the same quarter last year.

10. Return on Invested Capital (ROIC)

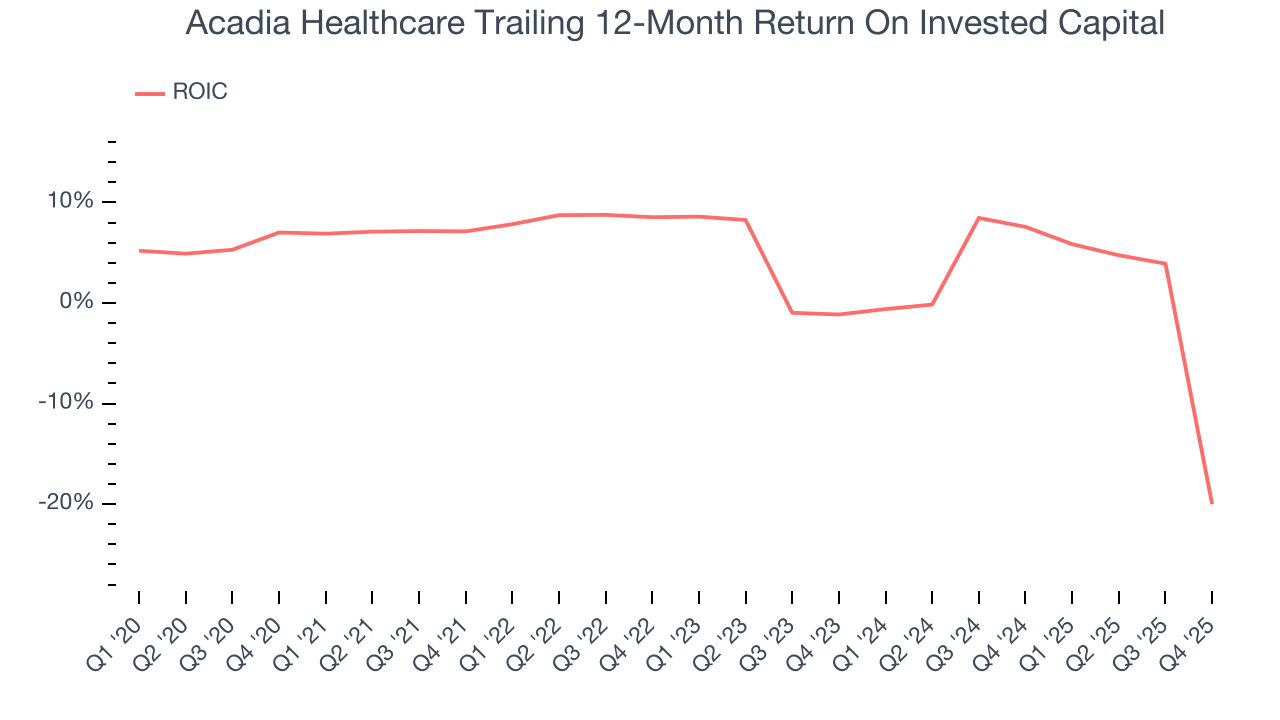

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Acadia Healthcare historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 0.4%, lower than the typical cost of capital (how much it costs to raise money) for healthcare companies.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, Acadia Healthcare’s ROIC has decreased significantly over the last few years. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

11. Balance Sheet Assessment

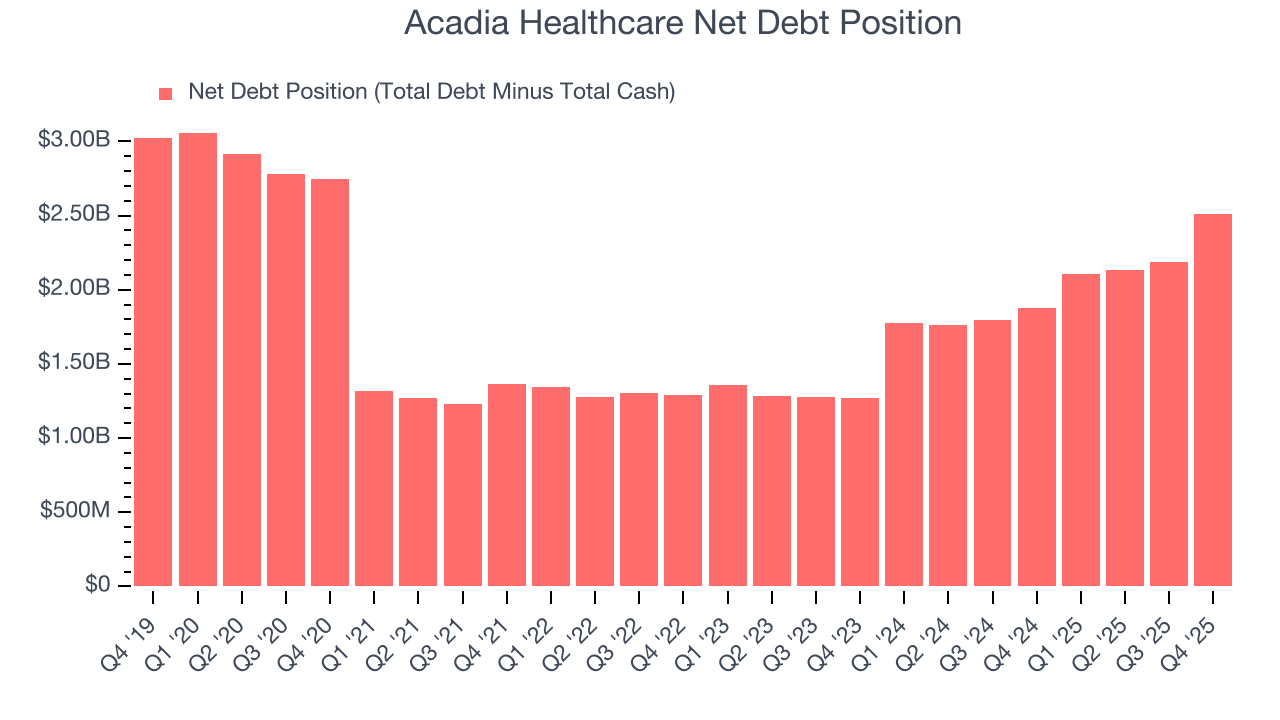

Acadia Healthcare reported $133.2 million of cash and $2.64 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $661.1 million of EBITDA over the last 12 months, we view Acadia Healthcare’s 3.8× net-debt-to-EBITDA ratio as safe. We also see its $63.01 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Acadia Healthcare’s Q4 Results

It was good to see Acadia Healthcare beat analysts’ EPS expectations this quarter. We were also glad its EBITDA guidance for next quarter exceeded Wall Street’s estimates. On the other hand, its full-year EPS guidance missed and its full-year EBITDA guidance fell slightly short of Wall Street’s estimates. Overall, this print was mixed but still had some key positives. The stock traded up 10.8% to $19.02 immediately after reporting.

13. Is Now The Time To Buy Acadia Healthcare?

Updated: March 17, 2026 at 11:50 PM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Acadia Healthcare.

We see the value of companies making people healthier, but in the case of Acadia Healthcare, we’re out. Although its revenue growth was decent over the last five years, it’s expected to deteriorate over the next 12 months and its declining EPS over the last five years makes it a less attractive asset to the public markets. And while the company’s operating margins are in line with the overall healthcare sector, the downside is its cash profitability fell over the last five years.

Acadia Healthcare’s P/E ratio based on the next 12 months is 15.3x. This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think there are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $22.71 on the company (compared to the current share price of $24.02), implying they don’t see much short-term potential in Acadia Healthcare.