Adobe (ADBE)

We’re cautious of Adobe. Its growth has been lacking and its cash conversion is projected to decline, a situation we’d avoid.― StockStory Analyst Team

1. News

2. Summary

Why Adobe Is Not Exciting

Originally named after Adobe Creek that ran behind co-founder John Warnock's house, Adobe (NASDAQ:ADBE) develops software products used for digital content creation, document management, and marketing solutions across desktop, mobile, and cloud platforms.

- Estimated sales growth of 9.1% for the next 12 months implies demand will slow from its two-year trend

- Operating margin expanded by 5.1 percentage points over the last year as it scaled and became more efficient

- On the plus side, its prominent and differentiated software leads to a best-in-class gross margin of 89.1%

Adobe falls short of our expectations. There are more promising prospects in the market.

Why There Are Better Opportunities Than Adobe

Adobe’s stock price of $345.12 implies a valuation ratio of 5.7x forward price-to-sales. Adobe’s multiple may seem like a great deal among software peers, but we think there are valid reasons why it’s this cheap.

Our advice is to pay up for elite businesses whose advantages are tailwinds to earnings growth. Don’t get sucked into lower-quality businesses just because they seem like bargains. These mediocre businesses often never achieve a higher multiple as hoped, a phenomenon known as a “value trap”.

3. Adobe (ADBE) Research Report: Q4 CY2025 Update

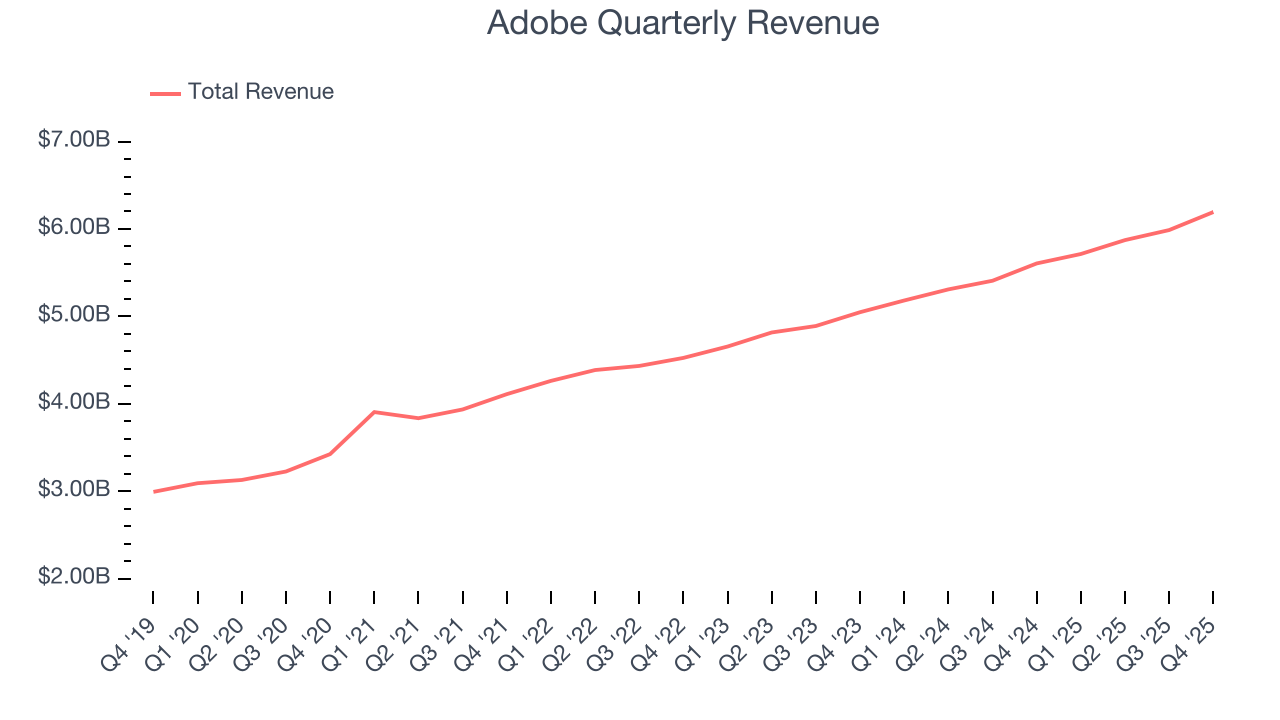

Creative software giant Adobe (NASDAQ:ADBE) reported Q4 CY2025 results exceeding the market’s revenue expectations, with sales up 10.5% year on year to $6.19 billion. Guidance for next quarter’s revenue was better than expected at $6.28 billion at the midpoint, 0.7% above analysts’ estimates. Its non-GAAP profit of $5.50 per share was 1.9% above analysts’ consensus estimates.

Adobe (ADBE) Q4 CY2025 Highlights:

- Revenue: $6.19 billion vs analyst estimates of $6.11 billion (10.5% year-on-year growth, 1.4% beat)

- Adjusted EPS: $5.50 vs analyst estimates of $5.40 (1.9% beat)

- Adjusted Operating Income: $2.82 billion vs analyst estimates of $2.78 billion (45.6% margin, 1.5% beat)

- Revenue Guidance for Q1 CY2026 is $6.28 billion at the midpoint, roughly in line with what analysts were expecting

- Adjusted EPS guidance for the upcoming financial year 2026 is $23.40 at the midpoint, in line with analyst estimates

- Operating Margin: 36.5%, up from 34.9% in the same quarter last year

- Free Cash Flow Margin: 50.5%, up from 35.5% in the previous quarter

- Annual Recurring Revenue: $19.2 billion

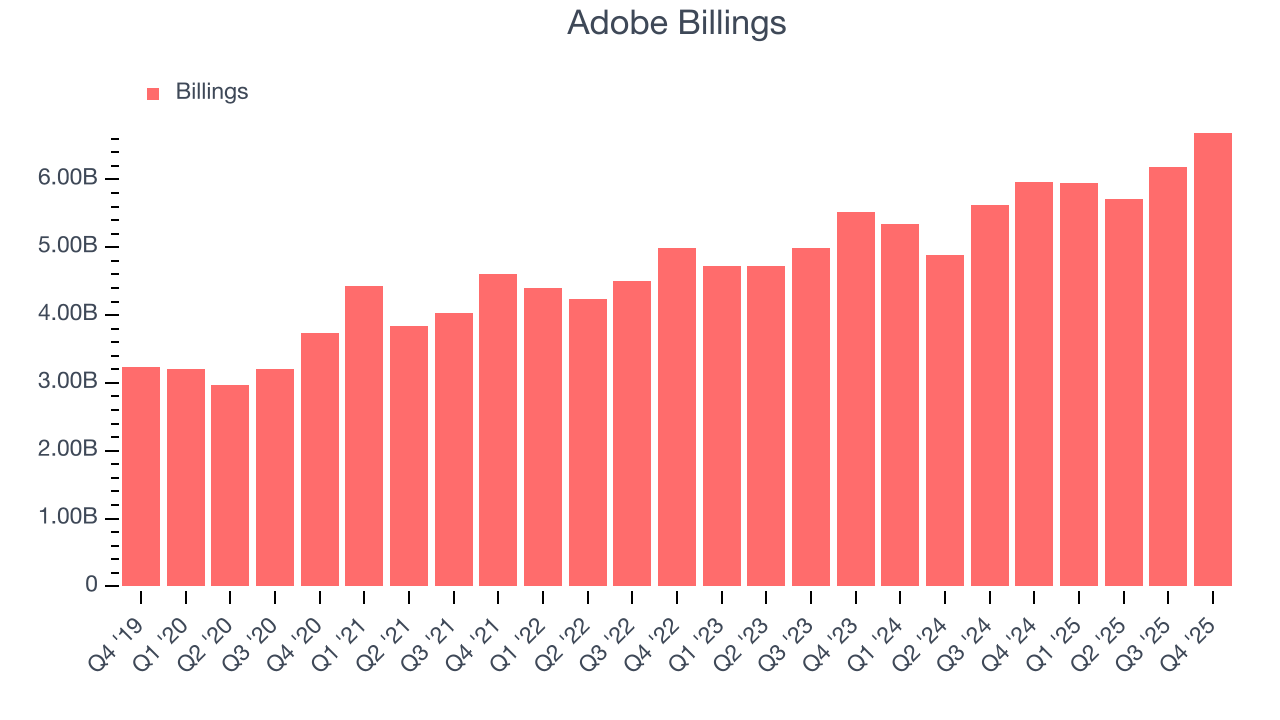

- Billings: $6.69 billion at quarter end, up 12.3% year on year

- Market Capitalization: $144.1 billion

Company Overview

Originally named after Adobe Creek that ran behind co-founder John Warnock's house, Adobe (NASDAQ:ADBE) develops software products used for digital content creation, document management, and marketing solutions across desktop, mobile, and cloud platforms.

Adobe operates through three main segments: Digital Media, Digital Experience, and Publishing and Advertising. The Digital Media segment includes the company's flagship Creative Cloud subscription service, featuring industry-standard applications like Photoshop, Illustrator, Premiere Pro, and InDesign, used by creative professionals, communicators, and increasingly, everyday users. This segment also houses Document Cloud, centered around Adobe Acrobat and Acrobat Sign, which enables digital document workflows across devices.

The Digital Experience segment provides an integrated platform through Adobe Experience Cloud that helps businesses manage customer relationships and deliver personalized experiences. Built on Adobe Experience Platform, these solutions collect and analyze customer data to create unified profiles that update in real time, allowing businesses to tailor their marketing and content delivery.

Adobe has significantly invested in artificial intelligence, integrating generative AI capabilities across its product suite. Adobe Firefly, the company's generative AI model, allows users to create images, text effects, vector graphics, and video using text prompts. For enterprises, Adobe offers Custom Models that can be trained on company-specific brand assets.

Revenue primarily comes from subscription models across both consumer and enterprise products. Adobe's customer base ranges from individual creators and small businesses to large multinational corporations spanning virtually every industry. The company maintains partnerships with technology providers, systems integrators, and marketing agencies to extend its market reach globally.

4. Design Software

The demand for rich, interactive 2D, 3D, VR and AR experiences is growing, and while the ubiquitous metaverse might still be more of a buzzword than a real thing, what is real is the demand for the tools to create these experiences, whether they are games, 3D tours or interactive movies.

Adobe's competitors in creative software include Canva, Affinity (Serif), and Corel, while its document management offerings compete with DocuSign (NASDAQ:DOCU) and Microsoft (NASDAQ:MSFT). In the digital experience space, Adobe faces competition from Salesforce (NYSE:CRM), Oracle (NYSE:ORCL), and SAP (NYSE:SAP).

5. Revenue Growth

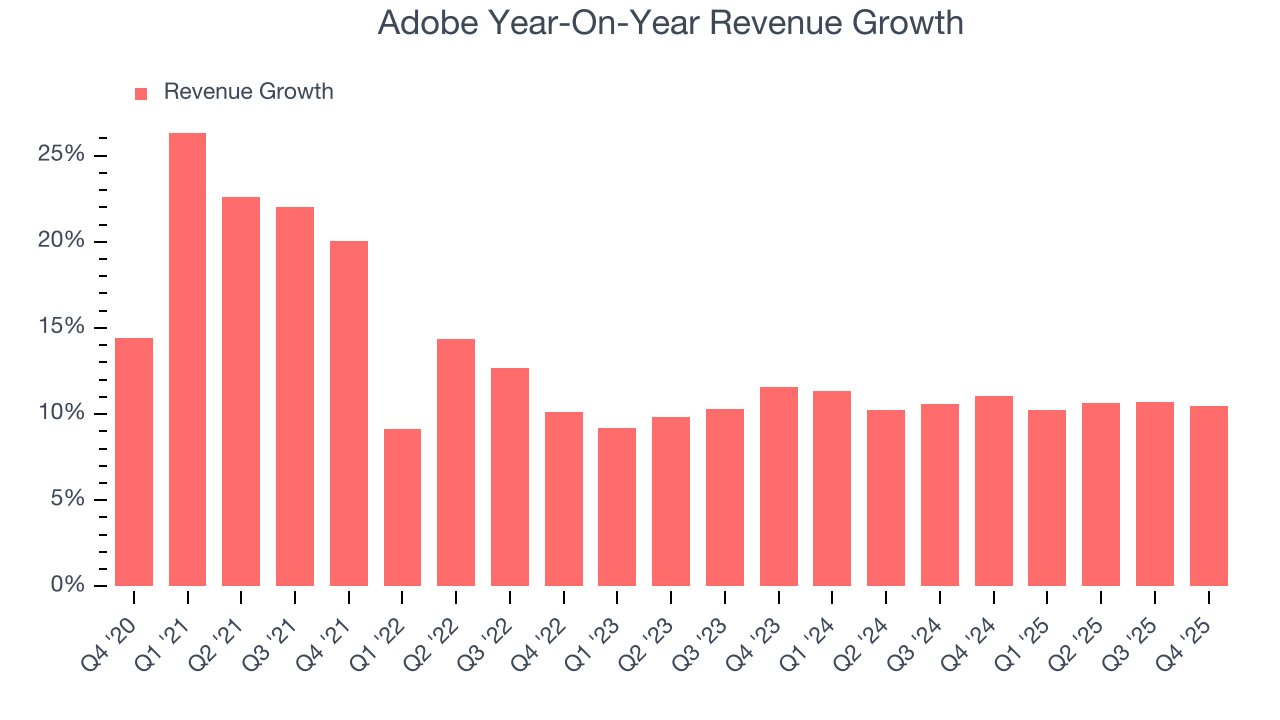

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Adobe grew its sales at a 13.1% annual rate. Although this growth is acceptable on an absolute basis, it fell short of our standards for the software sector, which enjoys a number of secular tailwinds.

Long-term growth is the most important, but within software, a half-decade historical view may miss new innovations or demand cycles. Adobe’s recent performance shows its demand has slowed as its annualized revenue growth of 10.7% over the last two years was below its five-year trend.

This quarter, Adobe reported year-on-year revenue growth of 10.5%, and its $6.19 billion of revenue exceeded Wall Street’s estimates by 1.4%. Company management is currently guiding for a 9.8% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 8.7% over the next 12 months, a slight deceleration versus the last two years. This projection doesn't excite us and implies its products and services will see some demand headwinds.

6. Billings

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Adobe’s billings came in at $6.69 billion in Q4, and over the last four quarters, its growth was underwhelming as it averaged 12.6% year-on-year increases. However, this alternate topline metric grew faster than total sales, meaning the company collects cash upfront and then recognizes the revenue over the length of its contracts - a boost for its liquidity and future revenue prospects.

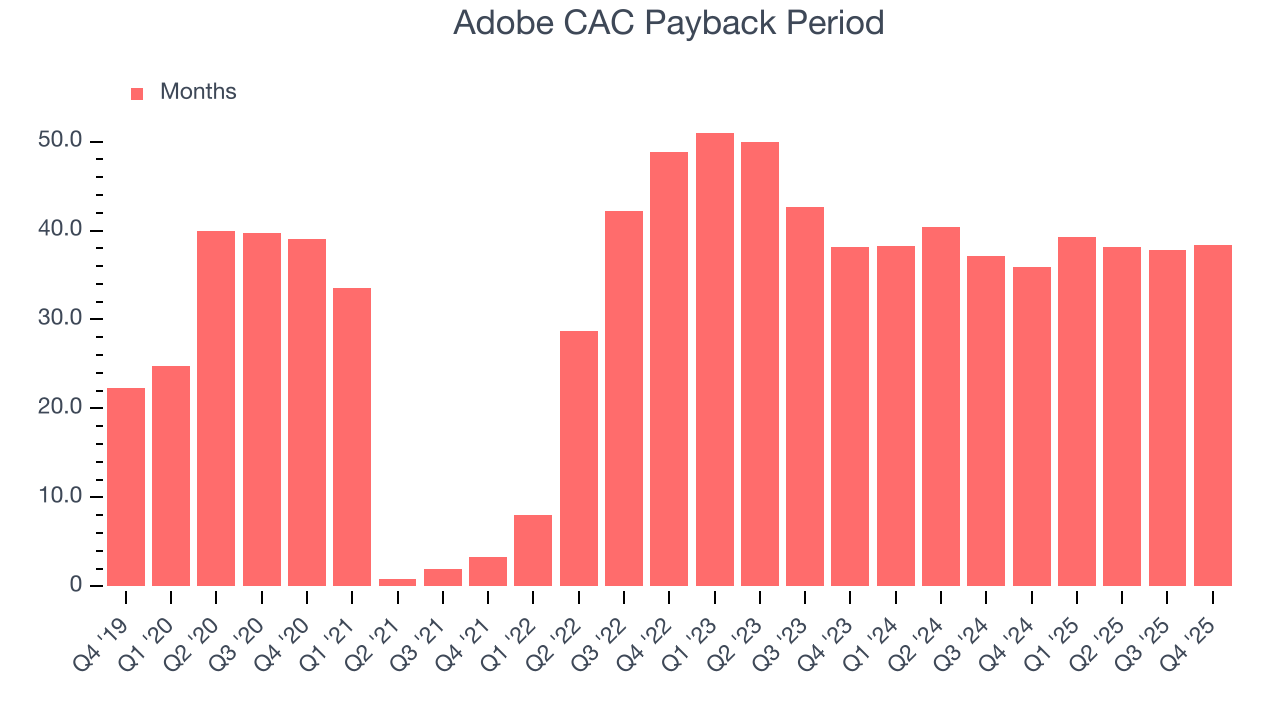

7. Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

Adobe is efficient at acquiring new customers, and its CAC payback period checked in at 38.4 months this quarter. The company’s relatively fast recovery of its customer acquisition costs means it can attempt to spur growth by increasing its sales and marketing investments.

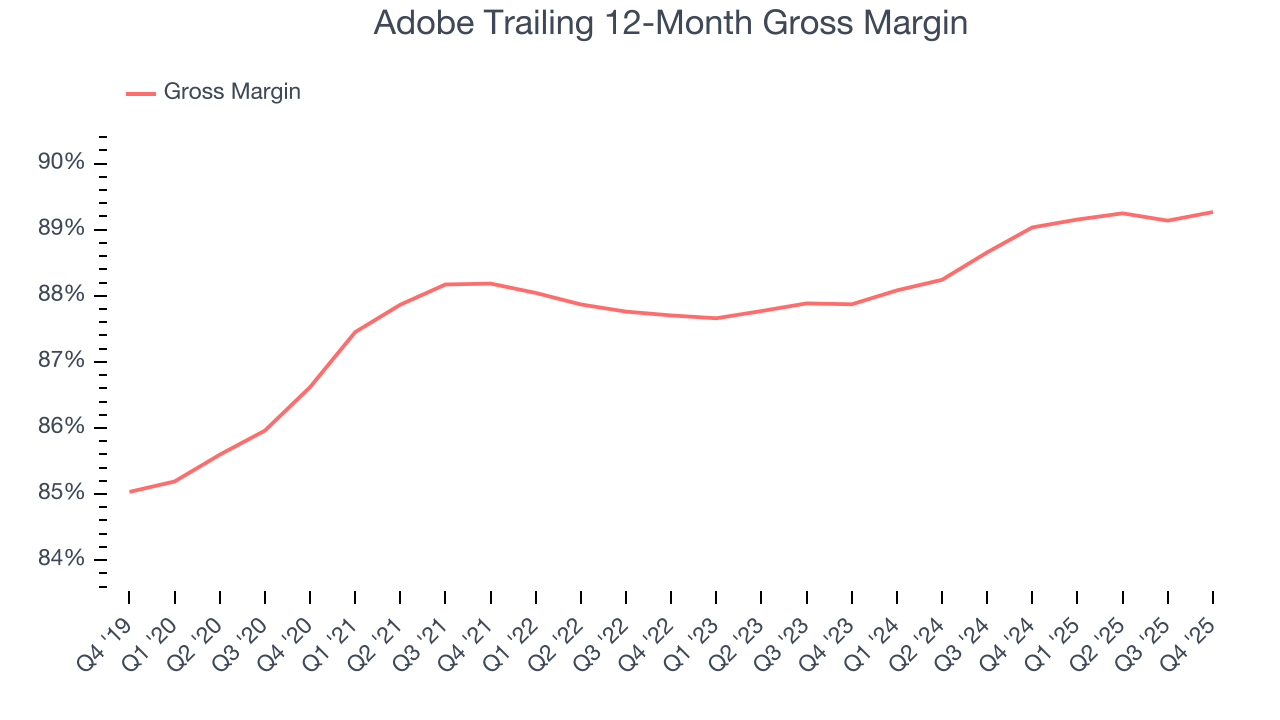

8. Gross Margin & Pricing Power

For software companies like Adobe, gross profit tells us how much money remains after paying for the base cost of products and services (typically servers, licenses, and certain personnel). These costs are usually low as a percentage of revenue, explaining why software is more lucrative than other sectors.

Adobe’s gross margin is one of the highest in the software sector, an output of its asset-lite business model and strong pricing power. It also enables the company to fund large investments in new products and sales during periods of rapid growth to achieve higher profits in the future. As you can see below, it averaged an elite 89.3% gross margin over the last year. That means Adobe only paid its providers $10.73 for every $100 in revenue.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. Adobe has seen gross margins improve by 1.4 percentage points over the last 2 year, which is solid in the software space.

In Q4, Adobe produced a 89.5% gross profit margin, in line with the same quarter last year. Zooming out, the company’s full-year margin has remained steady over the past 12 months, suggesting its input costs have been stable and it isn’t under pressure to lower prices.

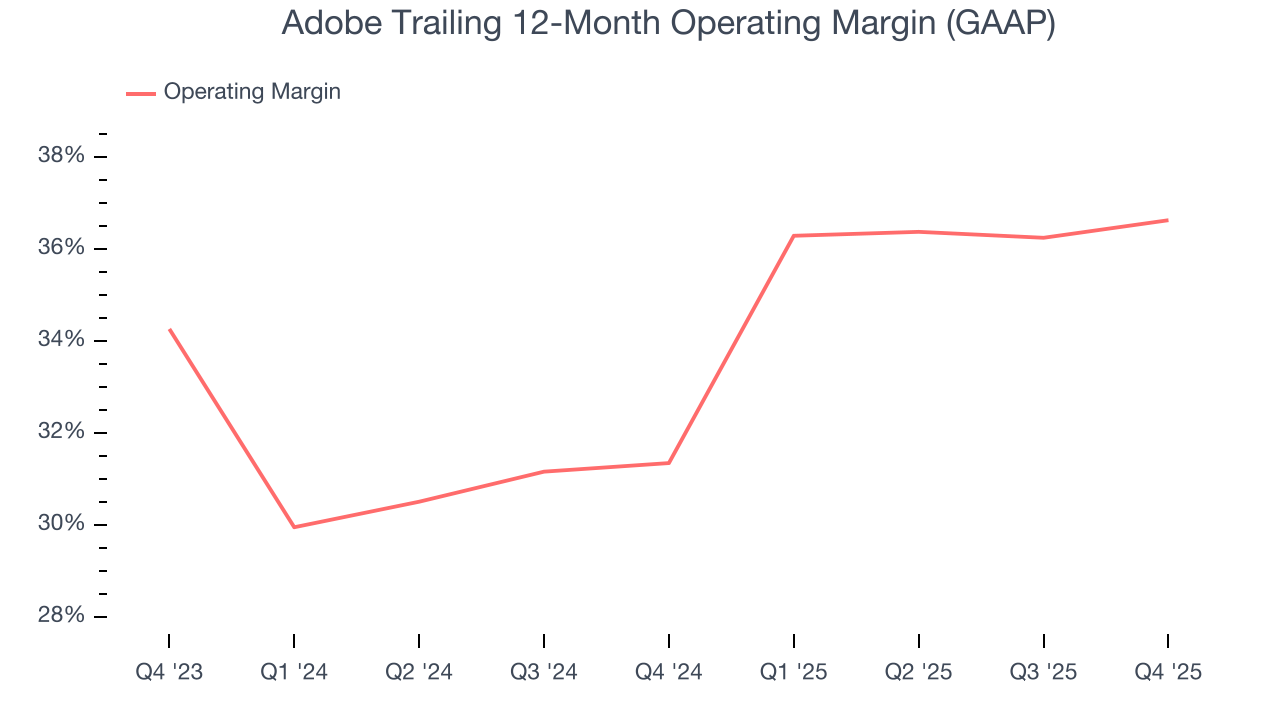

9. Operating Margin

Adobe has been a well-oiled machine over the last year. It demonstrated elite profitability for a software business, boasting an average operating margin of 36.6%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Looking at the trend in its profitability, Adobe’s operating margin rose by 5.3 percentage points over the last two years, as its sales growth gave it operating leverage.

In Q4, Adobe generated an operating margin profit margin of 36.5%, up 1.6 percentage points year on year. The increase was encouraging, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

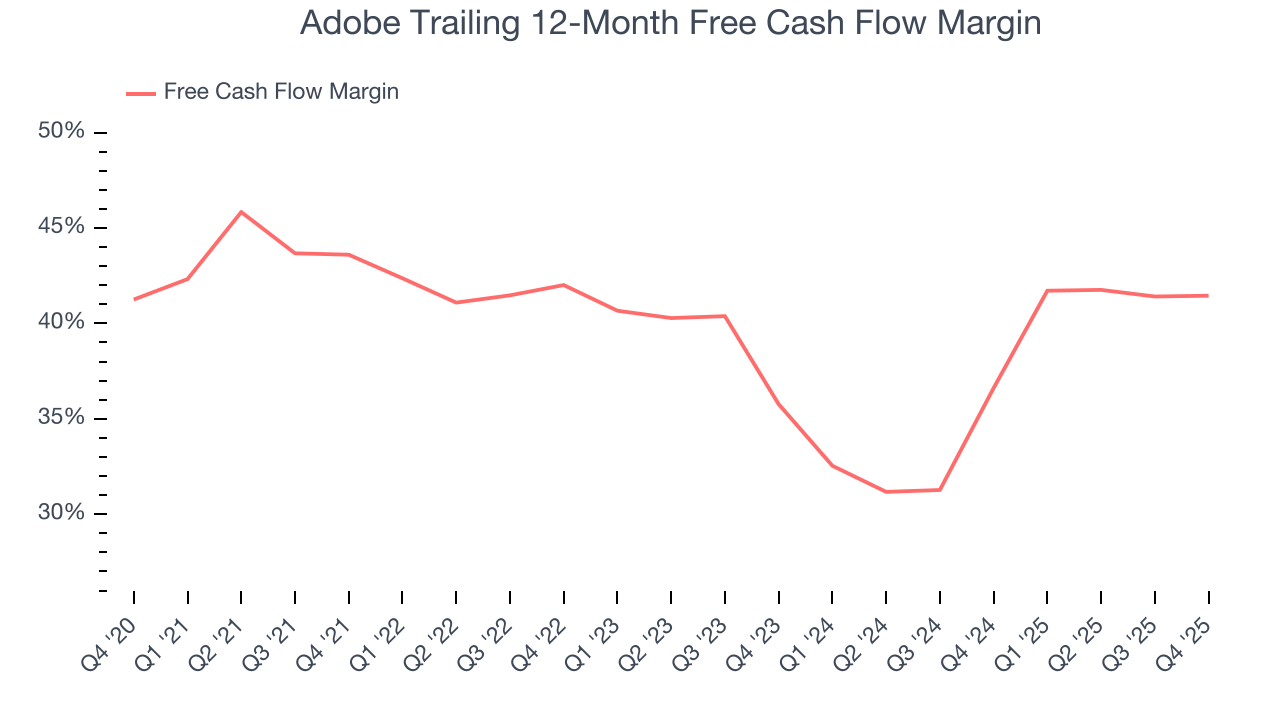

10. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Adobe has shown terrific cash profitability, driven by its lucrative business model and cost-effective customer acquisition strategy that enable it to stay ahead of the competition through investments in new products rather than sales and marketing. The company’s free cash flow margin was among the best in the software sector, averaging an eye-popping 41.4% over the last year.

Adobe’s free cash flow clocked in at $3.13 billion in Q4, equivalent to a 50.5% margin. This cash profitability was in line with the comparable period last year and above its one-year average.

Over the next year, analysts predict Adobe’s cash conversion will slightly fall. Their consensus estimates imply its free cash flow margin of 41.4% for the last 12 months will decrease to 39.7%.

11. Key Takeaways from Adobe’s Q4 Results

It was great to see Adobe’s EPS guidance for next quarter top analysts’ expectations. We were also glad its billings outperformed Wall Street’s estimates. Less exciting was that revenue guidance next quarter and EPS guidance for the full year were both just in line. Overall, we think this was still a solid quarter with some key areas of upside. The stock remained flat at $342.41 immediately following the results.

12. Is Now The Time To Buy Adobe?

Updated: December 10, 2025 at 4:14 PM EST

A common mistake we notice when investors are deciding whether to buy a stock or not is that they simply look at the latest earnings results. Business quality and valuation matter more, so we urge you to understand these dynamics as well.

Adobe isn’t a terrible business, but it isn’t one of our picks. For starters, its revenue growth was uninspiring over the last five years, and analysts expect its demand to deteriorate over the next 12 months. And while Adobe’s bountiful generation of free cash flow empowers it to invest in growth initiatives, its expanding operating margin shows it’s becoming more efficient at building and selling its software.

Adobe’s price-to-sales ratio based on the next 12 months is 5.5x. This valuation is reasonable, but the company’s shakier fundamentals present too much downside risk. We're fairly confident there are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $444.23 on the company (compared to the current share price of $342.41).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.