ADP (ADP)

We’re firm believers in ADP. It consistently invests in attractive growth opportunities, generating substantial cash flows and returns.― StockStory Analyst Team

1. News

2. Summary

Why We Like ADP

Processing one out of every six paychecks in the United States, ADP (NASDAQ:ADP) provides cloud-based human capital management solutions that help businesses manage payroll, benefits, talent acquisition, and HR administration.

- Dominant market position is represented by its $21.21 billion in revenue and gives it fixed cost leverage when sales grow

- Excellent adjusted operating margin highlights the strength of its business model

- Impressive free cash flow profitability enables the company to fund new investments or reward investors with share buybacks/dividends, and its improved cash conversion implies it’s becoming a less capital-intensive business

ADP is a standout company. The price looks reasonable based on its quality, so this could be a prudent time to invest in some shares.

Why Is Now The Time To Buy ADP?

ADP is trading at $208.56 per share, or 18x forward P/E. Looking at the business services space, we think the valuation is fair - potentially even too low - for the business quality.

Where you buy a stock impacts returns. Our analysis shows that business quality is a much bigger determinant of market outperformance over the long term compared to entry price, but getting a good deal on a stock certainly isn’t a bad thing.

3. ADP (ADP) Research Report: Q4 CY2025 Update

Payroll and HR services provider Automatic Data Processing (NASDAQ:ADP) reported revenue ahead of Wall Streets expectations in Q4 CY2025, with sales up 6.2% year on year to $5.36 billion. Its non-GAAP profit of $2.62 per share was 2% above analysts’ consensus estimates.

ADP (ADP) Q4 CY2025 Highlights:

- Revenue: $5.36 billion vs analyst estimates of $5.33 billion (6.2% year-on-year growth, 0.6% beat)

- Adjusted EPS: $2.62 vs analyst estimates of $2.57 (2% beat)

- Adjusted EBITDA: $1.52 billion vs analyst estimates of $1.49 billion (28.4% margin, 2.1% beat)

- Operating Margin: 26.2%, in line with the same quarter last year

- Free Cash Flow Margin: 20.6%, down from 22% in the same quarter last year

- Market Capitalization: $102.9 billion

Company Overview

Processing one out of every six paychecks in the United States, ADP (NASDAQ:ADP) provides cloud-based human capital management solutions that help businesses manage payroll, benefits, talent acquisition, and HR administration.

ADP's comprehensive suite of services spans the entire employment lifecycle, from recruitment to retirement. The company offers tailored solutions for businesses of all sizes through its cloud-based platforms: RUN Powered by ADP for small businesses, ADP Workforce Now for mid-sized and large companies, and ADP Vantage HCM for large enterprises. These platforms integrate various HR functions into unified systems that streamline administrative processes.

Beyond software, ADP provides outsourcing options where clients can delegate specific HR functions or entire departments to ADP's specialists. Its Professional Employer Organization (PEO) service, ADP TotalSource, establishes a co-employment relationship where ADP assumes certain employer responsibilities while clients maintain business control. This arrangement allows smaller businesses to offer benefits comparable to larger organizations.

ADP's payroll services handle tax filings, compliance reporting, and various payment methods including direct deposit and digital accounts. For a manufacturing company with 500 employees, for example, ADP might process biweekly payroll, calculate appropriate tax withholdings, manage time tracking, and provide employees with mobile access to their pay information.

The company generates revenue through subscription fees for its software platforms and service packages, with pricing typically based on the number of employees and selected features. Additional revenue comes from add-on services like retirement plan administration, insurance services, and employment tax management.

ADP operates globally with solutions available in over 140 countries, though its primary markets are the United States, Canada, and Europe. The company maintains specialized expertise in local employment regulations, helping multinational clients navigate complex compliance requirements across different jurisdictions.

4. Data & Business Process Services

A combination of increasing reliance on data and analytics across various industries and the desire for cost efficiency through outsourcing could mean that companies in this space gain. As functions such as payroll, HR, and credit risk assessment rely on more digitization, key players in the data & business process services industry could be increased demand. On the other hand, the sector faces headwinds from growing regulatory scrutiny on data privacy and security, with laws like GDPR and evolving U.S. regulations potentially limiting data collection and monetization strategies. Additionally, rising cyber threats pose risks to firms handling sensitive personal and financial information, creating outsized headline risk when things go wrong in this area.

ADP's main competitors include Paychex (NASDAQ:PAYX), Workday (NASDAQ:WDAY), Ceridian (NYSE:CDAY), and UKG (private), along with enterprise software providers like Oracle (NYSE:ORCL) and SAP (NYSE:SAP) that offer HR management modules.

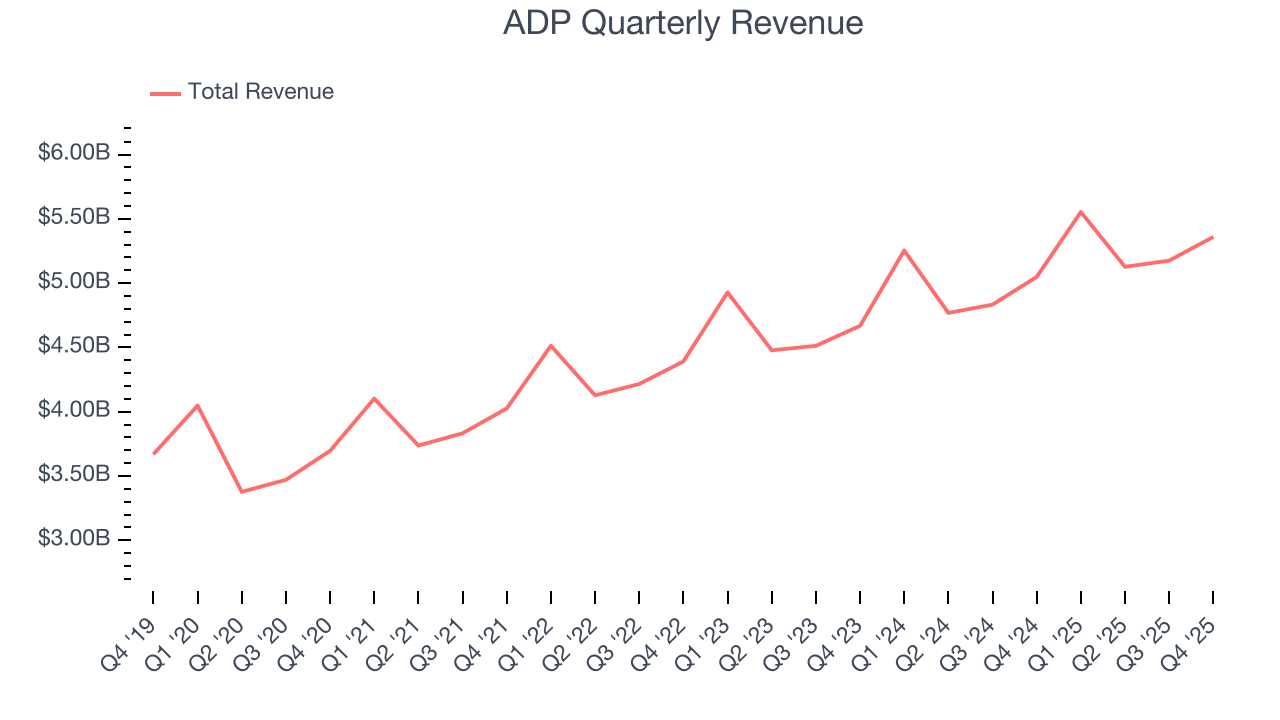

5. Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $21.21 billion in revenue over the past 12 months, ADP is a behemoth in the business services sector and benefits from economies of scale, giving it an edge in distribution. This also enables it to gain more leverage on its fixed costs than smaller competitors and the flexibility to offer lower prices.

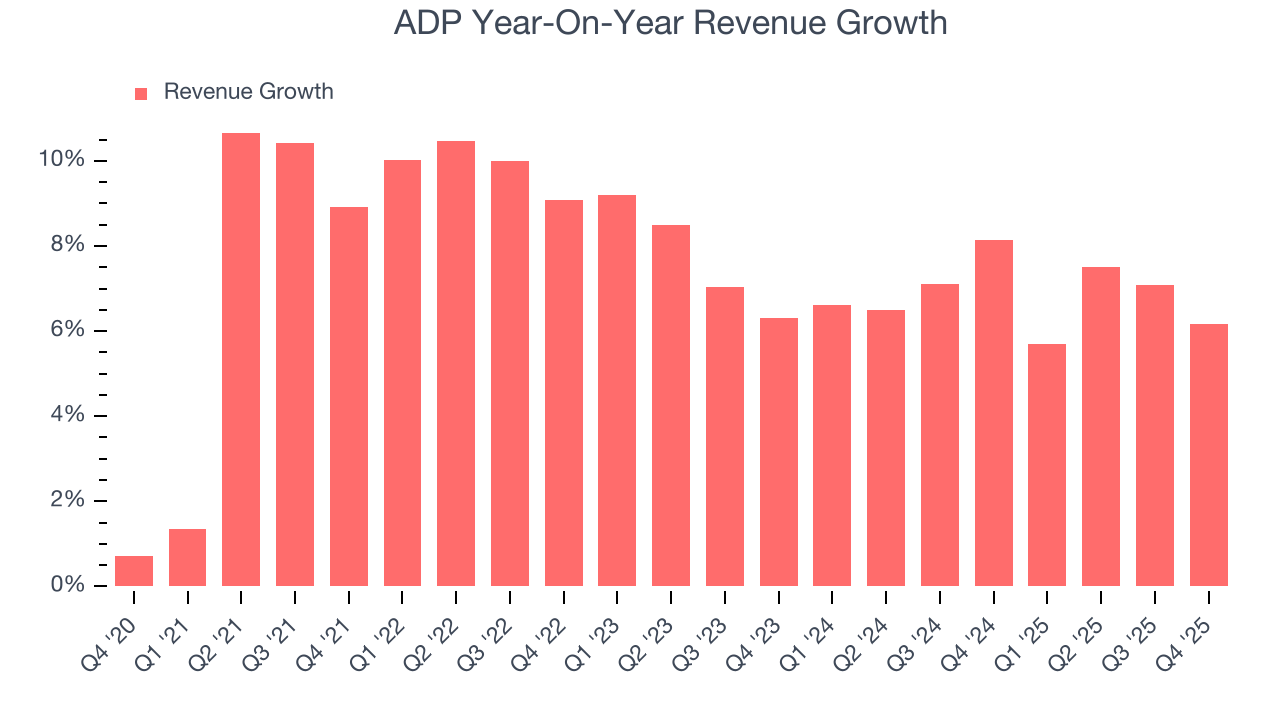

As you can see below, ADP’s 7.8% annualized revenue growth over the last five years was solid. This is a good starting point for our analysis because it shows ADP’s demand was higher than many business services companies.

We at StockStory place the most emphasis on long-term growth, but within business services, a half-decade historical view may miss recent innovations or disruptive industry trends. ADP’s annualized revenue growth of 6.8% over the last two years aligns with its five-year trend, suggesting its demand was stable.

This quarter, ADP reported year-on-year revenue growth of 6.2%, and its $5.36 billion of revenue exceeded Wall Street’s estimates by 0.6%.

Looking ahead, sell-side analysts expect revenue to grow 5.5% over the next 12 months, similar to its two-year rate. We still think its growth trajectory is satisfactory given its scale and suggests the market is forecasting success for its products and services.

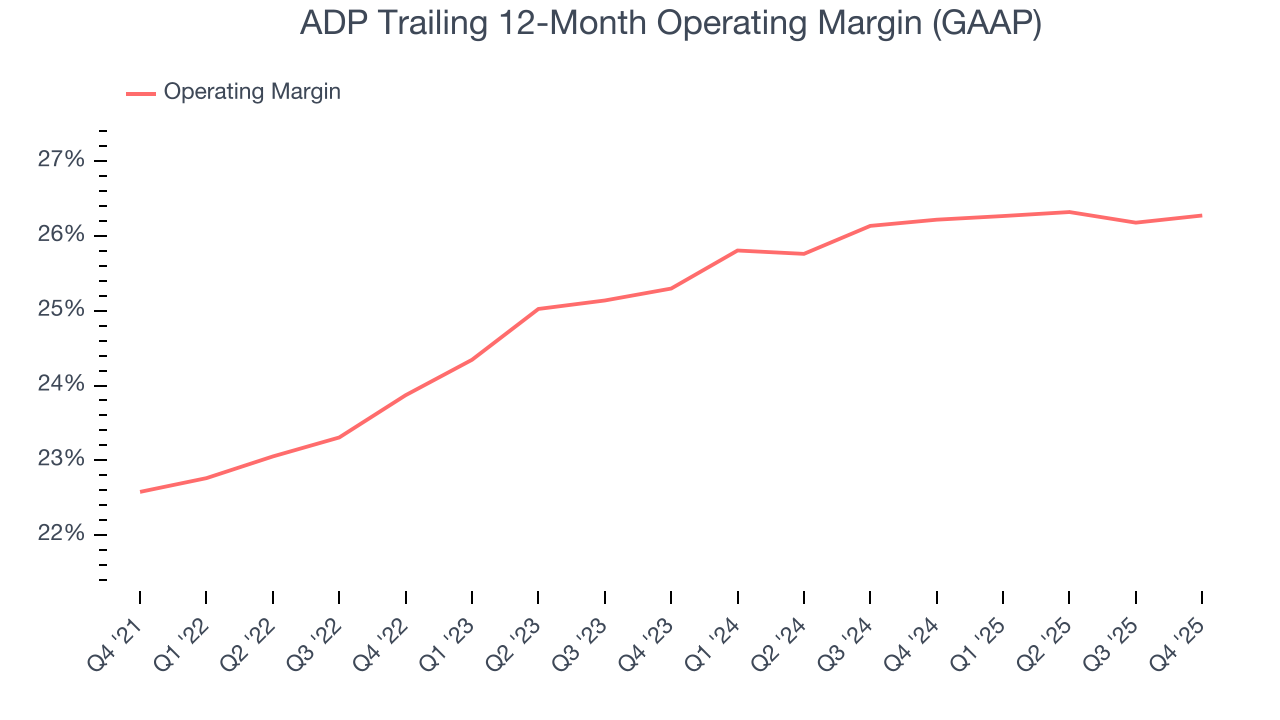

6. Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

ADP has been a well-oiled machine over the last five years. It demonstrated elite profitability for a business services business, boasting an average operating margin of 25%.

Analyzing the trend in its profitability, ADP’s operating margin rose by 3.7 percentage points over the last five years, as its sales growth gave it operating leverage.

In Q4, ADP generated an operating margin profit margin of 26.2%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

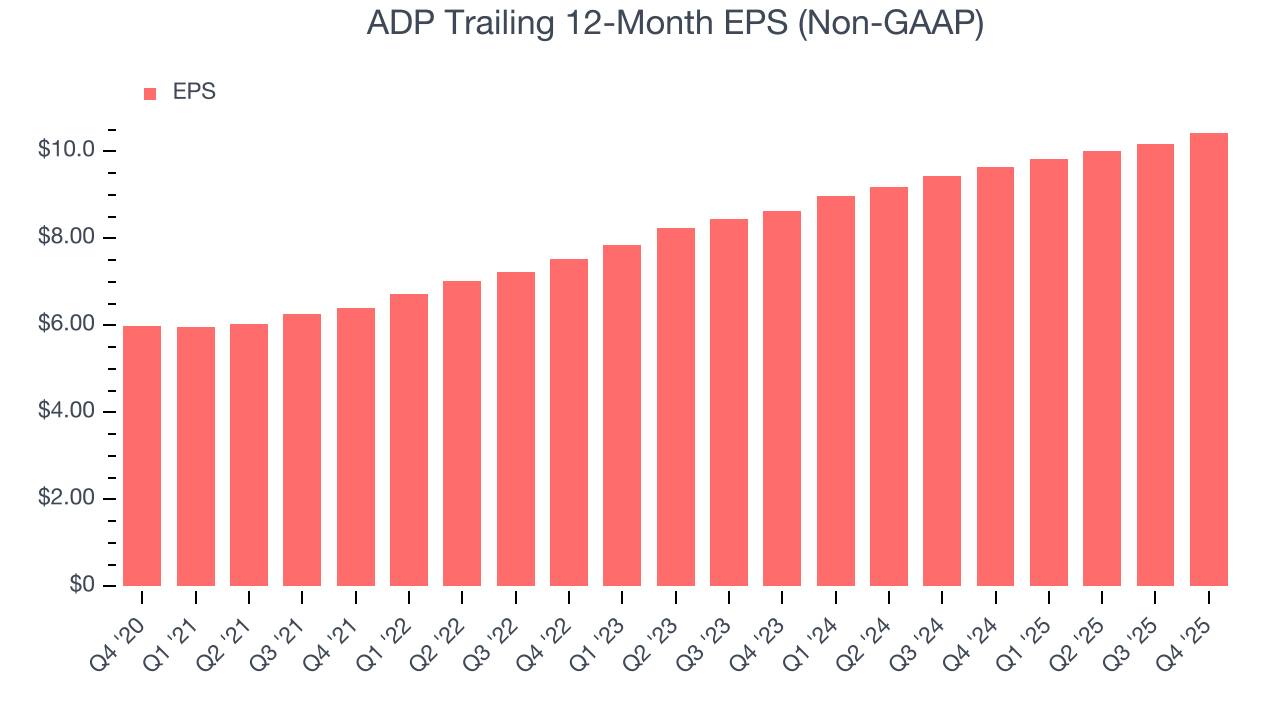

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

ADP’s EPS grew at a remarkable 11.7% compounded annual growth rate over the last five years, higher than its 7.8% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

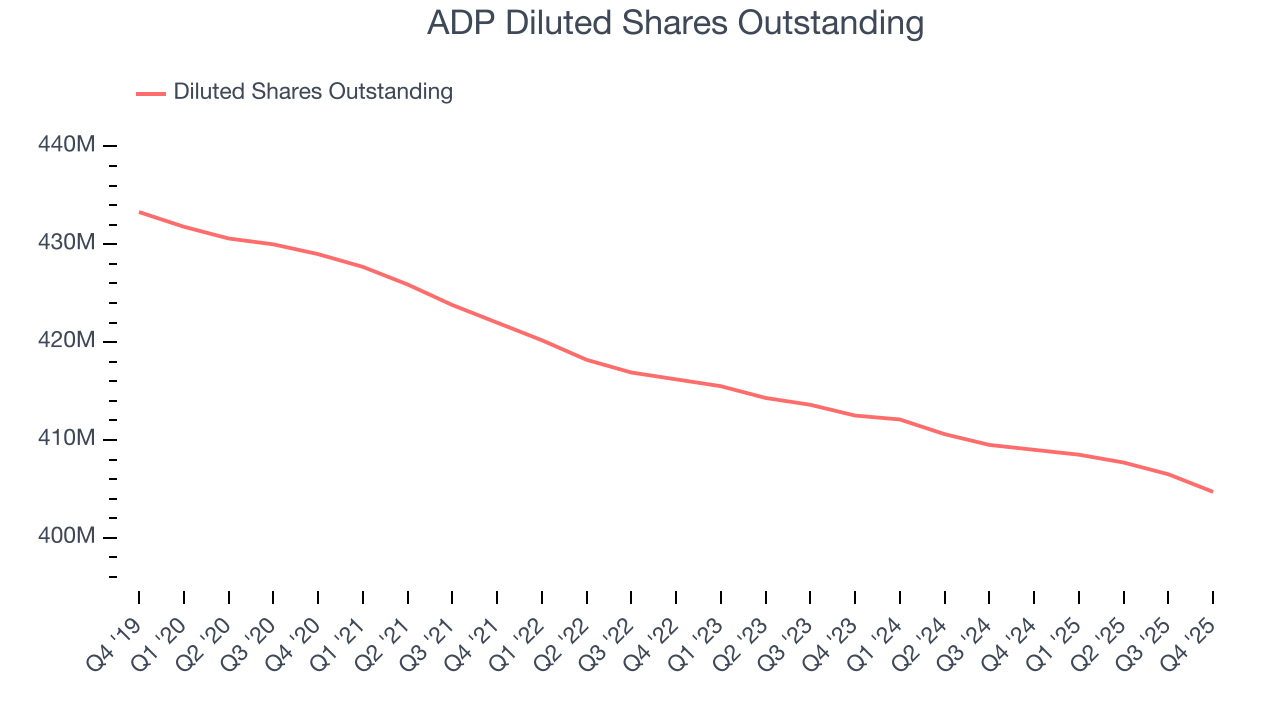

Diving into the nuances of ADP’s earnings can give us a better understanding of its performance. As we mentioned earlier, ADP’s operating margin was flat this quarter but expanded by 3.7 percentage points over the last five years. On top of that, its share count shrank by 5.7%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For ADP, its two-year annual EPS growth of 10% was lower than its five-year trend. This wasn’t great, but at least the company was successful in other measures of financial health.

In Q4, ADP reported adjusted EPS of $2.62, up from $2.35 in the same quarter last year. This print beat analysts’ estimates by 2%. Over the next 12 months, Wall Street expects ADP’s full-year EPS of $10.43 to grow 9.8%.

8. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

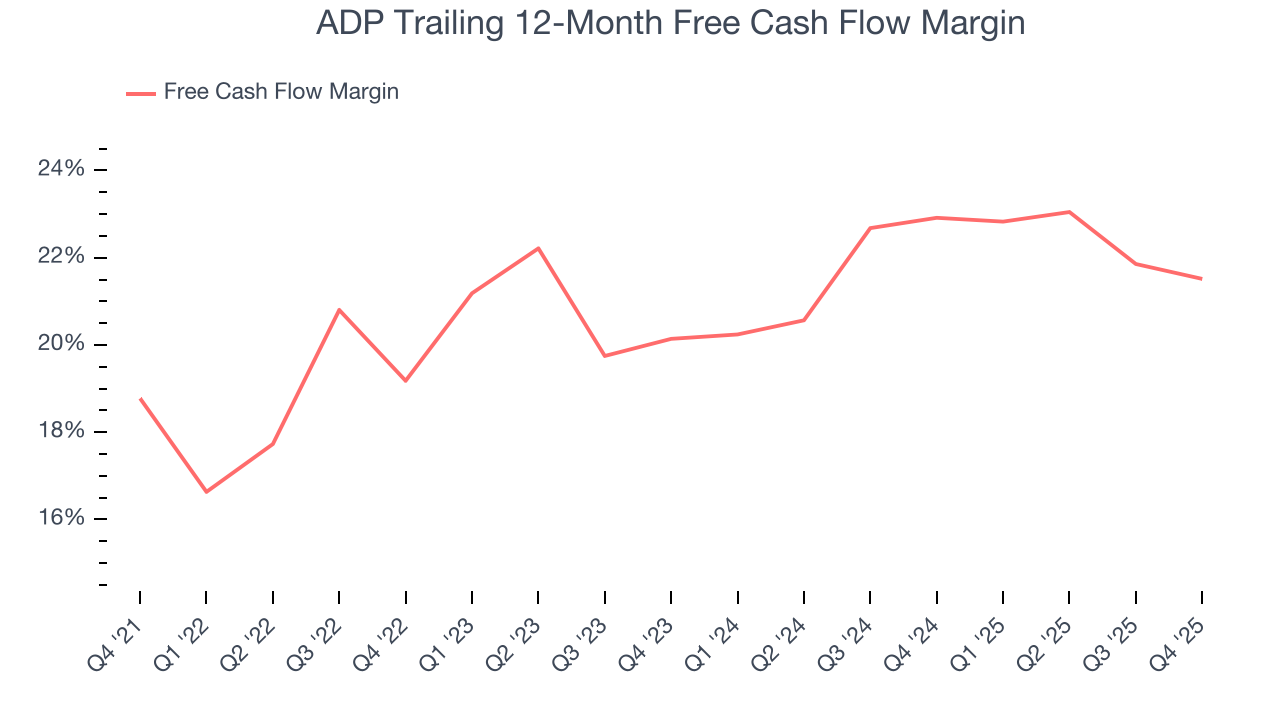

ADP has shown terrific cash profitability, enabling it to reinvest, return capital to investors, and stay ahead of the competition while maintaining an ample cushion. The company’s free cash flow margin was among the best in the business services sector, averaging 20.6% over the last five years.

Taking a step back, we can see that ADP’s margin expanded by 2.7 percentage points during that time. This is encouraging because it gives the company more optionality.

ADP’s free cash flow clocked in at $1.11 billion in Q4, equivalent to a 20.6% margin. The company’s cash profitability regressed as it was 1.4 percentage points lower than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, causing temporary swings. Long-term trends trump fluctuations.

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

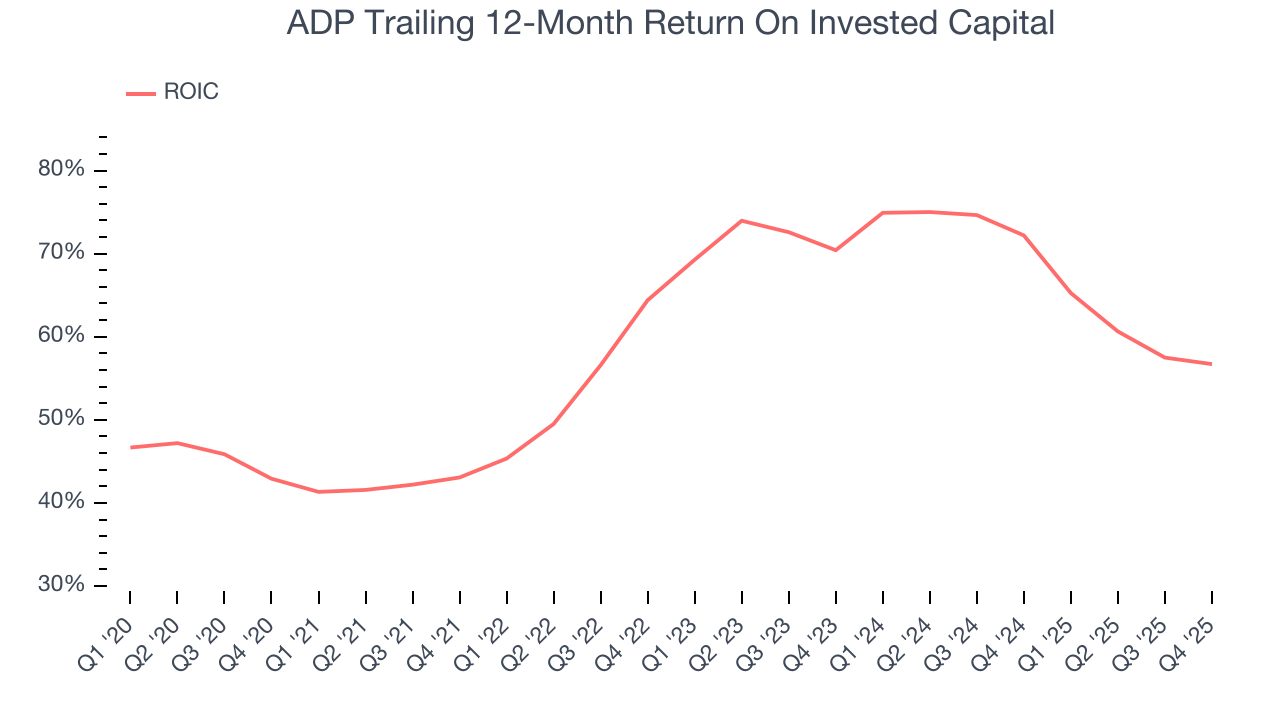

ADP’s five-year average ROIC was 61.4%, placing it among the best business services companies. This illustrates its management team’s ability to invest in highly profitable ventures and produce tangible results for shareholders.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, ADP’s ROIC has increased significantly. This is a great sign when paired with its already strong returns. It could suggest its competitive advantage or profitable growth opportunities are expanding.

10. Balance Sheet Assessment

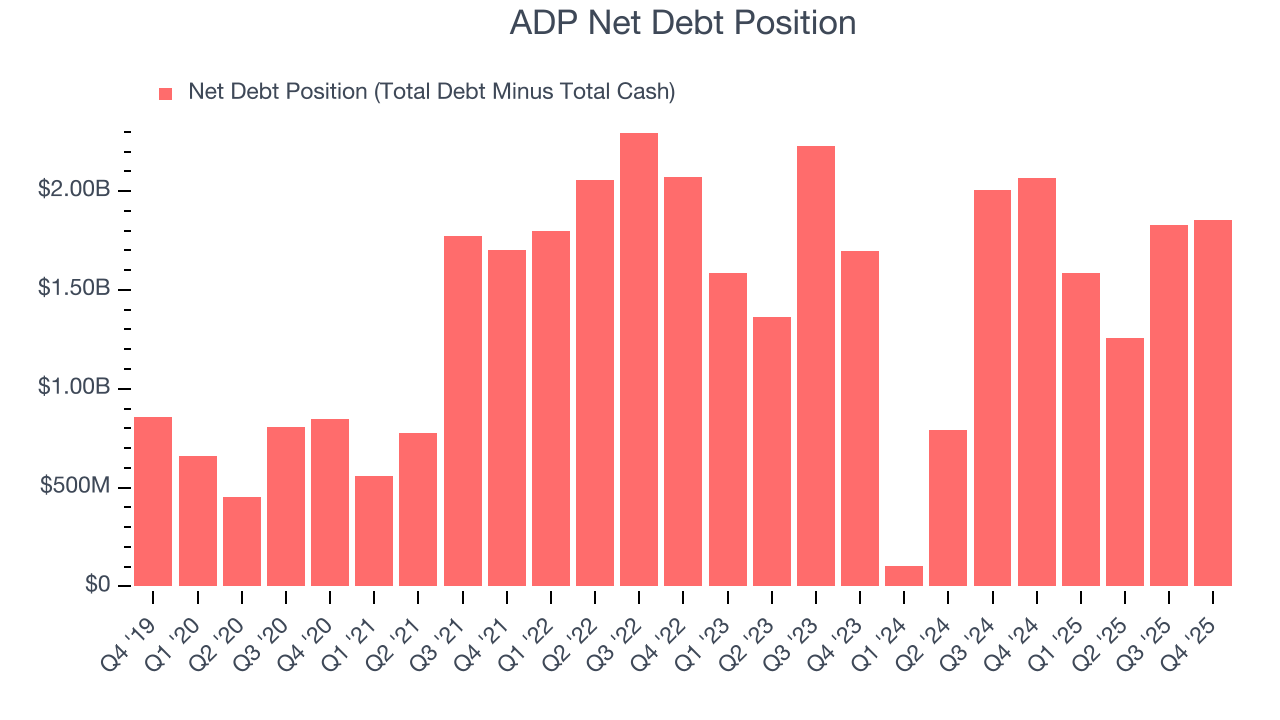

ADP reported $2.47 billion of cash and $4.32 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $6.06 billion of EBITDA over the last 12 months, we view ADP’s 0.3× net-debt-to-EBITDA ratio as safe. We also see its $45.6 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from ADP’s Q4 Results

It was good to see ADP beat analysts’ EPS expectations this quarter. We were also happy its revenue narrowly outperformed Wall Street’s estimates. Overall, this print had some key positives. The stock remained flat at $254.23 immediately after reporting.

12. Is Now The Time To Buy ADP?

Updated: March 16, 2026 at 12:00 AM EDT

Before making an investment decision, investors should account for ADP’s business fundamentals and valuation in addition to what happened in the latest quarter.

ADP is a high-quality business worth owning. For starters, its revenue growth was solid over the last five years. On top of that, its scale makes it a trusted partner with negotiating leverage, and its powerful free cash flow generation enables it to stay ahead of the competition through consistent reinvestment of profits.

ADP’s P/E ratio based on the next 12 months is 18x. Looking across the spectrum of business services companies today, ADP’s fundamentals shine bright. We like the stock at this price.

Wall Street analysts have a consensus one-year price target of $272 on the company (compared to the current share price of $208.56), implying they see 30.4% upside in buying ADP in the short term.