Akamai Technologies (AKAM)

We wouldn’t buy Akamai Technologies. Its weak revenue growth and gross margin show it not only lacks demand but also decent unit economics.― StockStory Analyst Team

1. News

2. Summary

Why We Think Akamai Technologies Will Underperform

With a massive distributed network spanning 4,100+ points of presence in nearly 130 countries, Akamai Technologies (NASDAQ:AKAM) provides a global distributed cloud platform that helps businesses deliver, secure, and optimize their digital experiences online.

- Bad unit economics and steep infrastructure costs are reflected in its gross margin of 58.9%, one of the worst among software companies

- Competitive market means the company must spend more on sales and marketing to stand out even if the return on investment is low

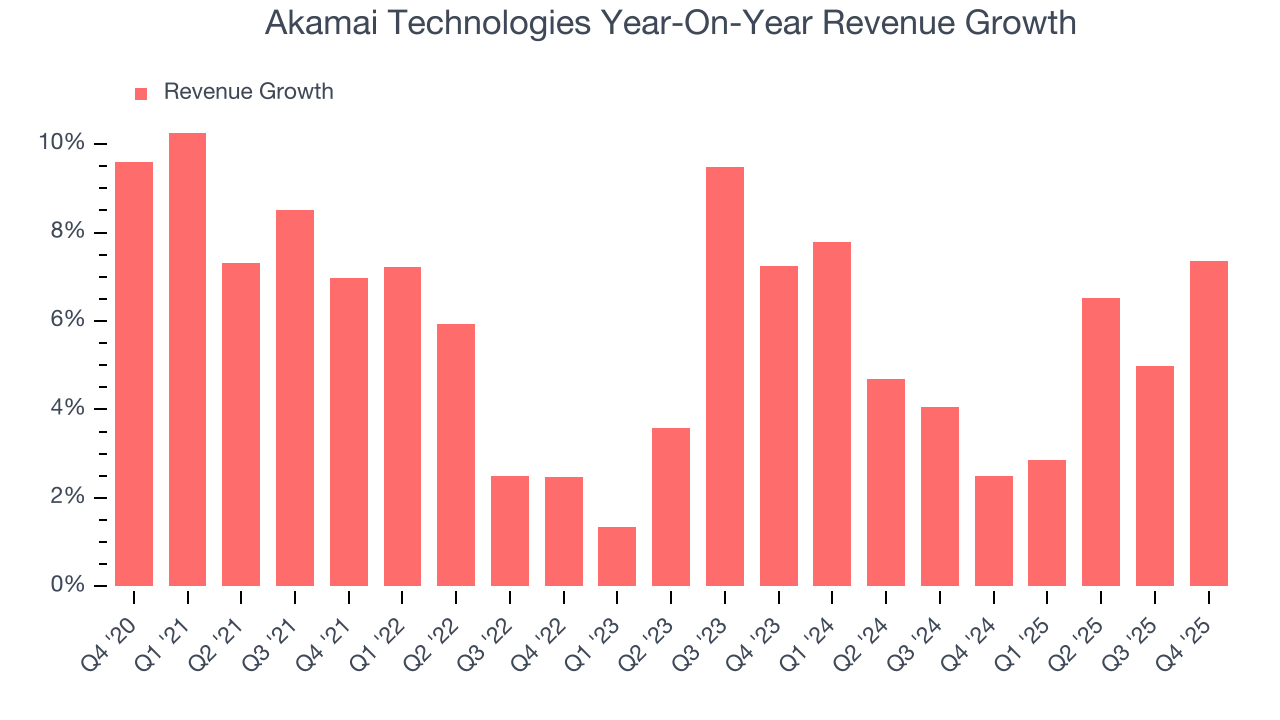

- Annual revenue growth of 5.1% over the last two years was well below our standards for the software sector

Akamai Technologies doesn’t meet our quality standards. You should search for better opportunities.

Why There Are Better Opportunities Than Akamai Technologies

At $105.80 per share, Akamai Technologies trades at 3.5x forward price-to-sales. Akamai Technologies’s valuation may seem like a great deal, but we think there are valid reasons why it’s so cheap.

We’d rather pay up for companies with elite fundamentals than get a bargain on weak ones. Cheap stocks can be value traps, and as their performance deteriorates, they will stay cheap or get even cheaper.

3. Akamai Technologies (AKAM) Research Report: Q4 CY2025 Update

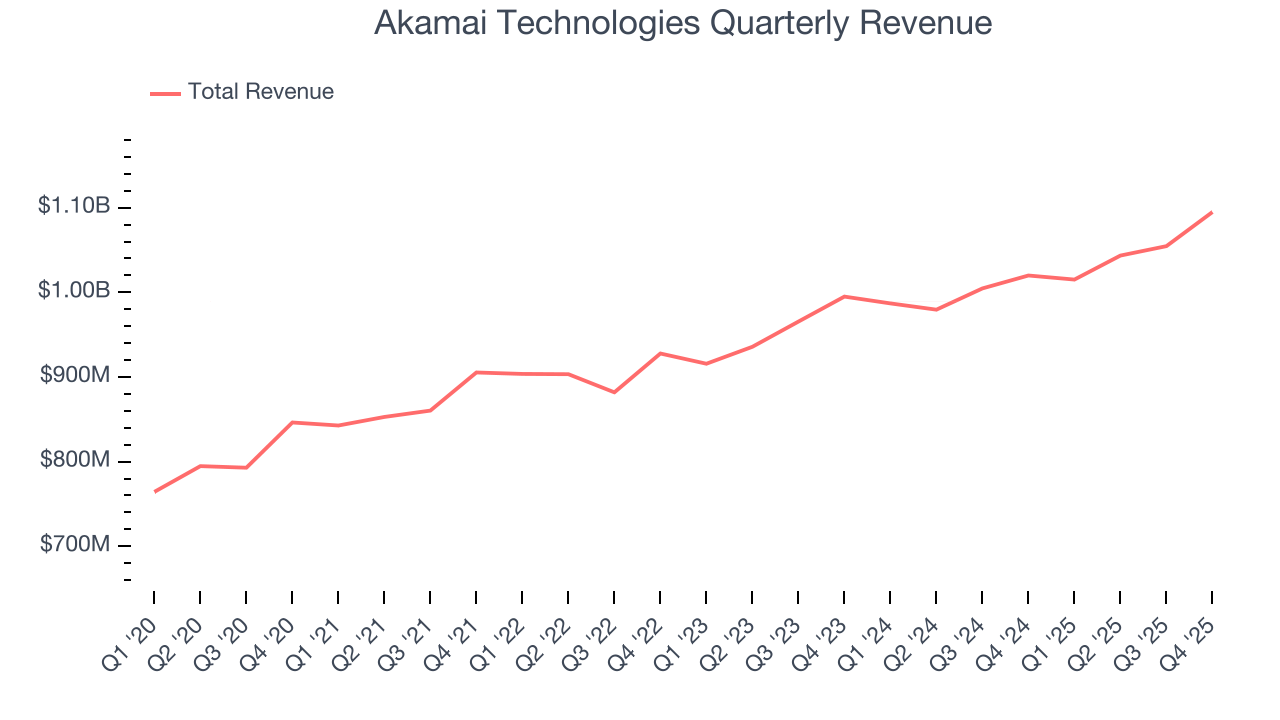

Cloud technology company Akamai Technologies (NASDAQ:AKAM) beat Wall Street’s revenue expectations in Q4 CY2025, with sales up 7.4% year on year to $1.09 billion. The company expects next quarter’s revenue to be around $1.07 billion, close to analysts’ estimates. Its non-GAAP profit of $1.84 per share was 5.1% above analysts’ consensus estimates.

Akamai Technologies (AKAM) Q4 CY2025 Highlights:

- Revenue: $1.09 billion vs analyst estimates of $1.08 billion (7.4% year-on-year growth, 1.6% beat)

- Adjusted EPS: $1.84 vs analyst estimates of $1.75 (5.1% beat)

- Adjusted Operating Income: $316 million vs analyst estimates of $311.4 million (28.9% margin, 1.5% beat)

- Revenue Guidance for Q1 CY2026 is $1.07 billion at the midpoint, roughly in line with what analysts were expecting

- Adjusted EPS guidance for the upcoming financial year 2026 is $6.70 at the midpoint, missing analyst estimates by 8.7%

- Operating Margin: 8.7%, down from 14.5% in the same quarter last year

- Free Cash Flow Margin: 14.8%, down from 23.4% in the previous quarter

- Market Capitalization: $15.73 billion

Company Overview

With a massive distributed network spanning 4,100+ points of presence in nearly 130 countries, Akamai Technologies (NASDAQ:AKAM) provides a global distributed cloud platform that helps businesses deliver, secure, and optimize their digital experiences online.

Akamai's platform, known as Akamai Connected Cloud, operates at a vast scale that gives it unique visibility into internet traffic patterns, congestion, and security threats worldwide. The company offers solutions in three core areas: security, content delivery, and compute services.

In security, Akamai provides protection against cyberattacks including DDoS mitigation, web application and API security, bot management, and zero trust solutions that help enterprises defend their digital assets. For content delivery, Akamai enables businesses to optimize website performance and media streaming, ensuring fast load times regardless of user location, device, or connection quality. These services are particularly valuable for companies delivering high-definition video, large software downloads, or operating global websites.

The compute services, enhanced by Akamai's 2022 acquisition of Linode, allow customers to build and deploy applications and workloads across the distributed platform. Unlike centralized cloud providers, Akamai's distributed architecture places computing resources closer to end users, reducing latency for time-sensitive applications.

A major e-commerce retailer might use Akamai to ensure their website loads quickly during a holiday sales event while simultaneously protecting it from DDoS attacks and credit card fraud attempts. Similarly, a streaming media company could use Akamai to deliver high-quality video content to millions of viewers worldwide while maintaining performance even during peak viewership periods.

4. Content Delivery

The amount of content on the internet is exploding, whether it is music, movies and or e-commerce stores. Consumer demand for this content creates network congestion, much like a digital traffic jam which drives demand for specialized content delivery networks (CDN) services that alleviate potential network bottlenecks.

Akamai competes with cloud and content delivery network providers like Cloudflare (NYSE:NET), Fastly (NYSE:FSLY), and Limelight Networks (NASDAQ:LLNW), along with major cloud providers such as Amazon Web Services (NASDAQ:AMZN), Microsoft Azure (NASDAQ:MSFT), and Google Cloud (NASDAQ:GOOGL).

5. Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Regrettably, Akamai Technologies’s sales grew at a weak 5.6% compounded annual growth rate over the last five years. This fell short of our benchmark for the software sector and is a poor baseline for our analysis.

Long-term growth is the most important, but within software, a half-decade historical view may miss new innovations or demand cycles. Akamai Technologies’s annualized revenue growth of 5.1% over the last two years aligns with its five-year trend, suggesting its demand was consistently weak.

This quarter, Akamai Technologies reported year-on-year revenue growth of 7.4%, and its $1.09 billion of revenue exceeded Wall Street’s estimates by 1.6%. Company management is currently guiding for a 5.7% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 5% over the next 12 months, similar to its two-year rate. This projection is underwhelming and indicates its newer products and services will not accelerate its top-line performance yet.

6. Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

Akamai Technologies’s recent customer acquisition efforts haven’t yielded returns as its CAC payback period was negative this quarter, meaning its incremental sales and marketing investments outpaced its revenue. The company’s inefficiency indicates it operates in a highly competitive environment where there is little differentiation between Akamai Technologies’s products and its peers.

7. Gross Margin & Pricing Power

For software companies like Akamai Technologies, gross profit tells us how much money remains after paying for the base cost of products and services (typically servers, licenses, and certain personnel). These costs are usually low as a percentage of revenue, explaining why software is more lucrative than other sectors.

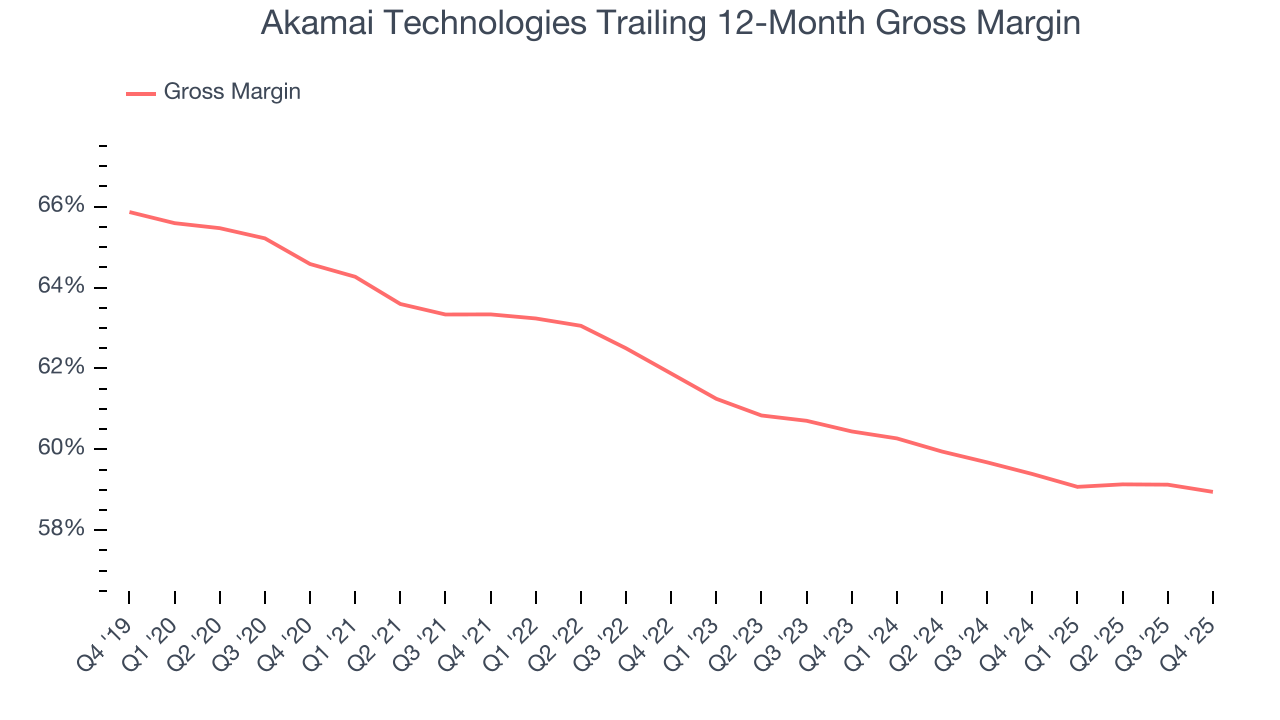

Akamai Technologies’s gross margin is substantially worse than most software businesses, signaling it has relatively high infrastructure costs compared to asset-lite businesses like ServiceNow. As you can see below, it averaged a 58.9% gross margin over the last year. Said differently, Akamai Technologies had to pay a chunky $41.05 to its service providers for every $100 in revenue.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. Akamai Technologies has seen gross margins decline by 1.5 percentage points over the last 2 year, which is poor compared to software peers.

Akamai Technologies’s gross profit margin came in at 58.7% this quarter, in line with the same quarter last year. Zooming out, the company’s full-year margin has remained steady over the past 12 months, suggesting its input costs have been stable and it isn’t under pressure to lower prices.

8. Operating Margin

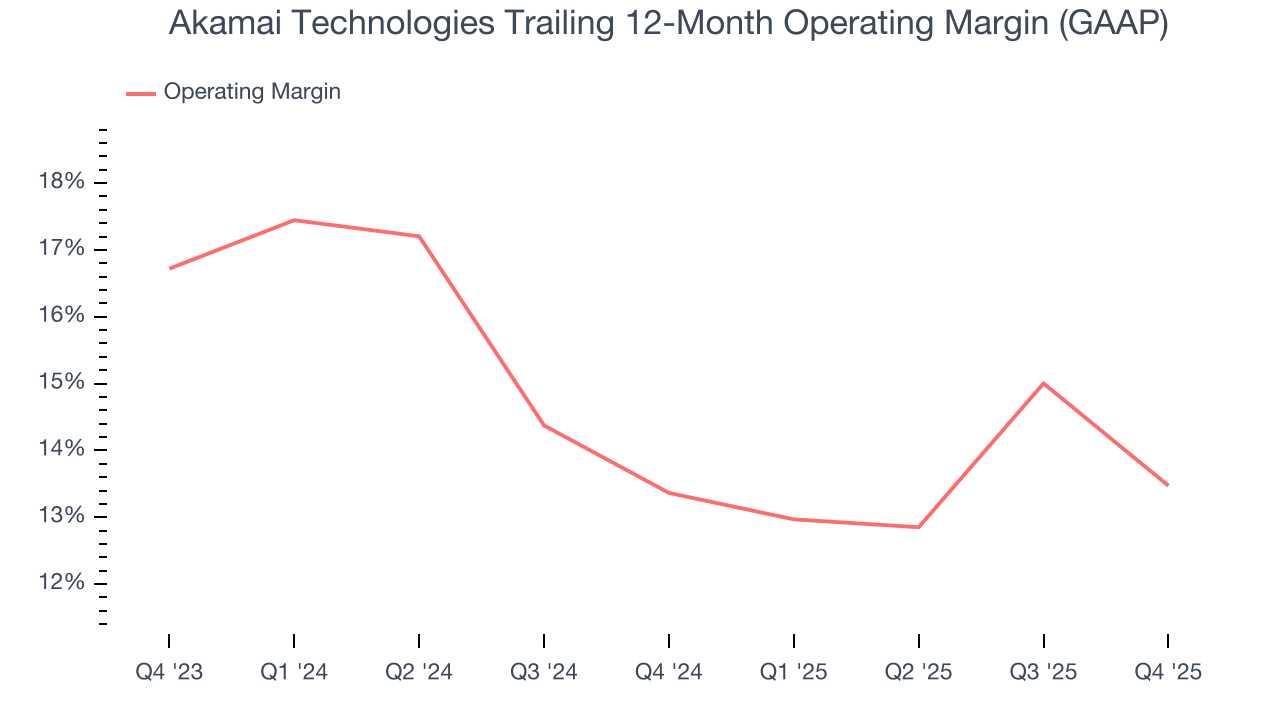

Akamai Technologies has been an efficient company over the last year. It was one of the more profitable businesses in the software sector, boasting an average operating margin of 13.5%. This result was particularly impressive because of its low gross margin, which is mostly a factor of what it sells and takes huge shifts to move meaningfully. Companies have more control over their operating margins, and it’s a show of well-managed operations if they’re high when gross margins are low.

Analyzing the trend in its profitability, Akamai Technologies’s operating margin might fluctuated slightly but has generally stayed the same over the last two years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, Akamai Technologies generated an operating margin profit margin of 8.7%, down 5.9 percentage points year on year. Since Akamai Technologies’s operating margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, R&D, and administrative overhead increased.

9. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

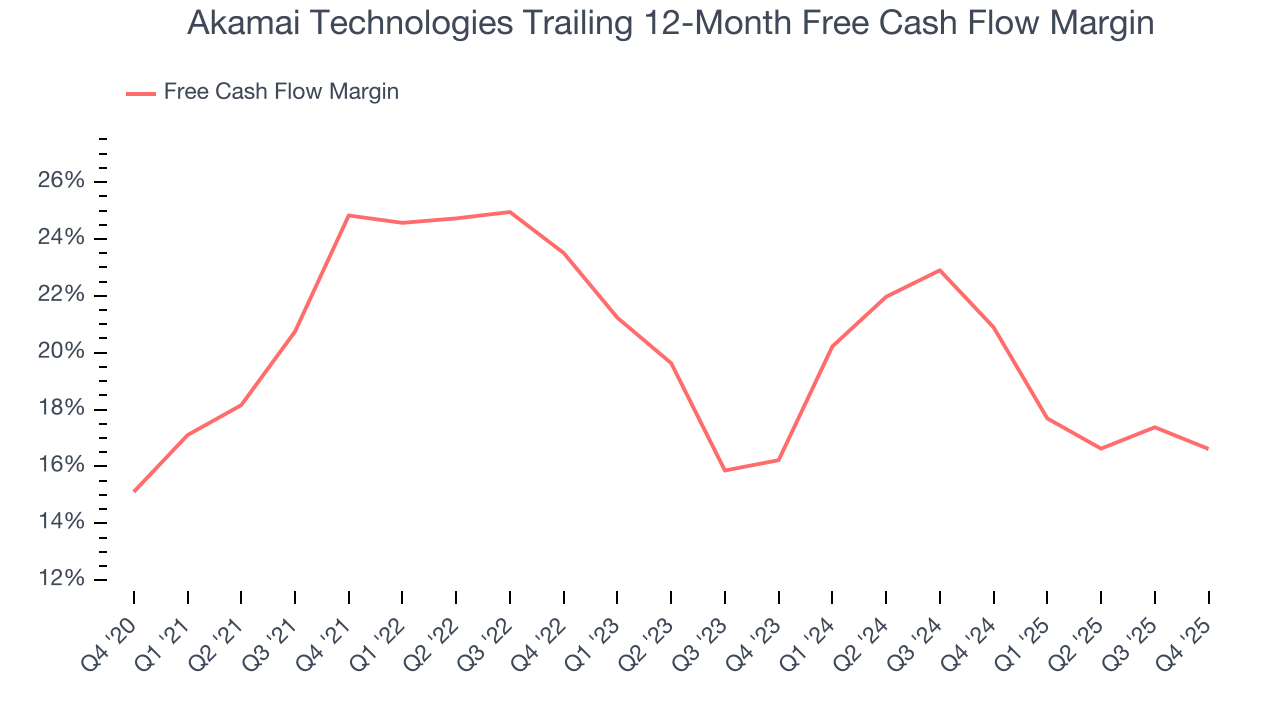

Akamai Technologies has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 16.6% over the last year, slightly better than the broader software sector.

Akamai Technologies’s free cash flow clocked in at $161.9 million in Q4, equivalent to a 14.8% margin. The company’s cash profitability regressed as it was 3 percentage points lower than in the same quarter last year, prompting us to pay closer attention. Short-term fluctuations typically aren’t a big deal because investment needs can be seasonal, but we’ll be watching to see if the trend extrapolates into future quarters.

Over the next year, analysts predict Akamai Technologies’s cash conversion will improve. Their consensus estimates imply its free cash flow margin of 16.6% for the last 12 months will increase to 20.1%, giving it more flexibility for investments, share buybacks, and dividends.

10. Balance Sheet Assessment

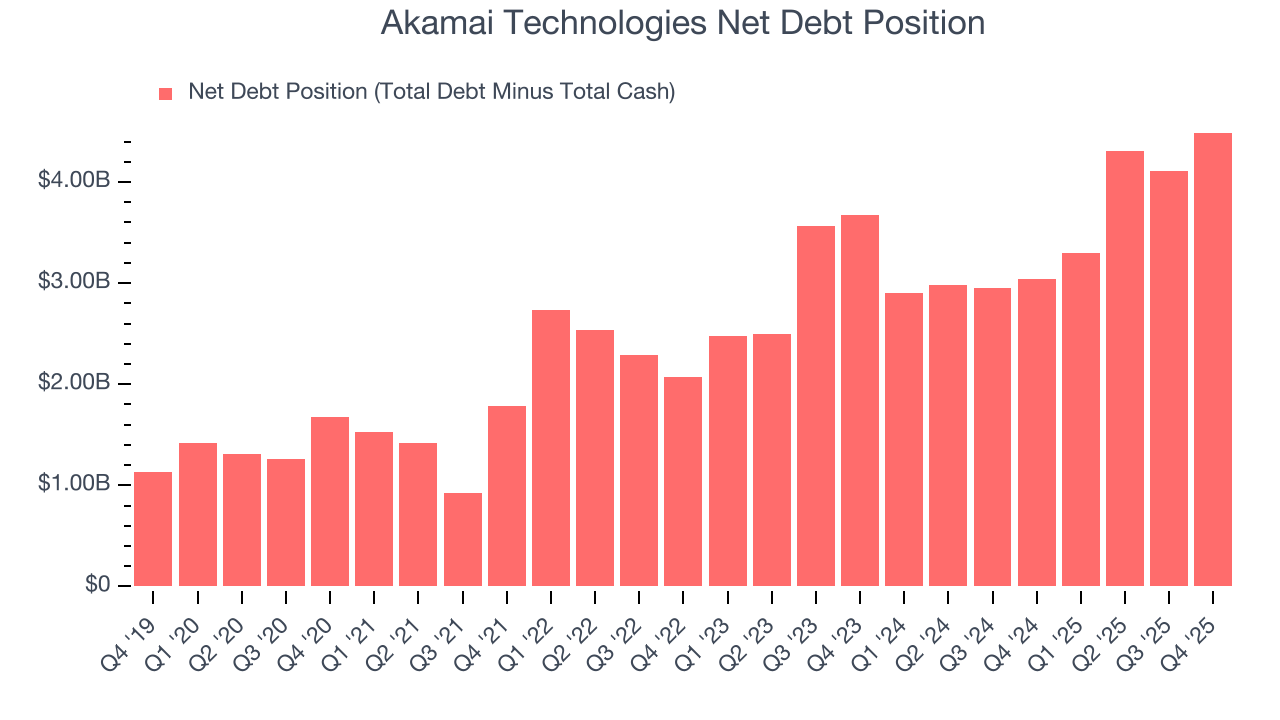

Akamai Technologies reported $1.19 billion of cash and $5.68 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $1.80 billion of EBITDA over the last 12 months, we view Akamai Technologies’s 2.5× net-debt-to-EBITDA ratio as safe. We also see its $19.32 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from Akamai Technologies’s Q4 Results

It was great to see Akamai Technologies expecting revenue growth to accelerate next year. We were also glad its full-year revenue guidance slightly exceeded Wall Street’s estimates. On the other hand, its full-year EPS guidance missed and its EPS guidance for next quarter fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 9% to $99.67 immediately following the results.

12. Is Now The Time To Buy Akamai Technologies?

Updated: March 16, 2026 at 10:03 PM EDT

Before investing in or passing on Akamai Technologies, we urge you to understand the company’s business quality (or lack thereof), valuation, and the latest quarterly results - in that order.

Akamai Technologies doesn’t pass our quality test. For starters, its revenue growth was weak over the last five years, and analysts don’t see anything changing over the next 12 months. While its strong operating margins show it’s a well-run business, the downside is its customer acquisition is less efficient than many comparable companies. On top of that, its gross margins show its business model is much less lucrative than other companies.

Akamai Technologies’s price-to-sales ratio based on the next 12 months is 3.5x. At this valuation, there’s a lot of good news priced in - we think other companies feature superior fundamentals at the moment.

Wall Street analysts have a consensus one-year price target of $109.46 on the company (compared to the current share price of $105.80).