Amplitude (AMPL)

We’re cautious of Amplitude. Its growth has decelerated and its failure to generate meaningful free cash flow makes us question its prospects.― StockStory Analyst Team

1. News

2. Summary

Why We Think Amplitude Will Underperform

Born from the realization that companies were flying blind when it came to understanding user behavior in their digital products, Amplitude (NASDAQ:AMPL) provides a digital analytics platform that helps businesses understand how people use their digital products to improve user experiences and drive revenue growth.

- Persistent operating margin losses suggest the business manages its expenses poorly

- Below-average net revenue retention rate of 102% suggests it has some trouble expanding within existing accounts

- One positive is that its impressive 27.3% annual revenue growth over the last five years indicates it’s winning market share

Amplitude’s quality doesn’t meet our expectations. Better businesses are for sale in the market.

Why There Are Better Opportunities Than Amplitude

At $7.44 per share, Amplitude trades at 2.5x forward price-to-sales. This sure is a cheap multiple, but you get what you pay for.

We’d rather pay up for companies with elite fundamentals than get a bargain on weak ones. Cheap stocks can be value traps, and as their performance deteriorates, they will stay cheap or get even cheaper.

3. Amplitude (AMPL) Research Report: Q4 CY2025 Update

Digital analytics platform Amplitude (NASDAQ:AMPL) beat Wall Street’s revenue expectations in Q4 CY2025, with sales up 17% year on year to $91.43 million. Guidance for next quarter’s revenue was better than expected at $92.7 million at the midpoint, 0.6% above analysts’ estimates. Its non-GAAP profit of $0.04 per share was in line with analysts’ consensus estimates.

Amplitude (AMPL) Q4 CY2025 Highlights:

- Revenue: $91.43 million vs analyst estimates of $90.35 million (17% year-on-year growth, 1.2% beat)

- Adjusted EPS: $0.04 vs analyst estimates of $0.05 (in line)

- Adjusted Operating Income: $4.18 million vs analyst estimates of $4.59 million (4.6% margin, relatively in line)

- Revenue Guidance for Q1 CY2026 is $92.7 million at the midpoint, roughly in line with what analysts were expecting

- Adjusted EPS guidance for the upcoming financial year 2026 is $0.11 at the midpoint, missing analyst estimates by 9.8%

- Operating Margin: -20.8%, up from -45.4% in the same quarter last year

- Free Cash Flow Margin: 12.2%, up from 3.8% in the previous quarter

- Customers: 4,700, up from 4,500 in the previous quarter

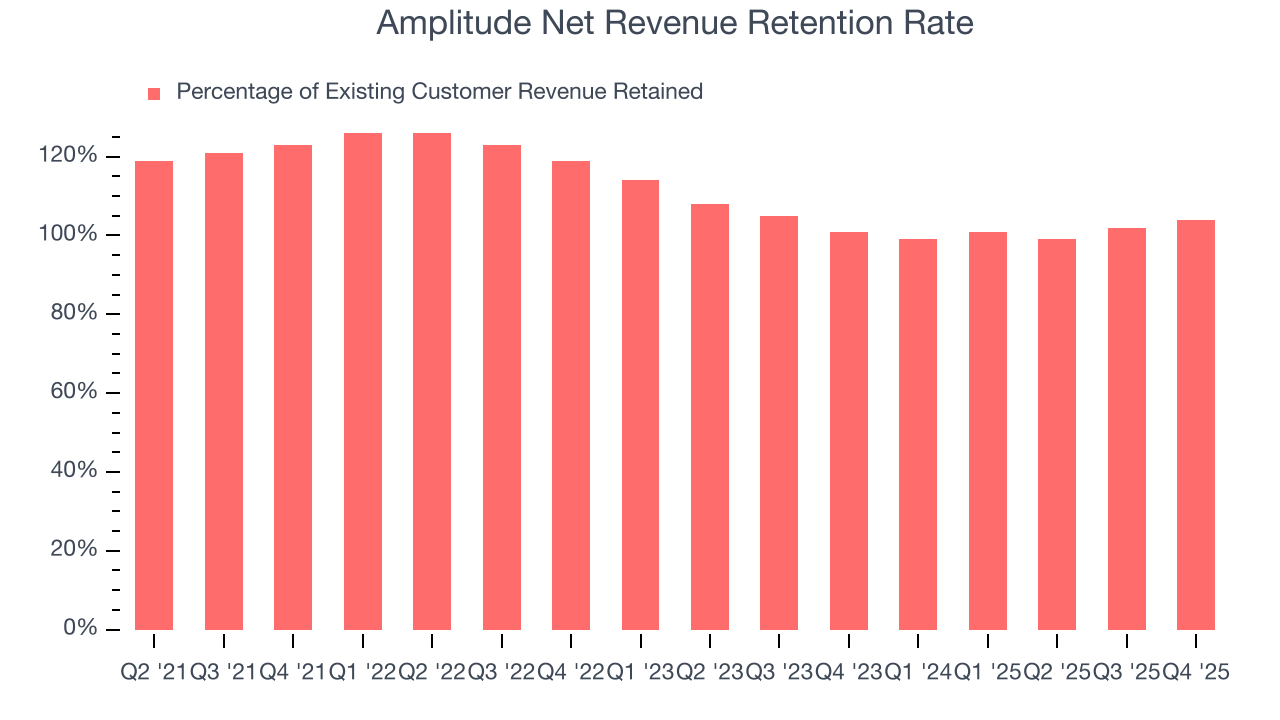

- Net Revenue Retention Rate: 104%, up from 102% in the previous quarter

- Annual Recurring Revenue: $366 million (17.3% year-on-year growth, beat)

- Market Capitalization: $847.6 million

Company Overview

Born from the realization that companies were flying blind when it came to understanding user behavior in their digital products, Amplitude (NASDAQ:AMPL) provides a digital analytics platform that helps businesses understand how people use their digital products to improve user experiences and drive revenue growth.

The Amplitude Digital Analytics Platform enables companies to collect, analyze, and act on customer behavioral data across websites, mobile apps, and other digital touchpoints. At the core of its technology is the Amplitude Behavioral Graph, a proprietary database specifically designed to process complex user interactions and identify patterns that lead to desired outcomes like conversions or retention.

The platform consists of several integrated components: Amplitude Analytics for understanding user behavior through quantitative and qualitative insights; Amplitude Experiment for testing new features; Amplitude CDP for managing customer data; and Session Replay for visualizing exactly how users interact with digital interfaces. Through these tools, teams can identify which user actions predict purchasing behavior, why customers abandon processes, and which pathways lead to successful outcomes.

A typical customer might use Amplitude to discover that users who complete a specific sequence of actions (like watching a tutorial video followed by creating a project) are significantly more likely to convert to paid subscribers. The product team could then redesign the onboarding flow to encourage this behavior pattern.

Amplitude operates on a subscription-based software-as-a-service (SaaS) model, serving over 2,700 customers across industries ranging from finance and retail to healthcare and telecommunications. Its platform is designed for cross-functional use, enabling product managers, marketers, engineers, analysts, and executives to work from a shared understanding of user behavior.

4. Data Analytics

Organizations generate a lot of data that is stored in silos, often in incompatible formats, making it slow and costly to extract actionable insights, which in turn drives demand for modern cloud-based data analysis platforms that can efficiently analyze the siloed data.

Amplitude competes with product analytics solutions like Pendo, Mixpanel, and Heap, as well as larger players including Adobe Experience Cloud and Google Analytics. In the experimentation space, it faces competition from Optimizely and LaunchDarkly, while in the customer data platform category, it competes with mParticle and Twilio Segment.

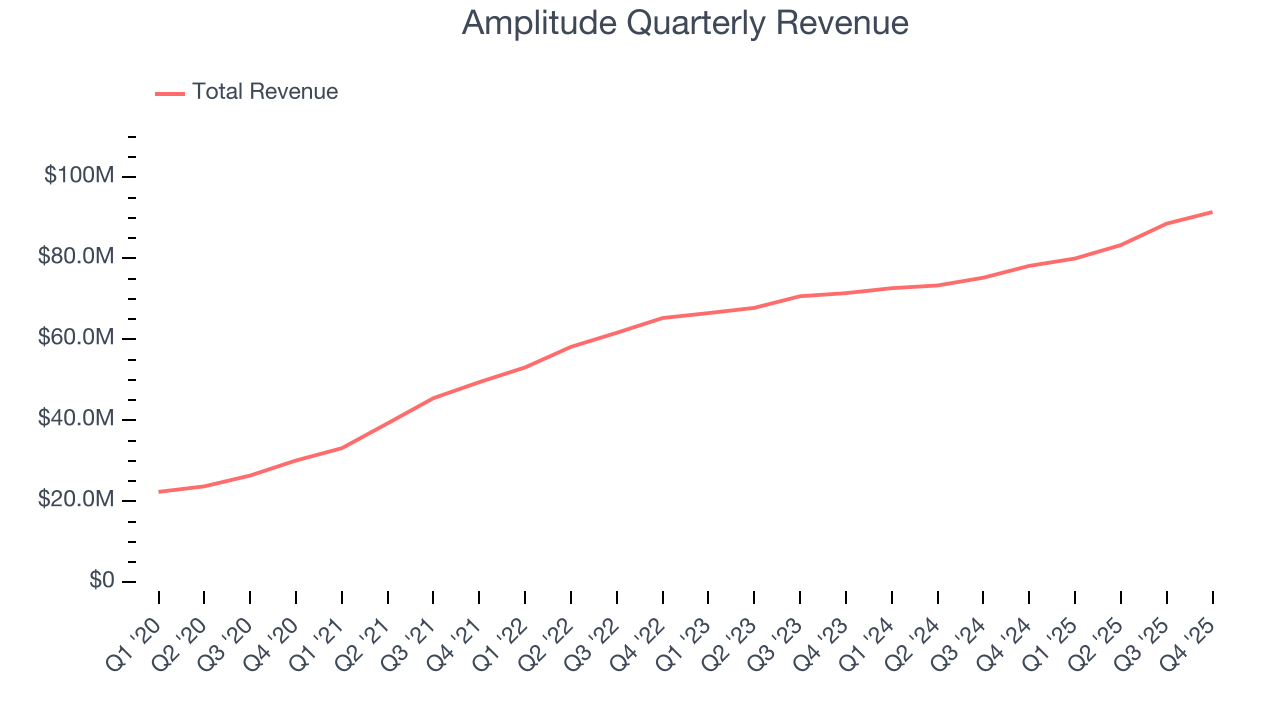

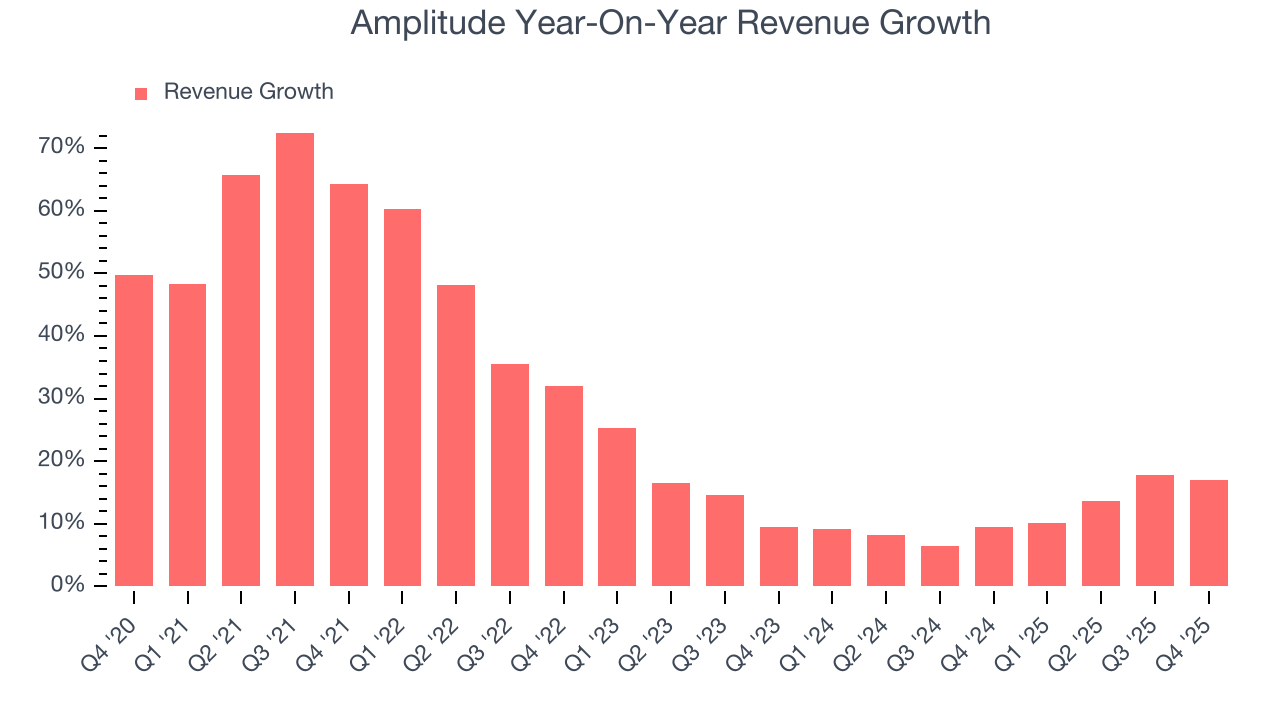

5. Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Thankfully, Amplitude’s 27.3% annualized revenue growth over the last five years was impressive. Its growth beat the average software company and shows its offerings resonate with customers.

Long-term growth is the most important, but within software, a half-decade historical view may miss new innovations or demand cycles. Amplitude’s recent performance shows its demand has slowed significantly as its annualized revenue growth of 11.5% over the last two years was well below its five-year trend.

This quarter, Amplitude reported year-on-year revenue growth of 17%, and its $91.43 million of revenue exceeded Wall Street’s estimates by 1.2%. Company management is currently guiding for a 15.9% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 13.7% over the next 12 months. While this projection implies its newer products and services will catalyze better top-line performance, it is still below average for the sector.

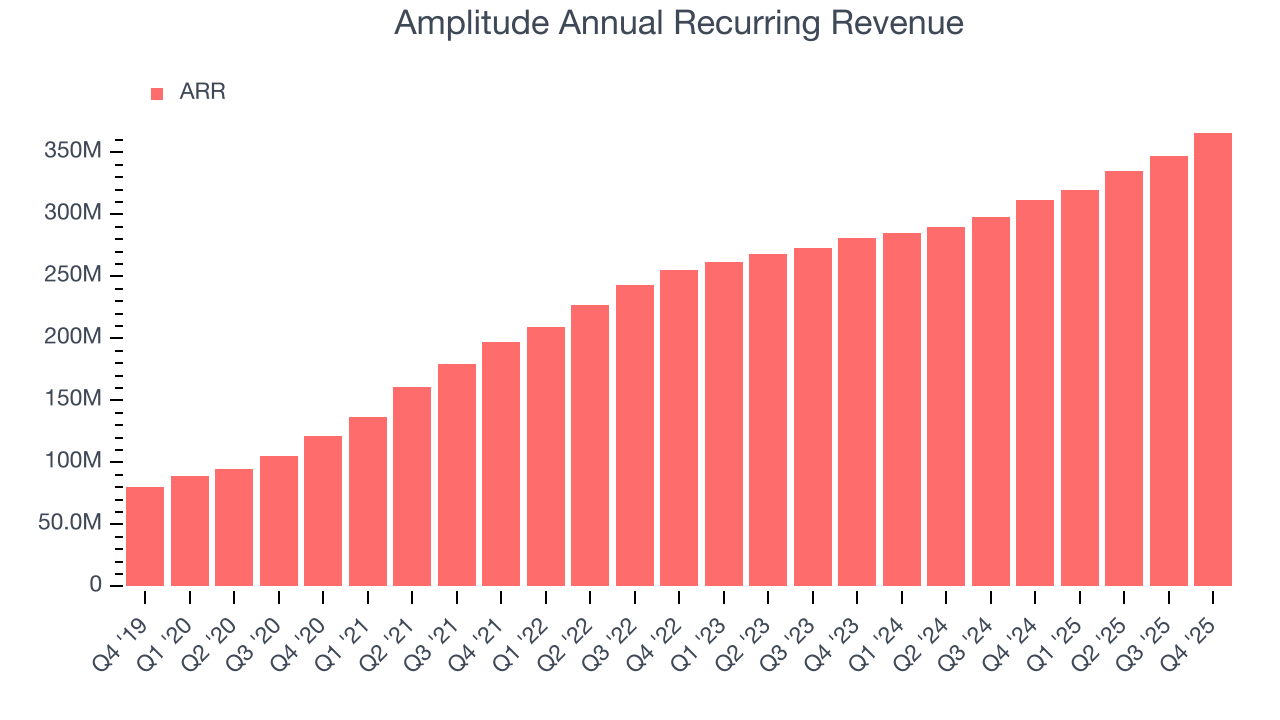

6. Annual Recurring Revenue

While reported revenue for a software company can include low-margin items like implementation fees, annual recurring revenue (ARR) is a sum of the next 12 months of contracted revenue purely from software subscriptions, or the high-margin, predictable revenue streams that make SaaS businesses so valuable.

Amplitude’s ARR punched in at $366 million in Q4, and over the last four quarters, its growth slightly outpaced the sector as it averaged 15.4% year-on-year increases. This performance aligned with its total sales growth and shows the company is securing longer-term commitments. Its growth also contributes positively to Amplitude’s revenue predictability, a trait long-term investors typically prefer.

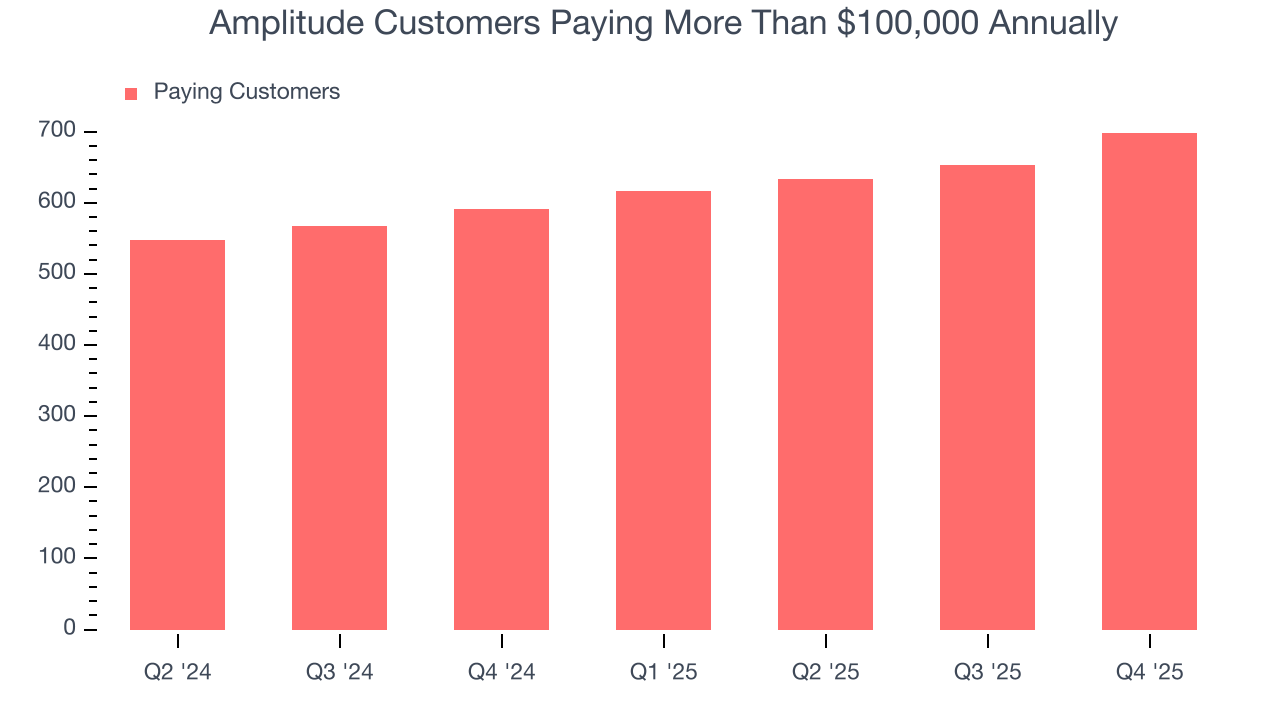

7. Enterprise Customer Base

This quarter, Amplitude reported 698 enterprise customers paying more than $100,000 annually, an increase of 45 from the previous quarter. That’s quite a bit more contract wins than last quarter and quite a bit above what we’ve observed over the previous year. Shareholders should take this as an indication that Amplitude’s go-to-market strategy is working well.

8. Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

It’s relatively expensive for Amplitude to acquire new customers as its CAC payback period checked in at 63.1 months this quarter. The company’s drawn-out sales cycles partly stem from its focus on enterprise clients who require some degree of customization, resulting in long onboarding periods that delay delay returns and limit customer growth.

9. Customer Retention

One of the best parts about the software-as-a-service business model (and a reason why they trade at high valuation multiples) is that customers typically spend more on a company’s products and services over time.

Amplitude’s net revenue retention rate, a key performance metric measuring how much money existing customers from a year ago are spending today, was 102% in Q4. This means Amplitude would’ve grown its revenue by 1.5% even if it didn’t win any new customers over the last 12 months.

Amplitude has an adequate net retention rate, showing us that it generally keeps customers but lags behind the best SaaS businesses, which routinely post net retention rates of 120%+.

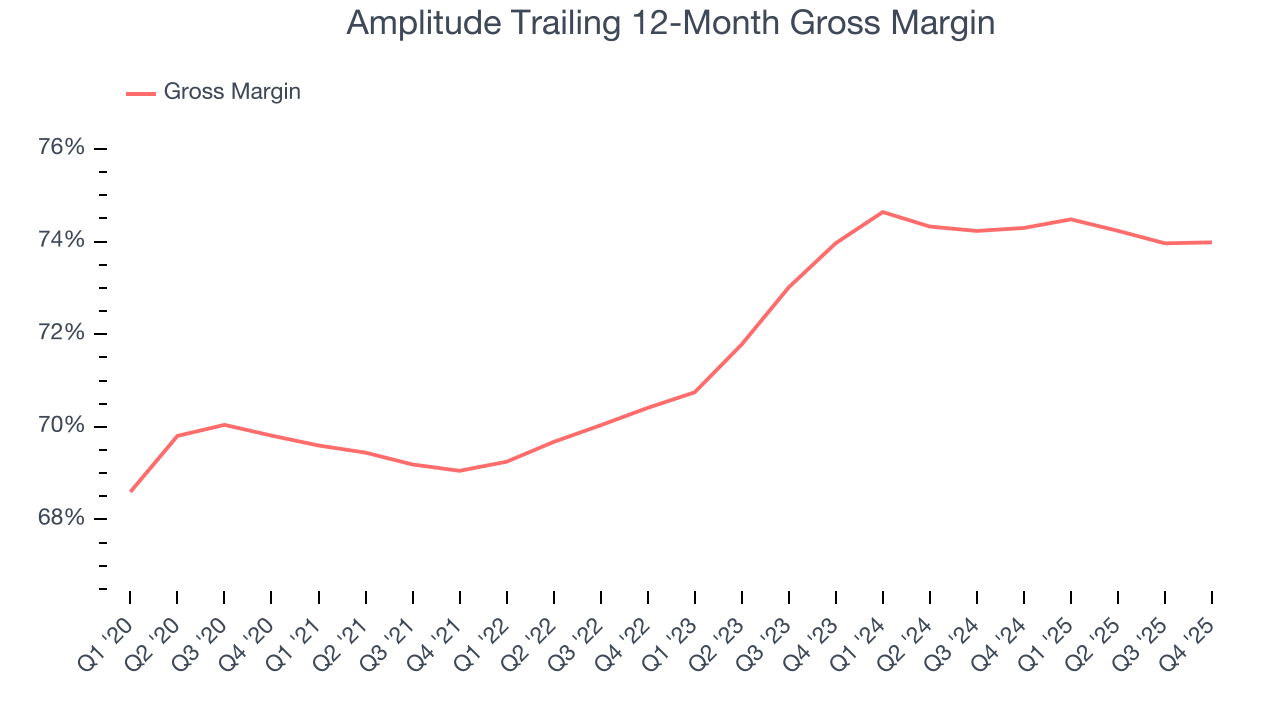

10. Gross Margin & Pricing Power

For software companies like Amplitude, gross profit tells us how much money remains after paying for the base cost of products and services (typically servers, licenses, and certain personnel). These costs are usually low as a percentage of revenue, explaining why software is more lucrative than other sectors.

Amplitude’s gross margin is better than the broader software industry and signals it has solid unit economics and competitive products. As you can see below, it averaged a decent 74% gross margin over the last year. That means for every $100 in revenue, roughly $73.99 was left to spend on selling, marketing, and R&D.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. Amplitude has seen gross margins improve by 0 percentage points over the last 2 year, which is slightly better than average for software.

Amplitude’s gross profit margin came in at 74.6% this quarter, in line with the same quarter last year. On a wider time horizon, the company’s full-year margin has remained steady over the past four quarters, suggesting its input costs have been stable and it isn’t under pressure to lower prices.

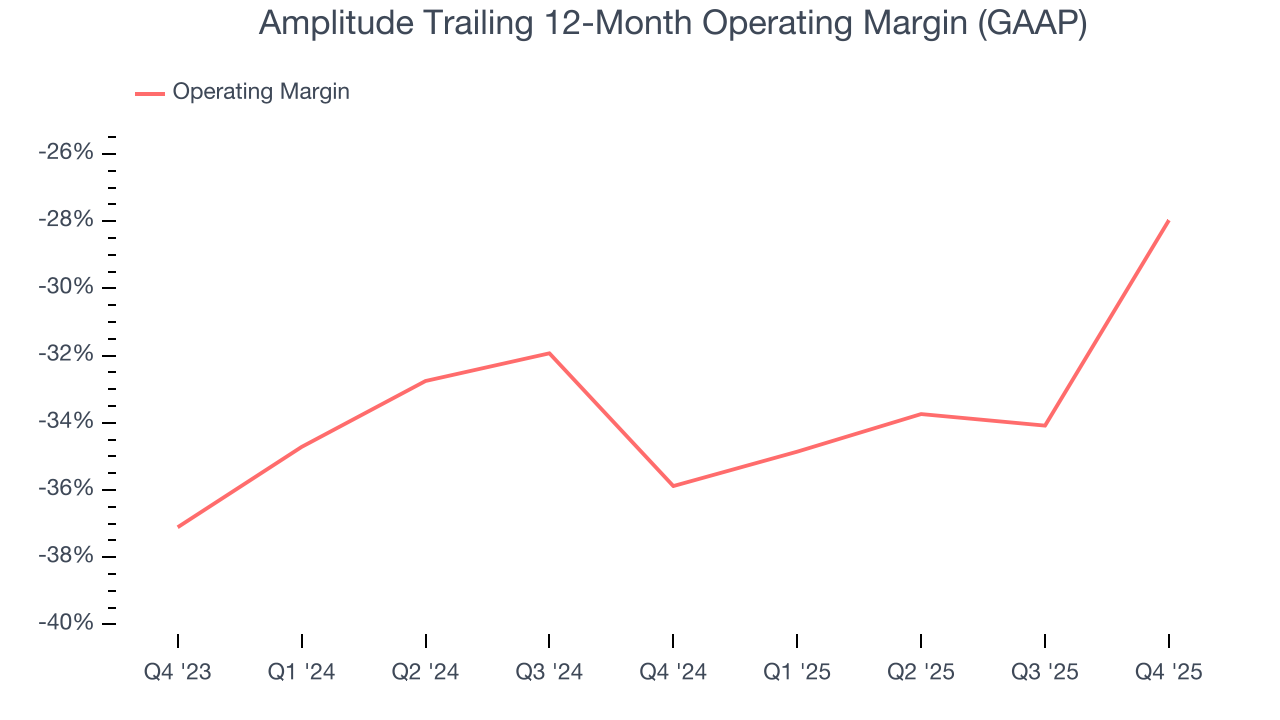

11. Operating Margin

Amplitude’s expensive cost structure has contributed to an average operating margin of negative 28% over the last year. Unprofitable, high-growth software companies require extra attention because they spend heaps of money to capture market share. As seen in its fast historical revenue growth, this strategy seems to have worked so far, but it’s unclear what would happen if Amplitude reeled back its investments. Wall Street seems to think it will face some obstacles, and we tend to agree.

Over the last two years, Amplitude’s expanding sales gave it operating leverage as its margin rose by 7.9 percentage points. Still, it will take much more for the company to reach long-term profitability.

Amplitude’s operating margin was negative 20.8% this quarter.

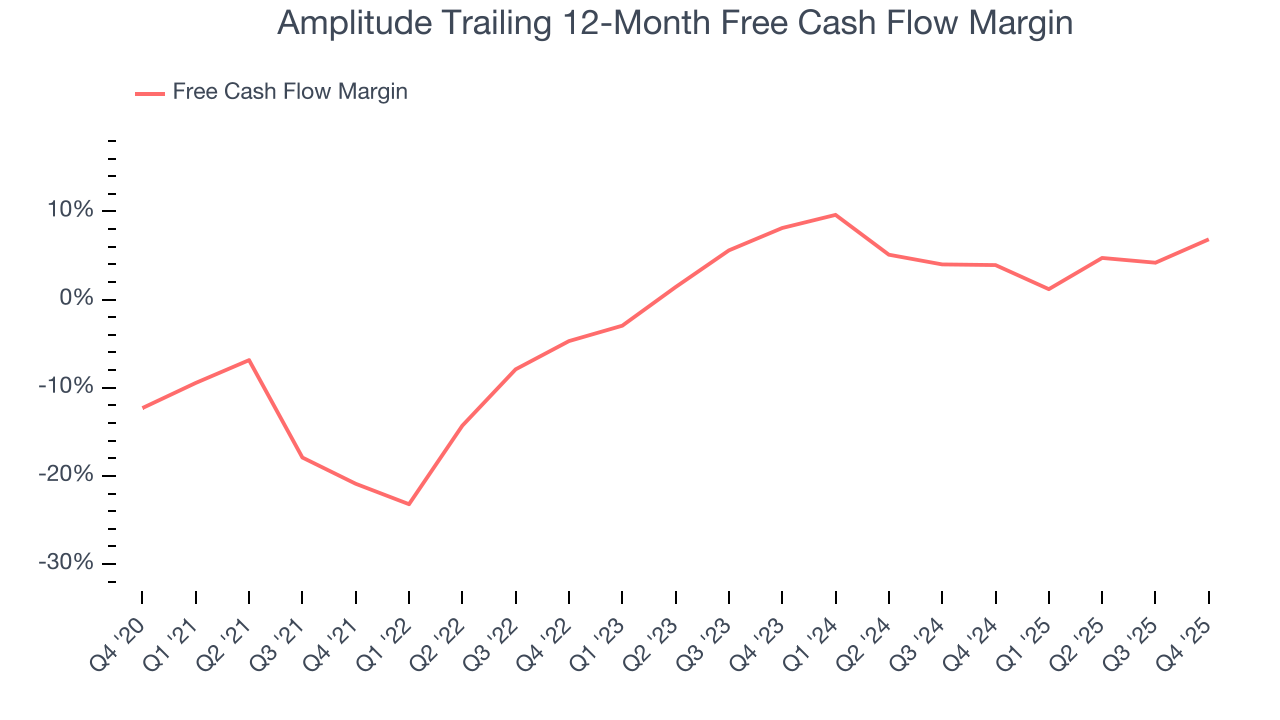

12. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Amplitude has shown weak cash profitability over the last year, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 6.8%, subpar for a software business.

Amplitude’s free cash flow clocked in at $11.18 million in Q4, equivalent to a 12.2% margin. This result was good as its margin was 10.3 percentage points higher than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, leading to temporary swings. Long-term trends are more important.

Over the next year, analysts’ consensus estimates show they’re expecting Amplitude’s free cash flow margin of 6.8% for the last 12 months to remain the same.

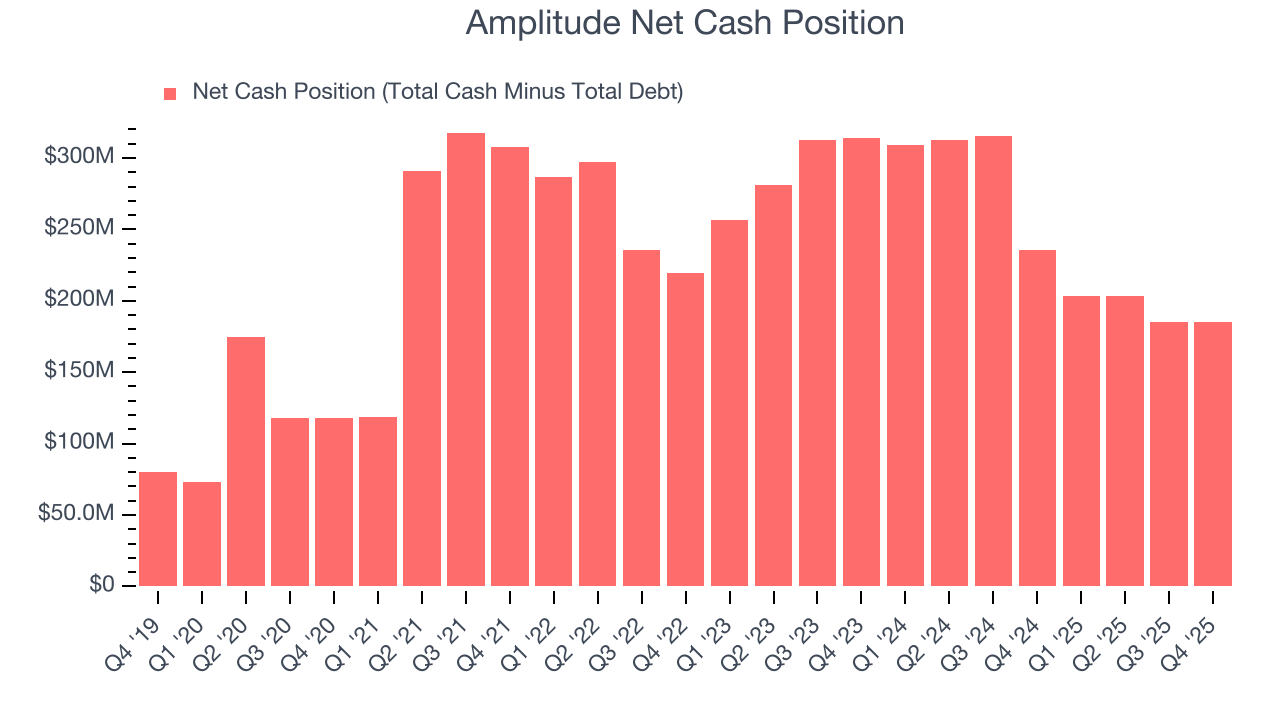

13. Balance Sheet Assessment

One of the best ways to mitigate bankruptcy risk is to hold more cash than debt.

Amplitude is a well-capitalized company with $192 million of cash and $6.88 million of debt on its balance sheet. This $185.1 million net cash position is 19.3% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

14. Key Takeaways from Amplitude’s Q4 Results

It was good to see Amplitude expecting revenue growth to continue next year. We were also glad its net revenue retention grew. On the other hand, its full-year EPS guidance missed and its EPS guidance for next quarter fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded up 2.7% to $7.37 immediately after reporting.

15. Is Now The Time To Buy Amplitude?

Updated: March 15, 2026 at 10:20 PM EDT

When considering an investment in Amplitude, investors should account for its valuation and business qualities as well as what’s happened in the latest quarter.

Amplitude isn’t a terrible business, but it doesn’t pass our bar. Although its revenue growth was strong over the last five years, it’s expected to deteriorate over the next 12 months and its operating margins reveal poor profitability compared to other software companies. And while the company’s gross margin suggests it can generate sustainable profits, the downside is its customers generally do not adopt its complementary products.

Amplitude’s price-to-sales ratio based on the next 12 months is 2.5x. While this valuation is reasonable, we don’t really see a big opportunity at the moment. We're fairly confident there are better investments elsewhere.

Wall Street analysts have a consensus one-year price target of $12.70 on the company (compared to the current share price of $7.44).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.