American Superconductor (AMSC)

We admire American Superconductor. Its rapid revenue growth gives it operating leverage, making it more profitable as it expands.― StockStory Analyst Team

1. News

2. Summary

Why We Like American Superconductor

Founded in 1987, American Superconductor (NASDAQ:AMSC) has shifted from superconductor research to developing power systems, adapting to changing energy grid needs and naval technology requirements.

- Impressive 27.1% annual revenue growth over the last five years indicates it’s winning market share this cycle

- Incremental sales significantly boosted profitability as its annual earnings per share growth of 49.7% over the last five years outstripped its revenue performance

- Expected revenue growth of 22.2% for the next year suggests its market share will rise

American Superconductor is a market leader. Any surprise this is one of our favorite stocks?

Is Now The Time To Buy American Superconductor?

American Superconductor’s stock price of $33.53 implies a valuation ratio of 34.5x forward P/E. There are high expectations given this pricey multiple; we can’t deny that.

Do you like the business model and believe in the company’s future? If so, you can own a smaller position, as our work shows that high-quality companies outperform the market over a multi-year period regardless of valuation at entry.

3. American Superconductor (AMSC) Research Report: Q4 CY2025 Update

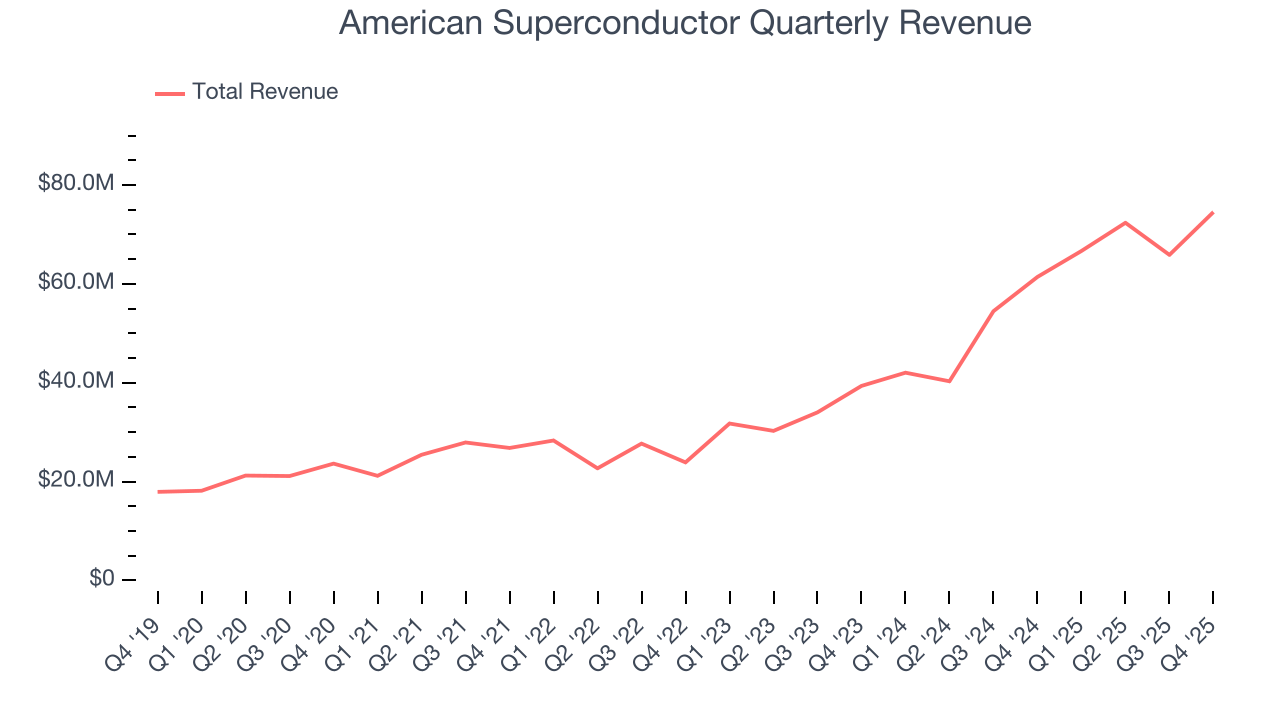

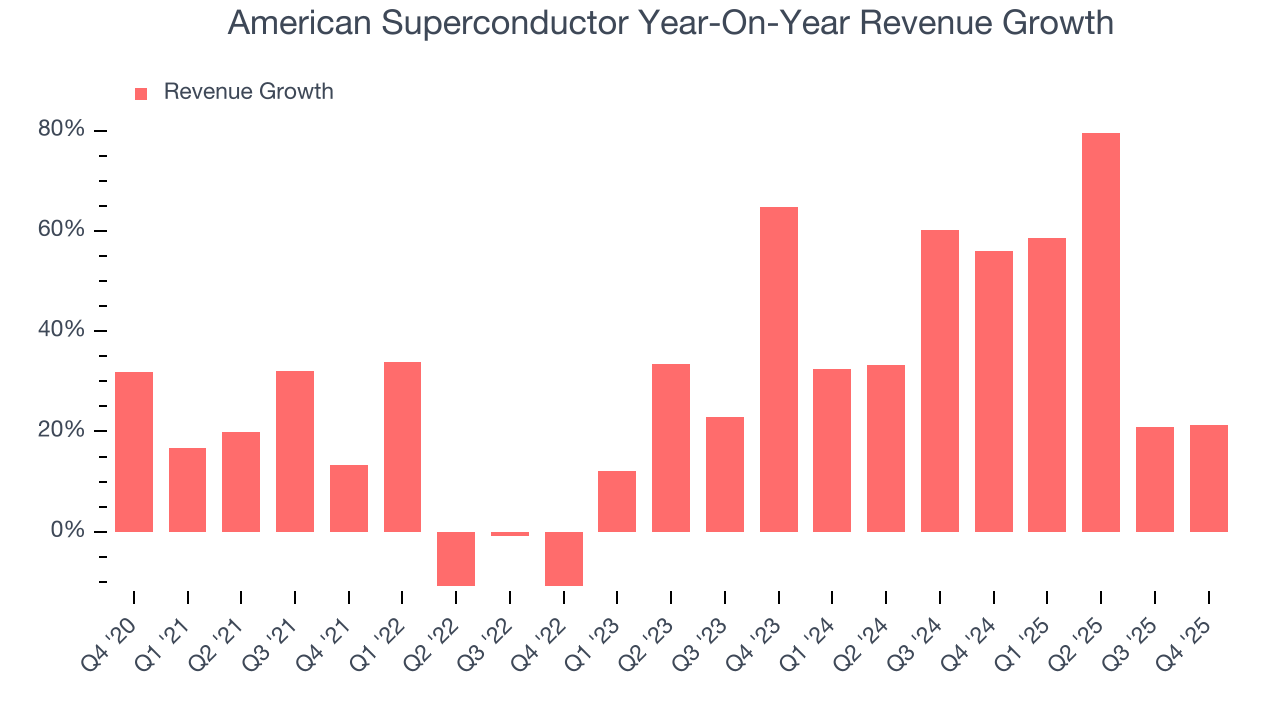

Power resiliency solutions provider American Superconductor (NASDAQ:AMSC) beat Wall Street’s revenue expectations in Q4 CY2025, with sales up 21.4% year on year to $74.53 million. On the other hand, next quarter’s revenue guidance of $80 million was less impressive, coming in 1.8% below analysts’ estimates. Its non-GAAP profit of $2.75 per share was significantly above analysts’ consensus estimates.

American Superconductor (AMSC) Q4 CY2025 Highlights:

- Revenue: $74.53 million vs analyst estimates of $69.03 million (21.4% year-on-year growth, 8% beat)

- Adjusted EPS: $2.75 vs analyst estimates of $0.15 (significant beat)

- Adjusted EBITDA: $5.02 million vs analyst estimates of $3.2 million (6.7% margin, 56.8% beat)

- Revenue Guidance for Q1 CY2026 is $80 million at the midpoint, below analyst estimates of $81.5 million

- Adjusted EPS guidance for Q1 CY2026 is $0.17 at the midpoint, below analyst estimates of $0.20

- Operating Margin: 4.5%, up from 2.8% in the same quarter last year

- Free Cash Flow Margin: 3.2%, down from 8.7% in the same quarter last year

- Market Capitalization: $1.36 billion

Company Overview

Founded in 1987, American Superconductor (NASDAQ:AMSC) has shifted from superconductor research to developing power systems, adapting to changing energy grid needs and naval technology requirements.

Founded in 1987, AMSC has been developing and implementing advanced technologies that enhance the reliability, efficiency, and security of power systems. The company's core focus is on creating solutions of power on the grid while also protecting and expanding the capabilities of the U.S. Navy's fleet.

AMSC's business is built around two primary segments: Grid and Wind. The Grid segment offers solutions designed to improve the reliability, security, and capacity of electrical power infrastructure. These include D-VAR systems for voltage control, REG (Resilient Electric Grid) systems for urban power grids, and VVO (Volt VAR Optimization) systems for distribution networks. The company's solutions address challenges faced by power grid operators, such as integrating renewable energy sources, managing power quality, and enhancing grid resilience against natural disasters and cyber threats.

In the marine sector, AMSC provides advanced ship protection systems to the U.S. Navy. The company's degaussing systems, which reduce a naval ship's magnetic signature, offer advantages over traditional copper-based systems in terms of weight reduction and energy efficiency.

The Wind segment of AMSC focuses on providing electrical control systems and engineering services to wind turbine manufacturers. The company designs and licenses wind turbine systems, offering a comprehensive approach that includes turbine design, customer support, and the supply of critical components such as electrical control systems.

4. Renewable Energy

Renewable energy companies are buoyed by the secular trend of green energy that is upending traditional power generation. Those who innovate and evolve with this dynamic market can win share while those who continue to rely on legacy technologies can see diminishing demand, which includes headwinds from increasing regulation against “dirty” energy. Additionally, these companies are at the whim of economic cycles, as interest rates can impact the willingness to invest in renewable energy projects.

Competitors of American Superconductor Corporation (NASDAQ: AMSC) include ABB Ltd. (NYSE: ABB), Siemens AG (OTC: SIEGY), and General Electric Company (NYSE: GE).

5. Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Thankfully, American Superconductor’s 27.1% annualized revenue growth over the last five years was incredible. Its growth surpassed the average industrials company and shows its offerings resonate with customers, a great starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. American Superconductor’s annualized revenue growth of 43.7% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

This quarter, American Superconductor reported robust year-on-year revenue growth of 21.4%, and its $74.53 million of revenue topped Wall Street estimates by 8%. Company management is currently guiding for a 20% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 24.8% over the next 12 months, a deceleration versus the last two years. Still, this projection is commendable and indicates the market is forecasting success for its products and services.

6. Gross Margin & Pricing Power

At StockStory, we prefer high gross margin businesses because they indicate the company has pricing power or differentiated products, giving it a chance to generate higher operating profits.

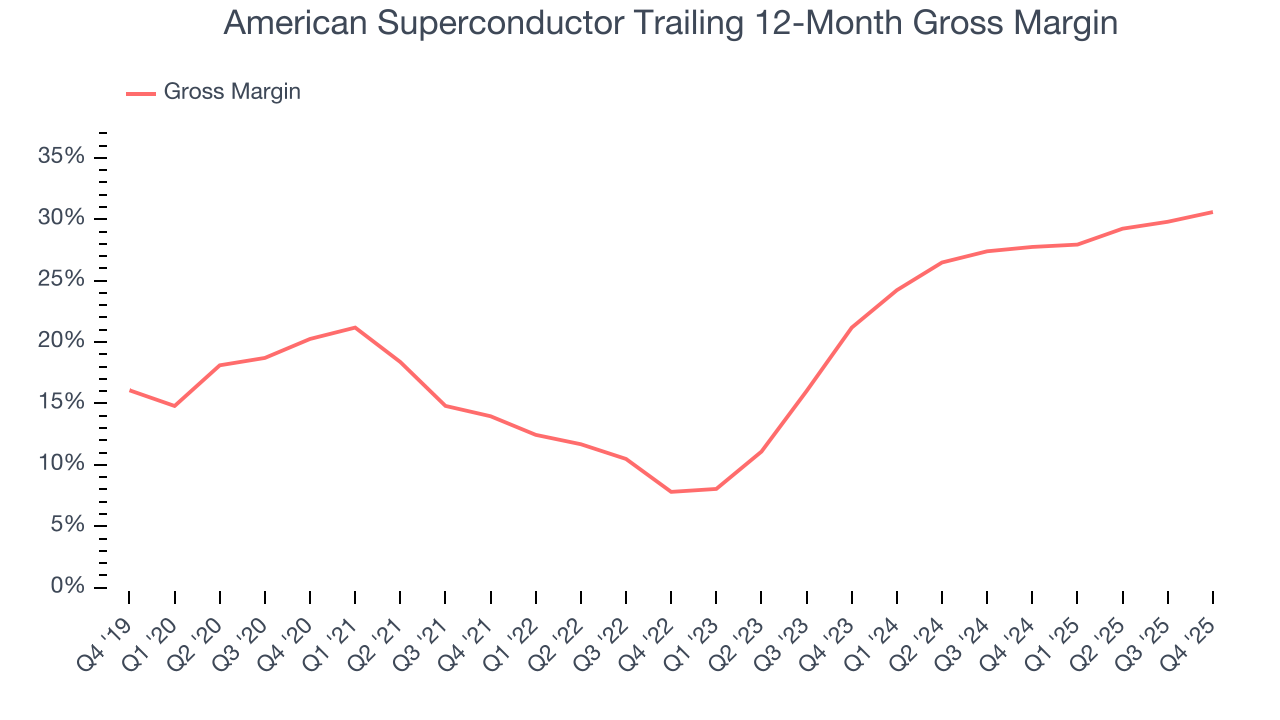

American Superconductor has bad unit economics for an industrials company, giving it less room to reinvest and develop new offerings. As you can see below, it averaged a 23.4% gross margin over the last five years. Said differently, American Superconductor had to pay a chunky $76.58 to its suppliers for every $100 in revenue.

This quarter, American Superconductor’s gross profit margin was 30.7%, up 3.4 percentage points year on year. American Superconductor’s full-year margin has also been trending up over the past 12 months, increasing by 2.8 percentage points. If this move continues, it could suggest better unit economics due to more leverage from its growing sales on the fixed portion of its cost of goods sold (such as manufacturing expenses).

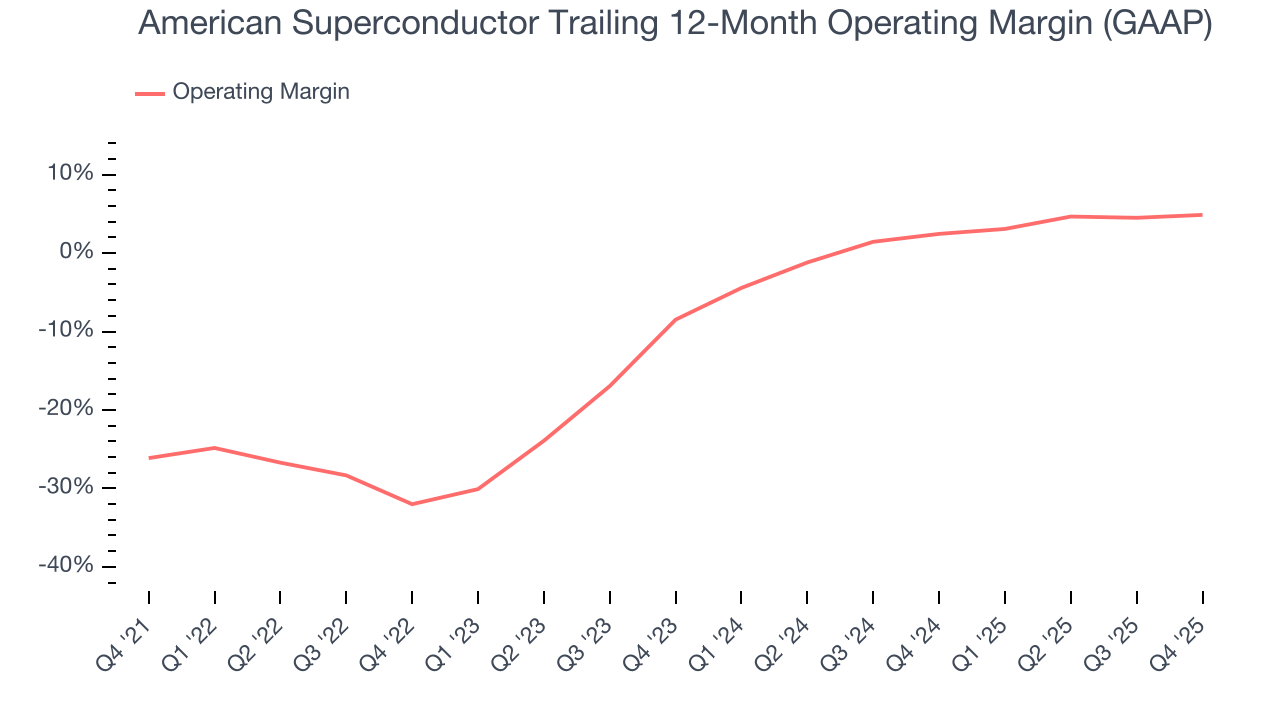

7. Operating Margin

Although American Superconductor was profitable this quarter from an operational perspective, it’s generally struggled over a longer time period. Its expensive cost structure has contributed to an average operating margin of negative 6.4% over the last five years. Unprofitable industrials companies require extra attention because they could get caught swimming naked when the tide goes out.

On the plus side, American Superconductor’s operating margin rose by 31 percentage points over the last five years, as its sales growth gave it operating leverage. Still, it will take much more for the company to show consistent profitability.

In Q4, American Superconductor generated an operating margin profit margin of 4.5%, up 1.7 percentage points year on year. Since its gross margin expanded more than its operating margin, we can infer that leverage on its cost of sales was the primary driver behind the recently higher efficiency.

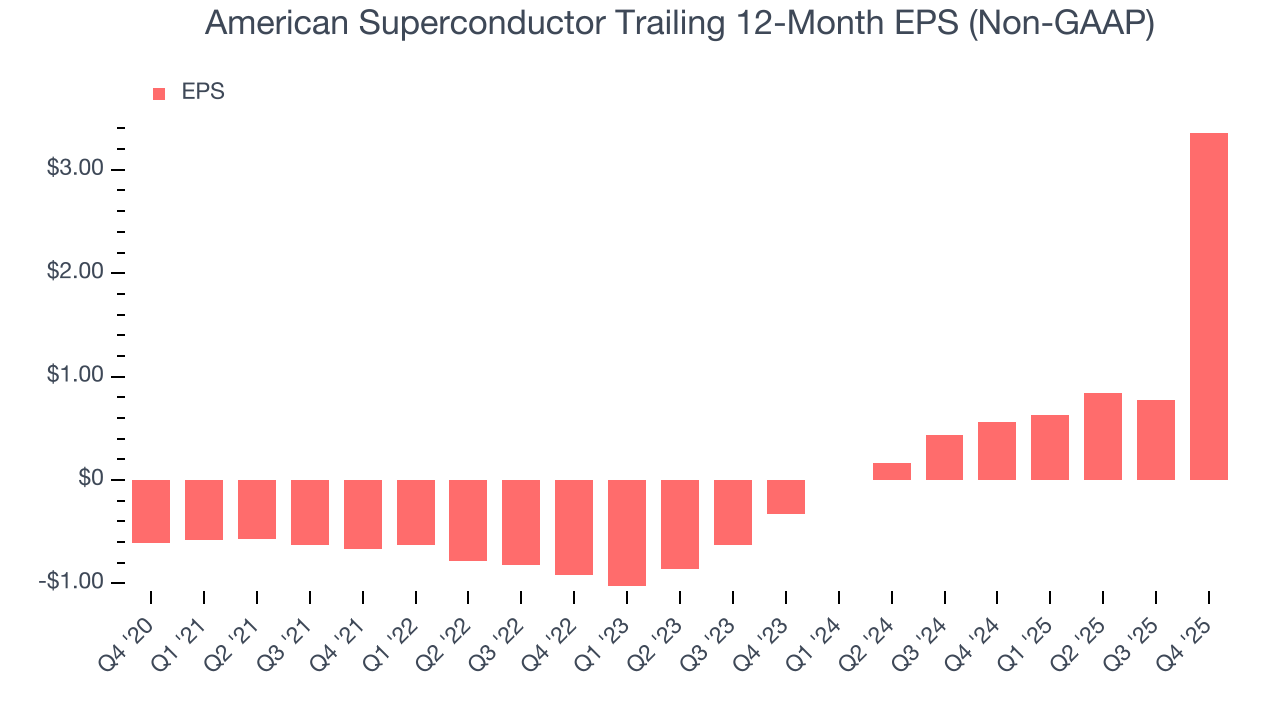

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

American Superconductor’s full-year EPS flipped from negative to positive over the last five years. This is a good sign and shows it’s at an inflection point.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For American Superconductor, its two-year annual EPS growth of 249% was higher than its five-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.

In Q4, American Superconductor reported adjusted EPS of $2.75, up from $0.16 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects American Superconductor’s full-year EPS of $3.36 to shrink by 70.3%.

9. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

While American Superconductor posted positive free cash flow this quarter, the broader story hasn’t been so clean. American Superconductor’s demanding reinvestments have drained its resources over the last five years, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 1.2%, meaning it lit $1.20 of cash on fire for every $100 in revenue.

Taking a step back, an encouraging sign is that American Superconductor’s margin expanded by 26.1 percentage points during that time. The company’s improvement and free cash flow generation this quarter show it’s heading in the right direction, and continued increases could help it achieve long-term cash profitability.

American Superconductor’s free cash flow clocked in at $2.36 million in Q4, equivalent to a 3.2% margin. The company’s cash profitability regressed as it was 5.6 percentage points lower than in the same quarter last year, but it’s still above its five-year average. We wouldn’t read too much into this quarter’s decline because capital expenditures can be seasonal and companies often stockpile inventory in anticipation of higher demand, causing short-term swings. Long-term trends are more important.

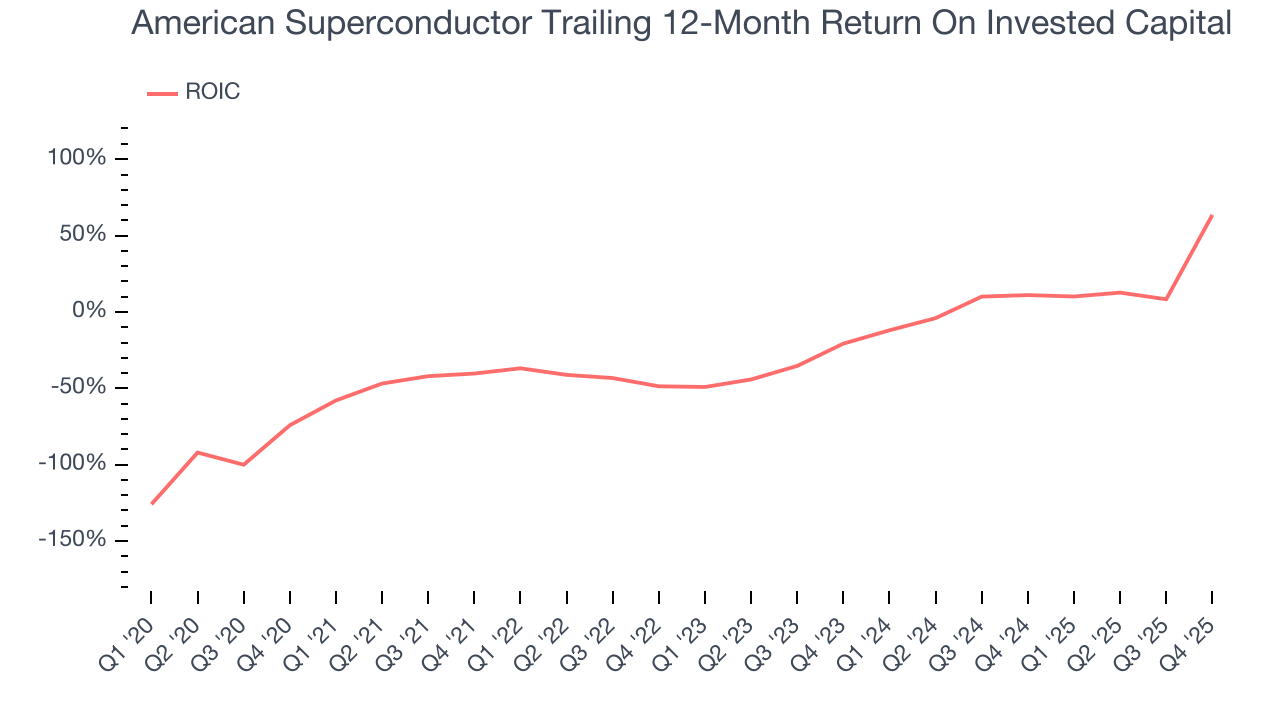

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Although American Superconductor has shown solid business quality lately, it struggled to grow profitably in the past. Its five-year average ROIC was negative 7%, meaning management lost money while trying to expand the business.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, American Superconductor’s ROIC has increased. This is a good sign, but we recognize its lack of profitable growth during the COVID era was the primary reason for the change.

11. Balance Sheet Assessment

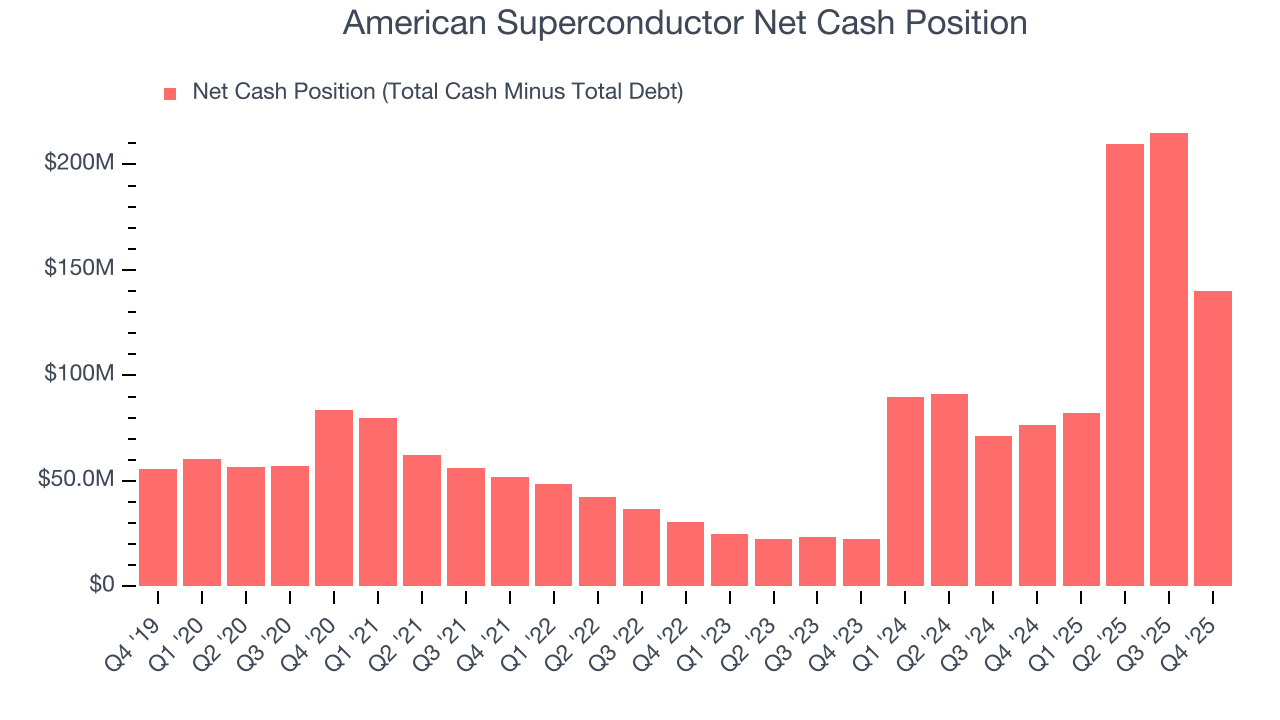

One of the best ways to mitigate bankruptcy risk is to hold more cash than debt.

American Superconductor is a profitable, well-capitalized company with $143.8 million of cash and $3.64 million of debt on its balance sheet. This $140.2 million net cash position is 10.3% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

12. Key Takeaways from American Superconductor’s Q4 Results

It was good to see American Superconductor beat analysts’ EPS expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. On the other hand, its EPS guidance for next quarter missed and its revenue guidance for next quarter fell short of Wall Street’s estimates. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 19.7% to $32.96 immediately after reporting.

13. Is Now The Time To Buy American Superconductor?

Updated: March 25, 2026 at 11:33 PM EDT

A common mistake we notice when investors are deciding whether to buy a stock or not is that they simply look at the latest earnings results. Business quality and valuation matter more, so we urge you to understand these dynamics as well.

American Superconductor is an amazing business ranking highly on our list. For starters, its revenue growth was exceptional over the last five years. And while its relatively low ROIC suggests management has struggled to find compelling investment opportunities, its rising cash profitability gives it more optionality. On top of that, American Superconductor’s expanding operating margin shows the business has become more efficient.

American Superconductor’s P/E ratio based on the next 12 months is 34.5x. There’s some optimism reflected in this multiple, but we don’t mind owning a high-quality business, even if it’s slightly expensive. It’s often wise to hold investments like this for at least three to five years, as the power of long-term compounding negates short-term price swings that can accompany relatively high valuations.

Wall Street analysts have a consensus one-year price target of $52.33 on the company (compared to the current share price of $33.53).