Angi (ANGI)

Angi doesn’t excite us. Its declining sales show demand has evaporated, a red flag for investors seeking high-quality stocks.― StockStory Analyst Team

1. News

2. Summary

Why Angi Is Not Exciting

Created by IAC’s mergers of Angie’s List and HomeAdvisor, ANGI (NASDAQ: ANGI) operates the largest online marketplace for home services in the US.

- Annual revenue declines of 17.9% over the last three years indicate problems with its market positioning

- Engagement has been a thorn in its side as its service requests averaged 21.3% declines

- A consolation is that its platform is difficult to replicate at scale and leads to a best-in-class gross margin of 95.3%

Angi doesn’t meet our quality standards. There are more rewarding stocks elsewhere.

Why There Are Better Opportunities Than Angi

At $7.56 per share, Angi trades at 3.5x forward EV/EBITDA. This sure is a cheap multiple, but you get what you pay for.

We’d rather pay up for companies with elite fundamentals than get a bargain on weak ones. Cheap stocks can be value traps, and as their performance deteriorates, they will stay cheap or get even cheaper.

3. Angi (ANGI) Research Report: Q4 CY2025 Update

Home services online marketplace ANGI (NASDAQ: ANGI) fell short of the market’s revenue expectations in Q4 CY2025, with sales falling 10.1% year on year to $240.8 million. Its GAAP profit of $0.17 per share was 50.2% below analysts’ consensus estimates.

Angi (ANGI) Q4 CY2025 Highlights:

- Revenue: $240.8 million vs analyst estimates of $243.7 million (10.1% year-on-year decline, 1.2% miss)

- EPS (GAAP): $0.17 vs analyst expectations of $0.34 (50.2% miss)

- Adjusted EBITDA: $39.7 million vs analyst estimates of $40.05 million (16.5% margin, 0.9% miss)

- Operating Margin: 2.5%, up from 0.8% in the same quarter last year

- Free Cash Flow Margin: 4.7%, up from 1.9% in the previous quarter

- Market Capitalization: $504.4 million

Company Overview

Created by IAC’s mergers of Angie’s List and HomeAdvisor, ANGI (NASDAQ: ANGI) operates the largest online marketplace for home services in the US.

Angi is an online marketplace focused on the large and very fragmented home services market. The marketplace seeks to match consumers' service requests with service professionals for a variety of home projects – everything from hanging a television to redoing a kitchen. Customers have the option to ask for a bid for a project or choose from a fixed price for a service, with the latter option the increasing focus for the business as consumers prefer the quicker time to service and lack of negotiation, while service providers who respond get assured revenue, rather than a negotiation or a fruitless waste of their advertising dollars.

For US homeowners who are generally faced with 6-10 household jobs per year, from replacing a dishwasher or boiler to wiring a new home entertainment system, Angi provides an aggregated collection of peer reviewed certified local service providers. For the service providers, Angi is another customer acquisition tool, where they can set defined budgets and measure how much business is coming in.

Many companies have tried their hand at building online marketplaces for home services but have struggled to match supply and demand; Angi is by far the largest platform in the US.

4. Gig Economy

The iPhone changed the world, ushering in the era of the “always-on” internet and “on-demand” services - anything someone could want is just a few taps away. Likewise, the gig economy sprang up in a similar fashion, with a proliferation of tech-enabled freelance labor marketplaces, which work hand and hand with many on demand services. Individuals can now work on demand too. What began with tech-enabled platforms that aggregated riders and drivers has expanded over the past decade to include food delivery, groceries, and now even a plumber or graphic designer are all just a few taps away.

Angi (NASDAQ: ANGI) competitors include Thumbtack, Houzz, Meta Platforms (NASDAQ:FB), Yelp (NYSE: YELP), and Porch Group (NASDAQ: PRCH)

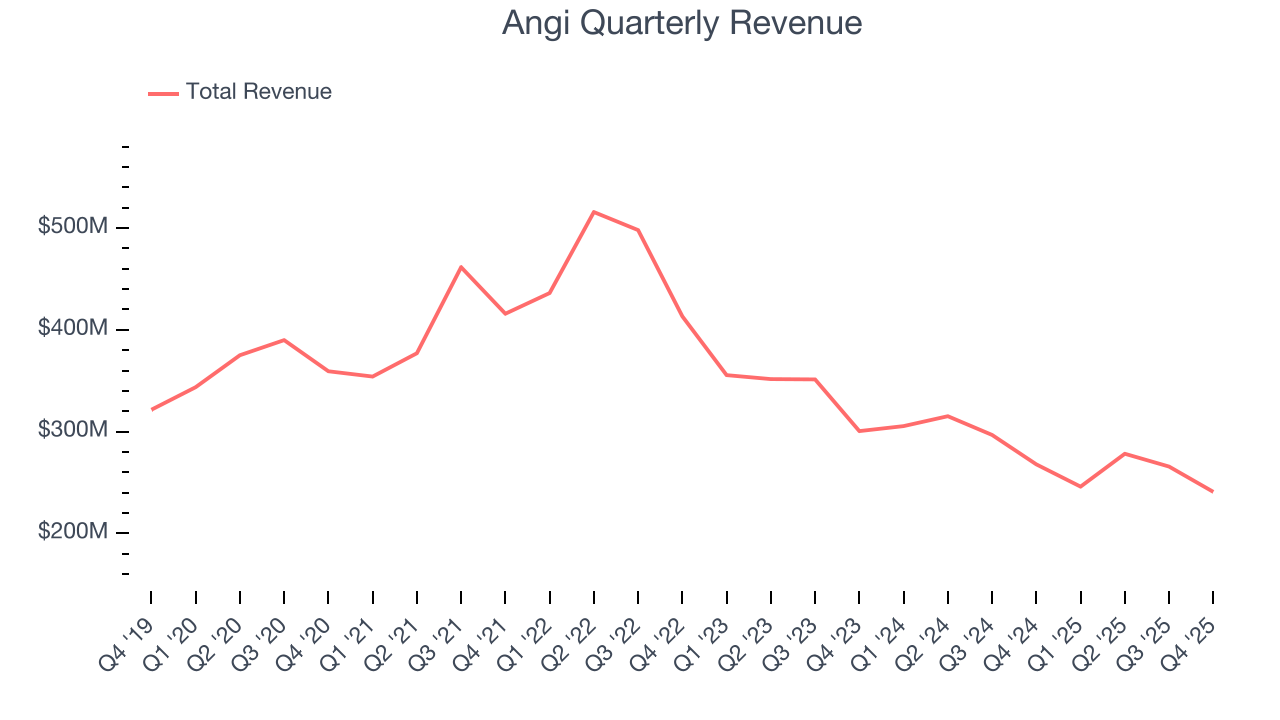

5. Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last three years, Angi’s demand was weak and its revenue declined by 17.9% per year. This wasn’t a great result and is a rough starting point for our analysis.

This quarter, Angi missed Wall Street’s estimates and reported a rather uninspiring 10.1% year-on-year revenue decline, generating $240.8 million of revenue.

Looking ahead, sell-side analysts expect revenue to grow 3.8% over the next 12 months. While this projection suggests its newer products and services will fuel better top-line performance, it is still below the sector average.

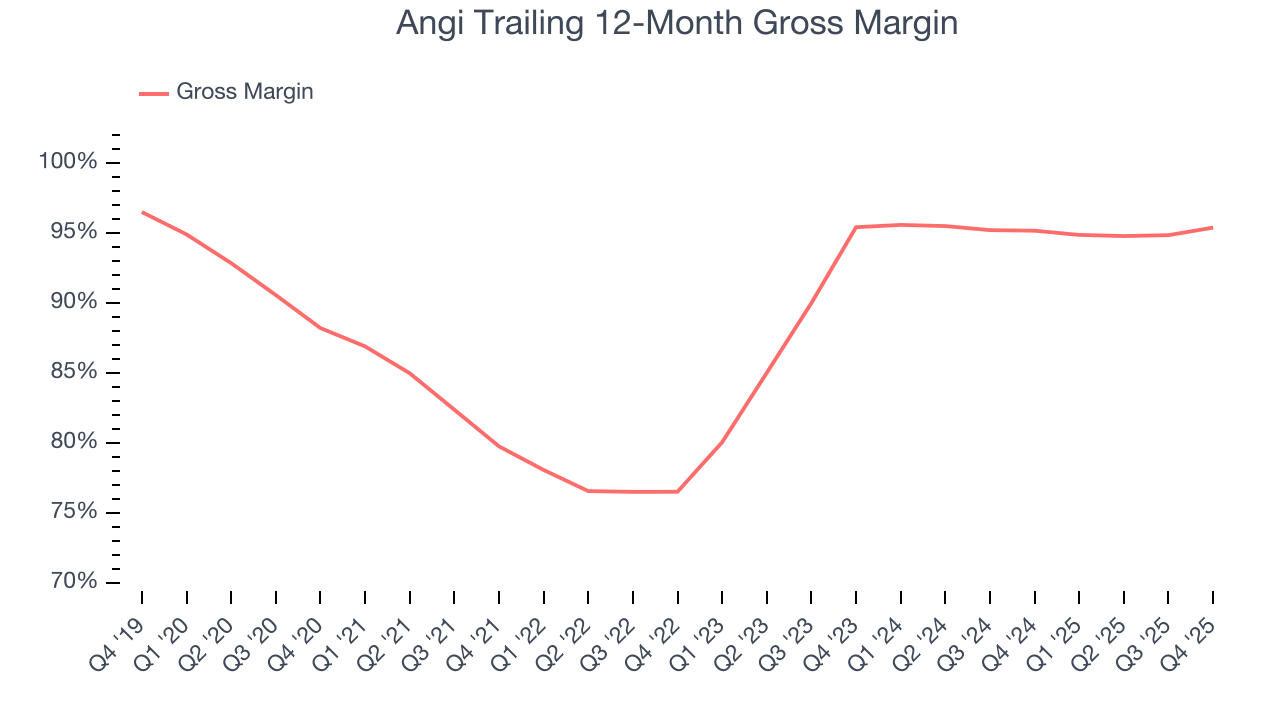

6. Gross Margin & Pricing Power

For gig economy businesses like Angi, gross profit tells us how much money the company gets to keep after covering the base cost of its products and services, which typically include server hosting, customer support, and payment processing fees. Another cost of revenue could also be insurance to protect against liabilities arising from providing transportation, housing, or freelance work services.

Angi’s gross margin is one of the highest in the consumer internet sector, an output of its asset-lite business model and strong pricing power. It also enables the company to fund large investments in product and marketing during periods of rapid growth to achieve higher profits in the future. As you can see below, it averaged an elite 95.3% gross margin over the last two years. That means Angi only paid its providers $4.72 for every $100 in revenue.

This quarter, Angi’s gross profit margin was 96.3%, up 2.2 percentage points year on year. On a wider time horizon, the company’s full-year margin has remained steady over the past four quarters, suggesting its input costs have been stable and it isn’t under pressure to lower prices.

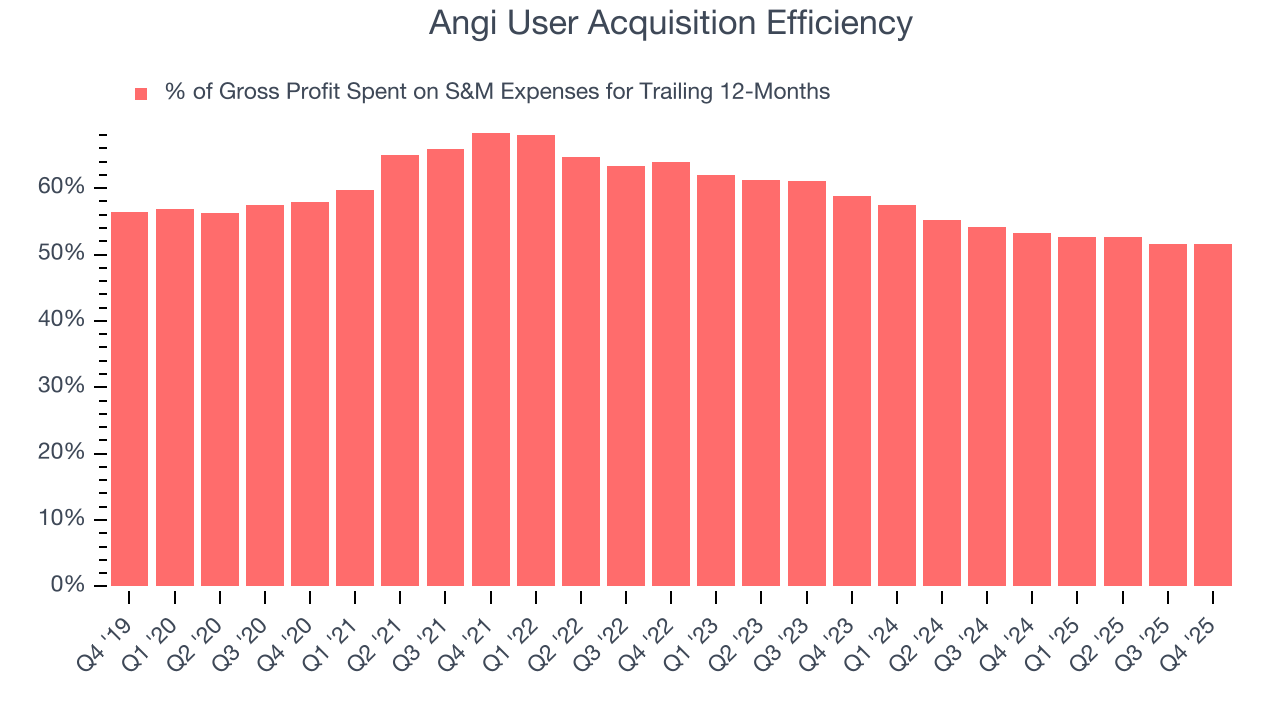

7. User Acquisition Efficiency

Unlike enterprise software that’s typically sold by dedicated sales teams, consumer internet businesses like Angi grow from a combination of product virality, paid advertisement, and incentives.

It’s expensive for Angi to acquire new users as the company has spent 51.6% of its gross profit on sales and marketing expenses over the last year. This inefficiency indicates that Angi’s product offering can be easily replicated and that it must continue investing to maintain an acceptable growth trajectory.

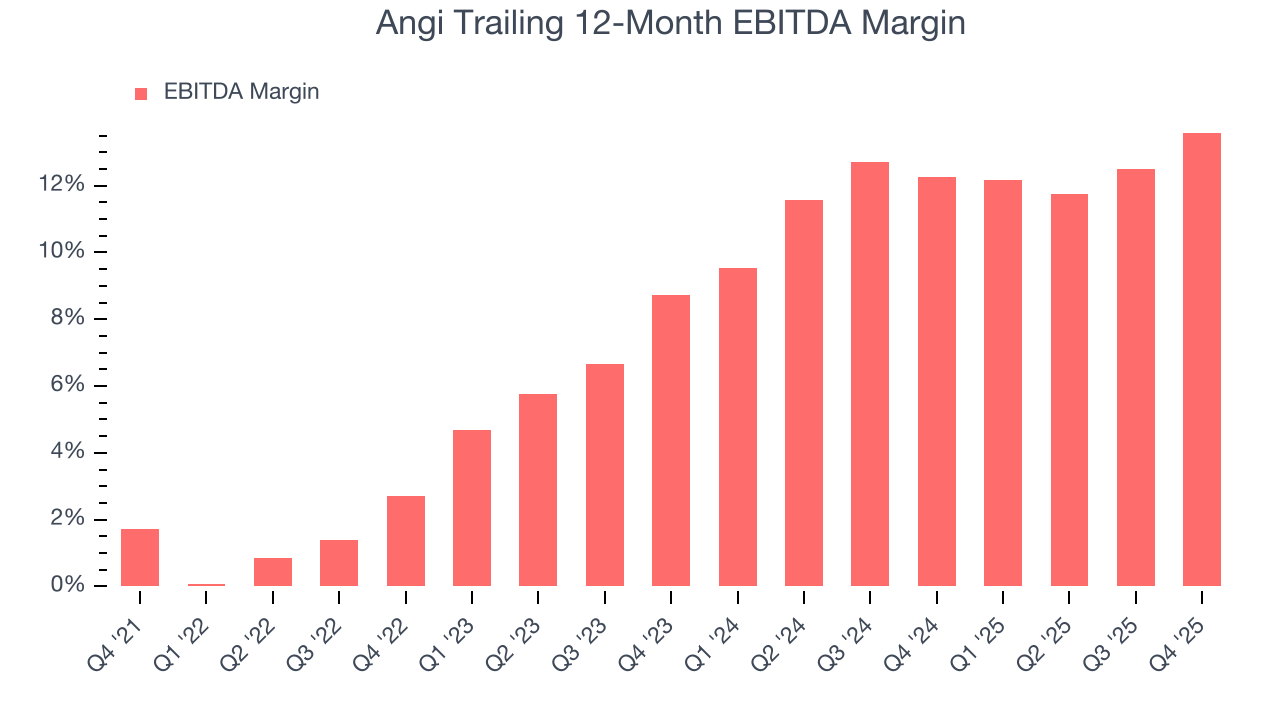

8. EBITDA

Investors regularly analyze operating income to understand a company’s profitability. Similarly, EBITDA is a common profitability metric for consumer internet companies because it excludes various one-time or non-cash expenses, offering a better perspective of the business’s profit potential.

Angi has been an efficient company over the last two years. It was one of the more profitable businesses in the consumer internet sector, boasting an average EBITDA margin of 12.9%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, Angi’s EBITDA margin rose by 10.9 percentage points over the last few years, showing its efficiency has improved.

This quarter, Angi generated an EBITDA margin profit margin of 16.5%, up 4.6 percentage points year on year. The increase was encouraging, and because its EBITDA margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

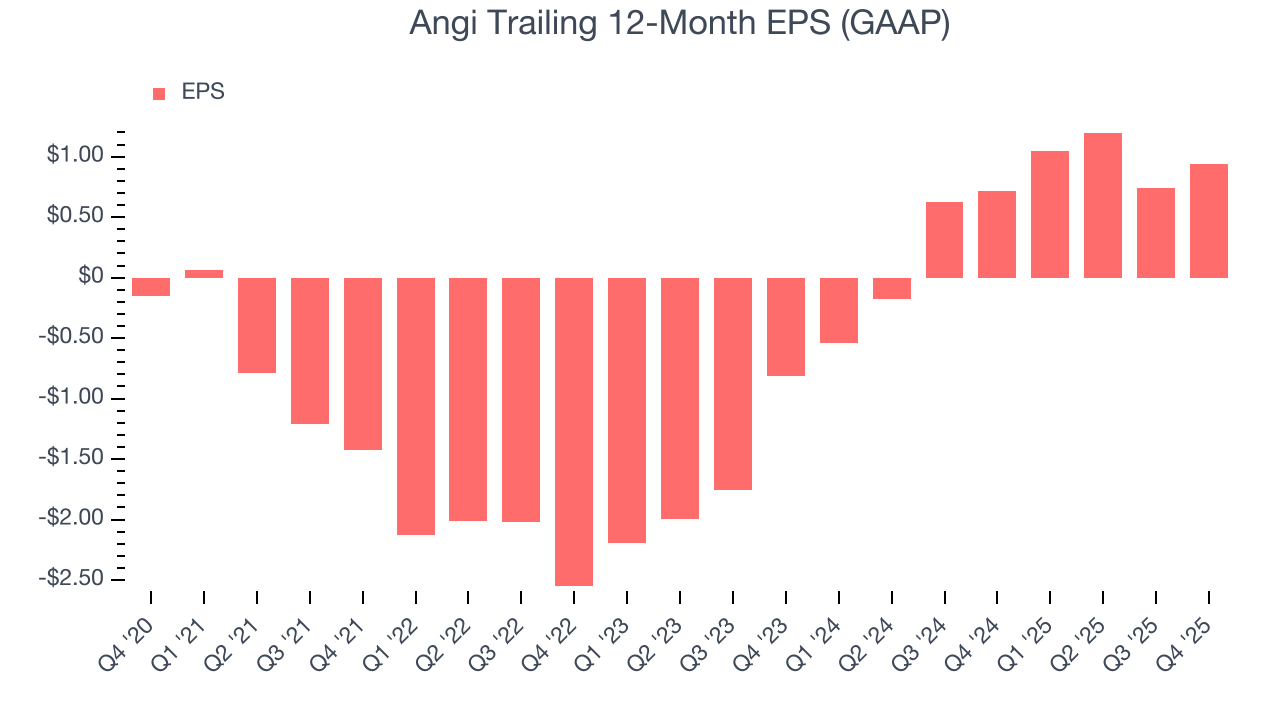

9. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Angi’s full-year EPS flipped from negative to positive over the last three years. This is encouraging and shows it’s at a critical moment in its life.

In Q4, Angi reported EPS of $0.17, up from negative $0.03 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates, but we care more about long-term EPS growth than short-term movements. Over the next 12 months, Wall Street expects Angi’s full-year EPS of $0.94 to grow 54.6%.

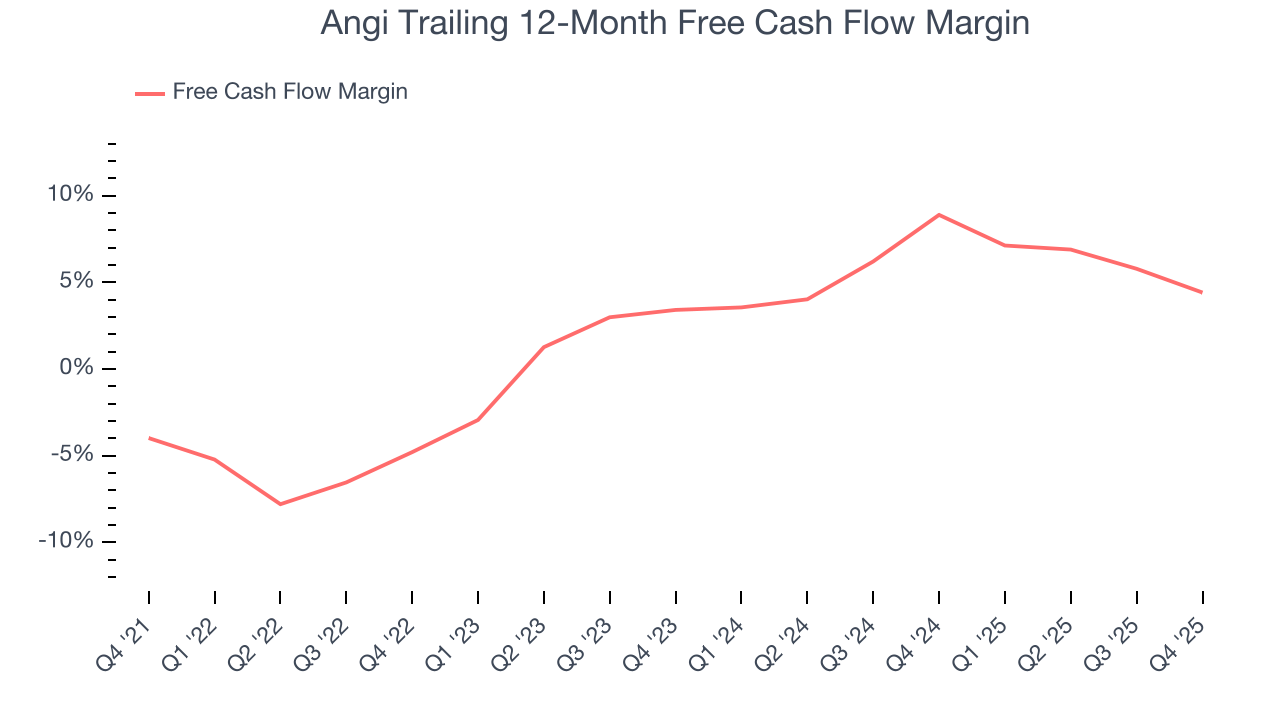

10. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Angi has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 6.8% over the last two years, slightly better than the broader consumer internet sector.

Taking a step back, we can see that Angi’s margin expanded by 9.2 percentage points over the last few years. This is encouraging because it gives the company more optionality.

Angi’s free cash flow clocked in at $11.4 million in Q4, equivalent to a 4.7% margin. The company’s cash profitability regressed as it was 5.4 percentage points lower than in the same quarter last year, prompting us to pay closer attention. Short-term fluctuations typically aren’t a big deal because investment needs can be seasonal, but we’ll be watching to see if the trend extrapolates into future quarters.

11. Balance Sheet Assessment

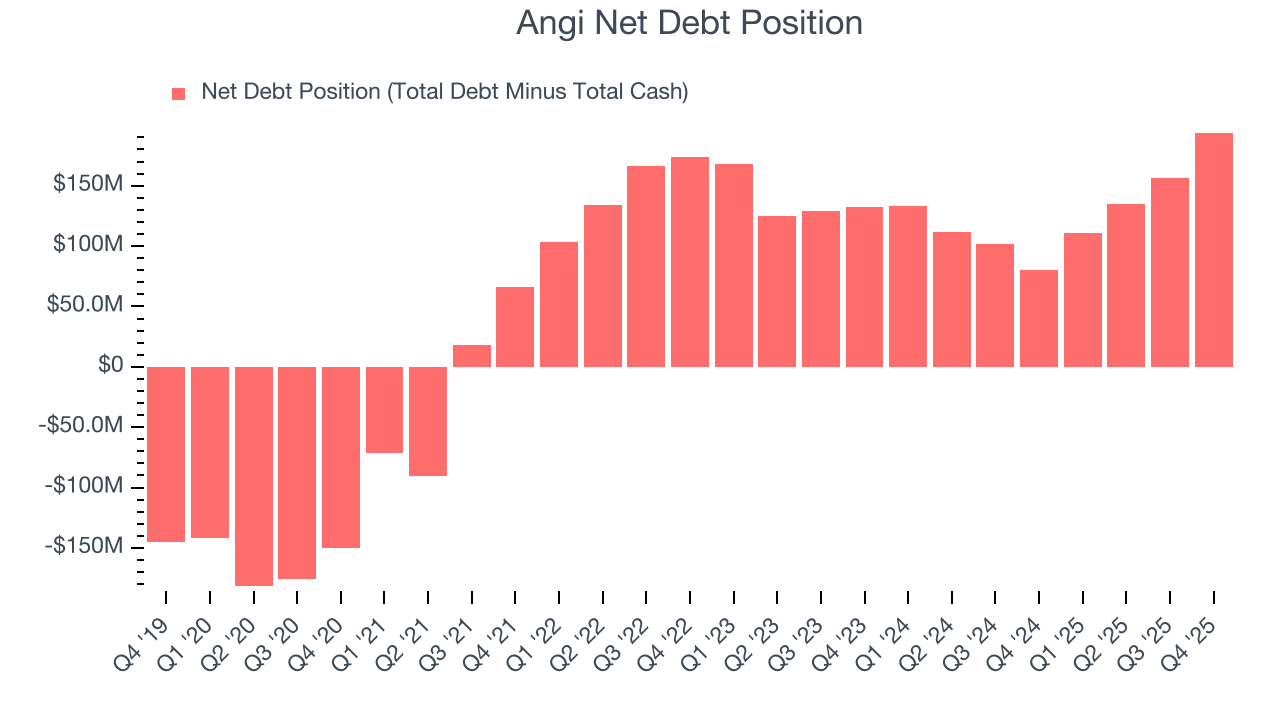

Angi reported $303.7 million of cash and $497.7 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $140.1 million of EBITDA over the last 12 months, we view Angi’s 1.4× net-debt-to-EBITDA ratio as safe. We also see its $2.17 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Angi’s Q4 Results

We struggled to find many positives in these results. Its revenue slightly missed and its EBITDA fell slightly short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 8.7% to $10.92 immediately following the results.

13. Is Now The Time To Buy Angi?

Updated: March 23, 2026 at 10:18 PM EDT

When considering an investment in Angi, investors should account for its valuation and business qualities as well as what’s happened in the latest quarter.

Angi isn’t a terrible business, but it doesn’t pass our bar. First off, its revenue has declined over the last three years. While its admirable gross margins are a wonderful starting point for the overall profitability of the business, the downside is its service requests have declined. On top of that, its sales and marketing efficiency is subpar.

Angi’s EV/EBITDA ratio based on the next 12 months is 3.5x. This valuation multiple is fair, but we don’t have much faith in the company. We're pretty confident there are more exciting stocks to buy at the moment.

Wall Street analysts have a consensus one-year price target of $14.29 on the company (compared to the current share price of $7.56).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.