Astronics (ATRO)

We love companies like Astronics. Its rapid revenue growth gives it operating leverage, making it more profitable as it expands.― StockStory Analyst Team

1. News

2. Summary

Why We Like Astronics

Integrating power outlets into many Boeing aircraft, Astronics (NASDAQ:ATRO) is a provider of technologies and services to the global aerospace, defense, and electronics industries.

- Additional sales over the last five years increased its profitability as the 45.2% annual growth in its earnings per share outpaced its revenue

- Forecasted revenue growth of 13.1% for the next 12 months indicates its momentum over the last two years is sustainable

- Annual revenue growth of 11.8% over the last two years was superb and indicates its market share increased during this cycle

We have an affinity for Astronics. The valuation seems reasonable in light of its quality, so this might be an opportune time to buy some shares.

Why Is Now The Time To Buy Astronics?

Astronics’s stock price of $65.27 implies a valuation ratio of 25.9x forward P/E. Most companies in the industrials sector may feature a cheaper multiple, but we think Astronics is priced fairly given its fundamentals.

By definition, where you buy a stock impacts returns. But according to our work on the topic, business quality is a much bigger determinant of market outperformance over the long term compared to entry price.

3. Astronics (ATRO) Research Report: Q4 CY2025 Update

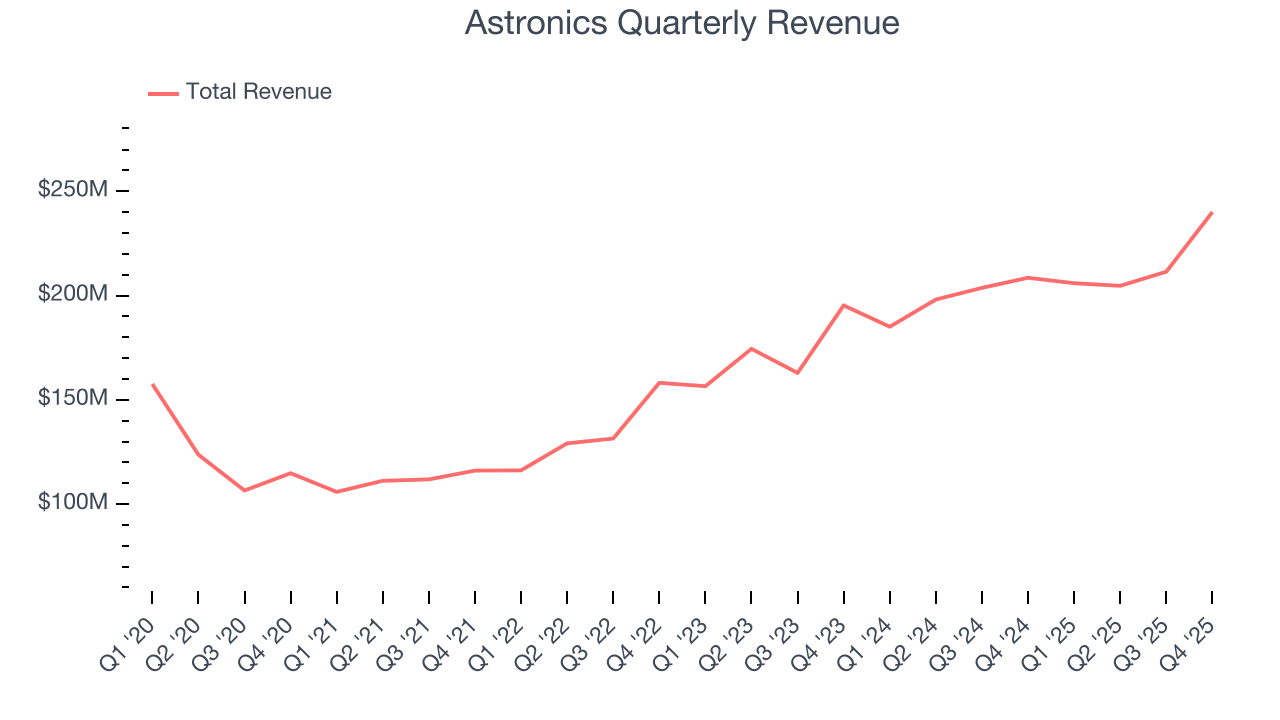

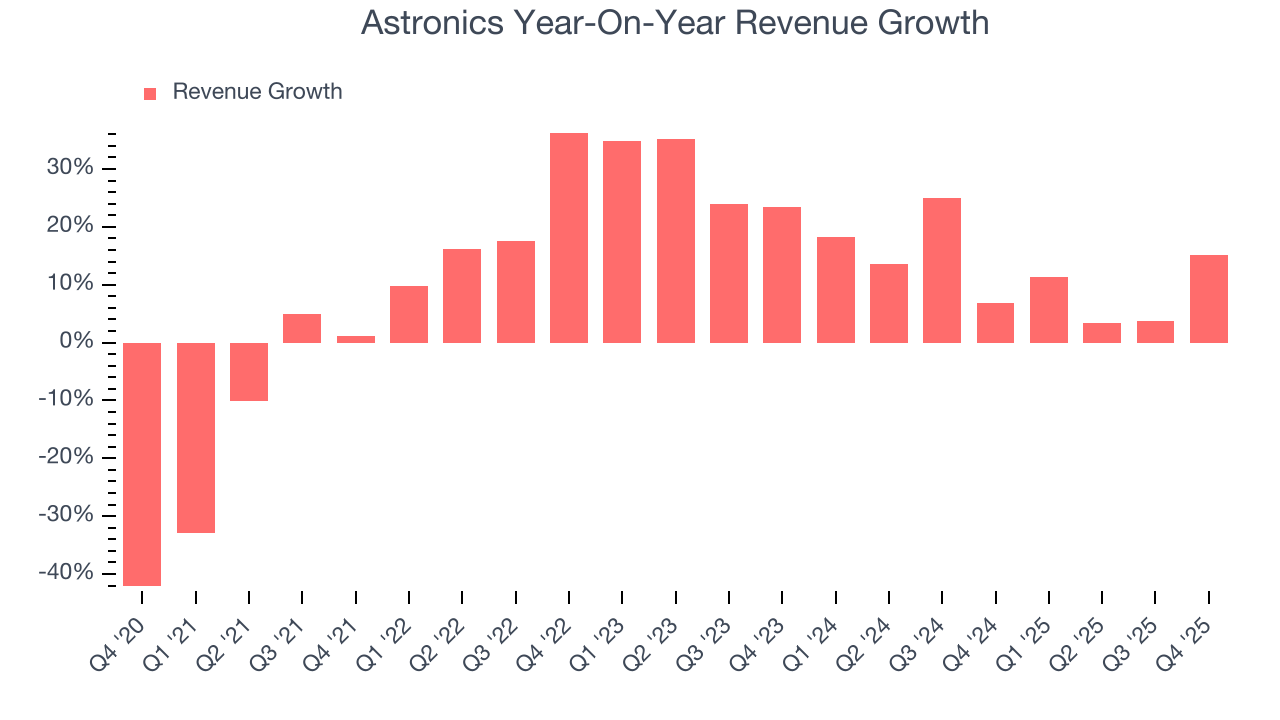

Aerospace and defense technology solutions provider Astronics Corporation (NASDAQ:ATRO) announced better-than-expected revenue in Q4 CY2025, with sales up 15.1% year on year to $240.1 million. On the other hand, next quarter’s revenue guidance of $225 million was less impressive, coming in 3.3% below analysts’ estimates. Its non-GAAP profit of $0.75 per share was 25% above analysts’ consensus estimates.

Astronics (ATRO) Q4 CY2025 Highlights:

- Revenue: $240.1 million vs analyst estimates of $237.1 million (15.1% year-on-year growth, 1.2% beat)

- Adjusted EPS: $0.75 vs analyst estimates of $0.60 (25% beat)

- Adjusted EBITDA: $45.67 million vs analyst estimates of $39.57 million (19% margin, 15.4% beat)

- Revenue Guidance for Q1 CY2026 is $225 million at the midpoint, below analyst estimates of $232.7 million

- Operating Margin: 14.8%, up from 4.3% in the same quarter last year

- Free Cash Flow Margin: 6.6%, down from 11.1% in the same quarter last year

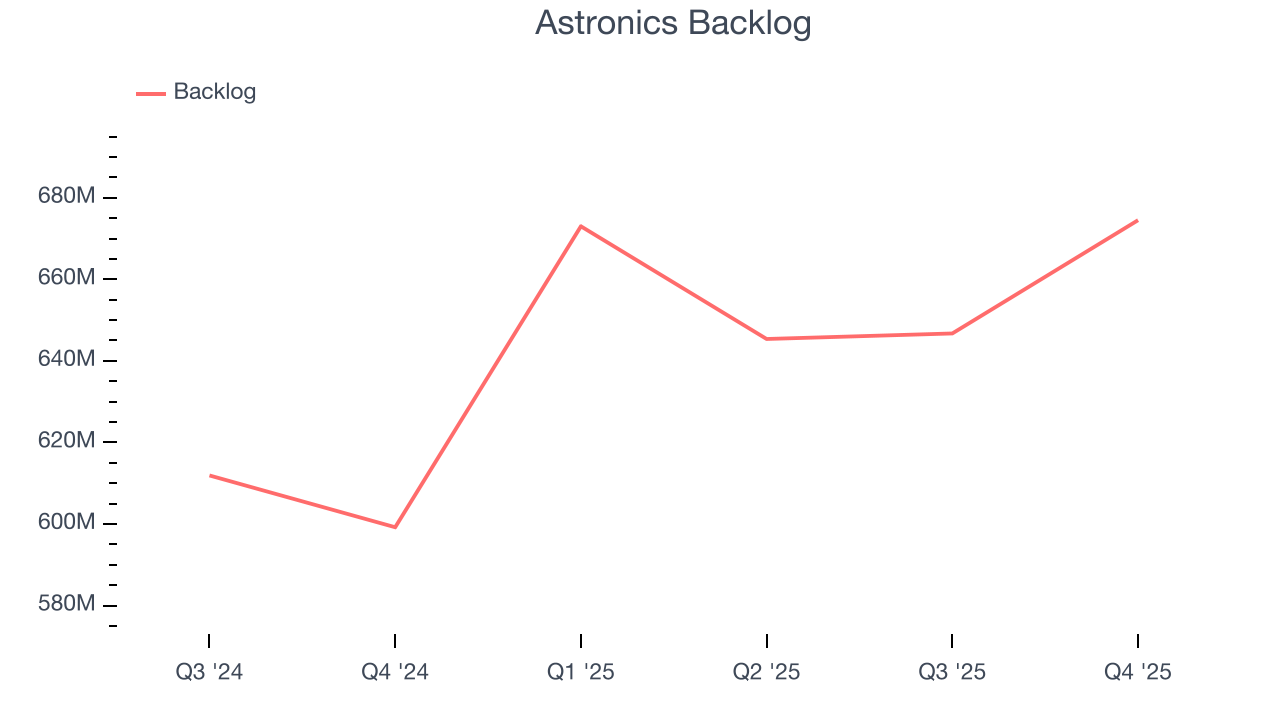

- Backlog: $674.5 million at quarter end, up 12.6% year on year

- Market Capitalization: $2.72 billion

Company Overview

Integrating power outlets into many Boeing aircraft, Astronics (NASDAQ:ATRO) is a provider of technologies and services to the global aerospace, defense, and electronics industries.

Founded in 1968 and headquartered in East Aurora, New York, Astronics has established itself in the development and manufacture of electrical power generation, distribution and motion systems, lighting and safety systems, avionics products, aircraft structures, and automated test systems. Astronics has its operations in the United States, Canada, France, and England, as well as engineering offices in Ukraine and India.

The company operates through two primary business segments: Aerospace and Test Systems. The Aerospace segment, which accounts for the majority of Astronics' sales, designs and manufactures products for the global aerospace industry. This segment's offerings include lighting and safety systems, electrical power generation and distribution systems, aircraft structures, avionics products, and systems certification services. Astronics' Aerospace customers span a wide range, including airframe manufacturers, suppliers, aircraft operators, and branches of the U.S. Department of Defense.

The Test Systems segment focuses on the design, development, manufacture, and maintenance of automated test systems that support the aerospace and defense, communications, and mass transit industries. This segment also produces training and simulation devices for both commercial and military applications. Astronics' Test Systems products are sold to a global customer base, including original equipment manufacturers and prime government contractors for both electronics and military products.

4. Aerospace

Aerospace companies often possess technical expertise and have made significant capital investments to produce complex products. It is an industry where innovation is important, and lately, emissions and automation are in focus, so companies that boast advances in these areas can take market share. On the other hand, demand for aerospace products can ebb and flow with economic cycles and geopolitical tensions, which can be particularly painful for companies with high fixed costs.

Astronics’ peers and competitors include AerSale (NASDAQ:ATRO) and Virgin Galactic (NASDAQ:SPCE)

5. Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Thankfully, Astronics’s 11.4% annualized revenue growth over the last five years was impressive. Its growth surpassed the average industrials company and shows its offerings resonate with customers, a great starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Astronics’s annualized revenue growth of 11.8% over the last two years aligns with its five-year trend, suggesting its demand was predictably strong.

Astronics also reports its backlog, or the value of its outstanding orders that have not yet been executed or delivered. Astronics’s backlog reached $674.5 million in the latest quarter and averaged 9.1% year-on-year growth over the last two years. Because this number is lower than its revenue growth, we can see the company fulfilled orders at a faster rate than it added new orders to the backlog. This implies Astronics was operating efficiently but raises questions about the health of its sales pipeline.

This quarter, Astronics reported year-on-year revenue growth of 15.1%, and its $240.1 million of revenue exceeded Wall Street’s estimates by 1.2%. Company management is currently guiding for a 9.3% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 12.3% over the next 12 months, similar to its two-year rate. This projection is healthy and implies the market is forecasting success for its products and services.

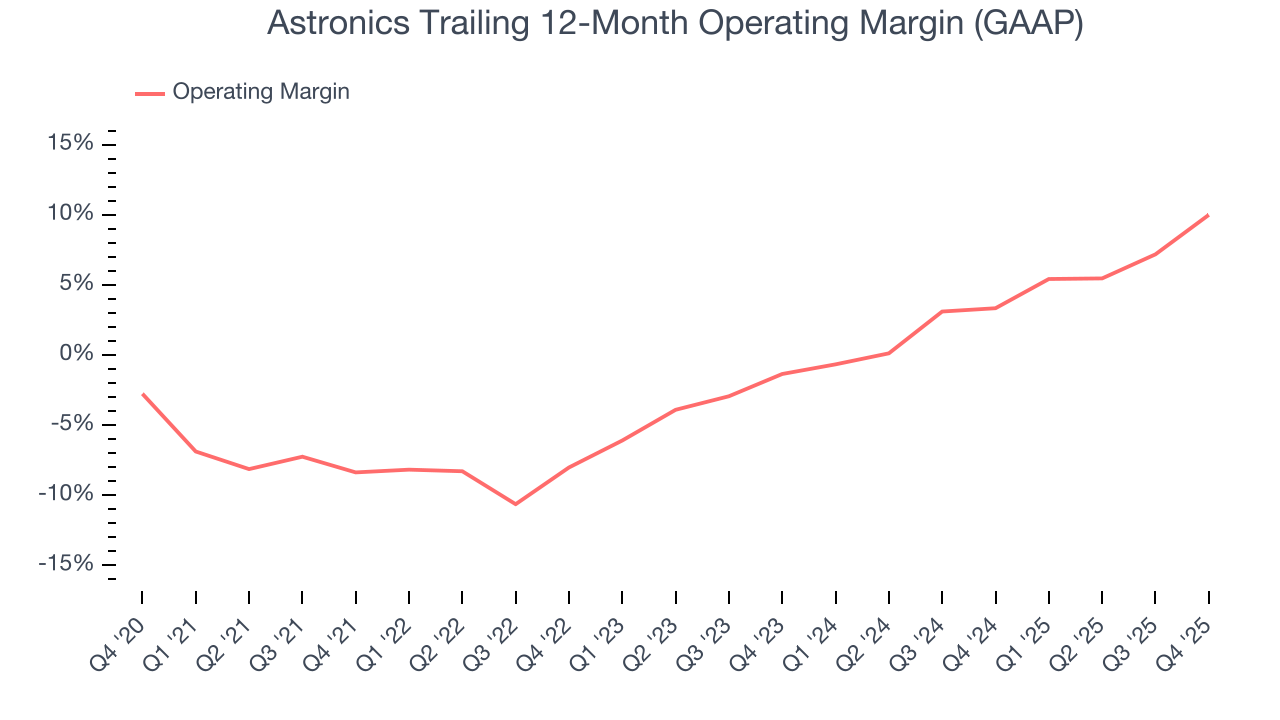

6. Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Astronics was roughly breakeven when averaging the last five years of quarterly operating profits, inadequate for an industrials business.

On the plus side, Astronics’s operating margin rose by 18.4 percentage points over the last five years, as its sales growth gave it immense operating leverage.

This quarter, Astronics generated an operating margin profit margin of 14.8%, up 10.5 percentage points year on year. This increase was a welcome development and shows it was more efficient.

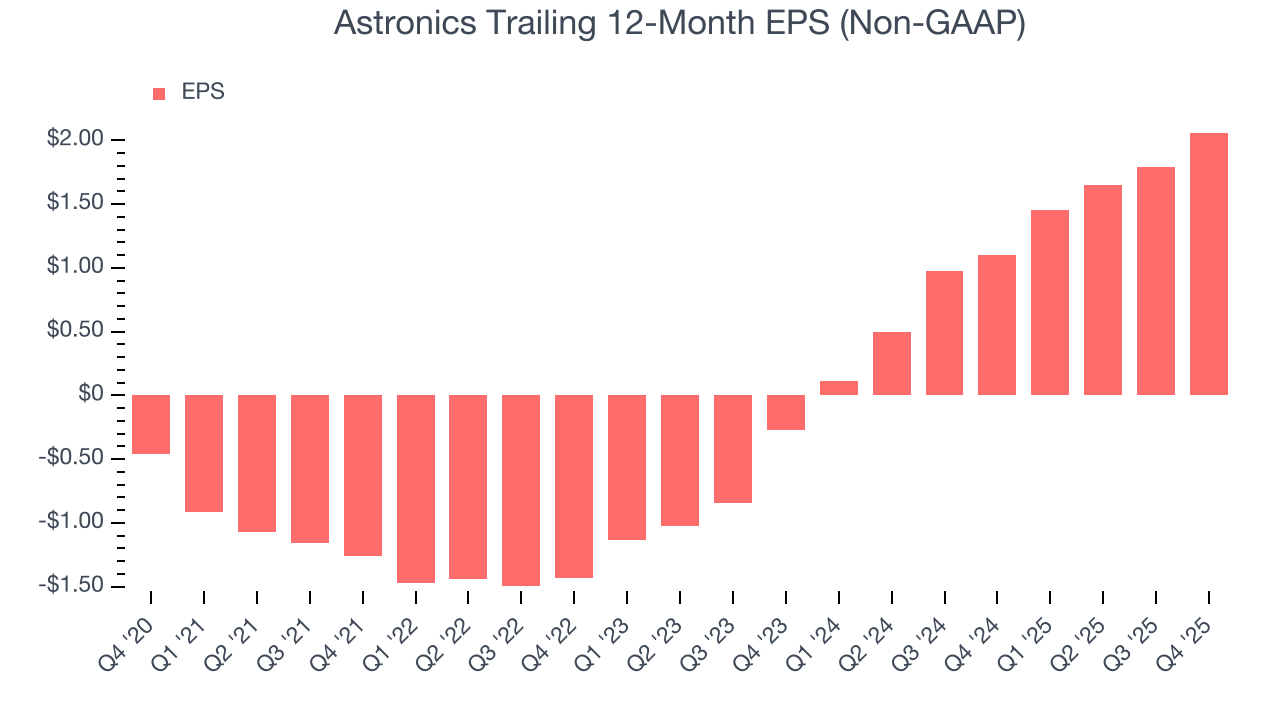

7. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Astronics’s full-year EPS flipped from negative to positive over the last five years. This is a good sign and shows it’s at an inflection point.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Astronics, its two-year annual EPS growth of 208% was higher than its five-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.

In Q4, Astronics reported adjusted EPS of $0.75, up from $0.48 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Astronics’s full-year EPS of $2.06 to grow 22.3%.

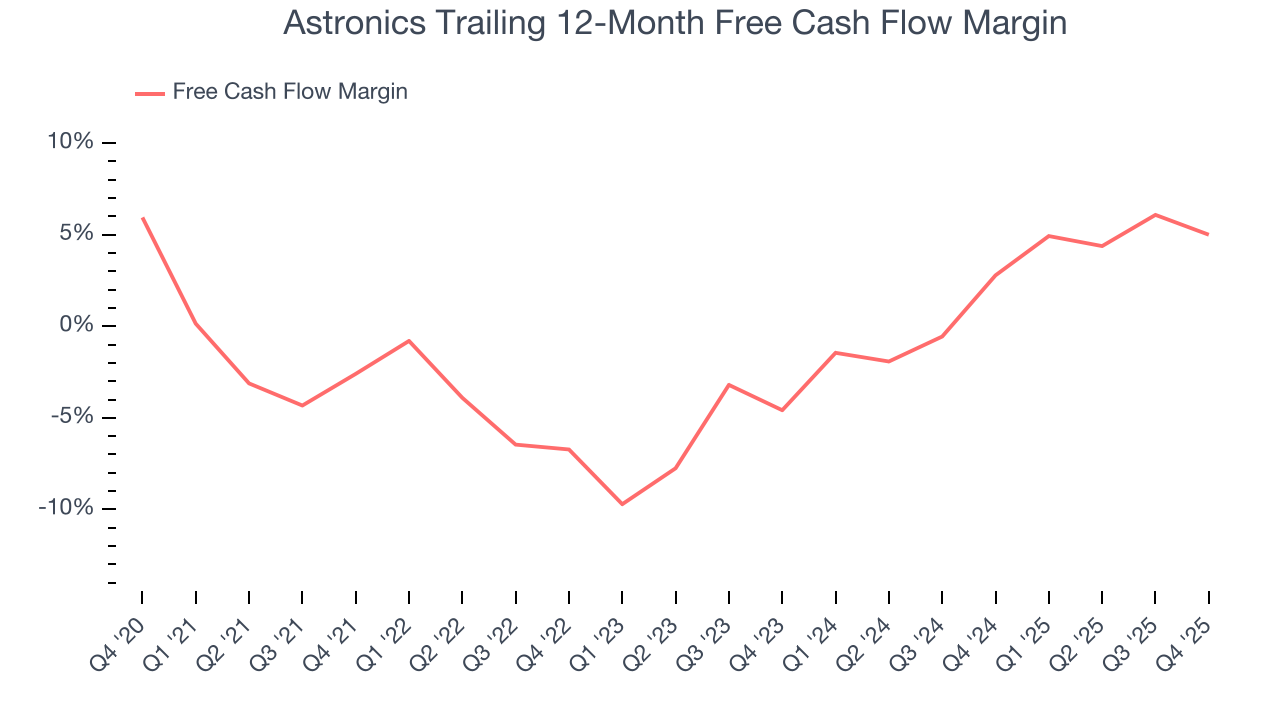

8. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Astronics broke even from a free cash flow perspective over the last five years, giving the company limited opportunities to return capital to shareholders.

Taking a step back, an encouraging sign is that Astronics’s margin expanded by 7.6 percentage points during that time. We have no doubt shareholders would like to continue seeing its cash conversion rise as it gives the company more optionality.

Astronics’s free cash flow clocked in at $15.81 million in Q4, equivalent to a 6.6% margin. The company’s cash profitability regressed as it was 4.6 percentage points lower than in the same quarter last year, but it’s still above its five-year average. We wouldn’t read too much into this quarter’s decline because capital expenditures can be seasonal and companies often stockpile inventory in anticipation of higher demand, causing short-term swings. Long-term trends trump temporary fluctuations.

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Although Astronics has shown solid business quality lately, it struggled to grow profitably in the past. Its five-year average ROIC was negative 0.3%, meaning management lost money while trying to expand the business.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Astronics’s ROIC has increased. This is a good sign, but we recognize its lack of profitable growth during the COVID era was the primary reason for the change.

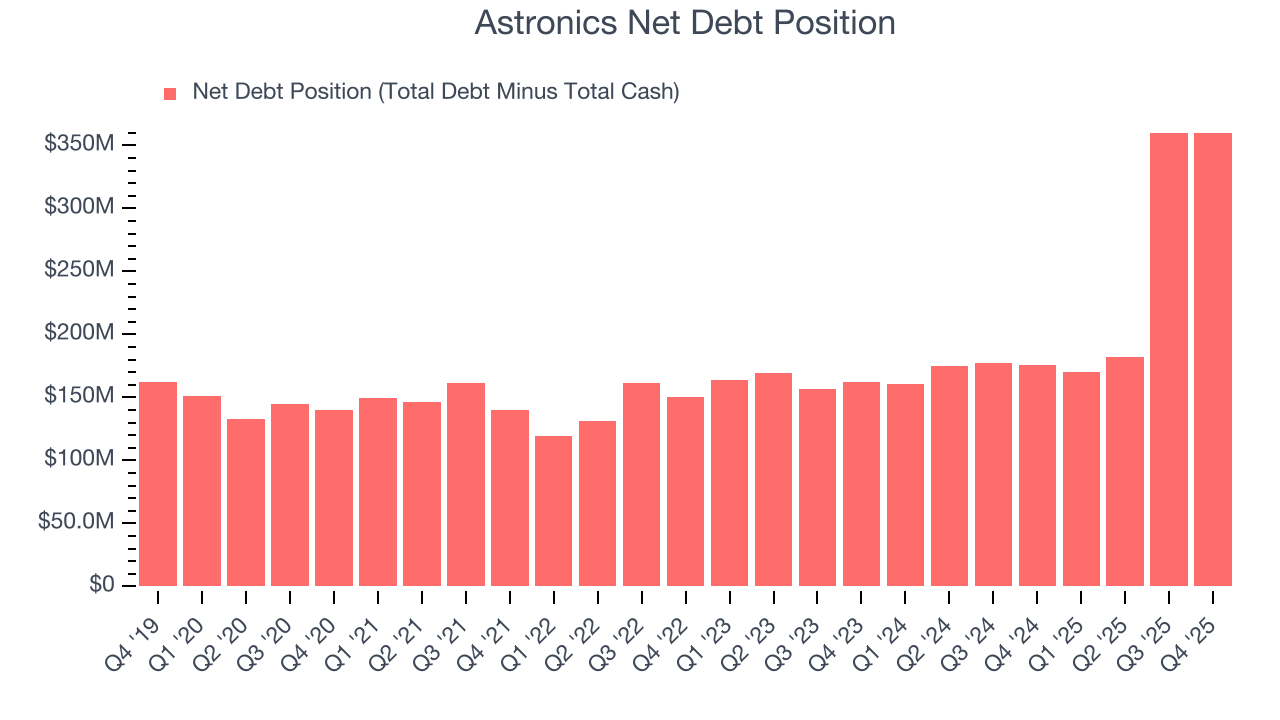

10. Balance Sheet Assessment

Astronics reported $18.18 million of cash and $378.4 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $134.5 million of EBITDA over the last 12 months, we view Astronics’s 2.7× net-debt-to-EBITDA ratio as safe. We also see its $5.77 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from Astronics’s Q4 Results

It was good to see Astronics beat analysts’ EPS expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. On the other hand, its revenue guidance for next quarter missed. Overall, we think this was a decent quarter with some key metrics above expectations. The market seemed to be hoping for more, and the stock traded down 2.5% to $77.49 immediately after reporting.

12. Is Now The Time To Buy Astronics?

Updated: March 26, 2026 at 11:38 PM EDT

Before making an investment decision, investors should account for Astronics’s business fundamentals and valuation in addition to what happened in the latest quarter.

Astronics is a rock-solid business worth owning. To begin with, its revenue growth was impressive over the last five years, and its growth over the next 12 months is expected to accelerate. And while its relatively low ROIC suggests management has struggled to find compelling investment opportunities, its rising cash profitability gives it more optionality. On top of that, Astronics’s expanding operating margin shows the business has become more efficient.

Astronics’s P/E ratio based on the next 12 months is 25.9x. Looking across the spectrum of industrials companies today, Astronics’s fundamentals shine bright. We like the stock at this price.

Wall Street analysts have a consensus one-year price target of $87.58 on the company (compared to the current share price of $65.27), implying they see 34.2% upside in buying Astronics in the short term.