BioMarin Pharmaceutical (BMRN)

BioMarin Pharmaceutical is intriguing. It not only prints profits but also has increased its margins, showing its fundamentals are improving.― StockStory Analyst Team

1. News

2. Summary

Why BioMarin Pharmaceutical Is Interesting

Pioneering treatments for conditions that often had no previous therapeutic options, BioMarin Pharmaceutical (NASDAQ:BMRN) develops and commercializes therapies that address the root causes of rare genetic disorders, particularly those affecting children.

- Performance over the past five years shows its incremental sales were extremely profitable, as its annual earnings per share growth of 13.8% outpaced its revenue gains

- Forecasted revenue growth of 13.6% for the next 12 months indicates its momentum over the last two years is sustainable

- On the flip side, its low returns on capital reflect management’s struggle to allocate funds effectively

BioMarin Pharmaceutical has some noteworthy aspects. If you’re a believer, the valuation looks fair.

Why Is Now The Time To Buy BioMarin Pharmaceutical?

At $55.37 per share, BioMarin Pharmaceutical trades at 11x forward P/E. Many healthcare companies feature higher valuation multiples than BioMarin Pharmaceutical. Regardless, we think BioMarin Pharmaceutical’s current price is appropriate given the quality you get.

This could be a good time to invest if you think there are underappreciated aspects of the business.

3. BioMarin Pharmaceutical (BMRN) Research Report: Q4 CY2025 Update

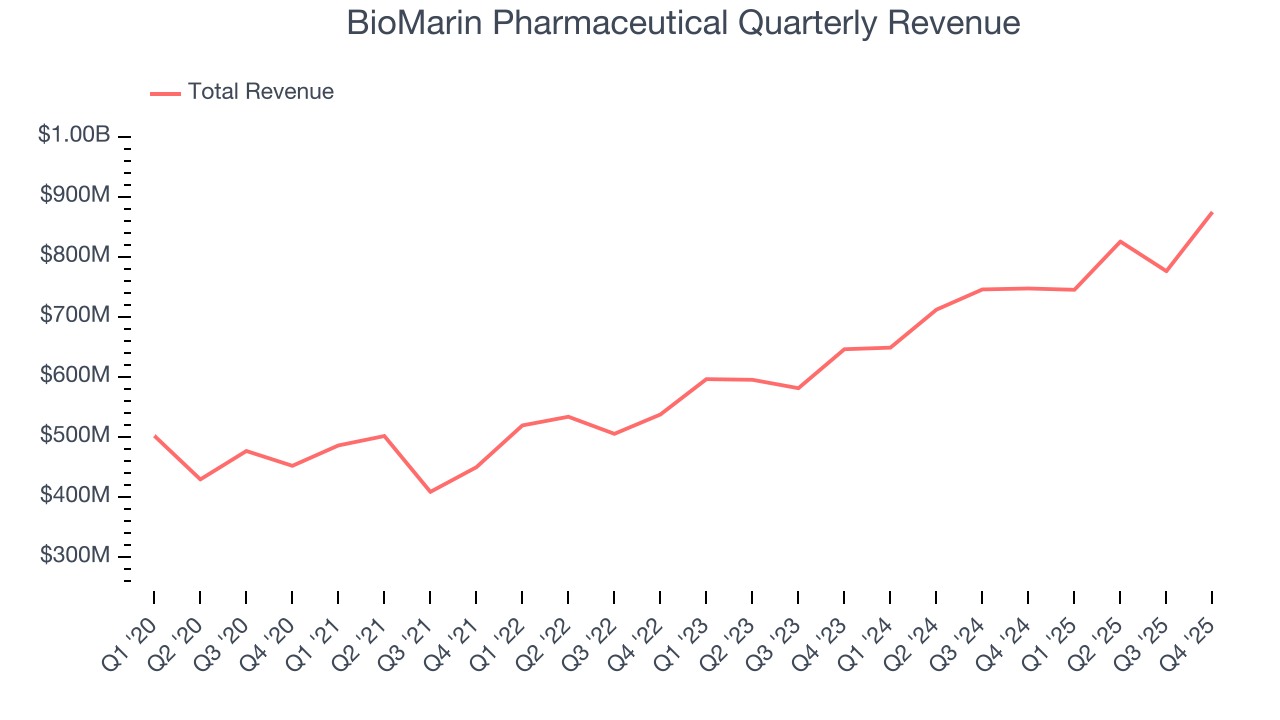

Biotech company BioMarin Pharmaceutical (NASDAQ:BMRN) reported Q4 CY2025 results exceeding the market’s revenue expectations, with sales up 17% year on year to $874.6 million. The company expects the full year’s revenue to be around $3.38 billion, close to analysts’ estimates. Its non-GAAP profit of $0.46 per share was 17.9% below analysts’ consensus estimates.

BioMarin Pharmaceutical (BMRN) Q4 CY2025 Highlights:

- Revenue: $874.6 million vs analyst estimates of $834.3 million (17% year-on-year growth, 4.8% beat)

- Adjusted EPS: $0.46 vs analyst expectations of $0.56 (17.9% miss)

- Adjusted EBITDA: -$39.76 million vs analyst estimates of $198.8 million (-4.5% margin, significant miss)

- Adjusted EPS guidance for the upcoming financial year 2026 is $5.05 at the midpoint, missing analyst estimates by 5.3%

- Operating Margin: -5.1%, down from 21.6% in the same quarter last year

- Free Cash Flow Margin: 6.7%, down from 22.2% in the same quarter last year

- Market Capitalization: $12.31 billion

Company Overview

Pioneering treatments for conditions that often had no previous therapeutic options, BioMarin Pharmaceutical (NASDAQ:BMRN) develops and commercializes therapies that address the root causes of rare genetic disorders, particularly those affecting children.

BioMarin's business model focuses on creating targeted therapies for genetic conditions with significant unmet medical needs. The company's approach involves understanding the underlying biology of these disorders and developing treatments that address their fundamental causes rather than just managing symptoms. This strategy has allowed BioMarin to establish a portfolio of specialized medications for conditions that often affect very small patient populations.

The company's product lineup includes several enzyme replacement therapies such as VIMIZIM for MPS IVA (a lysosomal storage disorder), NAGLAZYME for MPS VI, and BRINEURA for CLN2 (a form of Batten disease). These conditions involve deficiencies in specific enzymes that lead to progressive and debilitating symptoms. BioMarin also markets PALYNZIQ and KUVAN for phenylketonuria (PKU), a genetic disorder that affects the body's ability to process the amino acid phenylalanine.

More recently, BioMarin has expanded its portfolio with VOXZOGO for achondroplasia, the most common form of dwarfism, which promotes bone growth in children with open growth plates. In 2023, the company achieved a significant milestone with the approval of ROCTAVIAN, a gene therapy for severe hemophilia A that aims to restore the body's ability to produce clotting factor VIII.

BioMarin's commercial strategy involves direct sales in major markets like the U.S. and Europe, while partnering with distributors in other regions. Given the specialized nature of its products, the company works closely with healthcare providers who treat these rare conditions, often at specialized centers. BioMarin also collaborates with patient advocacy groups to raise awareness about these rare disorders and available treatments.

The company maintains robust research and development capabilities, with multiple clinical and preclinical candidates in its pipeline targeting additional rare genetic disorders. Manufacturing these complex biological products requires specialized facilities, which BioMarin operates to ensure quality control over its therapies.

4. Therapeutics

Over the next few years, therapeutic companies, which develop a wide variety of treatments for diseases and disorders, face strong tailwinds from advancements in precision medicine (including the use of AI to improve hit rates) and growing demand for treatments targeting rare diseases. However, headwinds such as rising scrutiny over drug pricing, regulatory unknowns, and competition from larger, more resourced pharmaceutical companies could weigh on growth.

BioMarin's competitors in the rare disease space include Sanofi's Genzyme unit (NASDAQ: SNY), Ultragenyx Pharmaceutical (NASDAQ: RARE), Alexion (now part of AstraZeneca, NASDAQ: AZN), and Vertex Pharmaceuticals (NASDAQ: VRTX). In gene therapy for hemophilia, BioMarin competes with CSL Behring (ASX: CSL) and Pfizer (NYSE: PFE).

5. Economies of Scale

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With $3.22 billion in revenue over the past 12 months, BioMarin Pharmaceutical has decent scale. This is important as it gives the company more leverage in a heavily regulated, competitive environment that is complex and resource-intensive.

6. Revenue Growth

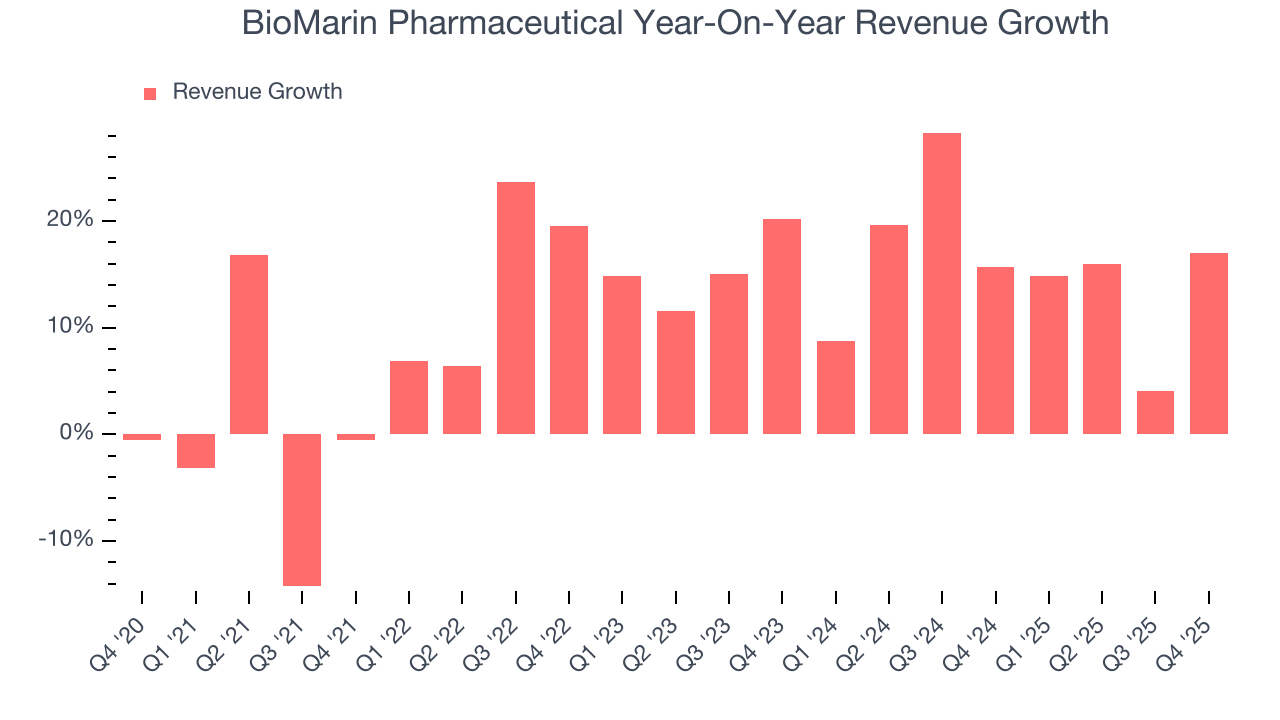

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Luckily, BioMarin Pharmaceutical’s sales grew at a decent 11.6% compounded annual growth rate over the last five years. Its growth was slightly above the average healthcare company and shows its offerings resonate with customers.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. BioMarin Pharmaceutical’s annualized revenue growth of 15.4% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

This quarter, BioMarin Pharmaceutical reported year-on-year revenue growth of 17%, and its $874.6 million of revenue exceeded Wall Street’s estimates by 4.8%.

Looking ahead, sell-side analysts expect revenue to grow 13.4% over the next 12 months, a slight deceleration versus the last two years. Still, this projection is noteworthy and suggests the market is baking in success for its products and services.

7. Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

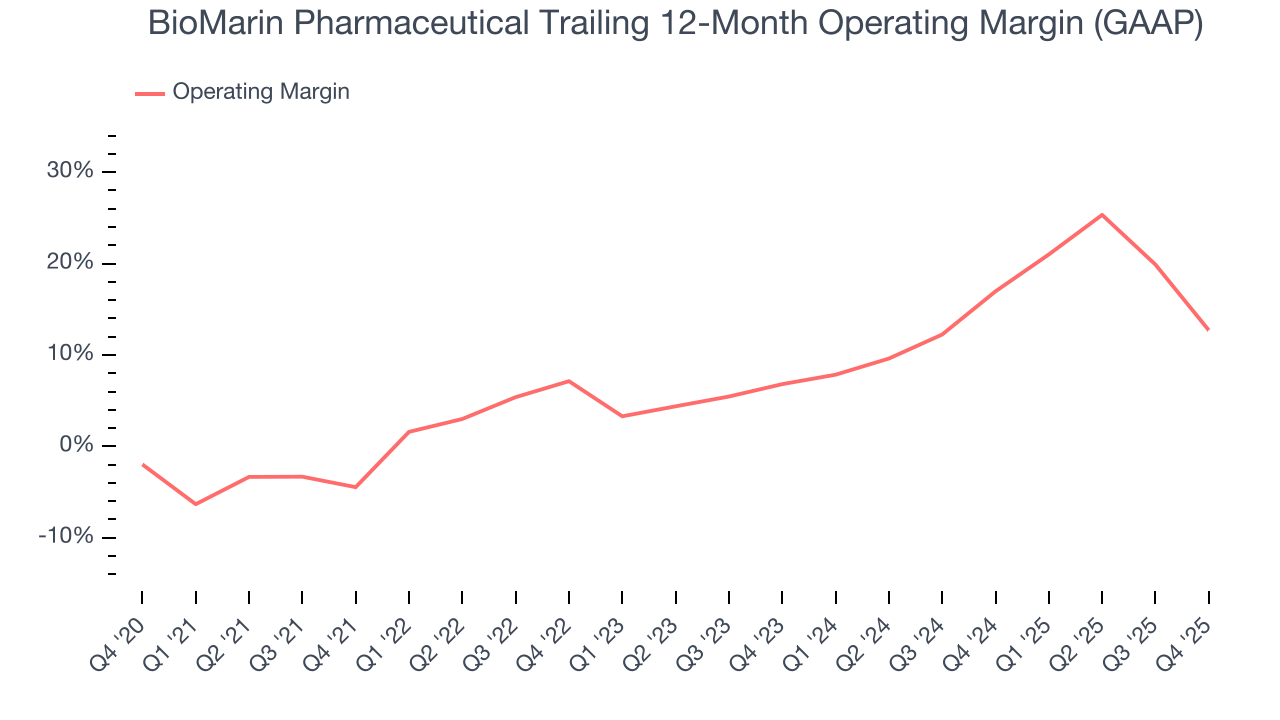

BioMarin Pharmaceutical was profitable over the last five years but held back by its large cost base. Its average operating margin of 9.1% was weak for a healthcare business.

On the plus side, BioMarin Pharmaceutical’s operating margin rose by 17.2 percentage points over the last five years, as its sales growth gave it immense operating leverage. Zooming in on its more recent performance, we can see the company’s trajectory is intact as its margin has also increased by 5.9 percentage points on a two-year basis. These data points are very encouraging and show momentum is on its side.

This quarter, BioMarin Pharmaceutical generated an operating margin profit margin of negative 5.1%, down 26.7 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

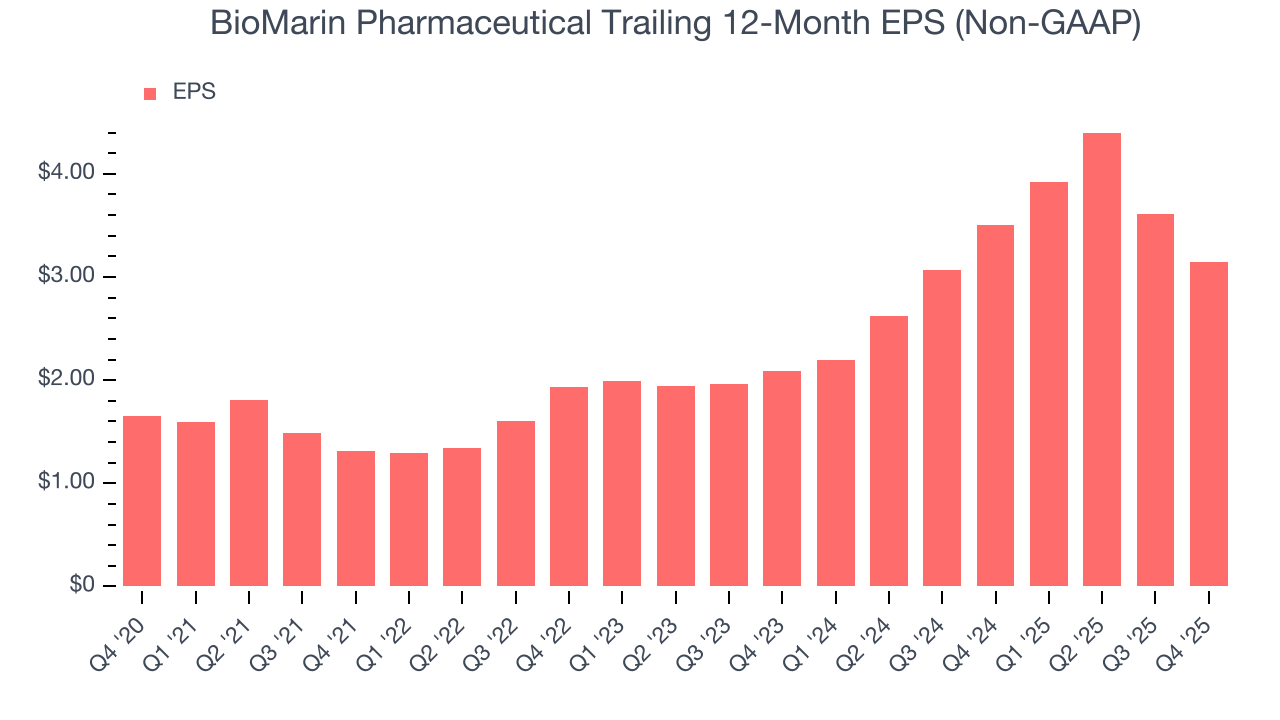

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

BioMarin Pharmaceutical’s EPS grew at a spectacular 13.8% compounded annual growth rate over the last five years, higher than its 11.6% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

Diving into BioMarin Pharmaceutical’s quality of earnings can give us a better understanding of its performance. As we mentioned earlier, BioMarin Pharmaceutical’s operating margin declined this quarter but expanded by 17.2 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q4, BioMarin Pharmaceutical reported adjusted EPS of $0.46, down from $0.92 in the same quarter last year. This print missed analysts’ estimates, but we care more about long-term adjusted EPS growth than short-term movements. Over the next 12 months, Wall Street expects BioMarin Pharmaceutical’s full-year EPS of $3.15 to grow 71.1%.

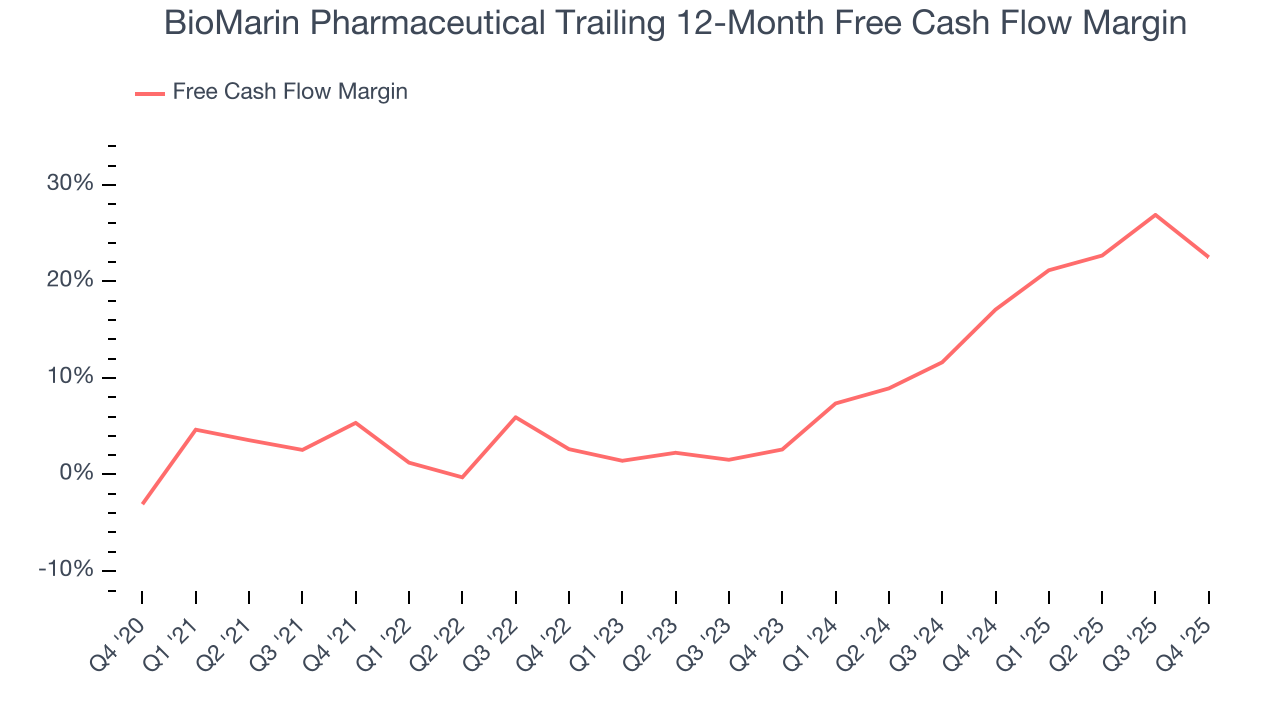

9. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

BioMarin Pharmaceutical has shown impressive cash profitability, giving it the option to reinvest or return capital to investors. The company’s free cash flow margin averaged 11.5% over the last five years, better than the broader healthcare sector. The divergence from its underwhelming operating margin stems from the add-back of non-cash charges like depreciation and stock-based compensation. GAAP operating profit expenses these line items, but free cash flow does not.

Taking a step back, we can see that BioMarin Pharmaceutical’s margin expanded by 17.2 percentage points during that time. This is encouraging because it gives the company more optionality.

BioMarin Pharmaceutical’s free cash flow clocked in at $58.92 million in Q4, equivalent to a 6.7% margin. The company’s cash profitability regressed as it was 15.5 percentage points lower than in the same quarter last year, but we wouldn’t put too much weight on the short term because investment needs can be seasonal, causing temporary swings. Long-term trends trump fluctuations.

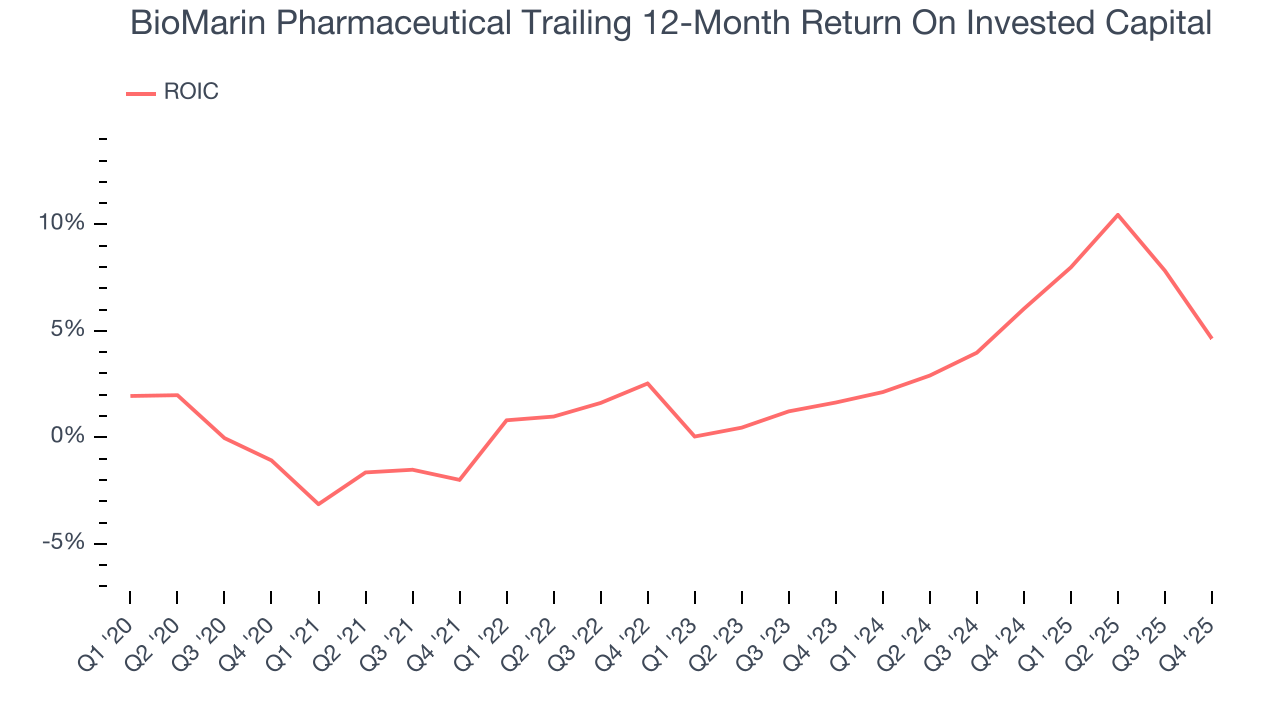

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Although BioMarin Pharmaceutical has shown solid fundamentals lately, it historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 2.6%, lower than the typical cost of capital (how much it costs to raise money) for healthcare companies.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. BioMarin Pharmaceutical’s ROIC has increased over the last few years. its rising ROIC is a good sign and could suggest its competitive advantage or profitable growth opportunities are expanding.

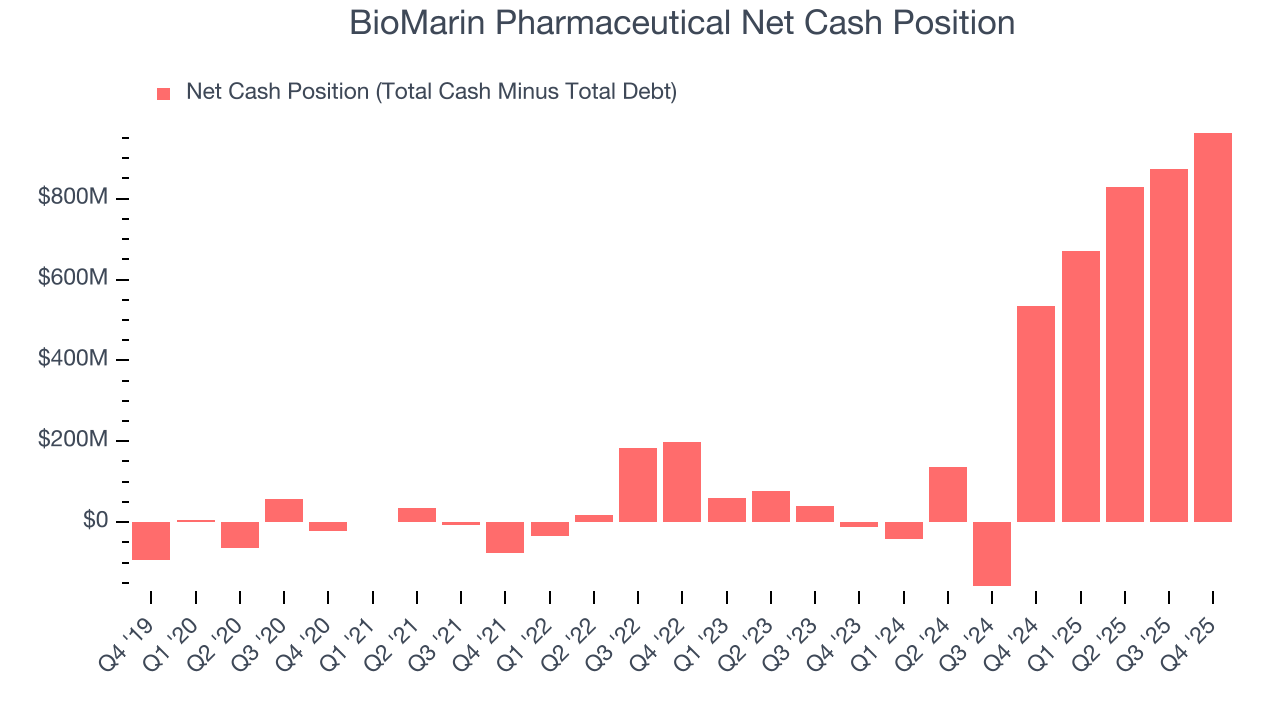

11. Balance Sheet Assessment

Companies with more cash than debt have lower bankruptcy risk.

BioMarin Pharmaceutical is a profitable, well-capitalized company with $1.56 billion of cash and $597.2 million of debt on its balance sheet. This $963.4 million net cash position is 7.8% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

12. Key Takeaways from BioMarin Pharmaceutical’s Q4 Results

We enjoyed seeing BioMarin Pharmaceutical beat analysts’ revenue expectations this quarter. On the other hand, its full-year EPS guidance missed and its EPS fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 2.7% to $61.21 immediately after reporting.

13. Is Now The Time To Buy BioMarin Pharmaceutical?

Updated: March 20, 2026 at 12:20 AM EDT

Before deciding whether to buy BioMarin Pharmaceutical or pass, we urge investors to consider business quality, valuation, and the latest quarterly results.

BioMarin Pharmaceutical is a fine business. First off, its revenue growth was good over the last five years and is expected to accelerate over the next 12 months. And while its relatively low ROIC suggests management has struggled to find compelling investment opportunities, its rising cash profitability gives it more optionality. On top of that, its spectacular EPS growth over the last five years shows its profits are trickling down to shareholders.

BioMarin Pharmaceutical’s P/E ratio based on the next 12 months is 11x. When scanning the healthcare space, BioMarin Pharmaceutical trades at a fair valuation. If you trust the business and its direction, this is an ideal time to buy.

Wall Street analysts have a consensus one-year price target of $88.87 on the company (compared to the current share price of $55.37), implying they see 60.5% upside in buying BioMarin Pharmaceutical in the short term.