Churchill Downs (CHDN)

Churchill Downs faces an uphill battle. Its weak sales growth and low returns on capital show it struggled to generate demand and profits.― StockStory Analyst Team

1. News

2. Summary

Why We Think Churchill Downs Will Underperform

Famous for hosting the Kentucky Derby, Churchill Downs (NASDAQ:CHDN) operates a horse racing, online wagering, and gaming entertainment business in the United States.

- Sales trends were unexciting over the last two years as its 9% annual growth was below the typical consumer discretionary company

- Lacking free cash flow limits its freedom to invest in growth initiatives, execute share buybacks, or pay dividends

- Below-average returns on capital indicate management struggled to find compelling investment opportunities

Churchill Downs’s quality doesn’t meet our expectations. We believe there are better businesses elsewhere.

Why There Are Better Opportunities Than Churchill Downs

At $86.39 per share, Churchill Downs trades at 12.6x forward P/E. This multiple is cheaper than most consumer discretionary peers, but we think this is justified.

We’d rather pay up for companies with elite fundamentals than get a bargain on weak ones. Cheap stocks can be value traps, and as their performance deteriorates, they will stay cheap or get even cheaper.

3. Churchill Downs (CHDN) Research Report: Q4 CY2025 Update

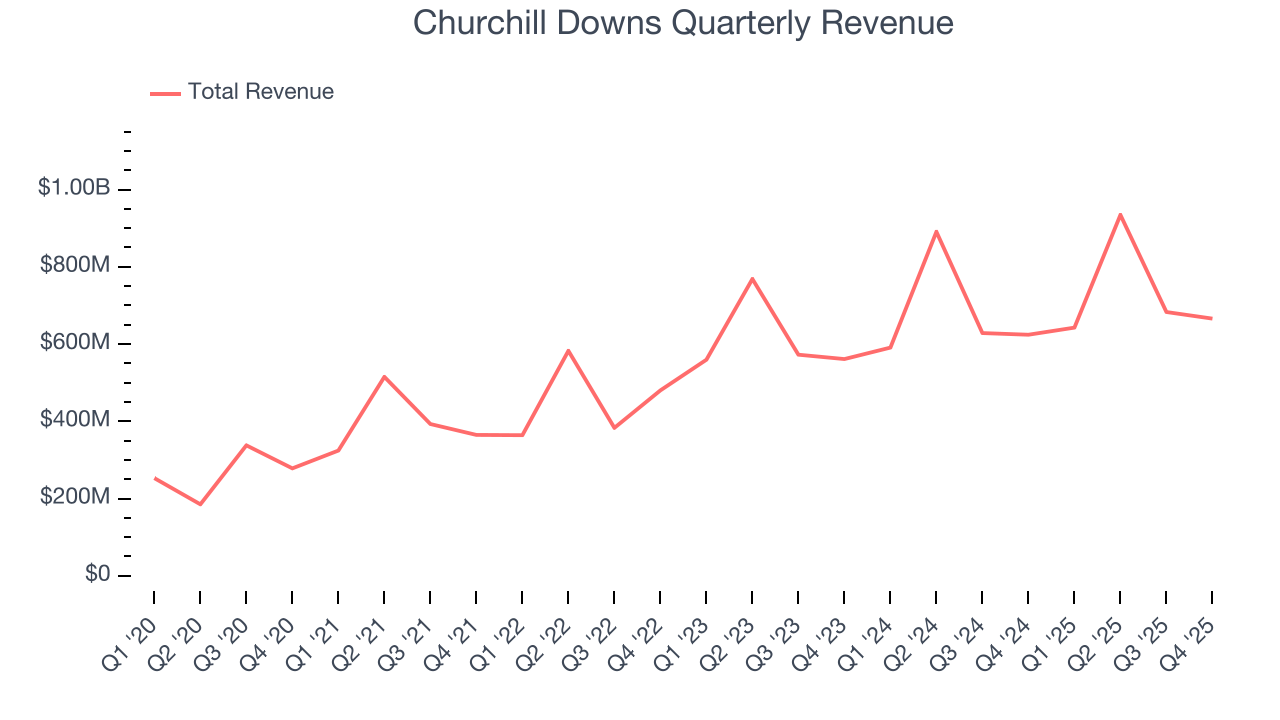

Racing, gaming, and entertainment company Churchill Downs (NASDAQ:CHDN) reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 6.7% year on year to $665.9 million. Its non-GAAP profit of $0.97 per share was 5.4% below analysts’ consensus estimates.

Churchill Downs (CHDN) Q4 CY2025 Highlights:

- Revenue: $665.9 million vs analyst estimates of $661.4 million (6.7% year-on-year growth, 0.7% beat)

- Adjusted EPS: $0.97 vs analyst expectations of $1.03 (5.4% miss)

- Adjusted EBITDA: $247 million vs analyst estimates of $245.8 million (37.1% margin, in line)

- Operating Margin: 18.5%, down from 20.3% in the same quarter last year

- Free Cash Flow Margin: 17.4%, up from 0.2% in the same quarter last year

- Market Capitalization: $6.71 billion

Company Overview

Famous for hosting the Kentucky Derby, Churchill Downs (NASDAQ:CHDN) operates a horse racing, online wagering, and gaming entertainment business in the United States.

Churchill Downs was founded in 1875 with the opening of its namesake racetrack in Louisville, Kentucky, primarily to showcase the Kentucky Derby. The Derby was created to bring high-quality horse racing to the United States. The company's founding was driven by a passion for horse racing and a vision to create a premier racing event that would rival the best in the world.

Today, Churchill Downs offers a diverse range of services that extend beyond its famed horse racing events. These include online betting platforms, casino gaming, and other entertainment services. By providing a digital wagering platform, the company addresses the modern consumer's desire for accessible and convenient betting options. Additionally, its casinos offer a variety of gaming and entertainment options, catering to a broad audience.

Churchill Downs generates revenue through a mix of sources, including racetrack operations, online wagering services, and casino gaming. The company's business model is based on leveraging the iconic status of its horse racing events while diversifying into digital gaming and casinos. This strategy capitalizes on the traditional appeal of horse racing and also adapts to changing consumer preferences in the entertainment and gaming industries.

4. Consumer Discretionary - Gaming Solutions

The Consumer Discretionary sector, by definition, is made up of companies selling non-essential goods and services. When economic conditions deteriorate or tastes shift, consumers can easily cut back or eliminate these purchases. For long-term investors with five-year holding periods, this creates a structural challenge: the sector is inherently hit-driven, with low switching costs and fickle customers. As a result, only a handful of companies can reliably grow demand and compound earnings over long periods, which is why our bar is high and High Quality ratings are rare.

Gaming solutions companies provide the technology infrastructure behind gambling—slot machines, table game systems, lottery terminals, sports-betting platforms, and back-end software for casinos and online operators. Tailwinds include the ongoing legalization of sports betting across U.S. states and international markets, growing adoption of digital and mobile wagering, and casino operators' demand for data-driven player engagement tools. However, headwinds include stringent and evolving regulatory requirements across jurisdictions, high upfront R&D costs to develop next-generation platforms, and customer concentration risk given the limited number of large casino operators. Increasing competition from in-house technology development by major operators also pressures demand.

Competitors in the gaming and horse racing industry include MGM Resorts (NYSE:MGM), Caesars Entertainment (NASDAQ:CZR), and PENN Entertainment (NASDAQ:PENN).

5. Revenue Growth

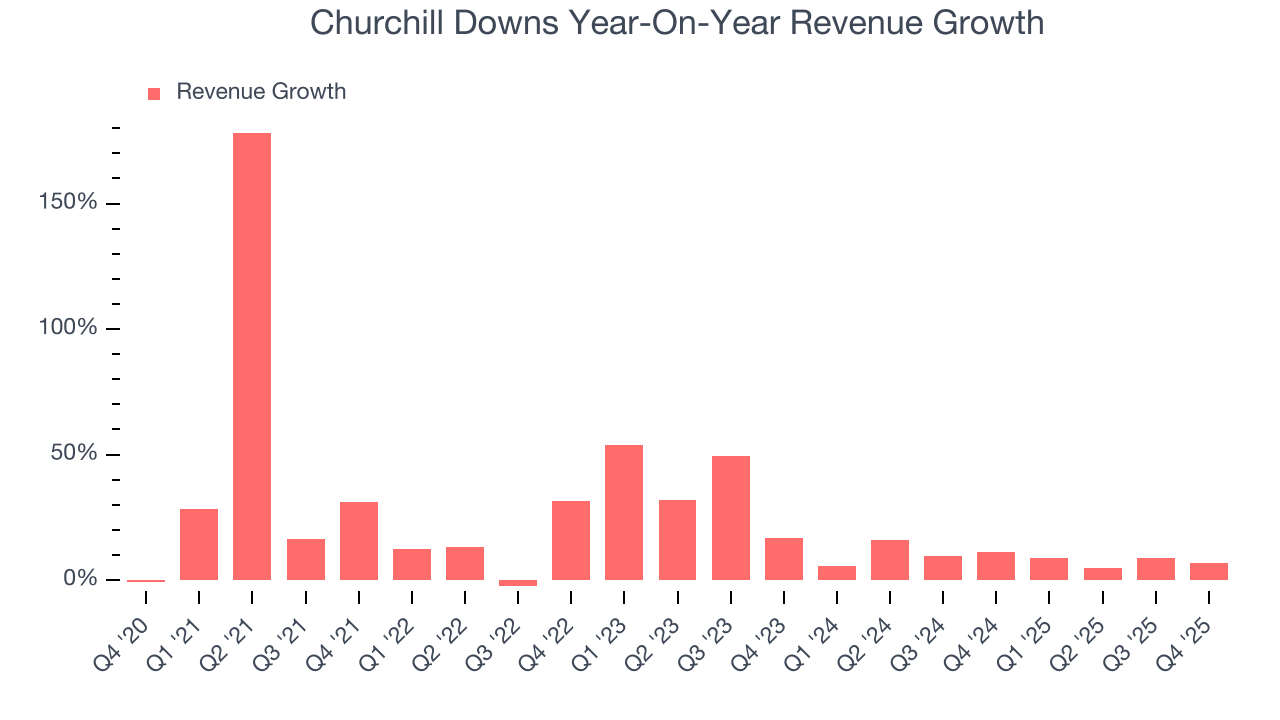

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Churchill Downs grew its sales at a 22.7% compounded annual growth rate. Though this growth is acceptable on an absolute basis, we need to see more than just topline growth for the consumer discretionary sector, which can display significant earnings volatility. This means our bar for the sector is particularly high, reflecting the non-essential and hit-driven nature of the products and services offered. Additionally, five-year CAGR starts around Covid, when revenue was depressed then rebounded.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. Churchill Downs’s recent performance shows its demand has slowed as its annualized revenue growth of 9% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

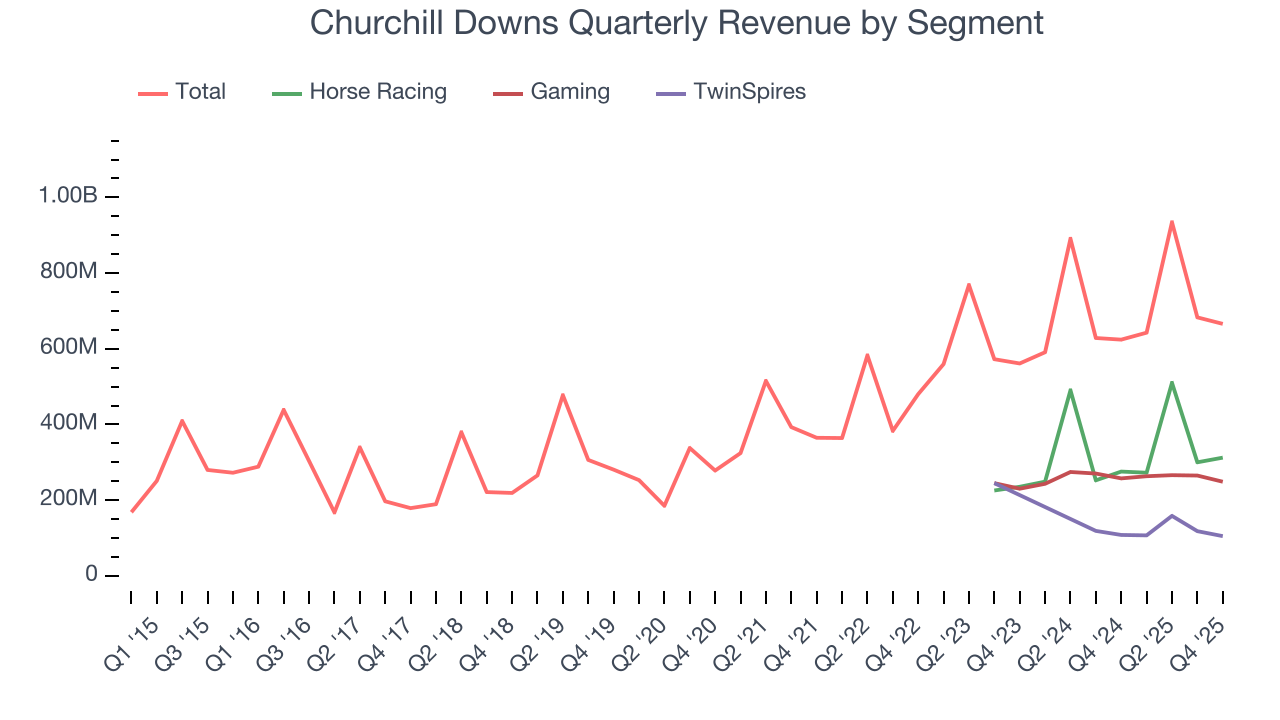

Churchill Downs also breaks out the revenue for its three most important segments: Horse Racing, Gaming, and TwinSpires, which are 46.9%, 37.3%, and 15.8% of revenue. Over the last two years, Churchill Downs’s Horse Racing (live and historical) and Gaming (casino games) revenues averaged year-on-year growth of 12.5% and 3.7% while its TwinSpires revenue (horse racing subsidiary) averaged 18.3% declines.

This quarter, Churchill Downs reported year-on-year revenue growth of 6.7%, and its $665.9 million of revenue exceeded Wall Street’s estimates by 0.7%.

Looking ahead, sell-side analysts expect revenue to grow 3.4% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and implies its products and services will face some demand challenges.

6. Operating Margin

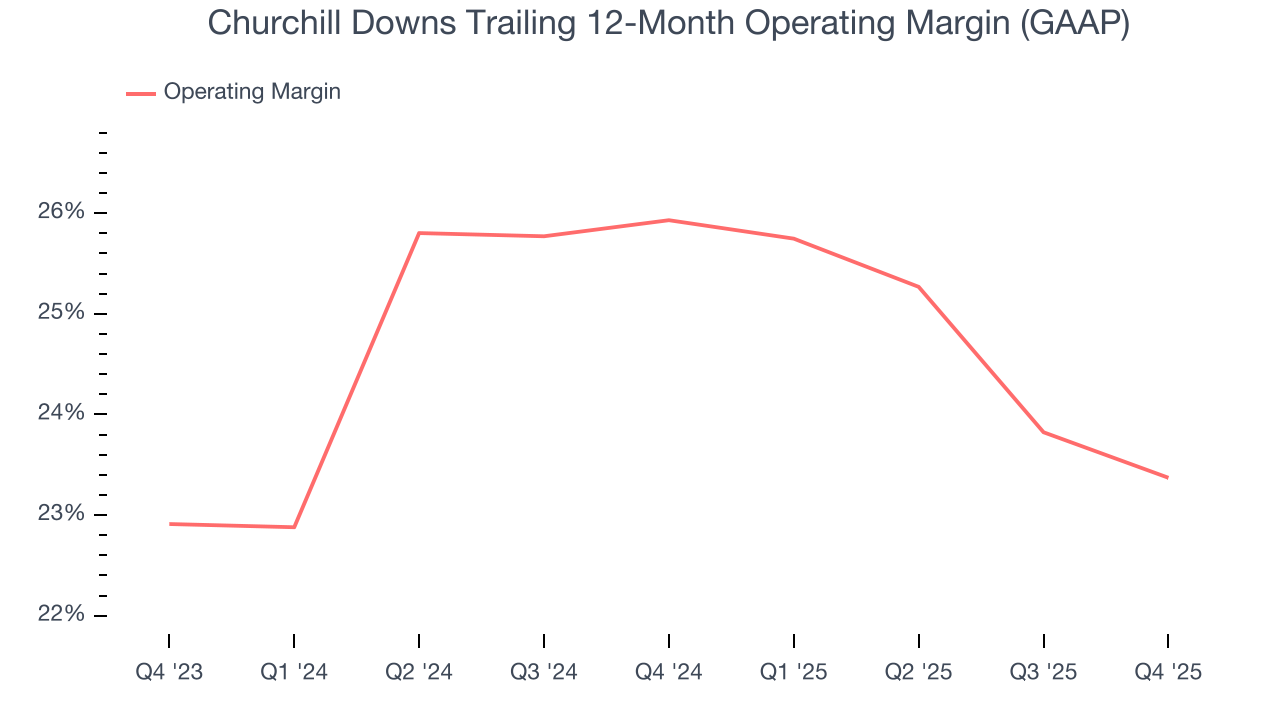

Churchill Downs’s operating margin has shrunk over the last 12 months and averaged 24.6% over the last two years. The company’s profitability was mediocre for a consumer discretionary business and shows it couldn’t pass its higher operating expenses onto its customers.

This quarter, Churchill Downs generated an operating margin profit margin of 18.5%, down 1.8 percentage points year on year. This reduction is quite minuscule and indicates the company’s overall cost structure has been relatively stable.

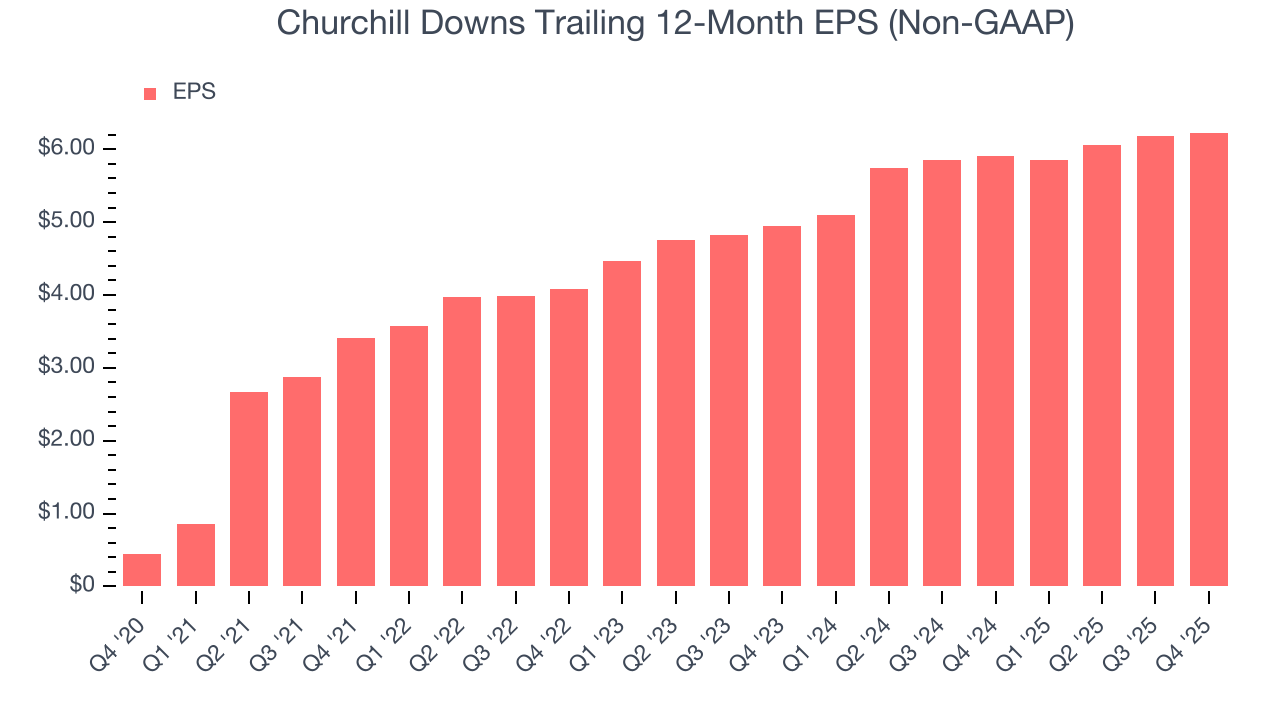

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Churchill Downs’s EPS grew at an astounding 69.1% compounded annual growth rate over the last five years, higher than its 22.7% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

In Q4, Churchill Downs reported adjusted EPS of $0.97, up from $0.92 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates, but we care more about long-term adjusted EPS growth than short-term movements. Over the next 12 months, Wall Street expects Churchill Downs’s full-year EPS of $6.23 to grow 8.6%.

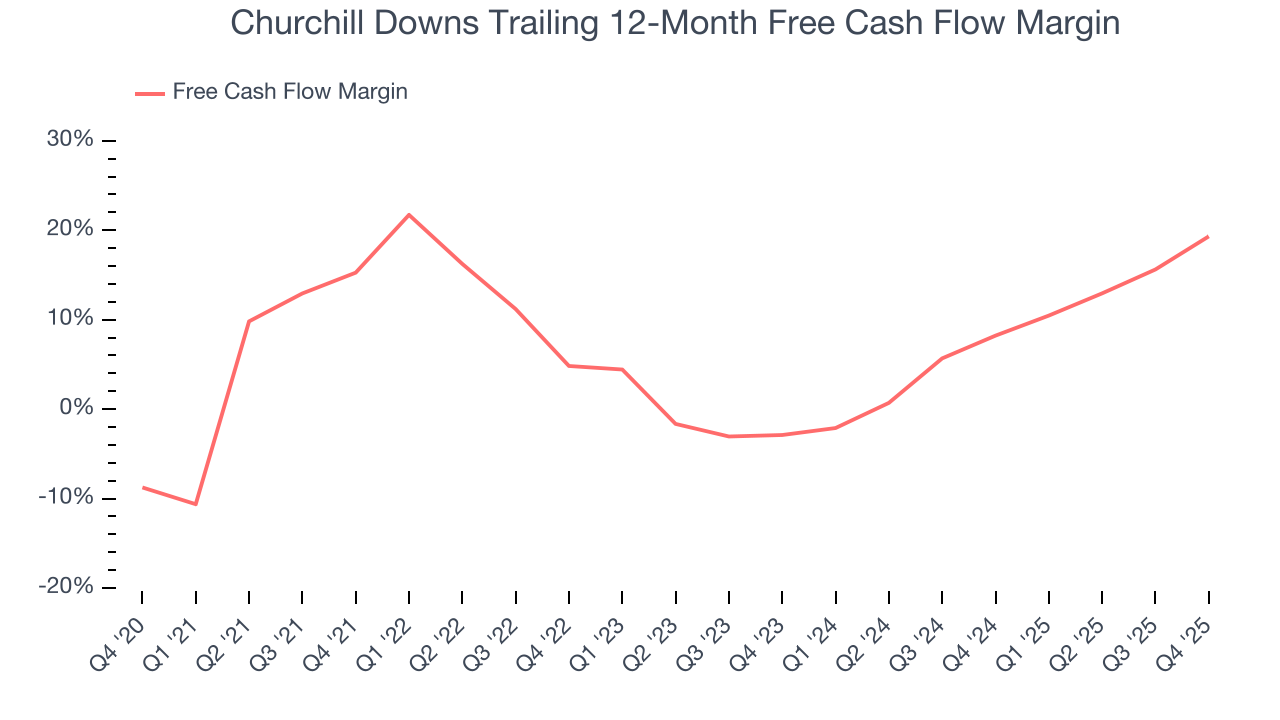

8. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Churchill Downs has shown poor cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 14%, lousy for a consumer discretionary business.

Churchill Downs’s free cash flow clocked in at $115.9 million in Q4, equivalent to a 17.4% margin. This result was good as its margin was 17.2 percentage points higher than in the same quarter last year, but we wouldn’t put too much weight on the short term because investment needs can be seasonal, causing temporary swings. Long-term trends are more important.

Over the next year, analysts predict Churchill Downs’s cash conversion will slightly fall. Their consensus estimates imply its free cash flow margin of 19.3% for the last 12 months will decrease to 17.8%.

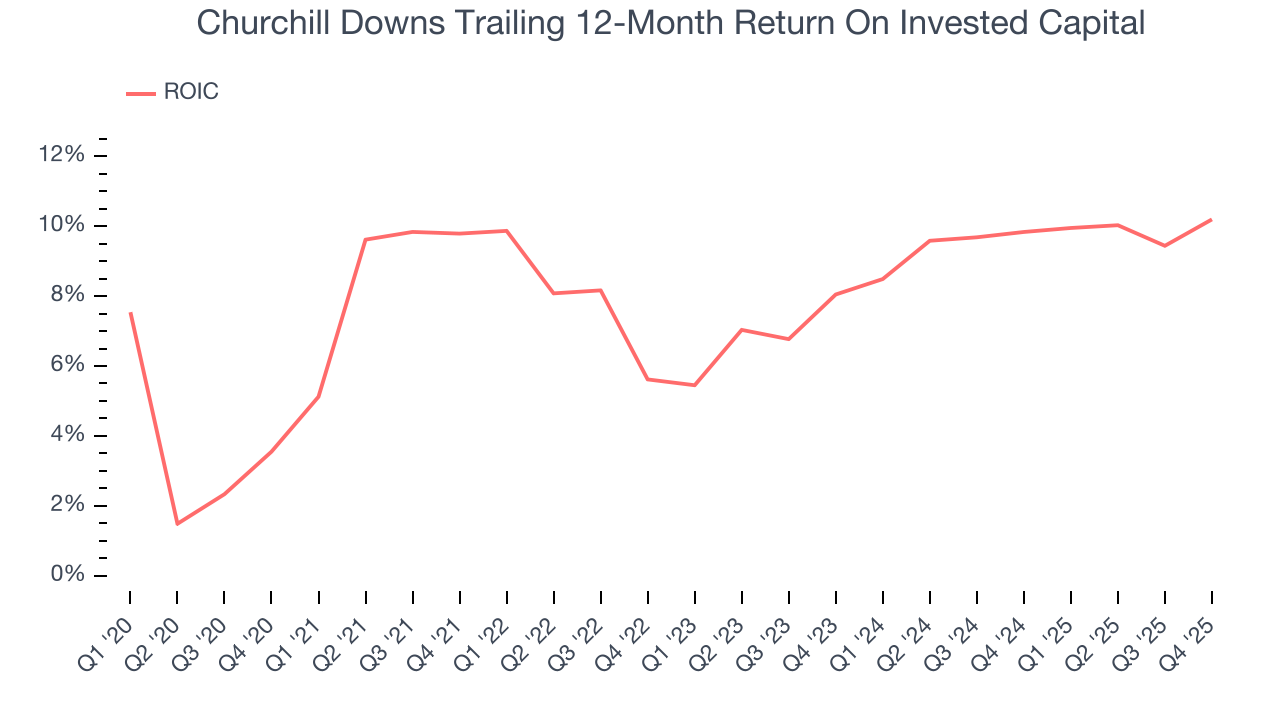

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Churchill Downs historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 8.7%, somewhat low compared to the best consumer discretionary companies that consistently pump out 25%+.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. On average, Churchill Downs’s ROIC increased by 2.3 percentage points annually each year over the last few years. This is a good sign, and we hope the company can continue improving.

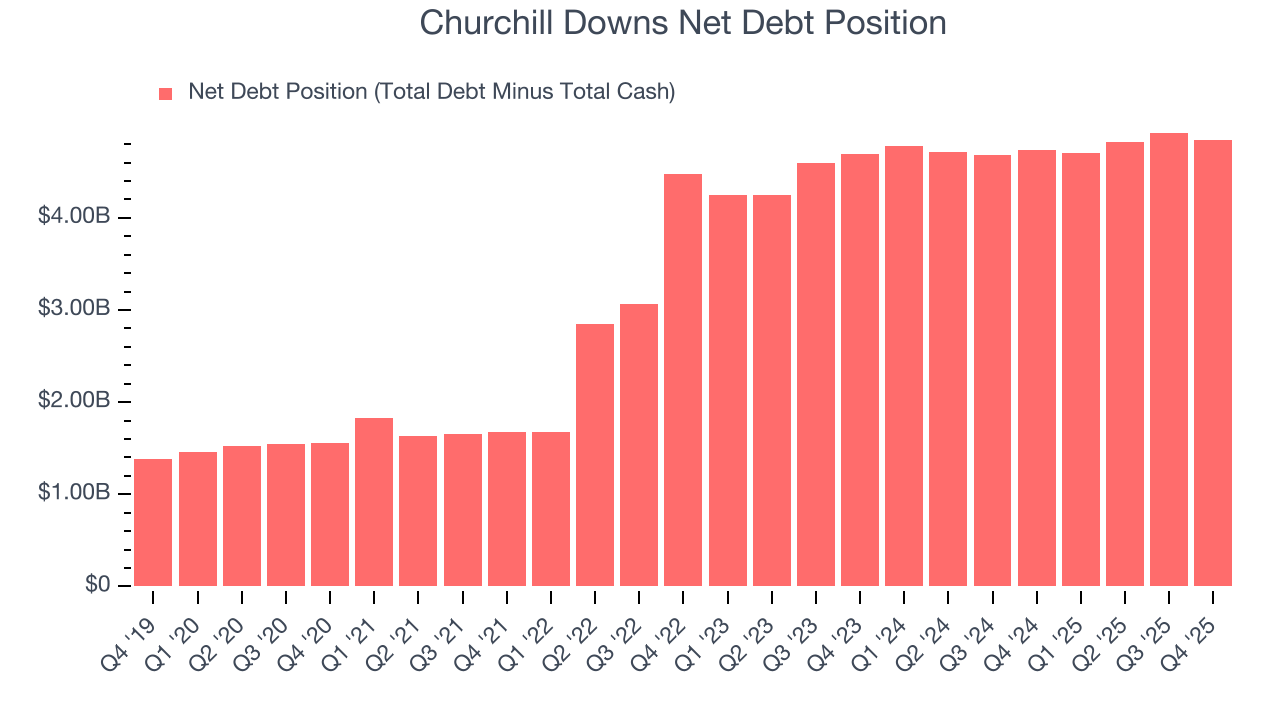

10. Balance Sheet Assessment

Churchill Downs reported $288.5 million of cash and $5.13 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $1.21 billion of EBITDA over the last 12 months, we view Churchill Downs’s 4.0× net-debt-to-EBITDA ratio as safe. We also see its $297.7 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from Churchill Downs’s Q4 Results

We struggled to find many positives in these results. Overall, this was a weaker quarter. The stock traded down 2.8% to $93.45 immediately after reporting.

12. Is Now The Time To Buy Churchill Downs?

Updated: March 15, 2026 at 11:04 PM EDT

Before investing in or passing on Churchill Downs, we urge you to understand the company’s business quality (or lack thereof), valuation, and the latest quarterly results - in that order.

Churchill Downs falls short of our quality standards. While its astounding EPS growth over the last five years shows its profits are trickling down to shareholders, the downside is its Forecasted free cash flow margin for next year suggests the company will fail to improve its cash conversion. On top of that, its projected EPS for the next year is lacking.

Churchill Downs’s P/E ratio based on the next 12 months is 12.6x. This valuation is reasonable, but the company’s shaky fundamentals present too much downside risk. There are superior stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $135.50 on the company (compared to the current share price of $86.39).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.