Clarus (CLAR)

Clarus faces an uphill battle. Its poor sales growth shows demand is soft and its negative returns on capital suggest it destroyed value.― StockStory Analyst Team

1. News

2. Summary

Why We Think Clarus Will Underperform

Initially a financial services business, Clarus (NASDAQ:CLAR) designs, manufactures, and distributes outdoor equipment and lifestyle products.

- Lackluster 2.3% annual revenue growth over the last five years indicates the company is losing ground to competitors

- Incremental sales over the last five years were much less profitable as its earnings per share fell by 33.5% annually while its revenue grew

- Poor expense management has led to operating margin losses

Clarus’s quality isn’t great. More profitable opportunities exist elsewhere.

Why There Are Better Opportunities Than Clarus

Clarus is trading at $2.76 per share, or 17.3x forward P/E. While valuation is appropriate for the quality you get, we’re still not buyers.

There are stocks out there similarly priced with better business quality. We prefer owning these.

3. Clarus (CLAR) Research Report: Q4 CY2025 Update

Outdoor lifestyle and equipment company Clarus (NASDAQ:CLAR) fell short of the market’s revenue expectations in Q4 CY2025, with sales falling 8.4% year on year to $65.41 million. The company’s full-year revenue guidance of $260 million at the midpoint came in 1.1% below analysts’ estimates. Its non-GAAP profit of $0.09 per share was 38.5% above analysts’ consensus estimates.

Clarus (CLAR) Q4 CY2025 Highlights:

- Revenue: $65.41 million vs analyst estimates of $68.88 million (8.4% year-on-year decline, 5% miss)

- Adjusted EPS: $0.09 vs analyst estimates of $0.07 (38.5% beat)

- Adjusted EBITDA: $1.17 million vs analyst estimates of $4.28 million (1.8% margin, 72.6% miss)

- EBITDA guidance for the upcoming financial year 2026 is $10 million at the midpoint, above analyst estimates of $9.36 million

- Operating Margin: -59.6%, up from -70.2% in the same quarter last year

- Market Capitalization: $121.7 million

Company Overview

Initially a financial services business, Clarus (NASDAQ:CLAR) designs, manufactures, and distributes outdoor equipment and lifestyle products.

The company was founded in 1991, but after recognizing the potential of the outdoor equipment market, pivoted to meet the needs of adventure enthusiasts in 2002.

Today, Clarus offers products across several brands, including Black Diamond Equipment, Sierra Bullets, PIEPS, and SKINourishment. Its brands sell goods such as advanced climbing gear, ski equipment, precision ammunition, and skincare products tailored for outdoor environments.

Clarus generates revenue through a multi-faceted approach, leveraging a direct salesforce, extensive retail partnerships, and an e-commerce platform to sell its products. This strategy allows the company to reach a diverse and global consumer base.

4. Consumer Discretionary - Leisure Products

The Consumer Discretionary sector, by definition, is made up of companies selling non-essential goods and services. When economic conditions deteriorate or tastes shift, consumers can easily cut back or eliminate these purchases. For long-term investors with five-year holding periods, this creates a structural challenge: the sector is inherently hit-driven, with low switching costs and fickle customers. As a result, only a handful of companies can reliably grow demand and compound earnings over long periods, which is why our bar is high and High Quality ratings are rare.

Leisure products companies manufacture recreational goods such as bicycles, marine vessels, fitness equipment, camping gear, and musical instruments. Tailwinds include heightened outdoor-activity participation, health-and-wellness awareness, and periodic innovation cycles that drive trade-up purchases. Headwinds are pronounced: demand is highly discretionary and sensitive to economic cycles—consumers readily defer big-ticket leisure purchases during downturns. Post-pandemic normalization has created excess channel inventory after demand surged then retreated. Raw-material and shipping cost inflation squeezes margins, while competition from low-cost imports and a fragmented market make pricing power elusive for most players.

Select competitors in the outdoor and recreation space include The North Face (owned by NYSE:VFC), Johnson Outdoors (NASDAQ:JOUT), and Smith & Wesson (NASDAQ:SWBI).

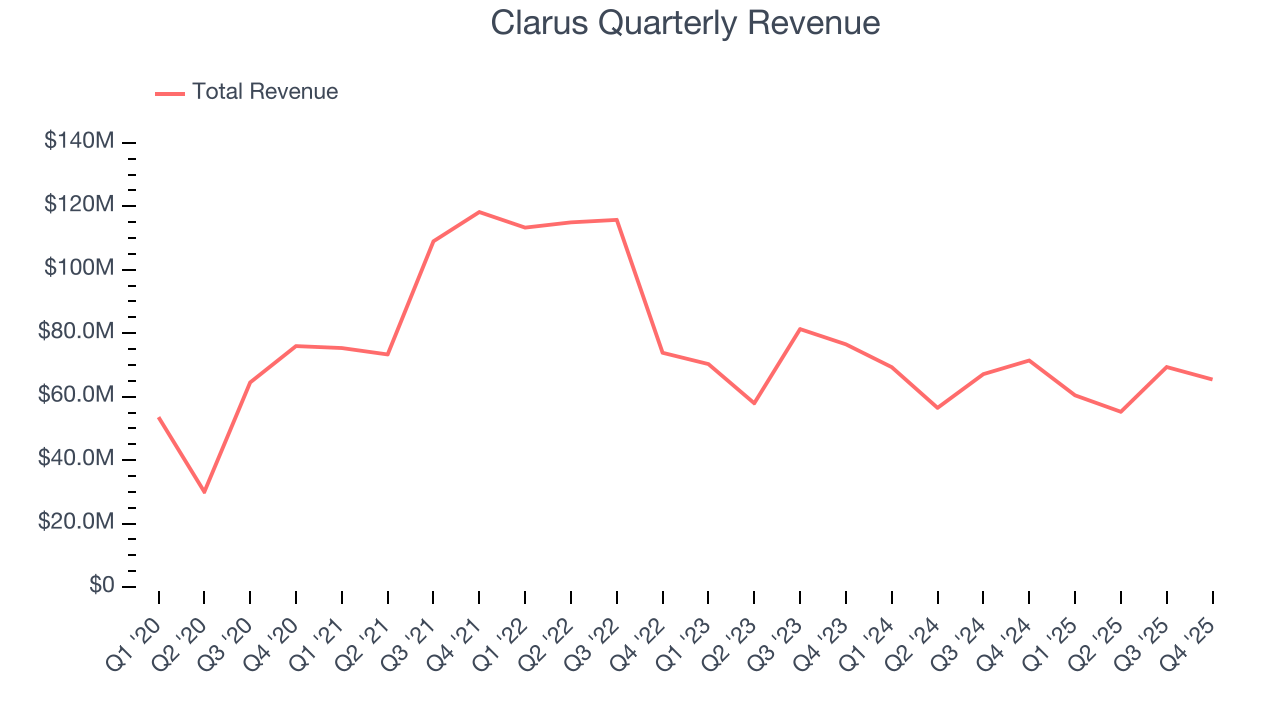

5. Revenue Growth

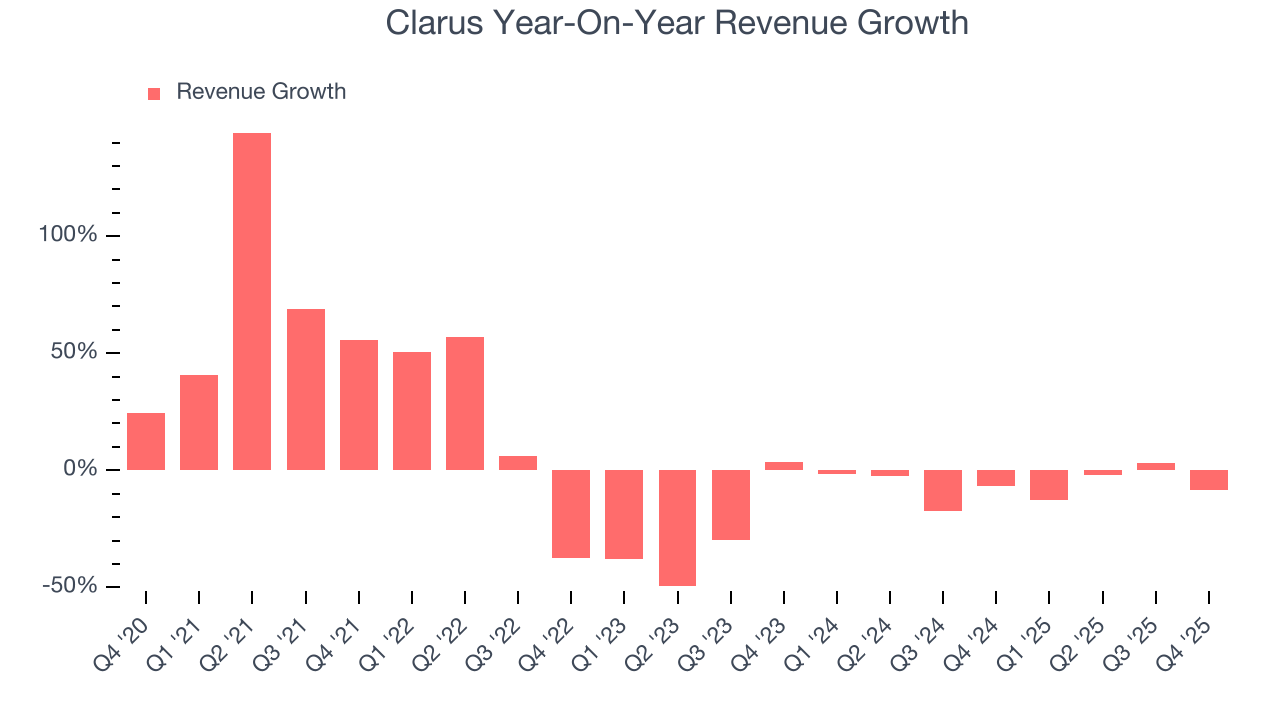

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, Clarus grew its sales at a weak 2.3% compounded annual growth rate. This fell short of our benchmarks and is a rough starting point for our analysis.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Clarus’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 6.4% annually.

This quarter, Clarus missed Wall Street’s estimates and reported a rather uninspiring 8.4% year-on-year revenue decline, generating $65.41 million of revenue.

Looking ahead, sell-side analysts expect revenue to grow 5.6% over the next 12 months. While this projection suggests its newer products and services will spur better top-line performance, it is still below average for the sector.

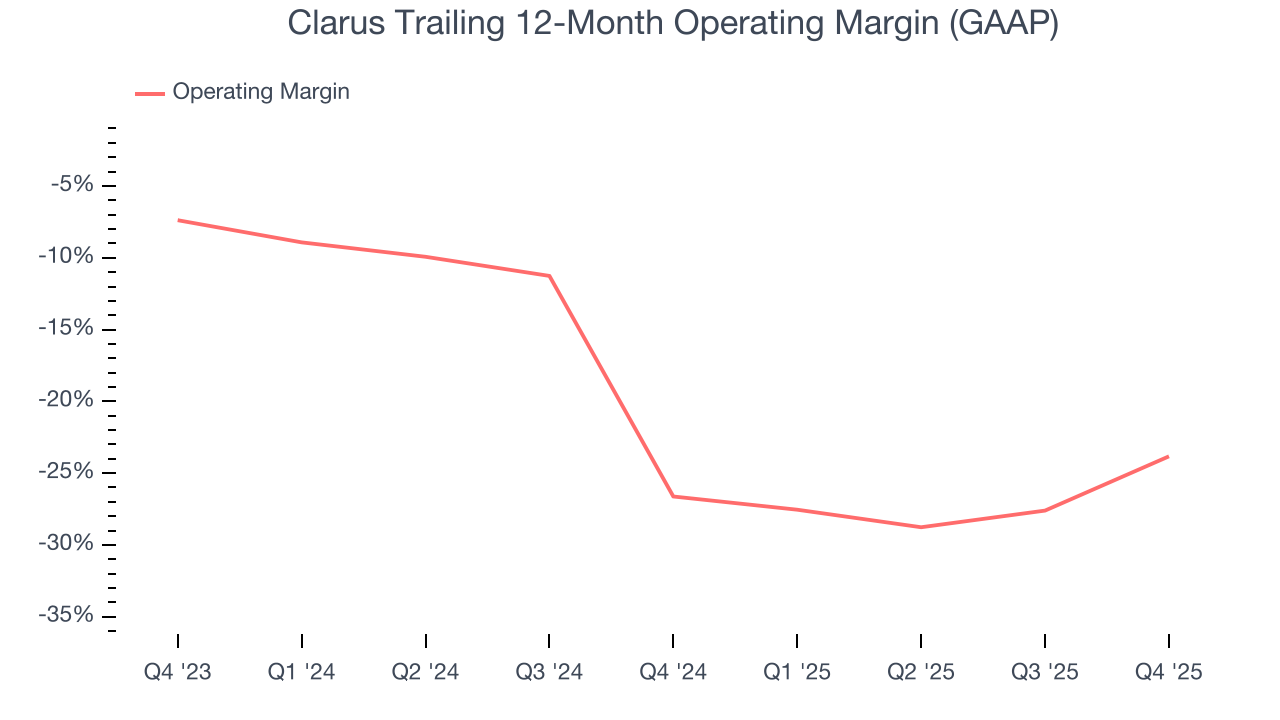

6. Operating Margin

Clarus’s operating margin has risen over the last 12 months, but it still averaged negative 25.3% over the last two years. This is due to its large expense base and inefficient cost structure.

This quarter, Clarus generated a negative 59.6% operating margin. The company's consistent lack of profits raise a flag.

7. Earnings Per Share

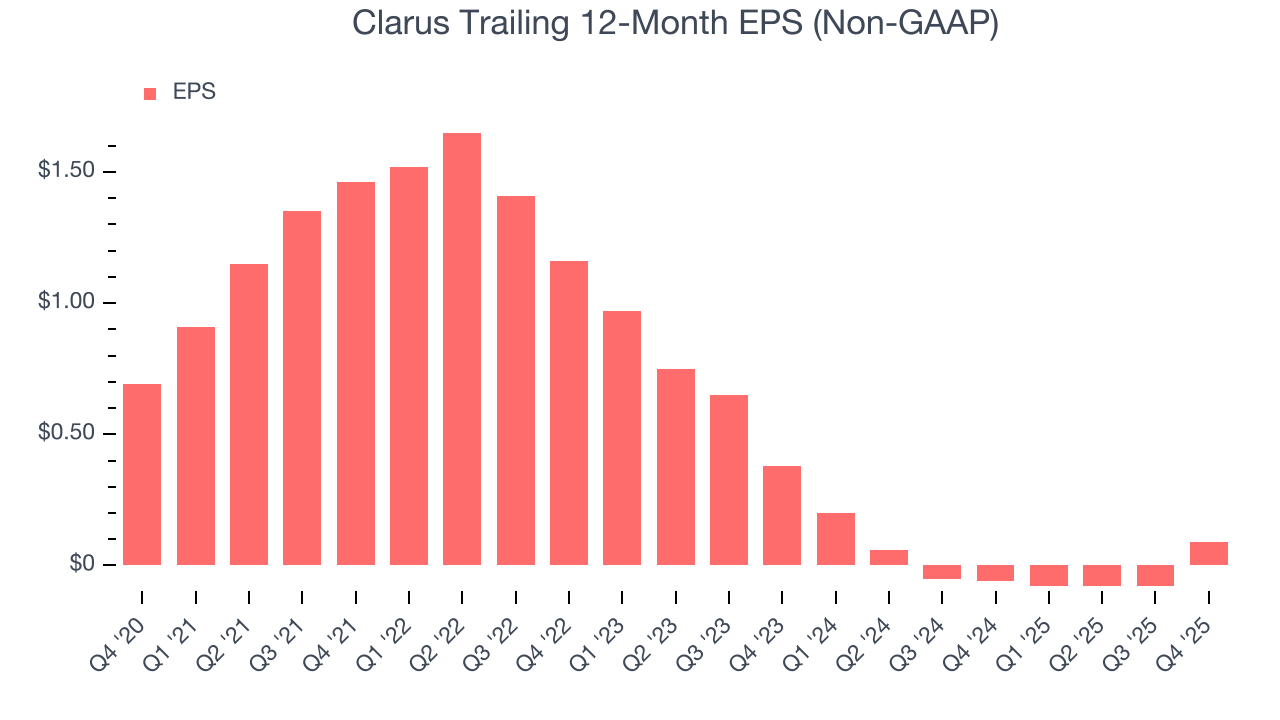

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Clarus, its EPS declined by 33.5% annually over the last five years while its revenue grew by 2.3%. This tells us the company became less profitable on a per-share basis as it expanded.

In Q4, Clarus reported adjusted EPS of $0.09, up from negative $0.08 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Clarus’s full-year EPS of $0.09 to grow 92.6%.

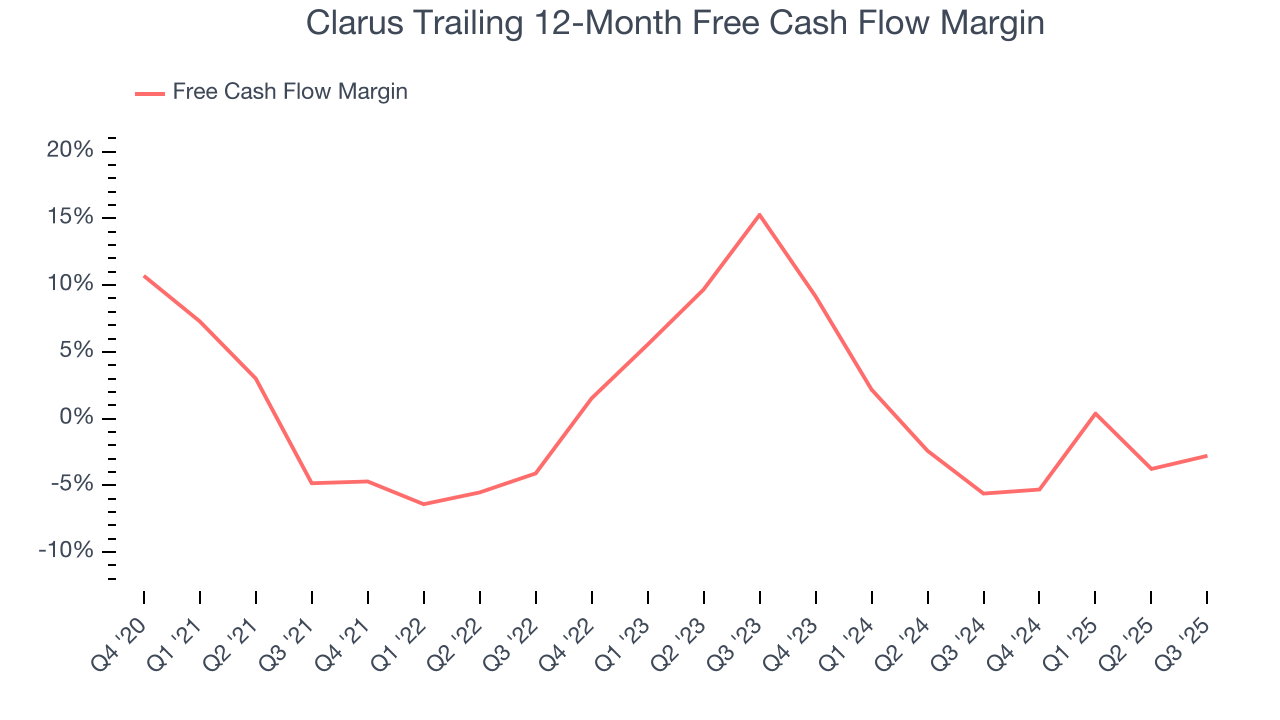

8. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Over the last two years, Clarus’s demanding reinvestments to stay relevant have drained its resources, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 7.9%, meaning it lit $7.91 of cash on fire for every $100 in revenue.

9. Return on Invested Capital (ROIC)

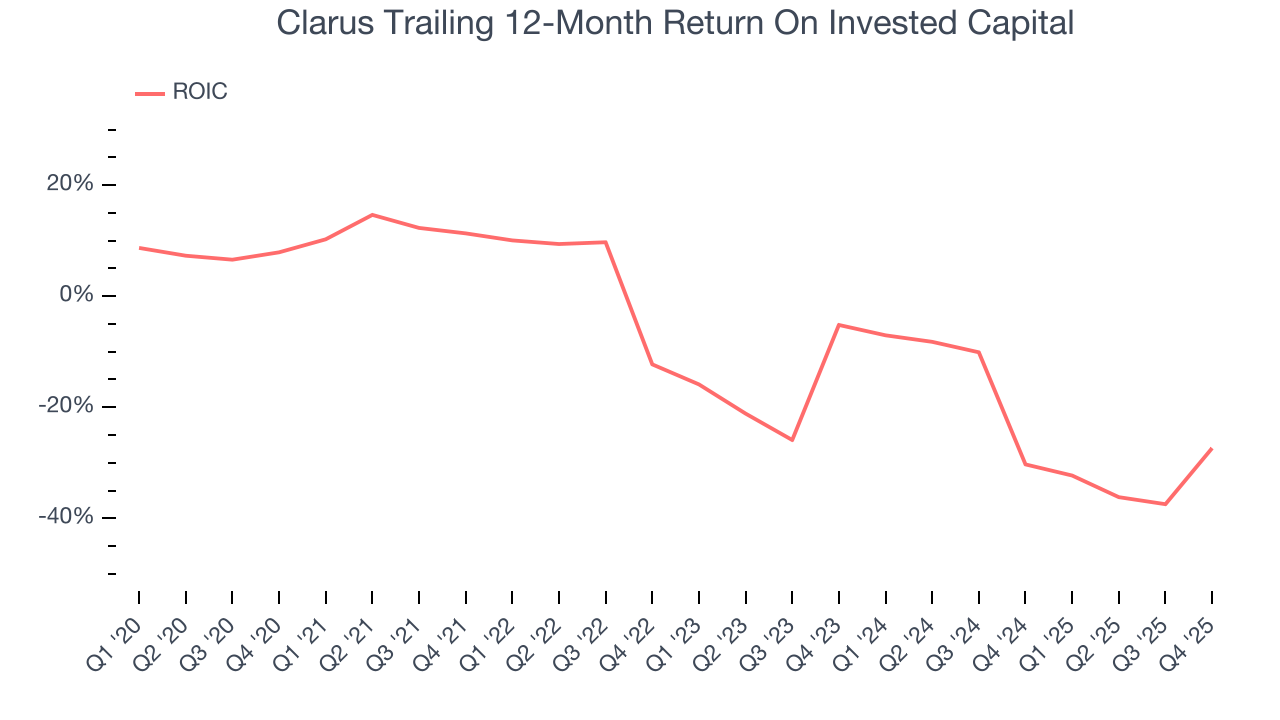

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Clarus’s five-year average ROIC was negative 12.8%, meaning management lost money while trying to expand the business. Its returns were among the worst in the consumer discretionary sector.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Clarus’s ROIC has unfortunately decreased significantly. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

10. Balance Sheet Assessment

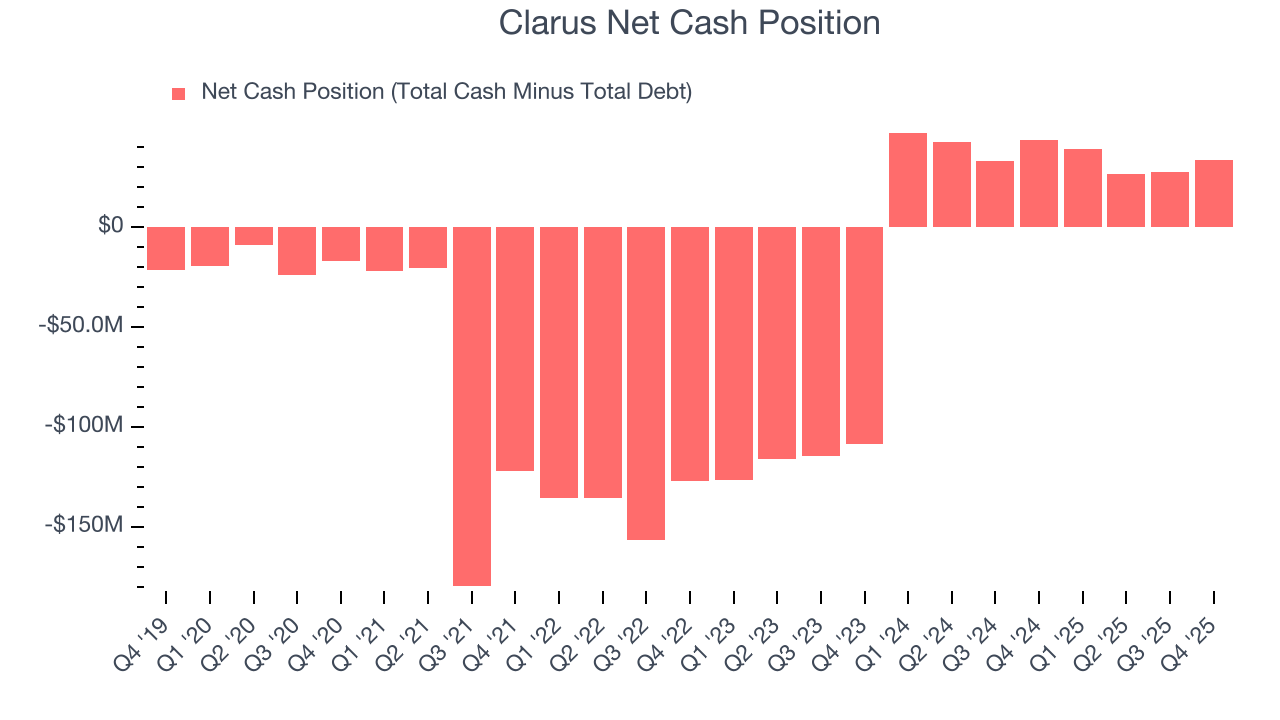

Companies with more cash than debt have lower bankruptcy risk.

Clarus is a well-capitalized company with $36.69 million of cash and $3.02 million of debt on its balance sheet. This $33.67 million net cash position is 29.3% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

11. Key Takeaways from Clarus’s Q4 Results

It was good to see Clarus beat analysts’ EPS expectations this quarter. We were also glad its full-year EBITDA guidance exceeded Wall Street’s estimates. On the other hand, its revenue missed and its EBITDA fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 2.8% to $3.01 immediately after reporting.

12. Is Now The Time To Buy Clarus?

Updated: March 15, 2026 at 10:58 PM EDT

We think that the latest earnings result is only one piece of the bigger puzzle. If you’re deciding whether to own Clarus, you should also grasp the company’s longer-term business quality and valuation.

We cheer for all companies serving everyday consumers, but in the case of Clarus, we’ll be cheering from the sidelines. While its projected EPS for the next year implies the company’s fundamentals will improve, the downside is its declining EPS over the last five years makes it a less attractive asset to the public markets. On top of that, its relatively low ROIC suggests management has struggled to find compelling investment opportunities.

Clarus’s P/E ratio based on the next 12 months is 17.3x. This valuation multiple is fair, but we don’t have much confidence in the company. There are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $3.85 on the company (compared to the current share price of $2.76).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.